Summary

In the third quarter of 2019, farmland values for the Seventh Federal Reserve District were down 1 percent from a year ago, despite signs of strength in some areas. Moreover, according to the 170 District agricultural bankers who responded to the October 1 survey, values for “good” agricultural land were 1 percent higher in the third quarter of 2019 than in the second quarter. Although 76 percent of survey respondents expected the District’s farmland values to be stable during the fourth quarter of 2019, there was a downward tilt to the expectations of bankers, as only 6 percent of them anticipated an increase in farmland values in the final quarter of this year and 18 percent anticipated a decrease.

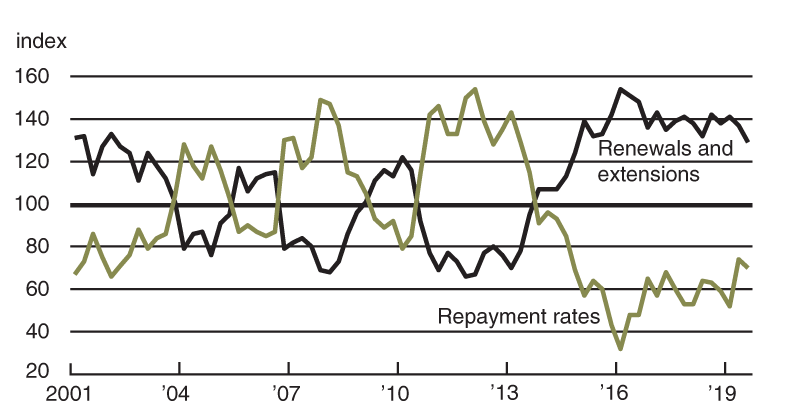

The District’s agricultural credit conditions slid yet again in the third quarter of 2019. Repayment rates for non-real-estate farm loans were down relative to the third quarter of 2018, and loan renewals and extensions were up. Demand for non-real-estate farm loans was higher than a year earlier. Also, for the first time since the second quarter of 2017, the availability of funds for lending by agricultural banks was up for a quarter relative to a year ago. In line with these results, the average loan-to-deposit ratio for the District edged down to 78.8 percent in the third quarter of 2019 from 80.2 percent in the second quarter (its all-time high). Average interest rates on agricultural loans moved down during the third quarter of 2019, which aided farm borrowers.

Farmland values

The District saw a year-over-year decrease of 1 percent in its farmland values in the third quarter of 2019. The District has not experienced a year-over-year change in its agricultural land values of greater than 1 percent over the past 12 quarters—an unprecedented streak of relative stability in farmland values. Nevertheless, there was substantial variation in farmland value changes among the District’s five states. Farmland values for Illinois and Wisconsin were down on a year-over-year basis (1 percent and 2 percent, respectively), while Indiana and Iowa farmland values were both unchanged from a year ago (see map and table below). The District’s agricultural land values were up 1 percent from the second quarter of 2019, although Illinois’s experienced a 1 percent quarterly decrease.

Challenging weather conditions during planting, a touch of drought in the summer, excess precipitation during harvest, and early frost all hampered District crop production in 2019. According to U.S. Department of Agriculture (USDA) forecasts, the five District states’ harvest of corn for grain in 2019 is projected to drop by 11 percent from 2018, to 5.88 billion bushels, and their soybean harvest is projected to drop by 21 percent, to 1.41 billion bushels (see chart 1). The District states’ corn and soybean harvests would be just the tenth and seventh largest on record, respectively. The USDA expected the nation’s corn harvest in 2019 to be 13.7 billion bushels, down 5.3 percent from 2018. The national soybean harvest in 2019 was forecasted to be 3.55 billion bushels—20 percent lower than in 2018.

1. Corn and soybean production for Seventh District states

For the third quarter of 2019, the average price of corn was 16 percent higher than a year ago, based on USDA data, while the average price of soybeans was 5.7 percent lower than a year ago. Still, given the reduced supplies of crops, the USDA recently raised its price forecasts for the 2019–20 crop year for both crops—to $3.85 per bushel for corn and $9.00 per bushel for soybeans. When calculated with these price estimates, the projected revenues from the 2019 corn and soybean harvests for District states would decrease from 2018 by 5.1 percent and 16 percent, respectively.

Livestock prices were mixed in the third quarter of 2019 relative to the same quarter of last year. Compared with a year earlier, the average prices for cattle and eggs were down 1.5 percent and 33 percent in the third quarter of 2019, while those for hogs and milk were up 12 percent and 17 percent, respectively. After a harrowing period of relatively low milk prices, the dairy sector started to regain its financial footing in the third quarter of this year.

Credit conditions

In the third quarter of 2019, agricultural credit conditions for the District were yet again worse relative to a year ago. For the July through September period of 2019, repayment rates on non-real-estate farm loans were lower than a year earlier. The index of loan repayment rates was 70 in the third quarter of 2019, as 2 percent of responding bankers observed higher rates of loan repayment than a year ago and 32 percent observed lower rates. Furthermore, renewals and extensions of non-real-estate agricultural loans were higher in the third quarter of 2019 relative to the same quarter of 2018, with 30 percent of the responding bankers reporting more of them and just 1 percent reporting fewer. For six straight years, repayment rates for non-real-estate farm loans have been lower each quarter relative to the same quarter of the year before, while loan renewals and extensions have been higher (see chart 2). Collateral requirements for loans in the third quarter of 2019 were tighter than in the same quarter of last year, as 21 percent of the respondents reported that their banks required more collateral and 1 percent reported that their banks required less.

2. Indexes of Seventh District credit conditions for non-real-estate farm loans

Source: Author’s calculations based on data from Federal Reserve Bank of Chicago surveys of farmland values.

Stronger demand for non-real-estate farm loans compared with a year ago was exhibited in the third quarter of 2019. This marked the 24th consecutive quarter (six years in a row) with such loan demand. Even so, the index of loan demand slipped to 115 in the third quarter of 2019, as 30 percent of survey respondents noted higher demand for non-real-estate loans than a year earlier and 15 percent noted lower demand. The availability of funds for lending by agricultural banks was higher than a year earlier for the first time since the second quarter of 2017. The index of funds availability rose to 103 in the third quarter of 2019, as 12 percent of the survey respondents indicated their banks had more funds available to lend than a year ago and 9 percent indicated their banks had less. With funds availability up relative to a year ago, the District’s average loan-to-deposit ratio retreated a bit from last quarter’s record high, dipping to 78.8 percent. The gap between the average loan-to-deposit ratio and the average level desired by the responding bankers widened to 4.0 percentage points. As of October 1, 2019, the District’s average interest rates on new operating loans, feeder cattle loans, and farm real estate loans had fallen to 5.71 percent, 5.77 percent, and 5.08 percent, respectively—their lowest levels in the past year.

bBankers responded to each item by indicating whether conditions in the current quarter were higher or lower than (or the same as) in the year-earlier quarter. The index numbers are computed by subtracting the percentage of bankers who responded “lower” from the percentage who responded “higher” and adding 100.

Note: Historical data on Seventh District agricultural credit conditions are available online.

Looking forward

Seventy-six percent of survey respondents predicted District farmland values to be stable in the fourth quarter of 2019, 18 percent predicted them to decrease, and 6 percent predicted them to increase. More respondents anticipated farmers to have weaker rather than stronger demand to acquire farmland this fall and winter compared with a year earlier, but the survey results showed the opposite for nonfarm investors. Additionally, respondents expected a rise in transfers of agricultural properties: 31 percent of the responding bankers forecasted an increase in the volume of farmland transfers relative to the fall and winter of a year ago, while 17 percent forecasted a decrease.

For the seventh consecutive year, crop net cash earnings were expected to contract over the fall and winter from their levels of a year earlier: 17 percent of survey respondents forecasted crop net cash earnings to increase over the next three to six months relative to a year ago, and 63 percent forecasted these earnings to decrease. According to the responding bankers, hog, cattle, and dairy farmers in the District were yet again expected to encounter diminished net cash earnings over the fall and winter relative to a year ago. Only 7 percent of the survey respondents predicted higher net earnings for hog and cattle operations over the next three to six months relative to a year earlier, while 59 percent predicted lower net earnings. Prospects for dairy operations looked slightly better, particularly as there were more survey respondents in Michigan and Wisconsin who anticipated higher net earnings for dairies this fall and winter relative to a year ago than those who anticipated lower net earnings.

Survey respondents expected loan repayment rates to decline this fall and winter from a year ago: Just 6 percent of the responding bankers forecasted a higher volume of farm loan repayments over the next three to six months compared with a year earlier, while 33 percent forecasted a lower volume. In addition, forced sales or liquidations of farm assets owned by financially distressed farmers were anticipated to increase in the next three to six months relative to a year ago, according to 54 percent of the responding bankers (only 2 percent anticipated a decrease). The District's non-real-estate farm loan volume in the October through December period of 2019 was expected to be higher compared with the same period of 2018. Similarly, the volume for District farm real estate loans was predicted to be higher in the fourth quarter of 2019 than a year earlier.

One responding banker from Indiana observed “an overall sense of unease among our farmers.” Furthermore, a survey respondent from Illinois commented on “trade issues causing most of the uncertainty and stress” among local bank customers. Though the farm sector is facing some volatility, current conditions could provide opportunities for some; as the Indiana banker wrote, “I expect this market will eliminate highly leveraged operators and allow others to expand their operations.”

Sources: Author’s calculations based on data from the U.S. Department of Agriculture, U.S. Bureau of Labor Statistics, and the Association of Equipment Manufacturers.

CONFERENCE REMINDER

Improving Midwest Agriculture and the Environment

On November 20, 2019, the Chicago Fed will hold a conference to examine environmental issues related to Midwest agriculture, with a particular focus on conservation practices. To register, go to the event page.