The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

While national retail sales information is readily available, it is difficult to obtain state or regional data. To address this need for local information, the Michigan Retailers Association and the Federal Reserve Bank of Chicago began a monthly survey of retailers in July 1994. The survey compares sales, inventories, prices, promotions, and hiring plans versus the prior year and analyzes retailers’ expectations. Seasonally adjusting the index will make it an even better tool for researchers and business analysts in the future.

Given that consumer spending represents two-thirds of the U.S. economy, understanding retailing is an important part of analyzing overall economic activity. While retail sales information is readily available nationally, it is more difficult to obtain on a state-by-state or regional basis. The Census Bureau published monthly retail sales data for large states from the mid-1980s to the mid-1990s but then discontinued the series. In an effort to better understand retail activity in Michigan, the Michigan Retailers Association and the Federal Reserve Bank of Chicago began a monthly survey of retailers in July 1994.1 This article discusses the survey, how seasonal adjustment improves the results, and how the results compare to published economic data.

The Michigan Retailers (MR) Survey is mailed to members of the Michigan Retailers Association who do business in Michigan—around 3,900 firms—in the fourth week of each month. The deadline for responses is usually during the second week of the following month. The response rate averages 7%, in line with the typical response rate for mail surveys. The respondents appear to represent a geographic sampling of many different firms throughout the state, while the sampling across retail sectors is diverse but not entirely representative of their distribution in Michigan.

The survey covers five areas: sales, inventories, prices, promotions, and hiring plans. Respondents indicate whether, based on their own business a year ago, the current month’s experience or their expectations for the next three months represent an increase, decrease, or no change. The results are then calculated into a diffusion index, which is the sum of the percentage indicating an increase plus half the percentage indicating no change, assumed to be positive. The Michigan Retailers Association publishes the results on the fourth Wednesday of the following month (i.e., the January data are released on the fourth Wednesday in February). The results provide insights into the Michigan retailing environment. However, a persistent seasonal pattern in the raw data has made month-to-month comparisons difficult.

Seasonal adjustment

It is well known that retailers experience significant seasonal effects in their business. While we ask respondents to keep these seasonal effects in mind—by asking them to compare their current activity with a year ago—there is still a significant seasonal pattern in the survey results. Every index we develop from the survey, except for sales in the current month,2 tests positive for a significant seasonal pattern.

Generating a seasonally adjusted series requires many observations of the data. Now that we have more than seven years’ worth of data, we can use the X-11 seasonal adjustment procedure developed by the Census Bureau to eliminate the seasonal patterns in the survey data. We began releasing seasonally adjusted data with the January 2002 survey results.3 This change allows researchers to make better use of the survey.

To illustrate the benefits of seasonal adjustment, figure 1 shows the unadjusted (black line) and seasonally adjusted (red line) inventory index. Before the adjustment, the data show a substantial buildup of inventories during the summer and early fall and a significant downsizing at the start of the year. This pattern is due to businesses stocking up for the holiday selling period. It is not unusual for inventories to rise during the summer and early fall; what we are really interested in is whether inventories are rising more or less than usual for this time of year. Seasonally adjusting the data provides an answer to this question. For example, the seasonally adjusted data reveal that during fall 2000 inventories were not increasing as rapidly as one would have thought.

1. Inventories index

How do the indexes perform?

Using survey data as an indicator of economic activity is not new. A popular survey, and an inspiration for our work, is the Institute for Supply Management’s (ISM) monthly manufacturing Purchasing Managers Survey. The ISM, formerly the National Association of Purchasing Management (NAPM), has been gathering information in one form or another since 1930 on various aspects of manufacturing, including new orders, production, prices, employment, and inventories.

There is a significant amount of literature about the usefulness of the ISM indexes for economic analysis and forecasting.4 Much of the research focuses on how well the indexes relate to published data. For example, Robert Bretz, former chairman of the Business Survey Committee of NAPM, reports that there is a strong correlation (an R2 of .71) between the quarterly average of the ISM production index and the quarterly growth rates of the Federal Reserve Board’s Industrial Production Index. Additional research has shown that when the ISM production index falls below 49.5, generally industrial production will be declining.5 Additionally, much of the research reports that because of the nature of the ISM indexes—they are also diffusion indexes—they tend to lead turning points in comparable economic data.

The popularity and applicability of the ISM indexes raises two questions for our survey. First, how well does the MR survey compare with published economic data? Second, does our survey have any leading indicator properties?

There are three main problems in assessing the performance of our survey. The first problem is the dearth of appropriate data to measure against the survey. Second, monthly data for both our survey indexes and the published data that we are using for comparison tend to be very volatile. To get a good picture of how well our index performs, we should use quarterly, or even annual data, as was done for much of the ISM analysis. However, this would mean basing our analysis on an even smaller number of observations. Instead, we have made efforts to smooth out the volatility wherever appropriate. The third problem we run into is that the ISM survey sample reflects the distribution of industries in the manufacturing sector; whereas, our survey sample is largely random, which might skew our results. Below, we look at how four of our five survey indexes measure against comparable published data. In the case of inventories, we have no comparable regional data, so we measure our index against national data. We have no comparable regional or national data for the promotions index.

Sales

An obvious choice of comparison for our sales data is the retail sales data published by the Census Bureau. Unfortunately, the Census Bureau stopped publishing monthly sales data after 1996, so we have only 30 observations to measure our survey against. The correlation coefficient6 of our monthly sales survey against the Census Bureau’s data on Michigan’s monthly total retail sales is 0.53. One of the problems of this comparison, however, is that the Census Bureau’s data include sales of motor vehicles—a very volatile portion of retail activity—and our sample contains few, if any, auto dealers.7 The Census Bureau does not provide motor vehicle retail sales data on a monthly basis at the state level, but it does break out retail sales of nondurable and durable goods. When we compare the MR sales survey against nondurable good retail sales, we get a better correlation coefficient of 0.64. Neither the sales index nor the expected sales index of the MR survey has any leading indicator properties for these data.

Another option for data comparison is monthly sales tax revenue, but these data can be somewhat problematic. The timing of sales tax payments may not correspond to the exact volume of sales. To overcome this challenge, we compared a three-month moving average of sales tax revenue with a three-month moving average of the MR sales index. The correlation coefficient was .43, and there was a very slight tendency for the MR sales index to lead the sales tax data. The correlation coefficient between the expected sales index and the sales tax revenue was .49, and the leading tendency of the expected sales index is also very slight—a somewhat disappointing conclusion since we would hope that the expected sales index would have strong leading indicator properties. But, similar to the problem with the retail sales data, the sales tax revenue data also include motor vehicle sales tax revenue.

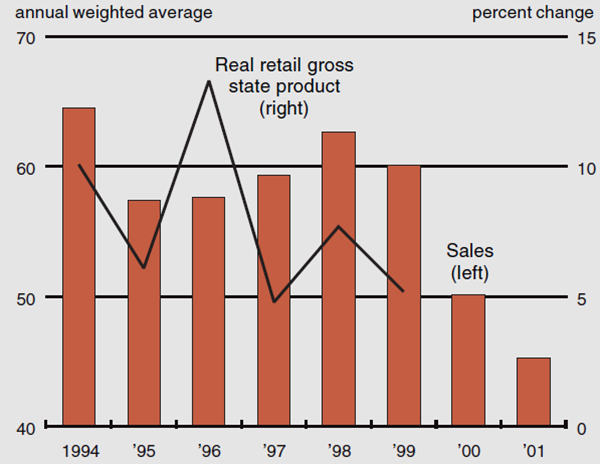

We also plotted our sales survey against real retail trade gross state product, which is available on an annual basis. To get an annual figure for our sales index, we took a weighted average of our sales index in each year; the weights were each month’s historical share of annual retail sales. We found that in five of the six years for which we have data, the MR sales index moves in the same direction as the growth rate of retail gross state product (see figure 2).

2. Sales index vs. real retail gross state product

Prices

Comparing the MR price indexes with various inflation measures exhibits the best correlations, but curiously they are not where we expected. We looked at the price and expected price index against the Midwest and Detroit Consumer Price Indexes (CPI). We eliminated food and energy prices, which tend to be more volatile than other prices, from our analysis by using the so-called core price index. Additionally, we looked at total and nondurable commodity prices—in order to exclude services prices—both including and excluding food and beverage.

While there were significant correlations looking at unsmoothed data, the correlation was even stronger when we used three-month moving averages. The correlation coefficient between the Midwest core price index and the MR price index was .68, and there was some tendency for the MR price index to lead changes in the Midwest core inflation rate. There was an even stronger tendency for the expected price index to lead changes in inflation: The coefficient for a three-month lead in the expected price index was .80.

However, the correlations with the Detroit CPI were not as strong as the correlations for the Midwest inflation rates. When we compared various Detroit inflation rates—for the core, commodities, and commodities excluding food and beverage—with both the price and expected price indexes, only one comparison yielded a correlation coefficient better than .50, and there were no leading indicator properties. Smoothing the data improved the correlation coefficients, but they were still not as high as those for the Midwest inflation rates. We had expected that the inflation measure more closely related to our survey sample would result in higher correlations. One reason for this might be that the Detroit CPI data are only available every other month, which decreases the number of observations and raises issues about the best way to aggregate the survey indexes into bimonthly data—whether to take a two-month average or to use every other month.

Employment

The final index for which we have comparable regional data is the hiring plans index. The Bureau of Labor Statistics releases monthly data on industry payroll employment for each state. For Michigan, we looked at total retail trade employment. We smoothed the survey index by taking a three-month moving average and compared it to the unsmoothed employment data. Still, the correlation coefficient for the hiring plans index was only .39, and there were no leading tendencies associated with it. The correlation for the expected hiring plans also was not very significant, but there was a strong tendency for the expected hiring plans index to lead employment. The correlation coefficient for the expected hiring plans index in the third month before the employment data was .51.

Though the level of the correlation is not enormous, there is probably a simple explanation for the deficiency. The survey asks respondents about hiring plans not employment levels. It could be that when respondents increase their hiring plans, they are unable to fill the job because of tight labor markets.

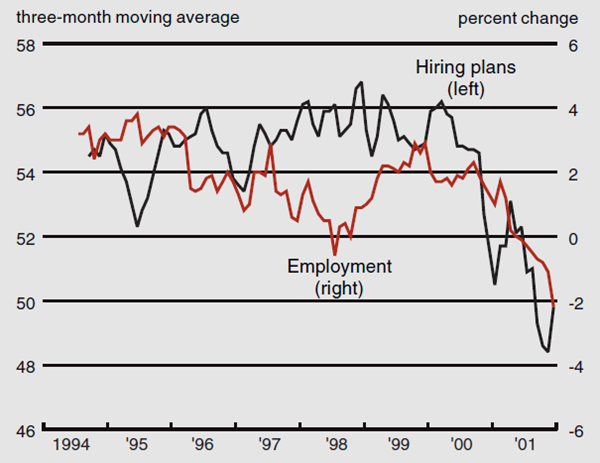

We have some evidence to back up this conclusion. As figure 3 shows, the major break in the relationship between the three-month moving average hiring plans index and the retail employment growth data occurs between July 1997 and July 1999. During this time, the unemployment rate in Michigan fell to a near record low of 3.7%, a sign of tight labor market conditions. Excluding this period, the correlation co-efficient between the smoothed hiring plans index and retail employment growth improves to .65 and the expected hiring plans index in the third month before improves to .73.

3. Hiring plans index vs. retail employment growth

Inventories

For the inventories index, there are no appropriate regional data available for comparison. However, there are comparable national data. The correlation coefficient for the MR inventory index against national retail inventories excluding motor vehicles is .65, and there is a slight tendency for the MR index to lead the national data. This could be a sign that regional inventory trends do not wander too far from national trends.

Conclusion

Our research shows that the MR survey is relevant in signaling economic changes: It generally correlates well with published data and occasionally has leading indicator properties. Seasonally adjusting the index improves these relationships and makes the index easier to understand. We will continue to track the relevance of the survey as we add more years of data, as well as exploring additional ways to improve its usefulness to researchers and business analysts.

Notes

1 The authors would like to thank the Michigan Retailers Association, particularly Tom Scott, for their continued partnership on the survey. They would also like to thank Scott Walster for his research assistance.

2 Although the current sales index does not exhibit a statistically significant seasonal pattern, we found that seasonally adjusting the index resulted in a modest improvement in its correlation with published data.

3 Historical data and press releases are available on the Michigan Retailers Association website at www.retailers.com/news/aboutri.html.

4 Among the most recent works summarizing this research is Ralph G. Kauffman, 1999, “Indicator qualities of the NAPM report on business,” Journal of Supply Chain Management, Vol. 53, No. 2, Spring, pp. 29–43. But Robert, J. Bretz, 1990, “Behind the economic indicators of the NAPM report on business,” Business Economics, July, pp. 42–48, is slightly more comprehensive.

5 Most recently reported in ISM, 2002, “January manufacturing ISM report on business,” February 1.

6 Our measure for correlation is the Pearson Product-Moment Correlation, which ranges from –1 to 1. A result close to 1 indicates that the two series tend to move in the same direction and magnitude, while results close to –1 indicate that the two series move in the opposite direction but at the same magnitude. Results close to 0 mean that there is no correlation between the series.

7 Since our survey is completely anonymous, we cannot know this for sure. While we do have a space for respondents to indicate their type of business, we do not have a box for automotive dealers. But an examination of the business titles on our mailing list reveals that we mail less than 1% of the surveys to businesses that probably sell vehicles. According to the U.S. Census Bureau’s 1992 Economic Census for the State of Michigan, 6% of all retail establishments in Michigan are automotive dealers.