The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Today, a good or service produced in a remote part of the world can compete with a local good or service more easily than 20 years ago. To some extent, this change is due to advances in technology (such as telecommunications) and to widespread economic development. But it is also due to trade liberalization, much of which can be attributed to the General Agreement on Trade and Tariffs (GATT), the world’s joint mechanism for regulating international trade and trade negotiations. Since GATT’s inception after World War II, more than 110 countries have joined. In addition, regional trading blocs have united countries in several regions of the world. These blocs reduce or eliminate tariffs among members, which in turn makes members’ goods less costly and more competitive in the world market. The European Economic Community, the Central American Common Market, and the U.S.- Canada Free Trade Agreement are just a few examples of regional trading blocs in existence today. The proposed North American Free Trade Agreement between the U.S., Canada, and Mexico is another.

Foreign trade and competition affect not only countries and world regions, but also local regions such as the Federal Reserve Seventh District (which includes most of Illinois, Indiana, Michigan, and Wisconsin, and all of Iowa). For example, prior to the 1960s, the Big Three automakers (General Motors, Chrysler, and Ford), which are headquartered in the District, had a substantial stronghold on vehicles produced and sold within the U.S. But thanks to aggressive marketing, differentiated products, and other factors, foreign auto producers managed to enter the U.S. market on a major scale. Between 1965 and 1992, they grew from 7% to 25% of total U.S. retail auto sales.

Many factors affect a nation’s or region’s ability to compete in a global marketplace such as this, where goods and services readily cross borders. This Chicago Fed Letter examines three of these factors: export performance, foreign direct investment in the U.S., and migration.1

Exports

Exports play a vital role in a nation’s economy. In the short term, they reflect production activity. In the long term, they create foreign exchange, which in turn enables purchases of foreign goods, services, and capital. Additionally, exports create and maintain jobs. In 1990, an estimated 7.2 million jobs in the U.S. were export-related—more than 7% of the civilian work force. Within the manufacturing sector, the figure was 17%. Export-related jobs earn nearly 17% more than nonexport-related jobs.2

In 1992, U.S. merchandise exports totaled $448 billion.3 Of this amount, $403 billion were manufacturing exports. More than half of all manufacturing exports came from three industries—transportation equipment, nonelectrical machinery, and electrical machinery. Between 1987 and 1992, U.S. manufacturing exports increased nearly $187 billion. As a percentage of GDP, they increased from 7% or 8% in the mid-l980s to over 11% in 1992.

Three-fourths of total 1992 manufacturing exports went to Europe, Southeast Asia, and Canada. Yet over the period 1987-92, manufacturing exports to Mexico experienced the largest percentage increase, up 183% from $13 billion to nearly $38 billion.

Agricultural exports are also important to the U.S. economy, representing approximately 10% to 12% of total U.S. exports over the last 5 years.4 Between 1987 and 1991, the value of U.S. agricultural exports increased 37% to about $40 billion.5

The Seventh District produced $57 billion worth of exports in 1992, about 13% of the U.S. total. District manufacturing exports totaled $55 billion, or 14% of U.S. manufacturing exports. Of District manufacturing exports, 32% were in electrical and nonelectrical machinery, while 31% were in transportation equipment. In 1992, Seventh District manufacturing exports to Canada ranked first in terms of value ($25 billion), accounting for nearly half the District’s exports in that category. Between 1987 and 1992, District exports to the Middle East experienced the largest percentage increase, up 108% to over $2 billion.

The U.S. has not just increased trade with its larger partners. It is also sending a steadily growing stream of exports to smaller economies, including developing and newly industrialized countries (see figure 1).6 As those countries’ economies continue to grow, so will their demand for the types of goods and services that the U.S. produces.

1. 1992 manufacturing exports by destination

| US | Seventh District | |||

|---|---|---|---|---|

| Destination | Billions of Dollars | % change since 1987 | Billions of Dollars | % change since 1987 |

| Europe | $109 | 78 | $11 | 81 |

| Southeast Asia | 102 | 101 | 8 | 99 |

| Canada | 84 | 67 | 25 | 30 |

| Mexico | 38 | 183 | 4 | 103 |

| South America | 22 | 89 | 2 | 67 |

| Middle East | 18 | 71 | 2 | 108 |

| Central America | 11 | 66 | 0 | 40 |

| Pacific Islands | 10 | 66 | 1 | 56 |

| Africa | 6 | 4 | 0 | –2 |

| Total Manufacturing Exportsa | $403 | 87 | $55 | 54 |

Foreign direct investment

Foreign direct investment (FDI), both in the U.S. and abroad, also has a major impact on the U.S. and the Seventh District.7 Foreign companies invest in the U.S. for a variety of reasons—more favorable U.S. market growth, lower production costs, or the availability of skilled labor, technology, and physical infrastructure. Companies may also invest abroad to circumvent high import tariffs or import quotas, or because home-country governments are politically unstable. In addition to jobs, foreign affiliates bring new technologies and contacts that may benefit U.S. industries. For example, many of the changes taking place today in the U.S. auto industry—lean manufacturing, just-in-time inventories, and so on—are a result of efforts by U.S. manufacturers to compete with Japanese transplant operations.

FDI is a two-way street; that is, foreign companies invest in the U.S. and U.S. companies invest abroad. Of course, foreign investment in the U.S. helps keep jobs and physical plants in this country—an attractive benefit, particularly in the eyes of the general public. Nevertheless, U.S. direct investment abroad also benefits the U.S., since overseas earnings may ultimately be repatriated. If a company maintains a U.S. headquarters, it also keeps professional jobs and higher wages here. Finally, U.S. direct investment abroad allows U.S. firms to sell products with less costly components—a benefit to consumers.

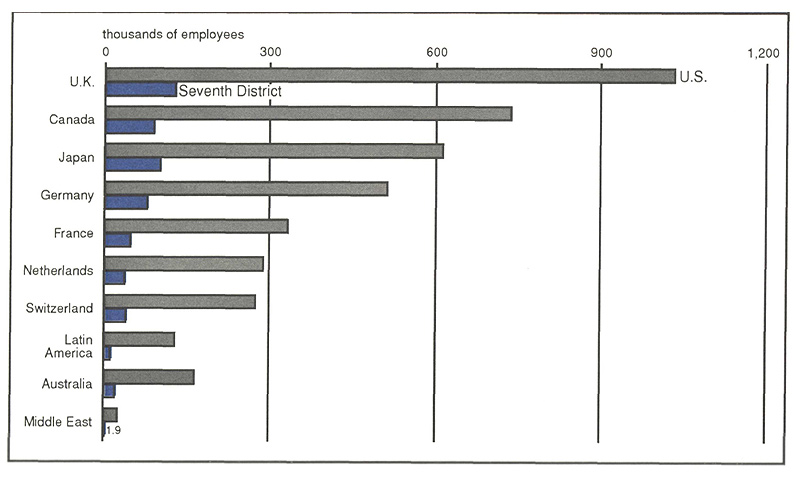

The total number of foreign affiliates in the U.S. increased from 2,999 in 1977 to 6,857 in 1990, up 129%. Over the same period, total employment at these affiliates increased by 4 million, or 289%. As figure 2 indicates, the United Kingdom had the largest number of employees in U.S. foreign affiliates in 1990, followed by Canada and Japan.

2. 1990 employment in foreign affiliates by country of ownership

In the Seventh District, increases in the number of foreign affiliates between 1977 and 1990 ranged from 223 (168%) in Iowa to 790 (105%) in Illinois. Employment at foreign affiliates in the District increased by 440,000, or 238%, over the same period (see figure 3). This relatively strong increase in FDI in what had been a lagging U.S. region has contributed in part to the region’s current economic revival.

3. 1990 employment in foreign affiliates (in thousands)

| All Industries | Total mfg. | Machinery | Other mfg. | Trade | Services | |

|---|---|---|---|---|---|---|

| Illinois | 243 | 125 | 30 | 35 | 60 | 28 |

| Indiana | 125 | 89 | 27 | 22 | 18 | 10 |

| Iowa | 37 | 22 | 4 | 8 | 10 | 1 |

| Michigan | 143 | 78 | 19 | 26 | 32 | 8 |

| Wisconsin | 79 | 49 | 14 | 14 | 13 | 7 |

| U.S. | 4,674 | 2,185 | 506 | 660 | 1,190 | 548 |

Migration

Persons entering the U.S. are either residents of foreign countries (aliens) or U.S. citizens. Aliens may enter either for brief visits as commuters or crewpersons of vessels or aircraft, or as immigrants—persons with permanent resident documents, refugee travel documents, or immigrant visas.

Like foreign direct investment, migration brings new technologies and skills to the U.S. To a lesser extent, it also brings capital investment and entrepreneurship. In addition, because many services such as business consulting are transportable through people, the ability to travel freely is vital for services growth.

In 1991, 455 million people entered the U.S.—294 million aliens and 161 million U.S. citizens. In the same year, almost 2 million immigrants (many of whom had entered the country in earlier years) were granted permanent resident status. By occupational group, over 900,000 of these immigrants were in farming, forestry, and fishing. Another 100,000 were operators, fabricators, or laborers, while 58,000 were in professional specialties and technical occupations. About 42 million people entered the Seventh District in 1991—a 57% increase over 1987. Immigrants admitted to the District in 1991 numbered 103,000.

State programs also promote trade

While much discussion to date has focused on federal programs that promote trade, state and regional policymakers have not overlooked the importance of competing in a global marketplace. Budgetary stress has led many state governments to cut back on development services, yet state export promotion programs continue to expand. These usually comprise a mix of services including market or strategy development and trade shows or leads. Some states also offer export financing.

The two most frequently used and effective tools of state governments to promote trade and investment are foreign offices and foreign trade zones. In 1986, there were 44 state foreign offices in Europe and the Far East. By 1991, there were 64, with the bulk of the new ones in Japan, China, Korea, Taiwan, and Hong Kong.

A foreign trade zone (FTZ) is an area in the U.S. into which goods can be imported duty-free until they are reexported or formally imported into the country. A warehouse, industrial park, or manufacturing or assembly plant can be designated an FTZ. A company using an FTZ pays duty on imported goods only when those goods actually leave the FTZ and enter the domestic market. Thus, the company never pays import duties on damaged goods or goods that it reexports. Also, goods that are substantially transformed within an FTZ are subject to a different (often reduced) import tariff than the original good would have been. In 1990 the nation had 383 FTZs. The Seventh District had 72.

Public or quasi-public organizations, such as port authorities or state economic development agencies, usually establish FTZs in order to bring jobs and other business opportunities to an area. FTZs increase the global attractiveness of an area by reducing costs to U.S. firms that use foreign inputs, and also by acting as storage or distribution facilities for foreign firms that do business in the U.S. Regional policymakers can also create FTZs to strengthen regional ties and promote a common interest in increased trade and investment.

Conclusion

In order to compete successfully with other countries, the U.S. must make use of all available opportunities. Exports and foreign investment help create and maintain US.jobs—a major goal of policymakers. In addition, they help the U.S. take advantage of new technologies and skills. Migration, both in the U.S. and abroad, also serves this goal. Together, these facts make clear that federal and state policies to foster and maintain international ties can enhance the competitive position of U.S. and District firms.

Purchasing Managers Surveys (production index)

Manufacturing output index (1987=100)

| July | Month ago | Year ago | |

|---|---|---|---|

| MMI | 119.0 | 118.5 | 111.7 |

| IP | 111.1 | 111.0 | 107.2 |

Motor vehicle production (millions, saar)

| August | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.0 | 5.4 | 5.4 |

| Light trucks | 4.3 | 4.0 | 3.7 |

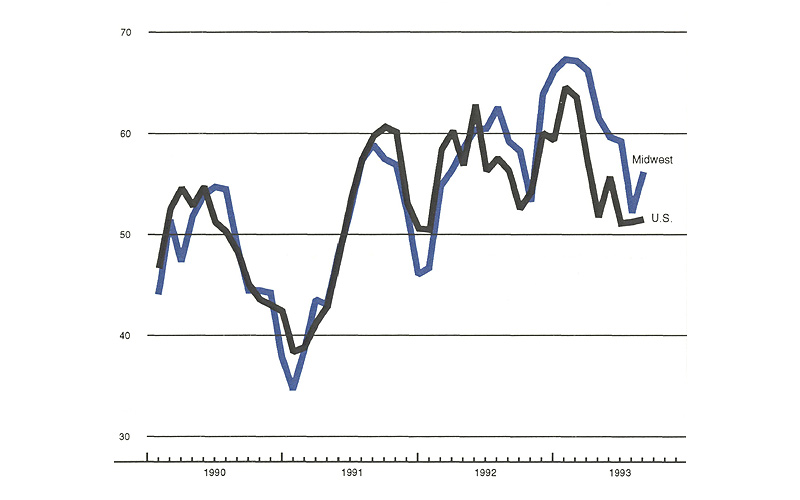

Purchasing Managers' Surveys: production index

| August | Month ago | Year ago | |

|---|---|---|---|

| MW | 56.3 | 52.3 | 59.3 |

| U.S. | 51.6 | 51.3 | 56.4 |

Purchasing Managers Surveys (production index)

Purchasing managers’ surveys show a slowdown in Midwest industrial growth in recent months from a relatively high growth rate earlier in the year. This pattern has been echoed in the Midwest Manufacturing Index. Activity normally slows considerably during late summer, but a loss of momentum was still apparent on a seasonally adjusted basis. Auto assemblies have lagged schedules made earlier in the year, and output gains have slowed for some other items important to the regional economy, including appliances, heavy-duty trucks, and primary and fabricated metals.

Auto sales softened in August and early September, but the weakness was due in part to low inventories and a pullback from fleet sales. Car production plans for the fourth quarter are expected to boost assemblies in the Seventh District by roughly 15% from the third quarter on a seasonally adjusted basis.

Notes

1 These factors and others are described in more detail in a forthcoming publication of the Federal Reserve Bank of Chicago, Regional Economics in Global Markets. This booklet, addressed to government officials, analysts, and businesspeople, examines a variety of tools that the nation and its regions can use to promote international ties. In addition to the tools discussed in this article, the booklet discusses others, such as foreign banking.

2 Lester A. Davis, “U.S.jobs supported by merchandise exports,” U.S. Department of Commerce, Economics and Statistics Administration, April 1992.

3 U.S. exports include those from Puerto Rico and the U.S. Virgin Islands.

4 Agricultural goods are defined as nonmarine food products and other products of agriculture that have not passed through a complex manufacturing process. They include fibers, raw hides and skins, fats and oils, and beer and wine.

5 U.S. Department of Agriculture, Foreign Agricultural Trade of the United States, 1991.

6 For an overview of these trends, see Bruce Kasman, “Recent U.S. export performance in the developing world,” Quarterly Review, Federal Reserve Bank of New York, Winter 1992-93.

7 Foreign direct investment refers to ownership or control of physical facilities located on foreign soil. Ownership is defined as a 10% interest.