Honda and tax incentives

Honda recently decided on a site in Indiana for its new North American auto assembly plant over sites in Ohio and Illinois. Indiana offered Honda generous incentives of EDGE tax credits, training assistance, and real and personal property tax abatements totaling up to $41.5 million. In addition, the state will provide infrastructure support for water, wastewater, and road improvements of approximately $44 million. This offer was generous relative to packages that have been offered lately by northern states to woo automotive plants. Did the incentives swing the deal for Indiana? And how can states hope to recoup these upfront costs and revenue losses? More importantly, is society well served by such raw-knuckled competition among states for production facilities? The answers are not definitive, but, though often condemned, the use of fiscal incentives may not be such a bad thing.

Large offers of this nature have become commonplace. Speaking at the Chicago Fed’s recent symposium on the automotive parts industry, Sean McAlinden of the Center for Automotive Research reported that the state of Georgia offered Korean carmaker KIA a package estimated to be worth $409 million. This was noticeably larger than the recent average offers of $57 million in tax incentives for automotive assembly plants for northern states and $44.2 million (plus free or subsidized infrastructure and job training) for southern states.

On completion of such deals, company representatives often proclaim that the incentives did not determine the choice of location, but were rather a sweetener or a comforting pledge of good faith. Professional site selection analysts tend to echo these sentiments. Taking such statements at face value, why do states offer such high stakes packages?

No doubt, there are benefits at the ballot box to those elected officials who can brag about bringing jobs and income to the state. It has been argued that these benefits, especially for investment projects that loom large in the media, result in overly generous offers and poor decision-making by state officials. This is one reason that some states enact legal requirements making the terms of such deals easily available to public scrutiny.

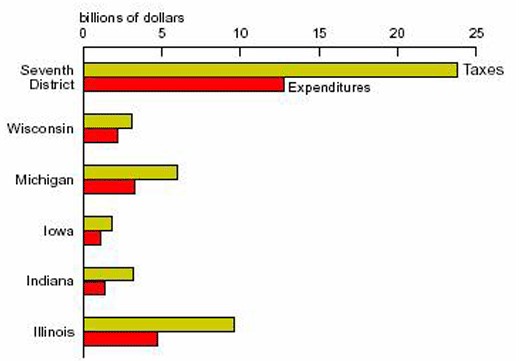

But how can states afford to make such offers? One reason is that the public service costs of hosting businesses are usually lower than the taxes paid by them; that is, there is typically a fiscal surplus inherent in state business tax systems that allows state officials to discount the public tax and service bills on new investment. When I examined the likely costs of public services provided to businesses in a 1996 study, I found that, across all U.S. regions, direct business taxes tended to exceed the value of direct service benefits provided to business by a ratio ranging from 1.5:1 to 2:1. This excess may allow room for governments to lower business tax bills through selective incentives.

Figure 1. State and local business taxes vs. local expenditures, Seventh District, 1992

Even so, opponents of the use of selective tax abatements may argue that incentives were unnecessary and that businesses have an information advantage in bargaining with states for incentives even when they will end up choosing the same location in any event. Certainly, the proclamations of businesses that afterwards contend that incentives were not a primary consideration in their location decision bear this out. If so, states are arguably better off refraining from incentives and instead spending the business tax bounty on public services or returning personal taxes to state residents.

In the case of auto plants, it is interesting to note that even if individual states “give away the store” in luring a particular auto assembly facility, the end result may ultimately benefit the state’s economy. The reason is that the assembly plants typically attract auto parts suppliers to the area. As Chicago Fed economist Thomas Klier has shown (below), a typical assembly plant can draw a significant nearby supplier base. For recently opened assembly plants in North America, an average of 19 to 20 direct suppliers have typically opened up within 60 miles of the plant. More generally, assembly plants tend to pull in many more supplier plants within several hundred miles, and supplier plant employment generally exceeds assembly plant employment by around 3.5:1.

It is true that in the case of the Honda assembly plant in Greensburg, IN, many of the supplier plants will be outside Indiana’s border and tax reach. However, if all or many adjacent states are successful in attracting assembly plants, the spillover benefits of taxation and income will accrue in roughly equal measure to the states. A so-called cluster of automotive production capability may be achieved for the multi-state region.

Table 1. Assembly plants and suppliers

But are the incentives necessary to achieve or preserve the region’s cluster of automotive plants? At least for highly capital-intensive industrial activities such as manufacturing, the so-called business climate of the state is paramount. Placement of an expensive investment by a company in a state must be based on a strong conviction that future government leaders will not expropriate the facility’s value through regulation, over-taxation, or non-cooperation in future land use and public infrastructure needs. The situation is not unlike making investments in a foreign country. When the capital investment is fixed and not easily moved, confidence in local government is a key factor in assessing investment risk.

In this regard, Honda’s decision to locate in Indiana rather than Ohio is understandable. While proximity to its large suppliers in Ohio and vicinity was a compelling reason for considering Indiana, the desirability of diversification among government entities may have also been a factor. As for the incentive package, there is surely more to a favorable state business climate than a flashy offer of tax incentives. But at the same time, the offer of a fiscal incentive package may be a strong signal to the business that its presence will be valued. In addition, a sizable and highly visible tax incentive package may represent an implicit acknowledgment by the state that the investment is wanted, making it more difficult for future political leaders to renege on the state’s cooperative relationship with the company.

Of course, implicit tax incentive contracts of this sort work both ways. Companies that receive generous tax incentive packages, but later do not deliver on promised jobs and investments, are easy targets for retribution by state officials. In many instances today, “clawback” provisions are included upfront that eliminate favorable tax treatment if companies do not deliver.

Even so, the “gold standard” by which public policies must be judged is whether the state could possibly do better. Opponents of tax incentives for business argue that, because of such tax breaks, critical public services such as education remain underfunded. In particular, public education suffers, contributing to sub-par income growth and exacerbating social problems such as crime, poor electoral participation, and poor public health. If we accept this view, the economic returns to the practice of competitive business tax incentives are not optimal; the economic returns from any short-term job and income gains to the local economy are less than the foregone returns that greater education spending would bring locally and nationally.

In rebuttal, one might argue that business taxes are not the only possible source of revenue for highly valued public services such as education. An ideal of government is one in which citizens understand both the value of public services provided and the real costs of these benefits and, subsequently, make their choices known at the ballot box.

With the tendency among governments to over-tax business activity, the electorate may believe that they are getting a free ride for public services—that they are not in fact paying for these services. But they are usually mistaken. People and households end up (indirectly) paying for public services in any event. After all, business taxes are ultimately reflected in higher product prices paid by state residents or in lower wages and salaries paid to employees.

So why do many voters and even some policy analysts advocate the taxation of business activity to finance public services that primarily benefit households? Some argue that Americans like their taxes hidden and furthermore that this is a reasonable way for governments to finance high-payoff public services. But this approach has risks. If taxes and prices for public services are hidden, can the citizenry really make sensible decisions about what levels, types, and extent of services government should provide? What do you think?