The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

In early July 1997, the Thai baht was devalued following a speculative attack by currency traders. The fallout from this event went far beyond the usual consequences of speculative currency attacks. Devaluations followed in Malaysia, the Philippines, Indonesia, and South Korea. In all five countries, economic activity went into a tailspin. As shown in figure 1, the declines in industrial production following the currency crises were of magnitudes associated with economic depression. These declines are especially noteworthy in light of the extraordinary economic growth in these countries during the years preceding the crisis, demonstrated in the third and fourth columns of figure 1.

1. Impact of Asian crisis on industrial production

| % change in industrial production | ||||

| Country | Date of float |

Prior 5 years |

Prior 12 months |

Following 12 months |

| Indonesia | August 15 | 76.1 | 17.3 | -18.7 |

| South Korea | November 17 | 53.0 | 5.4 | -4.6 |

| Malaysia | July 14 | 72.2 | 13.8 | -11.6 |

| Philippines | July 11 | 76.8 | 7.6 | -5.8 |

| Thailand | July 2 | 35.5 | 2.6 | -11.6 |

Source: Data Resources, Inc. (Thailand, Indonesia); International Financial Statistics (South Korea, Malaysia, Philippines).

Given the huge collateral damage to these countries’ economies, most economists agree that the 1997 crisis goes well beyond the usual case of an overvalued currency being forced by currency traders to realign its exchange rate. Massachusetts Institute of Technology economist Paul Krugman makes this point forcefully: “[T] he currency crises were only part of a broader financial crisis, which had very little to do with currencies or even monetary issues per se.”1

In this article, we focus on one important piece of the puzzle: “Was the crisis foreseen?” This question is important because it may help us decide between two distinct classes of candidate explanations. Following Paul Krugman, we may call these two candidates the “fundamentalist” and “self-fulfilling” approaches.2

The fundamentalist approach holds that the crisis resulted from a gradual accumulation of structural imbalances. Observers point to accounting practices that had inadequate transparency, bank loan decisions being made for political reasons rather than for sound economic rationales, and a legal infrastructure inadequate for a modern capitalist economy. For example, at the time of the 1997 crisis Thailand did not even have a well-functioning bankruptcy code.3 Even more strikingly, Indonesia’s bankruptcy law, drafted by the Dutch in 1905, remained unchanged through 1997 and had never even been translated from Dutch into the native language!4 Most notably, the banking sector in many of these countries had severe problems, with a vast accumulation of unrecognized bad loans.

The self-fulfilling approach holds that the crisis ultimately reflected a reversal in investor beliefs about the future economic prospects of the crisis countries. According to this explanation, this reversal in beliefs led investors to pull capital out of East Asia, causing the very economic downturn that the investors feared. In this sense, the reversal represented a self-fulfilling prophecy.

Which of these two approaches best explains the events of 1997? A key piece of evidence is whether the crisis was foreseen by investors. Under the fundamentalist approach, the crisis resulted from years of fundamental problems. These problems were common knowledge to investors and were perceived well before the speculative attacks that marked the onset of the full-blown crisis. For example, Burnside, Eichenbaum, and Rebelo5 provide evidence that the poor quality of bank assets was well known months or even years before the devaluations that marked the beginning of the crisis. Investors would have known that as these problems became worse, the odds favoring a severe financial crisis (including a currency devaluation) were increasing. The model of Burnside, Eichenbaum, Rebelo (1998) implies that the Thai devaluation could have been foreseen over two years before the devaluation occurred. Financial markets would react to the increased probability of devaluation by bidding up nominal interest rates and forward exchange rates (in dollars per own-currency). We therefore would see these financial indicators move prior to the onset of the crisis.

Evidence that the crisis was not foreseen by financial markets would represent a challenge for the fundamentalist approach. However, it would be easier to reconcile with the self-fulfilling approach. Investor sentiment is crucial for generating a self-fulfilling crisis. A crisis can result if investors switch from optimism to pessimism about future economic prospects. In principle, there is no reason why such a shift in sentiment need be foreseen by financial markets.

Evidence from financial markets

To measure whether the large currency devaluations were foreseen, we look at foreign exchange forward rates and nominal interest rates (denominated in the Asian countries’ currency). If investors forecasted an increase in the probability of a foreign exchange crisis, these rates would have responded before the actual beginning of the crisis.

We use daily data from Malaysia, Indonesia, and Thailand. We choose these countries because we were able to obtain exchange rate and interest rate data from offshore trading for these three currencies. The offshore aspect of these contracts is important, since it means that these data are market based and have not been manipulated in any way by domestic authorities. Our data are from Bloomberg Financial Markets, based on contracts issued and traded by Prebon Yamane Asia, an offshore brokerage firm based in Hong Kong.

The data we use for nominal interest rates are daily cross-currency interest rate swap contracts. In an interest rate swap, one party pays a fixed interest rate on some principal, or notional, amount, while the other party pays a floating rate on the notional amount that is based on some common quoted source, such as the six-month LIBOR (London interbank offered rate). For a cross-currency interest rate swap, the fixed rate is paid in one currency while the floating rate is paid in a different currency. These swaps are often used for risk-sharing purposes, such as when a company has floating debt outstanding in a foreign currency that it would like to replace with fixed-rate payments in its domestic currency. The price quotes for the interest rate swap contracts are the fixed semi-annual rate paid in the domestic Asian currency, with the six-month U.S. dollar-denominated LIBOR as the floating index rate. The purchaser of this swap has conceptually purchased a U.S. dollar floating rate note and issued a coupon bond denominated in the home currency.

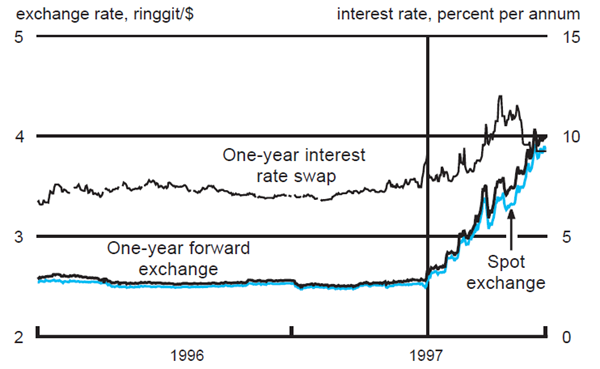

Any change in market predictions of future exchange rates should be reflected in these data. If a large future currency devaluation was foreseen, the forward exchange rate should increase, with an associated rise in the nominal interest rate.6 Figures 2 through 4 provide evidence on whether the Asian devaluations in 1997 were foreseen. They plot the spot exchange rate versus the U.S. dollar, the forward currency rates for delivery in one year, and the rates from the one-year swap contracts over the two-year period 1996-1997. The vertical lines give the date of devaluation.7

In Malaysia, the forward exchange rate does not budge until the speculative attacks on July 12, two days before the official devaluation (figure 2). The interest rate starts increasing on July 9, only three days prior to these speculative attacks and one week after the devaluation in neighboring Thailand. In Indonesia, neither the forward exchange rate nor the interest rate moves appreciably from its previous level until July 11, the date when the Indonesian central bank widened the trading band for the rupiah (about a month before the full devaluations on August 15, indicated by the vertical line in figure 3). In these countries at least, there is essentially no evidence that the financial markets foresaw the onset of the crisis.

2. Malaysian financial rates

Source: Bloomberg Financial Markets.

3. Indonesian financial rates

Source: Bloomberg Financial Markets.

In Thailand, financial markets moved approximately six weeks before the devaluation date. In particular, the forward exchange rates started to depreciate on May 15 (note the upward drift in figure 4), while the spot exchange rates actually started to appreciate. At that time, the nominal interest rates also started a pronounced upward movement, reaching levels exceeding 50% per annum in mid-June. Does this indicate that financial markets foresaw the crisis in Thailand (if only by six weeks)? The evidence suggests not. Rather, the initial increases in forward rates coincided with the onset of the crisis. In particular, these dynamics reflect the strategy chosen by the Bank of Thailand (BOT) to defend the baht following intense speculative attacks starting on May 7.

4. Thai financial rates

Source: Bloomberg Financial Markets.

As documented by Subir Lall of the International Monetary Fund,8 speculators launched their attack by taking short positions in forward baht contracts. The BOT’s defense was to squeeze these short positions. From May 8 through May 14, the BOT took long positions in forward baht contracts. On May 15, however, it stopped intervening in the forward market. This explains the increased forward baht rates starting on that date that are evident in figure 4. Rather, it started squeezing pre-existing short positions by aggressively raising baht interest rates (again, evident in figure 4) and by applying severe constraints on domestic banks’ baht transactions with offshore traders. These actions made it extremely expensive for foreign speculators to cover their short baht positions. The resulting scramble for baht is reflected in the baht appreciation from May 15 through the end of June that is apparent in figure 4.

Initially, the BOT’s defense of the baht appeared quite successful. On May 16, Therapong Monthienvichienchai, head of the Asian foreign exchange department of Deutsche Morgan Grenfell in Singapore, declared the BOT a clear winner. “In pushing interest rates up this high, we can say that the Bank of Thailand has won the battle, but of course, not the war.”9 Mr. Therapong’s words proved prophetic. The BOT was able to maintain its defense for six weeks. However, the BOT’s strategy could not be continued indefinitely. It required extremely high interest rates, coupled with effective segmentation of the onshore and offshore currency and swaps markets. Both of these policies imposed huge costs on domestic Thai businesses (especially importers). As we know, the defense was abandoned in early July, at which point there was no longer any need to keep interest rates at the extreme levels of the preceding weeks.

Conclusion

According to the evidence presented here, the Asian crisis was largely unforeseen. There is no evidence in the offshore currency or interest rate swaps markets for Thailand, Malaysia, or Indonesia that investors perceived an increased risk of devaluation prior to the onset of the crisis. This represents a substantial challenge to explanations that focus purely on economic fundamentals as the key determinants of financial crises. It suggests that investors did not interpret the problematic fundamentals in these countries (pointed to with the advantage of hindsight by observers) as precursors of crisis. Rather, it appears that the state of fundamentals was seen as consistent with continued economic and financial strength. This evidence favors the argument that there was an element of self-fulfilling prophecy in this crisis. Having said this, it must be noted that fundamentalist and self-fulfilling explanations can coexist. It may be that a self-fulfilling crisis can never occur if fundamentals are sufficiently strong. If fundamentals are weak, a self-fulfilling crisis may be possible, but not inevitable. The actual timing of a crisis would still be difficult to predict.

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| September | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 167.5 | 167.2 | 156.0 |

| IP | 151.8 | 151.3 | 142.9 |

Motor vehicle production (millions, seasonally adj. annual rate)

| October | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.2 | 5.8 | 5.7 |

| Light trucks | 6.7 | 6.9 | 7.1 |

Purchasing managers' surveys: net % reporting production growth

| November | Month ago | Year ago | |

|---|---|---|---|

| MW | 44.1 | 51.4 | 62.0 |

| U.S. | 49.6 | 48.4 | 58.6 |

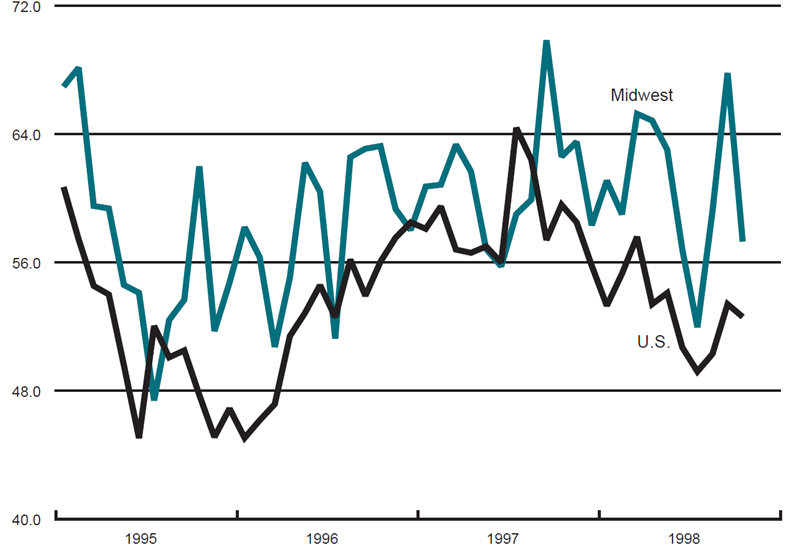

Manufacturing output indexes, 1992=100

The Chicago Fed Midwest Manufacturing Index (CFMMI) rose 0.2% from August to September, reaching a seasonally adjusted level of 167.5 (1992=100). Revised data show the index was at 167.2 in August. The Federal Reserve Board’s Industrial Production Index for manufacturing (IP) increased 0.3% in September.

Auto production decreased from 5.8 million units in September to 5.2 million units in October, and light truck production also decreased from 6.9 million units in September to 6.7 million units in October. The Midwest purchasing managers’ composite index (a weighted average of the Chicago, Detroit, and Milwaukee surveys) for production decreased to 44.1% in November from 51.4% in October. The purchasing managers’ index decreased in all three surveys. The national purchasing manager’s survey increased from 48.4% to 49.6% during this period.

Notes

1 Paul Krugman, 1998, “What happened to Asia?” Massachusetts Institute of Technology, working paper.

2 Paul Krugman, 1999, “Balance sheets, the transfer problem, and financial crises,” Massachusetts Institute of Technology, manuscript, January.

3 See Bertrand Renaud, Ming Zhang, and Stefan Koeberle, 1998, “How the Thai real estate boom undid financial institutions—What can be done now?” paper presented at the National Economic and Social Development Board seminar on Thailand’s Economic Recovery and Competitiveness, Bangkok, May 20.

4 See Tim Dodd, 1999, “Indonesia rewrites its bankruptcy laws,” Australian Finance Review, April 30, cited in John Walker, 2000, “Building an infrastructure for financial stability: Legal and regulatory framework,” paper presented at Federal Reserve Bank of Boston Conference on Building an Infrastructure for Financial Stability, June 21–23.

5 Craig Burnside, Martin Eichenbaum, and Sergio Rebelo, 1998, “Prospective deficits and the Asian currency crisis,” Federal Reserve Bank of Chicago, working paper, No. WP-98-5.

6 Since the spot and forward exchange rates are in units of Asian currency per dollar, an increase in these exchange rates represents a devaluation.

7 The discontinuities in the plots in these figures represent missing data. This problem is particularly severe for the forward exchange rate in Indonesia, where we obtained very few quotes prior to October 1996.

8 Subir Lall, 1997, “Speculative attacks, forward market intervention, and the classic bear squeeze,” International Monetary Fund, working paper, No. WP / 97 / 164.

9 “Speculators routed, but war far from over,” Bangkok Post, May 16, 1997.