The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Some in the banking industry have wrung their hands over the slow adoption of debit cards, e-cash, electronic bill payment, financial electronic data interchange (FEDI), and smart cards in the U.S. Whether or not these innovations grow swiftly, this subject is important for several reasons. First, payment services bring in significant revenues for financial institutions, and changes in technology could impact future revenues. Second, a cornerstone of policy on issues of safety, soundness, and consumer protection is the assumption that a significant portion of financial services activity flows through “trusted” financial institutions. As a result, it is important for policymakers, the industry, and the public to understand the broad implications of technology for the payments mechanism and banking.

How will the future path of electronic payment systems be determined? One school of thought argues that a number of obstacles and barriers stand in the way of e-payment innovations and that these will need to be addressed before e-payment technologies can be successful. Other studies have suggested an alternative theory—that the advent of the internet will cause revolutionary changes in banking and commerce requiring fundamentally new payment systems to evolve.1 At the root of this debate are several questions. Why do some innovations succeed and others fail? How do these changes occur? Are e-money innovations and the supporting law and technology infrastructure driven by planning for future needs or by focusing more narrowly on past problems? Will the innovations be spurred by current institutions or by nontraditional providers?

In this Chicago Fed Letter, I provide an overview of developments in e-money systems and commerce. I then explore research on the economics of innovation to put these changes in a broader context. Lastly, I analyze the potential implications of changes in banking and commerce for the evolution of e-money. In the process, I build on a theory advanced by Clayton Christianson that aims to explain and predict how different product innovations do or do not occur.2

The changing nature of commerce

The nature of commerce will continue to change with the growing familiarity of the internet and the worldwide web. Use of the worldwide web is on track to reach a critical mass of U.S. households many times more quickly than the telephone did when it was introduced into American households. The Gartner Group predicts that over $7 trillion worth of business-to-business (B2B) commerce will be conducted electronically in 2004, and over $380 billion of business-to-consumer (B2C) commerce will be conducted electronically in 2003.3 While the last five years have seen firms experiment with the internet to advertise the availability of products and to offer services for sale in a transaction capacity, more fundamental changes in commerce have begun to emerge. Consider eBay, which allows consumers to trade with consumers without a direct intermediary, creating a fundamentally new market of buyers and sellers who would otherwise have been unlikely to find one another. Yet, while providing important benefits, this new commercial environment also exposes consumers to risks that they may not be accustomed to managing, such as finality of payments and recourse in case of untimely delivery or poor quality. Similarly, emerging internet-based B2B portals may offer significant improvements to market participants, but again may potentially expose them to important risks, relating to seller performance, buyer financial stability, and dispute resolution.

Changing nature of payment systems

As one would expect, payment systems have been evolving to meet the changing needs of buyers and sellers. New payment instruments are being created to expand the reach of the payments infrastructure that has been in place for decades; current systems are being reengineered at the fringe; and fundamentally new payment systems are being developed as well. For instance, while the development of new e-cash technologies continues to be explored, PayPal, an internet payment mechanism, puts a “new front end” on existing credit card and ACH (automated clearing house) networks to make them more convenient for consumers and to allow consumers to send money to each other. Paper checks are being converted to electronic transactions and cleared via the ACH and ATM (automated teller machine) networks by some retailers as a device to reduce check-clearing costs and to begin to wean some consumers from checks. Some organizations are also exploring the use of ATM networks and the ACH for internet transactions in order to offer a lower cost alternative to credit cards. Some retailers have also implemented store-based debit cards that are cleared and settled over the ACH rather than ATM networks, again to reduce costs while broadening the store’s relationship with its customers.

That organizations are using “different payment networks” for “similar” commercial purposes and the “same payment networks” for “very different” commercial reasons is not a new phenomenon. For instance, for decades some organizations have used checks for payments of hundreds of thousands of dollars rather than using large-dollar, real-time funds transfer systems. Other organizations have traditionally used large-dollar, real-time funds transfer systems to make fairly modest-sized payments. Some of these events are motivated by the fact that it is easier to pay using “preset mechanisms” than to change to a new system for infrequent transactions. At other times, decisions are driven by a payment instrument’s “special features.” For example, a firm might use checks for large-dollar payments to slow down the process for exchanging funds or to improve its negotiating leverage with a supplier. On other occasions, a firm might use large-dollar payments mechanisms to guarantee timely payment. Thus, a significant amount of pressure is exerted on payment systems as various parties attempt to push innovations with certain characteristics or to leverage other instruments for their relative strengths.

Payment innovations

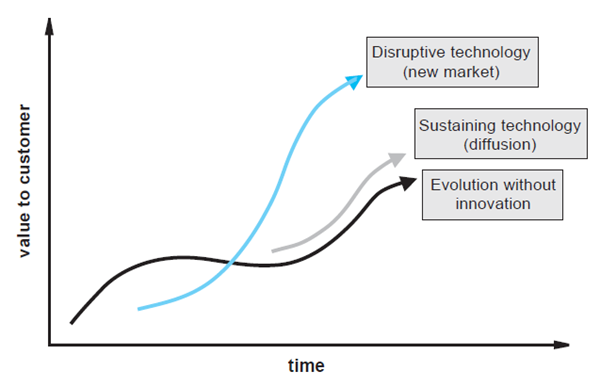

How does the process of innovation occur? There are two general, complementary theories of how new products are adopted. The first theory, the new product diffusion model, assumes that the primary determinant of new product adoption is the time it takes customers to learn about a product, to experiment with it, and then ultimately to use it. This theory assumes that customers view a new product or service as a clear substitute for past products. These types of innovations essentially “sustain” or “extend” the current product (see figure 1). Christianson notes that new entrants in this market will tend to find it harder to enter successfully against incumbent competitors, who can roll out innovations profitably to their existing customer bases.

1. New product innovation models

The second theory, the new market development model, suggests that some innovations—disruptive technologies—lead to new products or services that by themselves have a limited market potential (see figure 1). This theory suggests that, in order to reach mass markets, firms need to offer additional product features and / or infrastructure, tailoring the product to new uses and to nontraditional customers. In many of these cases, Christianson suggests that “new” or “nontraditional” providers tend to have an advantage over incumbent firms since they have the freedom to focus on fringe benefits rather than focusing on mass market needs.4

Why haven’t e-payments succeeded?

Theory 1: Product diffusion

Building on new product diffusion theory, some studies cite a laundry list of barriers standing in the way of e-payment innovations. On the demand side, studies have cited customer resistance or inertia, lack of incentives, and lack of customer awareness of the innovation as obstacles to change. On the supply side, studies have pointed to the lack of clear standards, the need to overcome industry fragmentation, inadequate incentives among incumbents, and the presence of network externalities. This theory assumes implicitly that a significant portion of e-payment innovations are clear substitutes for existing services and that additional work by incumbent firms alone or in collaboration will lead to broad acceptance.

Theory 2: New market development

The second theory suggests that broader structural changes are underway, driven by technology, and these changes are blurring the lines between banking and commerce. While it is both natural and critical for incumbent firms to experiment, this theory suggests that these innovations tend to unleash improvements that incumbents may not find valuable in the short- or mid-term. Some observers may suggest that incumbent firms in these industries “do not understand their markets” or “are not adequately investing in the future.” However, Christianson finds that incumbent firms, for purely profit maximizing reasons, may not want to choose to pioneer some of these innovations themselves, leaving other firms with different specialties to do so.

Blurring lines of banking and commerce

Figure 2 provides an overview of the historical changes underway in the financial services industry. Looking back 20 years, banks competed primarily on the basis of geography. With the advent of deregulation and technology, significant changes occurred in the 1980s and 1990s with the emergence of more product-based institutions. It is not clear how the industry structure will progress in the 21st century, but future models of financial services might include: 1) a universal bank that bundles a broad range of financial products and services under one roof for a broad range of customers,5 2) an institution that focuses on the broad financial and nonfinancial needs of a narrow segment of the market,6 3) a “virtual portal” or “aggregator” that uses technology to integrate financial services from a variety of specialized providers,7 or 4) a traditional, financial institution, which focuses on a limited number of financial products.

2. Financial services industry structure

According to the new market development theory, many of the so-called obstacles and barriers to innovation may be better viewed as symptoms of the broader changes underway, rather than as problems per se. For example, a larger number of financial institutions may need to have a broader relationship with customers (i.e., a move towards universal banking). In these cases, institutions may be able to invest in e-payment innovations as a cost of doing business for obtaining the customer’s broader business, rather than purely as a revenue generator.8 As a second example, a larger fraction of customers may need to become more willing to accept fee-based services rather than bundled services.9 In this case, rising consumer receptivity to fees could spur potential innovations. In a third example, some e-money innovations may not be commercially feasible until other banking and nonbanking functions are more closely integrated (i.e., a move toward the second model).10

A payment systems framework

The above discussion makes it clear that payment systems questions are complex, involve a significant number of interrelated issues associated with commercial relationships, technology, the law, and business practices, and involve coordination among a variety of parties with different and sometimes competing interests. Adding to the complexity of these relationships, payment systems involve long-term infrastructure investments, which evolve slowly over time. As a result, it is critical to evaluate payment systems changes in a broader context, which recognizes the various component factors, including the nature of the commercial relationship as well as the nature of the payment systems used. See figure 3 for a graphical schematic of the simplified payments relationship. Frameworks like this one allow for more careful analysis of which innovations are clear substitutes for one another and the potential implications for different parties.

3. Payments framework

Conclusion

This article provides an alternative theory to the traditional “obstacles and barriers” theory for explaining why some e-money innovations have not succeeded more quickly. In the process, it provides a framework for characterizing new innovations as well as better understanding where, when, how, and by whom these new innovations will occur.

This theory has potentially important implications for public policy. In terms of safety and soundness policy, some would argue that the growing role of nonbanks will pose significant questions to safety and soundness. Yet, the “new market development” theory suggests that nonbanks will not necessarily replace the functions of banks but rather provide parts of services that financial institutions do not have a comparative advantage in providing.11 Second, much of consumer protection policy is based around bundling protections around a few fairly common banking products. To the degree that commerce and banking continue to mingle, public authorities may need to be particularly careful about attempting to regulate the relative rights, warranties, and incentives associated with alternative e-money implementations, leaving markets to influence the outcomes.12

It should be noted that the above types of questions are not new. Indeed, banking and commercial markets have been facing these types of issues for years. The above points are observations advanced as a theory for how e-money systems may evolve. Clearly, these are not resolved questions; rather they are questions warranting careful monitoring. More importantly, the policy implications for private sector and public sector leaders may be quite different depending on one’s view of how the market is evolving.13

Notes

1 A critical issue running through both of these theories relates to the problems associated with implementing products with network externalities. For instance, see G. Gowrisankaran and J. Stavins, 1999, “Are there network externalities in electronic payments?” Global Financial Crises: Implications for Banking and Regulation, proceedings from the 35th Conference on Bank Structure and Competition, Chicago: Federal Reserve Bank of Chicago, pp. 302–312.

2 Clayton Christianson, 1997, The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail, Boston, MA: Harvard Business School Press.

3 Leah Knight, 2000, “Triggering the B2B electronic commerce explosion,” Trends and Directions Note, Stamford, CT: Gartner Group; and Blaine Mathieu, 1999, “Global consumer e-commerce forecast update,” Trends and Directions Note, Stamford, CT: Gartner Group.

4 An important segment of the “new market development” theory, as I define it, is for those innovations 1) with positive network externalities and 2) with users who make significant and irreversible investments leading to an installed base. This installed base, coupled with the presence of switching costs, leads to significant challenges for new innovations to prosper. As a result, I argue that some innovations, which might appear to be natural extensions of current products (such as smart cards for credit cards), actually fall into the “new market development” category. For more on this subject, see Michael L. Katz and Carl Shapiro, 1993, “Network externalities, competition, and compatibility,” Princeton University, Woodrow Wilson School, discussion paper in economics, No. 54, September.

5 For instance, see Liz Moyer, 1999, “Citigroup’s strategy: Multiple products, multiple channels,” American Banker, Vol. 164, No. 191, October 5.

6 For a broader discussion, see Peter Wallison, 2000, “The Gramm-Leach-Bliley Act eliminated the separation of banking and commerce,” The Changing Financial Industry Structure and Regulation: Bridging States, Countries, and Industries, proceedings from Conference on Bank Structure and Competition, Chicago: Federal Reserve Bank of Chicago, pp. 34–41.

7 For instance, see Ross Snel, 1999, “Intuit offers view of accounts with more than one provider,” American Banker, Vol. 164, No. 220, November 1.

8 For instance, see Steve Ollenberg, 1999, proceedings from the Federal Reserve Bank of Chicago and Illinois Institute of Technology’s Electronic Payments Workshop, Chicago, IL, September.

9 For instance, see “Impose those fees—And stick to your guns,” American Banker, Vol. 165, No. 65, April 4, 2000.

10 For instance, see Catherine Allen, 1999, “Remarks,” proceedings from the Federal Reserve Bank of Chicago and Illinois Institute of Technology’s Electronic Payments Workshop, Chicago, IL, September.

11 For instance, see “Banks giving aggregators respect, biz,” American Banker, Vol. 165, No. 157, August 16, 2000.

12 For instance, see Henry H., Perritt Jr., 1999, “Remarks” in proceedings from the Workshop on Promoting the Use of Electronic Payments: Assessing the Business, Legal, and Technological Infrastructures, Chicago, IL, September.

13 The author would like to recognize the participants at Electronic Commerce Canada’s Conference “The E-Business Transformation: Where to Go?” for their helpful comments on an early version of this article.