The community development movement in the United States has stepped into markets where economic and social disadvantage co-exist. One of the primary objectives in our recent monograph, Community Economic Development in the United States: The CDFI Industry and America’s Distressed Communities (New York: Palgrave, 2017), was to examine the differences between the lending activities of mainstream financial institutions and that of two critical elements in the community development industry in the United States—Community Development Financial Institutions (CDFIs) as well as the array of financial actors in the New Market Tax Credit (NMTC) industry. While in our monograph, we analyzed both tax expenditures and community development versus mainstream financial institution investment activity at a national scale, here we examine these data solely for the Seventh Federal Reserve Bank District, an area comprising the entirety of Iowa, and much of Illinois, Wisconsin, Indiana, and Michigan.

There are numerous reasons why economic development lags, sometimes severely, in some of the nation’s communities. America’s inner city neighborhoods, much of the rural landscape, and not an insignificant proportion of the inner ring of suburbs in the nation’s metropolitan areas suffer from diminished economic development and investment due to numerous causes that (often) amplify one another. We identify four such sources of what economists refer to as "market failures."

First is the uneven development and obsolescence of much of the "built environment" – the totality of the basic infrastructural system (the streets, utility systems, rail lines, etc.), also comprising offices, manufacturing plants, warehousing facilities, and most importantly, housing. The decay of the built environment in some areas is especially relevant to their distress, but also to growth elsewhere in their regions. As the needs of the economy and housing tastes change, the tendency has been to build new housing and facilities on the fringes of cities and, increasingly, the edges of metropolitan areas. Over time, especially since the end of World War II, the cores of inner cities were largely abandoned by companies, families, and financial institutions, and economic and population growth moved to outlying suburbs. Since most elements of the nation’s built environment are fixed in place, obsolescence takes root in places where reinvestment, redevelopment, or repurposing does not. This trend has served to isolate, socially and economically, many urban areas, and led to abandonment by businesses and families from increasingly blighted communities.2

Second, federal housing policy, especially policies adopted in response to the economic crisis of the Great Depression, dramatically undermined the housing markets of America’s cities and rural communities. The Federal Housing Act of 1934 created government-funded mortgage insurance and a new agency – the Federal Housing Administration (FHA) – to administer this new and untested tool. The goal was to stabilize the American housing market, which had been in decline since the mid-1920s and in free-fall after the stock market crash in October 1929. Under the Act, only long-term, low interest rate, fully amortizing3 mortgages were eligible for federally sponsored mortgage insurance. The FHA developed and promulgated its underwriting manuals (1935, 1936, and 1938) that dictated the standards in extraordinary detail which were required for a home to qualify for mortgage insurance. For instance, an eligible house had to have not less than three bedrooms, a separate kitchen and living room, windows for each room, full indoor plumbing, and a heating system; and sleeping quarters could not be in cellars or attics. Minimum construction standards had to be meticulously followed and inspected by FHA personnel. A large proportion of the standing housing in the mid-1930s could not meet these standards and were consequently not eligible for mortgage insurance. Perhaps two-thirds to three-quarters of all housing at that time were disqualified from the new mortgage insurance program. Furthermore, these FHA underwriting manuals were dictatorial regarding the social and racial/ethnic characteristics of neighborhoods where mortgage insurance could be issued.

With the implementation of mortgage insurance, especially during the 1950s and 1960s when housing development was explosive (and largely confined to new suburban subdivisions), the FHA was both successful in facilitating the massive expansion and upgrading of the nation's housing stock, albeit for white homeowners exclusively.4 It was also a contributing factor – given the prohibition on insuring mortgages for older housing – to inner city and rural disinvestment.5

Third, public investment strategies (and concentrations of tax expenditures) exacerbate and reinforce patterns of uneven economic development. American metropolitan areas are highly fragmented into literally hundreds of municipalities that vary notably in terms of social class, housing price, and commerce; policymakers and scholars have recognized that many individual localities have neither the ability nor the will to provide adequate public goods and services.6 Predictably, wealthy suburban localities have the capacity to provide very high quality schools, parks, and public services while poor and moderate income suburban municipalities have a significantly lower tax base and thereby less ability to provide similar quality public goods and services. Even within large central cities, geographers have documented unequal provision of public goods across neighborhoods, the effect of which is to provide the underpinnings for development in wealthier neighborhoods and undermining those impacted by long-term disinvestment in public goods and services.7

Finally, a shortage of data impedes credit flow to some communities. Mortgage lending volume, we have noted, has historically (and largely continues to be) skewed towards newer or re-developing housing markets, supporting the economic health of high- and middle-income areas. For consumer financial services and small business lending, banks are guided by both regulatory parameters and profit opportunities. However, banks and other financial institutions make lending decisions increasingly on the basis of credit scores and an array of data about individuals and businesses. More established communities once again enjoy an advantage; the data for wealthier places tends to be more detailed and more readily available. In less wealthy communities, that have historically experienced less lending, there is little information upon which banks or other financial institutions can make lending decisions. There might be significant demand and need for loans in poorer communities, but with limited credit histories and other pertinent financial data, depository institutions tend to avoid such areas.

The activities of the community development industry in the Seventh Federal Reserve District

In central city low-income (and frequently minority) communities, as well as in many rural areas, the CDFI industry provides financial services and makes many loans and investments in communities that have been for decades in the backwaters of economic and social development across the country. CDFIs and Community Development Entities (CDEs using tax credits in the NMTC program) foster economic and housing development in some of the most challenging areas of the US communities.

While here we only provide an abbreviated version of a more systematic and detailed investigation of the portfolios of the many CDFIs and CDEs, the main outlines of our findings provided in chapters 4 and 5 of our monograph can be quickly summarized, noting once again these observations relate solely to the Chicago Fed District. Our findings are quite striking: the community development industry has, over the past several years, successfully made extensive investments in some of the most distressed communities: very low- and low-income areas, impoverished communities, and places that are largely occupied by minorities, including Native Americans. Indeed, compared to the investments of mainstream financial institutions, CDFIs and CDEs have focused their investments into highly troubled communities – across the country, and in the Midwest communities of the Seventh District.

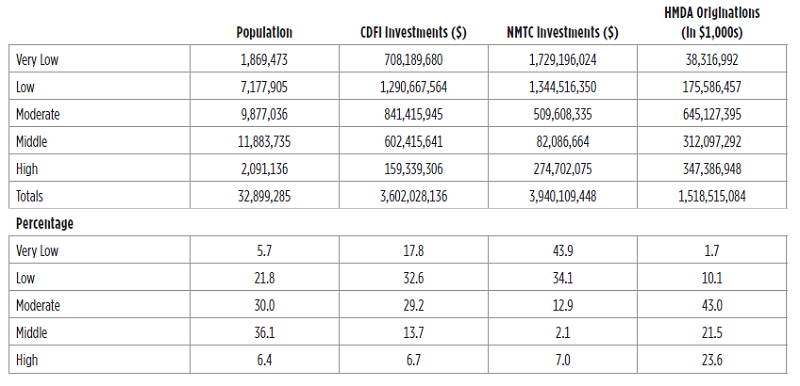

Table 1 provides a summary of both the magnitude and differences between the investments made by mainstream financial institutions and the CDFI and NMTC industry in Midwest communities served by the Federal Reserve Bank of Chicago. In this table, we aggregate investments by the median family income of census tracts providing the total population (in 2000) of tracts by income and then sequentially the total dollars in home mortgages, home improvements, and refinancing by mainstream financial institutions using the Home Mortgage Disclosure Act (HMDA) data, as well as transaction information on CDFIs and CDEs (under the NMTC program) derived from CIIS data collected and annually published by the CDFI Fund.

Table 1. Community development and mainstream investments, by income of census tract, Federal Reserve Seventh District, 2006-2010

As would be expected, given the mandate of the CDFI Fund, CDFIs and CDEs have invested primarily in very low- and low-income tracts in both urban and rural areas. In contrast, mainstream financial institutions have consistently concentrated their investments in middle and upper income communities. The contrasts are marked: whereas banks, mortgage companies, and other mainstream financial institutions have invested barely 12 percent in very low- and low-income communities, CDFIs have in contrast made over 50 percent of their overall investments in these communities and CDEs under the NMTC program nearly 80 percent of their investments in very low- and low-income neighborhoods. Nearly one-quarter of all HMDA investments were concentrated in these highest income tracts (where median family income was 200 percent or more of area median income) while a very small proportion of CDFI and NMTC investments (6.7 percent and 7.0 percent respectively) were located in these affluent areas.

The data presented on this first table also highlights another fact: the total amount of loans and investments made by mainstream financial institutions dwarfs that of the community development industry. Namely, the total dollar amount of home mortgages, home improvement, and refinancing loans over the five-year period reported here (2006-2010) sums to over $1.5 trillion while CDFI investments total $3.6 billion and the NMTC program over $3.9 billion. While over $7.5 billion in community development is a substantial amount, it pales in comparison to the investments made by mainstream financial institutions. As a result, community development lending can only be expected to provide a modest engine of economic and housing development to the nation's economically distressed communities. Policies that could even modestly divert the resources of banks and other regulated financial institutions to distressed regions would likely spur economic growth in those communities.

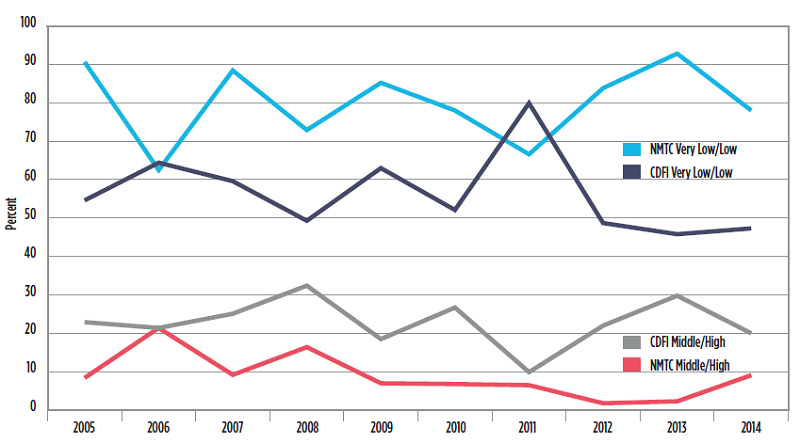

A brief examination of the lending behavior of the community development industry in contrast to that of mainstream financial institutions over the decade from 2005 through 2014 shown in figures 1 and 2 again highlight the differences in table 1. In both figures, we show, not the total dollar amount of investment, but rather the percentage of the total dollar investment for respectively, CDFIs, CDEs, and finally mainstream financial institutions in very low- and low- income tracts, as well as the percentage of total investments in high- and very high-income tracts. Figure 1 displays community development investment over this decade and demonstrates that both CDFI and especially NMTC lending was consistently concentrated in very low- and low-income communities in the Federal Reserve's Seventh District: for CDFIs, loans and investments were generally concentrated in poor areas, and NMTC investments were consistently higher in distressed communities. Additionally, throughout this decade, both CDFIs and CDEs made a consistently low proportion of their investments in more affluent communities in the Seventh Federal Reserve District. Finally, there is little discernible effect of the Great Recession on community development lending via the CDFI Fund.

Figure 1. Percentage of community development lending in very low- and low- and middle- and high-income tracts, Seventh District, 2005-2014

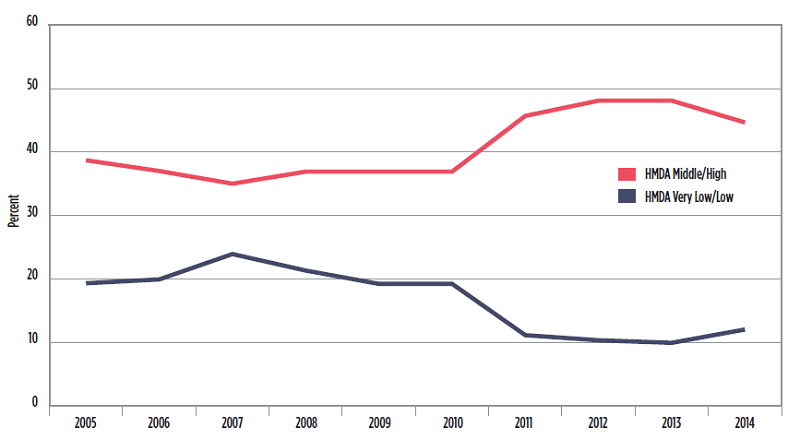

The home lending activities (using HMDA data) of mainstream financial institutions (figure 2) over this same period differ starkly as we would expect given the findings presented in table 1. Not only, as expected, is the total amount of HMDA-reported home lending by banks, credit unions, and other regulated financial institutions consistently concentrated in more affluent areas, the effects of the Great Recession are quite prominent. Namely, as the crisis unfolded, mainstream financial institutions simultaneously increased their home mortgage investments into middle and upper income tracts while diminishing housing investments in low-income communities.

Figure 2. Percentage of mainstream financial institution's home mortgage originations, by very low- and low-income, and middle- and high-income tracts, Seventh Federal Reserve District, 2005-2014

A last area we want to highlight, and this was the topic we examined at length in chapter 4 of our monograph, is tax expenditures. Tax expenditures or tax credits are as old as the American tax code. Beginning with the creation of an income tax system, homeowners were permitted to deduct the interest on their mortgage payments. Initially this was a small portion of the federal budget, but over the past century, the use of such incentives has become an ever larger and permanent feature of American fiscal policy. Tax incentives are now used to reduce the cost of local property taxes, to provide child care, to enhance the production of low-income rental housing, to encourage education, underwrite the use of alternative and sustainable forms of energy, to provide an income floor for low-income workers, and to enhance the development and expansion of businesses and encourage commercial developments in low-income areas under the New Markets Tax Credit Program.

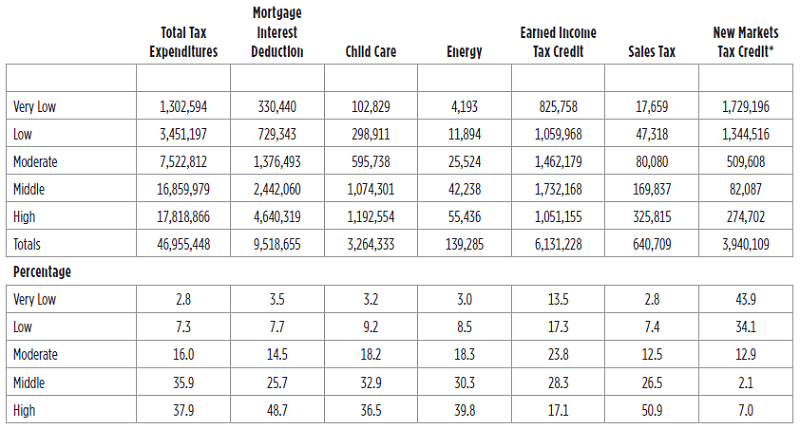

Table 2 provides an abbreviated summary of tax expenditures that we discuss in chapter 4 of Community Economic Development in the U.S. Again, we focus on the distribution of these resources for a single year (2012) by the income of areas, here zip codes, the only aggregation of tax expenditures publicly available.

Table 2. Tax expenditures (in $1,000s) 2012, by income of zip codes, Federal Reserve Seventh District

*Data reported for the NMTC Program is cumulative 2005-2014.

What is most evident from the data provided in table 2 is the striking inequality of tax expenditures in the United States, a trend that has persisted for decades. Overall, based on this one year of information, total tax expenditures are noticeably biased towards the highest income areas of these Midwest areas: zip codes where incomes are the very highest absorb over one-third of the total dollar amount of these credits with another third in high-income areas. This occurs because the very large components of tax expenditures in the IRS code – the interest deduction for home mortgages, as well as deductions tax payers make for local property and sub-federal income taxes – all consistently benefit high- and very high-income areas.

In contrast, the New Markets Tax Credit, a program administered by the CDFI Fund, concentrated the use of these tax expenditures to very low- and low-income communities in both urban and rural areas across the country, as per the intent of the legislation that created the program. The New Markets Program channels most (85 percent) of the investments leveraged by this program into very low-, low-, and moderate-income neighborhoods.

For over 60 years, the community development movement, initially community development corporations, and later CDFIs, have consistently sought to bring economic opportunity and social progress to America's distressed communities in both urban and rural settings. CDFIs (and CDEs in the NMTC program) have been successful in providing much needed financial literacy and training to residents and businesses, to complement investments to create and retain businesses, rehab homes, and create critically needed community facilities. While the total resources available to the community development movement in the United States is modest, CDFIs and those community-level investors using the NMTC program have provided an alternative, and sometimes the only alternative, to mainstream financial institutions for America's many economically forgotten communities.

1 The authors stress that the opinions and views expressed here are theirs and theirs alone, and do not reflect the position of the Department of the Treasury or the federal government.

2 Rae, Douglas W., 2003, Urbanism and Its End, New Haven, CT: Yale University Press, chap. 4; Gordon, Colin, 2008, Mapping Decline, Philadelphia, PA, University of Pennsylvania Press, pp. 13-22.

3 Where interest and principal were (for the first time) paid simultaneously, and the loan was repaid in full with the final payment.

4 The FHA persisted, even after the landmark Shelley v. Kraemer Supreme Court decision that rendered racially restrictive covenants legally unenforceable, continued to refuse to insure mortgages for properties that would be occupied for non-whites until at least the passage of the Fair Housing Act in 1968. See Immergluck, Dan, 2004, Credit to the Community, Armonk, NY: M.E. Sharpe, p. 96; Gordon, Adam, 2005, “The Creation of Homeownership: How New Deal Changes in Banking Regulation Simultaneously Made Homeownership Accessible to Whites and Out of Reach for Blacks,” Yale Law Journal, Vol 115, No. 1, October, pp. 204-207.

5 The FHA persisted, even after the landmark Shelley v. Kraemer Supreme Court decision that rendered racially restrictive covenants legally unenforceable, continued to refuse to insure mortgages for properties that would be occupied for non-whites until at least the passage of the Fair Housing Act in 1968. See Immergluck, Dan, 2004, Credit to the Community, Armonk, NY: M.E. Sharpe, p. 96; Gordon, Adam, 2005, “The Creation of Homeownership: How New Deal Changes in Banking Regulation Simultaneously Made Homeownership Accessible to Whites and Out of Reach for Blacks,” Yale Law Journal, Vol 115, No. 1, October, pp. 204-207.

6 Olson, Mancur, 1965, The Logic of Collective Action, Cambridge, MA: Harvard University Press, pp. 13-15; Hirsch, Werner Z., 1968, “The Supply of Urban Public Services,” in Harvey Perloff and Lowdon Wingo (eds.) Issues in Urban Economics, Baltimore, MD: Johns Hopkins Press, pp. 477, 503, 519.

7 Harvey, David, 1973, Social Justice and the City, Baltimore, MD: Johns Hopkins, chapter 2; Clark, Gordon L., “Democracy and the Capitalist State: Towards a Critque of the Tiebout Hypothesis,” in Alan D. Burnett and Peter J. Taylor (eds.) Political Studies from Spatial Perspectives, 1981, New York: John Wiley, pp. 91-92.