The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

François R. Velde, Marcelo Veracierto In January 1999, Argentine president Carlos Saúl Menem announced his intention of “dollarizing” Argentina’s economy, i.e., adopting the U.S. dollar as Argentina’s sole currency. His intent is to protect the Argentine economy from speculative attacks on its currency, such as those observed in recent international financial crises. There are two ways to implement dollarization. One is for Argentina to proceed on its own; the other is for Argentina to seek a formal arrangement with the U.S. In this article, we discuss the possible costs and benefits of dollarization. We show that, while it is feasible for Argentina to act unilaterally, there are strong incentives to seek a bilateral arrangement.

Some recent history

Argentina has a long history of high inflation rates fueled by chronic fiscal deficits. When Menem was elected president in May 1989, the economy was already sliding into hyperinflation. In March 1991, the Congress passed the “convertibility law,” establishing the convertibility of the austral (the Argentine currency since 1985) at a rate of 10,000 australes per U.S. dollar. In January 1992, the peso replaced the austral (1 peso for 10,000 australes).

Under the convertibility law, the central bank stands ready to sell dollars at the rate of $1 per peso. Reserves, consisting of gold and foreign currency or deposits and bonds payable in gold and foreign currency, must be maintained at a level no less than 100% of the monetary base. Up to 33% of reserves can be held in bonds of the Argentine government. But, as of April 7, 1999, 4% of reserves were actually held in that form. Furthermore, the central bank cannot change the amount of these bonds by more than 10% in any given year.

The convertibility law also forbids the central bank from monetizing government deficits. Thus, the system cannot be sustained in the long term without sound fiscal discipline. This has forced the government to privatize many state-owned companies and to carry out other major reforms, including trade liberalization, freeing of international capital flows, and deregulation of the banking industry, with resulting benefits to the economy.

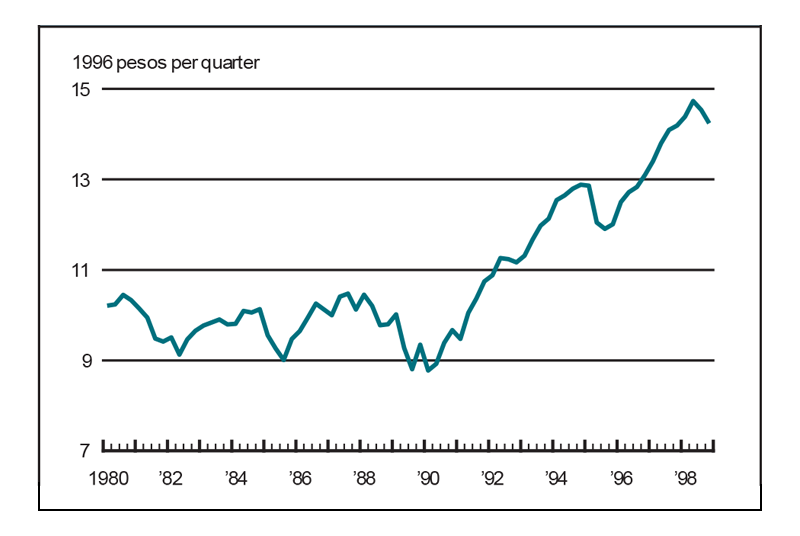

For example, the average annual rate of inflation, which reached a staggering 600% from 1983 to 1991, maintained a stable pace of 4.6% from 1992 to 1998 under the convertibility plan. Figure 1 shows how, after a long period of stagnation, the growth rate of output jumped from 0.4% in 1983–91 to 3.9% in 1992–98. The 1990s expansion was interrupted only twice, coinciding with the Mexican balance of payments crisis (the “Tequila effect”) in 1995 and the recent international turmoil in 1998 (figure 1).

1. Gross domestic product of Argentina

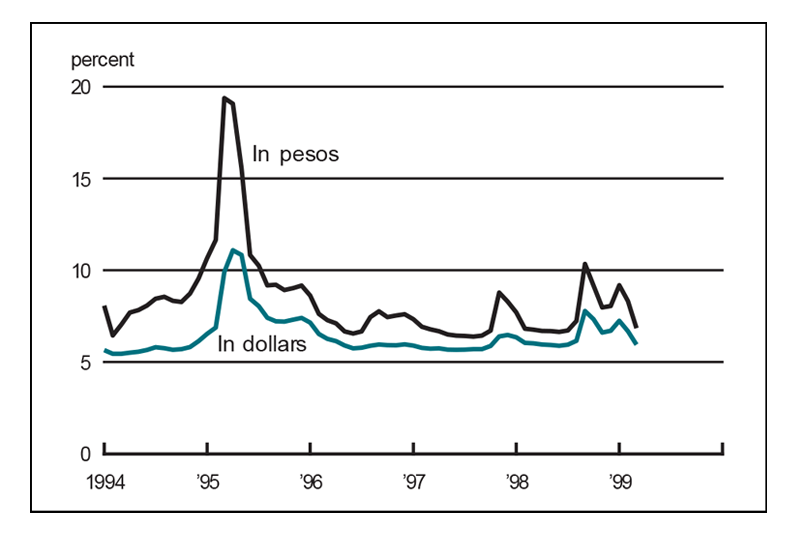

Although the Argentine peso has remained pegged at $1 since 1991, currency crises elsewhere in the world have prompted speculation on a possible devaluation of the peso, in spite of limited trade links between the affected countries and Argentina. For example, Mexico’s share of Argentine exports was only 1.7% in 1994, and Argentina’s exports overall accounted for just 9% of its gross domestic product (GDP). Similarly, although Brazil is Argentina’s main trading partner, exports to Brazil represented only 3% of Argentine GDP in 1998. Interest rates rise sharply with each speculative attack, as shown in figure 2. Furthermore, the premium in interest rates on peso-denominated loans over dollar-denominated loans rises as well, suggesting that the perceived risk of devaluation is much higher.

2. Interest rates on 30–60 daytime deposits

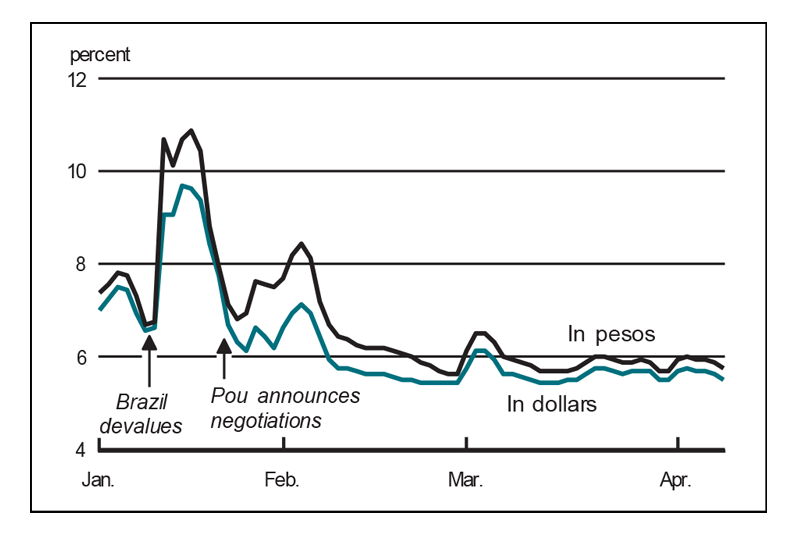

Two days after Brazil devalued the real on January 13, 1999, it became known that President Menem had asked his finance minister to study dollarization. On January 22, the president of Argentina’s central bank, Pedro Pou, stated that a working group was to be formed and meetings would take place with U.S. officials over the coming weeks to discuss ideas and possibly work toward a treaty of monetary association. Figure 3 shows the response of markets to such news, indicating how sensitive interest rates are to the perception of a possible devaluation.

3. Buenos Aires interbank offered rate

Notes: One-day peso and dollar loans. Time period covered is January 4, 1999, to April 12, 1999.

What does dollarization mean?

Dollarization means the elimination of the Argentine currency, the peso, and its complete replacement with the U.S dollar. At present, the monetary base in Argentina consists of the peso-denominated currency. It would be converted into U.S. Federal Reserve notes. The U.S. dollar would be the sole legal tender and sole unit of account.

The Argentine economy is already partly dollarized. For example, 60% of private nonfinancial sector deposits are in dollars. The reserve requirements of commercial banks are met with dollar-denominated assets. Argentines are already used to quoting prices and carrying out transactions in dollars. Complete dollarization would not dramatically change their habits and practices.

For Argentina to dollarize unilaterally, the only requirement is to eliminate the peso-denominated monetary base. Since commercial banks presently hold reserves in dollar-denominated assets, the monetary base is just the currency in circulation. To replace the currency, Argentina needs to buy dollars and exchange all outstanding peso notes for dollar notes. Argentina already has enough resources to buy the required amount of dollars. As of April 7, 1999, the central bank held $18.26 billion in reserves (excluding Argentine bonds), while the monetary base was $14.60 billion.

It is true that if Argentina adopts the dollar as its national currency, it will be unable to pursue an independent or active monetary policy. But Argentina has not had an independent monetary policy since the passage of the convertibility law in 1991. What the repeated speculative attacks on the peso indicate, however, is that retaining the option to resume an independent policy has proven expensive for Argentina.

Another consequence of adopting the dollar is that no Argentine institution will be able to act as lender of last resort to the banking sector by issuing currency to financial institutions in distress. Again, Argentina has not had that ability since 1991. But it has devised alternative mechanisms to deal with liquidity crises.

One is the use of the foreign exchange reserves that the central bank has accumulated in excess of the requirements of the convertibility law. Currently, these stand at about $3.6 billion, about 4% of the banking sector’s total deposits. The central bank can lend these excess reserves to illiquid banks on a short-term basis against collateral. Another mechanism is the imposition of reserve requirements on banks. Since 1995, banks can meet the requirement with interest-bearing dollar-denominated assets held either in a foreign bank account or at the central bank. The central bank has total discretion in setting the reserve requirements. Currently, these reserves amount to $16.8 billion, about 20% of deposits. A third mechanism is a deposit insurance fund, created in 1995, to which banks must contribute on a risk-adjusted basis; it is intended to reach the level of 5% of deposits. Finally, Argentina has arranged a contingent repo facility with a consortium of private foreign banks. This facility gives the central bank the right to exercise a put option on Argentine bonds for cash at any time, subject to repurchase at the end of the agreement period. The facility amounts to $6.7 billion, about 8% of total deposits. These mechanisms provide protection for nearly 40% of Argentina’s deposits, or more than double the monetary base.

A cost–benefit analysis

The decision to dollarize can be taken on the basis of a cost–benefit analysis. The most obvious cost to Argentina is the lost seigniorage on the peso, because once the peso is replaced by the dollar, that seigniorage will accrue to the U.S. The benefit is eliminating the consequences of Tequila effects. (Since dollarization is a one-time event that affects the whole future of the Argentine economy, we need to compare net present values, which requires that some assumptions be made about future growth rates of certain variables.)

The cost of unilateral dollarization for Argentina stems mainly from the loss of the foreign reserves that it would have to sell in exchange for dollars. These reserves bear interest and therefore are a source of income for Argentina. This income is called seigniorage and comes from the structure of any central bank’s balance sheet: Its liabilities (money) bear no interest, while its assets do. But once Argentina’s reserves are replaced by dollar bills, this source of income disappears.

How large would that loss be? According to the central bank’s income statement, the income on all liquid reserves in 1997 amounted to $781 million, an average nominal rate of return of 4.7% (or 2.3% in real terms, given the U.S. rate of inflation for that year). Since liquid reserves were in excess of the monetary base (which averaged $14 billion in 1997), only $658 million actually represents seigniorage, i.e., income on the reserves that back the monetary base. Since nominal GDP was $324 billion in that year, seigniorage represented only 0.2% of GDP.

This number seems small, but it is only a flow. Seigniorage is collected every year. To calculate the costs for Argentina of dollarizing, we compute the value of all future seigniorage that would accrue to the government from the peso-denominated monetary base if it did not dollarize. We estimate what the monetary base would be in the future and use a discount rate to compute the net present value of seigniorage under two alternative scenarios. One is that the velocity of circulation of money remains constant; the other is that the monetary base remains constant.

Using a nominal rate of return of 4.7% on liquid reserves, a nominal discount rate of 6%, an inflation rate of 2%, and a long-run growth rate of real output equal to 3% (roughly the U.S. average to which Argentina may converge), the first scenario leads to a present value of seigniorage foregone equal to $65.8 billion. In the second scenario, the present value of the seigniorage foregone is exactly the current value of the monetary base, about $14 billion, or 4% of GDP.

Which scenario is more appropriate for Argentina? That is hard to say. In other countries, the monetary base usually grows at roughly the same rate as nominal output. On the other hand, Argentina’s monetary base stayed roughly constant in nominal terms from 1994 to 1998 and shrank by 20% as a share of GDP, clearly as a result of the Tequila effect.

What about benefits? As figure 1 shows, the Argentine economy grew at a steady 8% annual rate from 1990:Q1 to 1994:Q4 and at the same rate from 1995:Q4 to 1998:Q2. The Tequila effect appears as a permanent shock to the output level in 1995 that did not affect growth rates before or after the crises (had output continued to grow without interruption, it would now be higher than it is: The loss was never recovered).

We think of Tequila effects as follows. Every year, a Tequila shock might occur, with some probability, independent of previous occurrences. If the shock occurs, output is lower than it would have been in the absence of a shock. Afterward, growth resumes at its normal rate, but output is permanently lower than it would have been without the shock. This model embodies what we see in figure 1, namely, that the growth rate was not permanently affected by the Tequila effect, but a sharp reduction in output occurred in 1995.

For simplicity, we compare flows rather than net present values, but the results are the same. If Argentina dollarizes, it loses seigniorage each year. On the other hand, it avoids the possible output loss of a Tequila effect. Unilateral dollarization will then be advantageous if the expected output loss exceeds the lost seigniorage. One can think of giving up seigniorage as the premium to insure against possible output losses.

For the Tequila effect, the permanent output loss turns out to be about 14%. Current forecasts for GDP growth in 1999 suggest that the impact of the Asian crisis will be the same size. Using the numbers above, and under the scenario that velocity will remain constant, we find that the annual probability of a Tequila effect would have to be 1.4% to make Argentina indifferent between dollarizing and not dollarizing. Given that Argentina has been hit twice in ten years, unilateral dollarization is unambiguously desirable.

While Argentina could substantially benefit from a unilateral dollarization, there are incentives for Argentina to seek an arrangement with the U.S. That is because, in order to dollarize, Argentina has to buy noninterest-bearing dollars with the interest-bearing reserves it holds; the U.S. in effect swaps interest-bearing debt for noninterest-bearing debt. According to our calculations above, this represents a one-time transfer from Argentina to the U.S. of about $65.8 billion under one scenario (constant velocity) or $14 billion under the other (constant monetary base). It is not surprising that Argentina is seeking to dollarize the economy within some form of formal arrangement with the U.S. that would allow it to reduce the size of this transfer.

A formal arrangement might also be of value to Argentina as a form of credible commitment. Since Argentina could unilaterally reverse unilateral dollarization by reintroducing a new domestic currency and making it legal tender, investors might remain wary of the Argentine government’s future actions and continue to demand higher interest rates to compensate for this uncertainty. A formal, international commitment to maintain the dollar as the currency of Argentina could be more persuasive.

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| March | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 129.8 | 129.4 | 127.9 |

| IP | 137.0 | 137.0 | 134.1 |

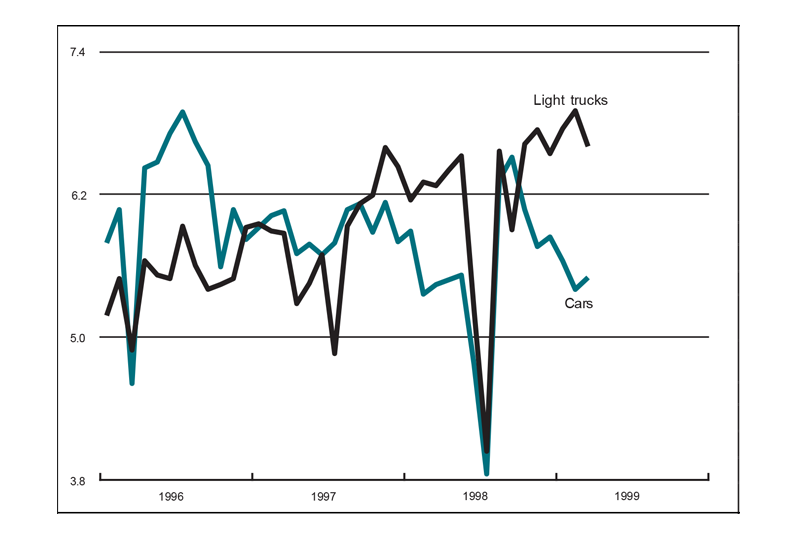

Motor vehicle production (millions, seasonally adj. annual rate)

| March | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.5 | 5.4 | 5.4 |

| Light trucks | 6.6 | 6.9 | 6.3 |

Purchasing managers' surveys: net % reporting production growth

| April | Month ago | Year ago | |

|---|---|---|---|

| MW | 68.8 | 59.2 | 64.6 |

| U.S. | 57.6 | 59.6 | 53.4 |

Motor vehicle production (millions, seasonally adj. annual rate)

The Chicago Fed Midwest Manufacturing Index (CFMMI) rose 0.3% from February to March to a seasonally adjusted level of 129.8 (1992 = 100). The Federal Reserve Board’s Industrial Production Index for manufacturing (IP) was unchanged in March after having risen 0.3% the prior month. Light truck production decreased from 6.9 million units in February to 6.6 million units in March, and car production increased slightly from 5.4 million units for February to 5.5 million units for March.

The Midwest purchasing managers’ composite index (a weighted average of the Chicago, Detroit, and Milwaukee surveys) for production increased to 68.8% in April from 59.2% in March. The purchasing managers’ indexes increased in Chicago and Detroit but decreased in Milwaukee. The national purchasing managers’ survey for production decreased from 59.6% in March to 57.6% in April.