Summary

In the third quarter of 2017, agricultural land values for the Seventh Federal Reserve District were down 1 percent from a year ago. Moreover, on a year-over-year basis, “good” farmland values were little changed for the fourth quarter in a row. According to the 201 agricultural bankers who responded to the October 1 survey, District farmland values were overall unchanged in the third quarter of 2017 from the second quarter. The vast majority of survey respondents expected the District’s agricultural land values to be stable during the fourth quarter of 2017, but 25 percent of them expected a decrease in farmland values in the final quarter of 2017 and 2 percent expected an increase.

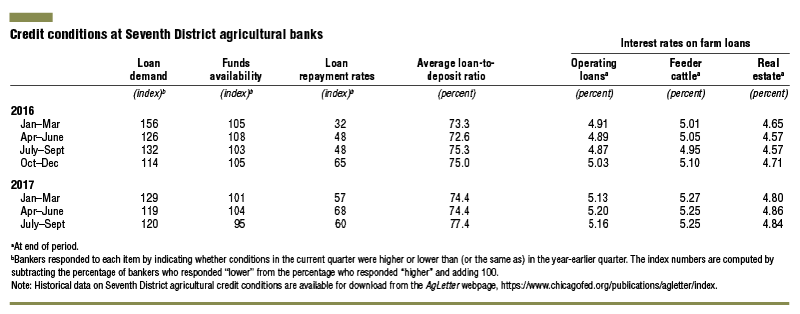

District agricultural credit conditions deteriorated in the third quarter of 2017. For the third quarter, the availability of funds for lending by agricultural banks was down relative to a year ago—the first such occurrence in 11 years. However, for the third quarter, the demand for non-real-estate loans was up relative to a year ago. The result was a surge in the average loan-to-deposit ratio for the District to 77.4 percent—its highest level in nine years. Furthermore, repayment rates for non-real-estate farm loans were lower in the third quarter of 2017 relative to the same quarter last year, and loan renewals and extensions were higher. Remaining near their historically low levels, average interest rates on farm loans moved little during the third quarter of 2017.

Farmland values

District farmland values saw a year-over-year decrease of 1 percent in the third quarter of 2017. The District did not experience a year-over-year decrease or increase in its agricultural land values greater than 1 percent in the past four quarters. Such relative stability in farmland values had not occurred in the District since 1970. Illinois and Indiana farmland values were down on a year-over-year basis (3 percent and 4 percent, respectively), while Iowa and Wisconsin farmland values were both up 2 percent (see map and table below). The District’s agricultural land values were unchanged from the second quarter of 2017.

Difficult weather conditions during planting season, a trying drought, and heavy rains during harvest all threatened to batter District crops this crop year. In the end, according to U.S. Department of Agriculture (USDA) forecasts, the five District states’ harvest of corn for grain in 2017 would fall by 7.8 percent from 2016, whereas soybean production would just break the record, set last year (see chart 1). The new record soybean crop (0.2 percent above 2016’s level, according to USDA projections) resulted from harvesting 5.9 percent more acres in 2017 than in the previous year. Both District-wide corn and soybean yields (bushels per acre) were down from their all-time highs, set in 2016.

1. Corn and soybean production for Seventh District states

Many agricultural prices remained fairly close to their levels of a year ago, and some even rose. For the third quarter of 2017, corn prices were flat relative to the third quarter of last year, based on USDA data. Soybean prices were down 5.2 percent from the third quarter of 2016. Nevertheless, soybean net returns were likely to exceed those of corn on a per-acre basis for most farm operations. Except for cattle producers, livestock operators saw improvements in product prices in the third quarter of 2017 relative to the same quarter of a year earlier. Compared with a year ago, egg, hog, and milk prices were up 40 percent, 11 percent, and 4.7 percent in the third quarter of 2017, respectively. Meanwhile, cattle prices slipped 1.2 percent from the third quarter of 2016. So, on the whole, agricultural prices did not seem as bleak as a year ago, but there was not much (if any) improvement for most farm operations—and farmland values.

Credit conditions

In the third quarter of 2017, the District’s agricultural credit conditions seemed worse relative to a year ago once again. For the first time since the third quarter of 2006, the availability of funds for lending by agricultural banks was lower relative to a year earlier. At 95 for the third quarter of 2017, the index of funds availability showed that, by and large, agricultural banks in the District had less funds for lending than a year ago; 10 percent of the survey respondents indicated their banks had more funds available to lend during the third quarter of 2017 than a year earlier and 15 percent indicated their banks had less. In the third quarter of 2017, demand for non-real-estate loans compared with a year ago continued to be stronger. The index of loan demand ticked up to 120, as 35 percent of survey respondents noted higher demand for non-real-estate loans than a year earlier and 15 percent noted lower demand. The combination of decreased funds availability and elevated loan demand contributed to a sizable jump in the District’s average loan-to-deposit ratio to 77.4 percent—its highest level since the third quarter of 2008 (see chart 2). Even so, the average level desired by the responding bankers was 4.2 percentage points higher.

2. Quarterly average loan-to-deposit ratio for Seventh District

There were still lower repayment rates on non-real-estate farm loans relative to a year ago in the July through September period of 2017. The index of loan repayment rates dropped to 60 in the third quarter of 2017, as 3 percent of responding bankers observed higher rates of loan repayment relative to a year ago and 43 percent observed lower rates. Loan renewals and extensions on non-real-estate agricultural loans were higher in the third quarter of 2017 relative to the same quarter of 2016, with 40 percent of the responding bankers reporting more of them and just 1 percent reporting fewer. Collateral requirements for loans in the third quarter of 2017 tightened relative to the third quarter of 2016, as 22 percent of the respondents noted that their banks required more collateral and none noted that their banks required less. As of October 1, 2017, the District’s average interest rates on new operating loans and farm real estate loans had edged down to 5.16 percent and 4.84 percent, respectively; at 5.25 percent, the average interest rate on new feeder cattle loans had not changed.

Looking forward

Most survey respondents (73 percent) predicted farmland values to be stable in the fourth quarter of 2017, while 25 percent of responding bankers expected farmland values to decrease in the October through December period of 2017 and 2 percent expected farmland values to increase. In addition, respondents anticipated notably weaker demand by farmers (and to a lesser extent by nonfarm investors) to acquire farmland this fall and winter compared with a year ago. Moreover, a fairly tight supply of available properties for sale may contribute to the continued stability of farmland values. Nineteen percent of the responding bankers forecasted an increase in the volume of farmland transfers relative to the fall and winter of a year ago, and 25 percent forecasted a decrease.

Both crop and livestock net cash earnings were expected to shrink this fall and winter from their levels of a year ago, based on the predictions of survey respondents. For crops, only 2 percent of survey respondents anticipated net cash earnings to rise over the next three to six months, while 85 percent anticipated these earnings to fall. The USDA forecasted price intervals of $2.80 to $3.60 per bushel for corn and $8.35 to $10.05 per bushel for soybeans in the 2017–18 crop year; calculations using the midpoints of these price ranges and the USDA’s estimated harvest totals for the five states of the District indicate that crop revenues would be down 12 percent and 2.7 percent from a year earlier for corn and soybeans, respectively. According to responding bankers, this fall and winter, hog, cattle, and dairy farmers are expected to encounter diminished net cash earnings relative to a year ago as well, though to a lesser degree than crop farmers. Nineteen percent of the survey respondents predicted higher net earnings for hog and cattle operations over the next three to six months relative to a year ago, while 44 percent predicted lower net earnings. Similarly, 8 percent of survey respondents anticipated higher net earnings for dairy operations over the fall and winter compared with a year ago, while 39 percent anticipated lower net earnings.

Survey respondents expected loan repayment rates to decline further this fall and winter; only 2 percent of the responding bankers forecasted a higher volume of farm loan repayments over the next three to six months compared with a year ago, while 53 percent forecasted a lower volume. Furthermore, forced sales or liquidations of farm assets among financially distressed farmers were anticipated to increase in the next three to six months relative to a year earlier, according to 51 percent of the responding bankers (just 2 percent anticipated a decrease in such measures). District non-real-estate loan volume in the October through December period of 2017 was expected to be higher compared with the same period of 2016, mainly because of increases in the volumes of operating loans and loans guaranteed by the Farm Service Agency (FSA) of the USDA. With the liquidity of lenders ebbing, as seen in rising loan-to-deposit ratios, banks may increasingly need to use FSA guarantees or turn away troubled borrowers.

There was concern not only for the health of agriculture, but also for the vitality of rural economies. Nearly two-thirds of the survey respondents expressed the view that a weakening agricultural economy had led to weaker Main Street business activity, while 18 percent did not agree (and 17 percent were not certain). Until the outlook for farming improves, the economy of the rural Midwest is likely to remain constrained.