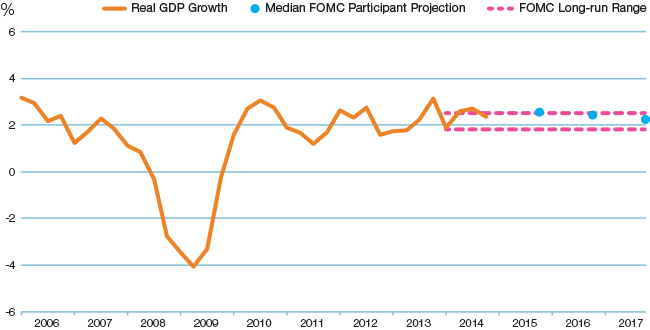

Economic Growth

Year-over-Year Real Gross Domestic Product Growth

Data current as of April 15, 2015. Sources: Data from the Bureau of Economic Analysis and the Board of Governors of the Federal Reserve System, accessed via Haver Analytics.

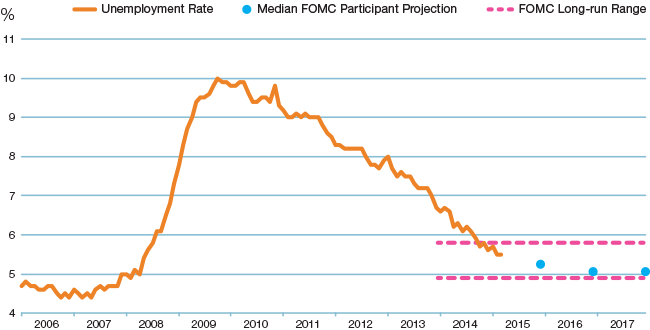

Labor Markets

Percent of Labor Force Unemployed

Data current as of April 15, 2015. Sources: Data from the Bureau of Labor Statistics and the Board of Governors of the Federal Reserve System, accessed via Haver Analytics.

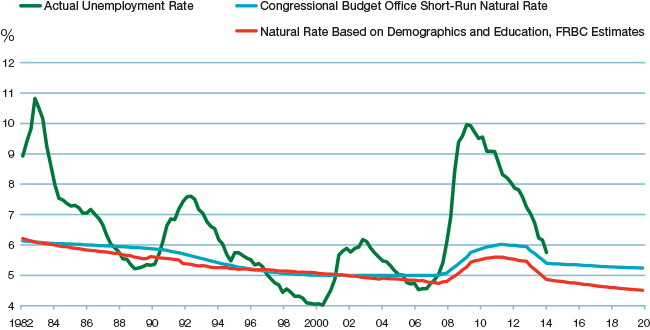

Unemployment Research

Actual Unemployment Rate and Natural Rates

Data current as of April 15, 2015. Sources: Bureau of Labor Statistics and Congressional Budget Office, accessed via Haver Analytics and authors’ calculations from the Current Population Survey.

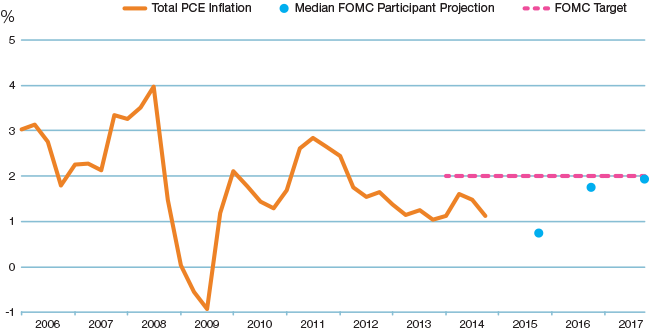

Inflation

Year-over-Year Personal Consumption Expenditures (PCE) Inflation

Data current as of April 15, 2015. Sources: Data from the Bureau of Economic Analysis and the Board of Governors of the Federal Reserve System, accessed via Haver Analytics.

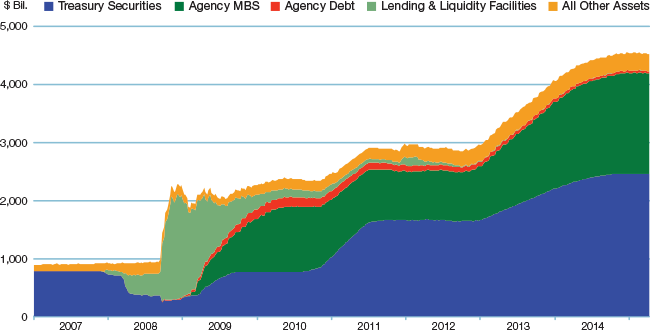

Balance Sheet

Federal Reserve Asset Categories

Data current as of April 15, 2015. Sources: Data from the Board of Governors of the Federal Reserve System, accessed via Haver Analytics.

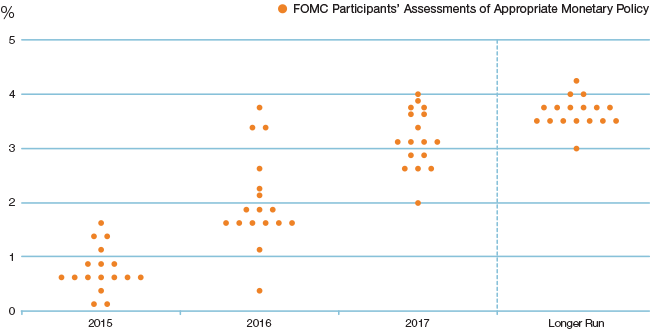

Federal Funds Rate

Target Federal Funds Rate at Year-End

Data current as of April 15, 2015. Sources: Data from the Board of Governors of the Federal Reserve System, accessed via Haver Analytics.