Introduction and summary

Regulatory reforms in the wake of the 2007–08 financial crisis have increased the focus on the systemic importance of central counterparties (CCPs), which guarantee the performance of their clearing members’ financial contracts.1 This, in turn, has increased policymakers’ and practitioners’ focus on risk management at CCPs. A key component of any CCP’s risk-management strategy is the CCP’s default waterfall. The default waterfall stipulates the sequence of financial resources that a CCP can draw upon to cover the unsatisfied financial obligations of a defaulted clearing member. At the top of the waterfall are the margin and default fund contributions of the defaulting clearing member.The remainder of the waterfall comprises contributions from the CCP, known as skin-in-the-game, and contributions from clearing members. This article describes how the structure for these CCP- and member-funded tranches affects how the interests of CCPs, clearing members, and their prudential regulators are aligned.

Complicating the determination of an appropriate default waterfall framework is the fact that CCP ownership structure affects the incentives created by a CCP’s default waterfall design. In this article, we examine three CCP ownership structures: quasi-national, demutualized, and mutualized CCPs.2 There has been little public policy discussion about the role of CCP ownership structure in determining how effectively a CCP’s skin-in-the-game aligns its own incentives with those of its clearing members. Also neglected in policy discussions have been the ways in which variations in the amount of a CCP’s skin-in-the-game might affect the degree to which such incentives are aligned. This article attempts to address both issues.Default waterfall overview

All CCPs have a default waterfall that provides financial resources for managing a clearing member default. The waterfall consists of both prefunded resources and unfunded obligations. When a clearing member defaults, the CCP must continue to meet defaulter’s financial obligations, whose performance it guarantees, to the nondefaulting clearing members, attempt to find clearing members willing accept the defaulter’s clients, and return to a matched book status by liquidating or auctioning off the defaulter’s positions. If the CCP cannot find other clearing members willing to onboard the defaulter’s clients, then the clients’ positions must be liquidated in order to restore the CCP to a matched book status. The default waterfall provides funding to cover the cost of meeting the defaulter’s obligations and liquidating the defaulter’s positions, as well as, if necessary, those of its clients.

The default waterfall structures recommended in this article include contributions from both clearing members and CCPs. To understand why it is crucial for both clearing members and CCPs to contribute financial resources to the default waterfall, we first describe the incentives that would arise if this were not the case.

Default waterfall entirely funded by CCP: No mutualization of risk

Imagine a CCP default waterfall model where the waterfall contained no contributions from clearing members. The default waterfall would be composed exclusively of the defaulting member’s margin and the CCP’s capital. There would be little to no clearing member participation on the CCP’s risk committee as none of the clearing members would be exposed to the financial repercussions associated with the potential failure of another clearing member. No risk, no representation. This model would be fraught with moral hazard because clearing members, having no real financial risk associated with the CCP, would have little incentive to monitor the quality of the CCP’s risk management or observe the conduct of other clearing members in the marketplace. Client porting3 would likely be more challenging as clearing members could afford to be extraordinarily selective in the clients that they onboarded, knowing that any shortfall associated with the liquidation of the orphaned clients’ positions would fall exclusively upon the CCP. In order to fund such a waterfall, the CCP’s fee structure would have to far exceed current industry norms and could be so expensive as to discourage the use of the relevant derivative products by market participants.

On the bright side, it would likely be easy to involve clearing members in the auction of the open positions of a defaulted clearing member because traders would know ex ante that any default shortfall would be borne solely by the CCP. Bids might be low, but there should be no shortage of them. This model would also allow the CCP to demonstrate its confidence in its margining model as it would have exposed a significant amount of its capital to the effectiveness of its margining system.

Default waterfall entirely funded by members: Full mutualization of risk 4

At the other extreme would be a CCP default waterfall model where the entire waterfall, after the defaulter’s initial margin and default fund contribution, was funded by clearing member contributions. This model would preclude the CCP from making any credible professions about the robustness of its margin system. No risk, no credibility. There would likely be significant conflict over the power and composition of the CCP’s risk committee as all of the financial risk of clearing would fall upon the clearing members. Moral hazard would not be a problem, because clearing members would be diligent in monitoring the CCP’s risk-management practices and the observable trading practices of the other clearing members. That said, clearing membership criteria might become so rigorous that they would significantly deter the entrance of new clearing members.

This model does have some advantages. Clearing members would have a greater interest in the auction of the defaulter’s positions succeeding and so would bid more aggressively than if the default waterfall contained no clearing member contributions; if the auction failed, they would be responsible for a portion of any mutualized liquidation loss that exceeded the defaulter’s initial margin and default fund contribution. Similarly, surviving clearing members would have an increased incentive to onboard orphaned clients. A failure to do so would lead to the auction of the orphaned clients’ open positions, with any financial shortfall absorbed by the mutualized default fund. With financial backing from clearing members, the CCP could operate with a fee structure that would be favorable enough to attract end-user market participants and provide a livelihood for client clearing trade intermediaries. Clearing members would have no difficulty characterizing and marketing their services as providing credit intermediation to their clients, as the clearing membership would be providing the CCP’s entire default waterfall.

Getting the default waterfall “just right”

Neither the exclusively CCP-funded nor the exclusively clearing-member-funded default waterfall model is practical. However, knowing that both CCP and clearing member funds should be included in the waterfall is not enough; the arrangement and size of the various tranches also matter. Thus, the challenge for policymakers and practitioners is to design a default waterfall framework that is “just right.”

As we discuss later, ownership structure has an effect on the incentives created by the composition of a CCP’s default waterfall. However, there are key structural features that we believe should be common to all CCP waterfalls.

The junior tranche

In all CCP ownership structures, there are clear policy benefits to having material CCP skin-in-the-game at the top of the default waterfall. This junior tranche accomplishes two important objectives, serving as both an auction inducement and a nuisance-avoidance deductible.

As part of any default management process, a CCP needs to return to a matched book by liquidating the open positions of the defaulting clearing member. The junior tranche of CCP capital should provide an incentive for clearing members and, under appropriate circumstances, other interested market participants, to participate meaningfully in the auction of a defaulter’s positions. Clearing members bidding on a defaulter’s portfolio have a financial incentive to bid as low as possible but still high enough to become the highest bidder. If low bids result in losses on the defaulter’s portfolio, the shortfall is covered by the resources in the default waterfall. The presence of a junior tranche in the waterfall above the mutualized resources allows clearing members to place lower bids than they would otherwise since, until the junior tranche and defaulter’s resources are depleted, an auction loss will not harm the nondefaulting clearing members.

The nuisance-avoidance deductible function of the junior tranche allows clearing members to avoid the politically difficult task of replenishing their default fund contribution after the default of a modest-sized clearing member. The concept is perhaps best illustrated with an example.

At 9:02 a.m. on December 12, 2013, the proprietary trading team at HanMag Securities, based in South Korea, placed a total of 36,000 orders for Korea Composite Stock Price Index 200 options, consisting of both calls and puts. The strategy was ostensibly to buy at limit-low and sell at limit-high to exploit any mispriced retail orders. However, by mistake, orders were priced with a remaining maturity of zero days instead of 365 days. Other largely algorithmic trading firms quickly traded against these mispriced options. HanMag Securities lost approximately $39.6 million (46.2 billion South Korean won) in less than two minutes and was unable to settle with the Korea Exchange (KRX) CCP.

Under article 394 of South Korea’s Capital Act, the KRX was liable for the loss only after a default loss equivalent to $190 million, so the HanMag default loss went directly into the clearing member mutualized portion of the KRX default waterfall. Many of the largest banks in the world are KRX clearing members. Clearing members were subsequently required to replenish their respective contributions to the KRX guarantee fund for modest sums of money, relative to the size of the financial institutions involved.5 However, the internal political optics of the replenishment process were nothing short of monumental.6 Many senior bank executives had believed that the replenishment of one’s contribution to a CCP guarantee fund would be a once-in-career occurrence.

Although major clearing member defaults have occurred, most clearing member defaults in the past half-century have been of modest-sized firms.7 A modest-sized junior tranche8 would allow the business heads of a CCP’s clearing members to avoid having to obtain corporate funding to replenish contributions to a CCP guarantee fund in the event of such a default. An additional benefit of using the junior tranche rather than going straight to the mutualized portion of the waterfall is that doing so could help avoid drawing undue attention to a clearing member default, something in the interests of CCP management and the relevant prudential authority. The presence of a junior tranche would seem to align the incentives of all concerned.

The senior tranche

All CCPs, regardless of ownership structure, would benefit from having a senior tranche funded by the CCP9 located at the bottom of the default waterfall.

A clearing member default of any material size would likely exhaust the junior tranche. Once the CCP has managed the default and established the loss, the senior tranche then could be used to immediately replenish the CCP’s junior tranche. This should quickly restore public confidence in the CCP after the default. CCPs must have the financial and human capital to open and operate as usual the day after a default, even while liquidating collateral, transferring customer positions and margin assets, and managing the auction sequence of the defaulter’s positions. While a CCP might expect its clearing membership and the end-user market participants to tolerate a reasonable delay while it replenishes its senior tranche, the ability to replenish its junior tranche immediately with resources from its senior tranche should help the CCP to maintain public confidence.

The magnitude of CCP skin-in-the-game

A number of industry participants have written policy position papers advocating that a CCP’s skin-in-the-game be of a minimum quantity—for example, a fixed percentage of the default waterfall or equal to the first-, second-, or third-largest clearing member’s contribution.10 They have also advocated that 100 percent of a CCP’s skin-in the-game be at the very top of the default waterfall, arguing that this approach would best align the incentives of CCP management, the clearing membership, and the shareholders of any parent corporation. These policy position papers have not typically been accompanied by meaningful supporting analysis.11 Absent more compelling evidence in favor of such proposals, the magnitude of a CCP’s skin-in-the-game should be determined by discussions between the CCP and the CCP’s prudential regulator that take into account the CCP’s unique risk profile and the market it serves.12

Care in determining the size of the CCP’s skin-in-the-game is especially important, since a junior tranche that is too large could have adverse effects by reducing the incentives of clearing members to onboard a defaulting clearing member’s clients.

Finding clearing members to onboard orphaned clients is important because if a CCP fails to do so, at some point it has no choice but to liquidate those positions.13 The liquidation process, the ensuing financial disruption, and the unavoidable unfavorable outcome would not foster public confidence in centralized clearing.

Absent appropriate incentives, many clearing members will seek to avoid onboarding orphaned clients because if they do onboard them, the business heads of the clearing members can be held accountable by their senior managers for knowingly accepting unprofitable or marginally profitable clients.14

As a result, the junior tranche should be small enough to incentivize clearing members to onboard orphaned clients. The larger the CCP’s junior tranche, the lower the probability that a liquidation of client positions would exhaust the junior tranche and result in a mutualized loss to all clearing members. Therefore, a CCP’s junior tranche should be small enough that the surviving clearing members feel that it is possible for the liquidation loss to exhaust the junior tranche and penetrate the mutualized portion of the default waterfall. They would then have a greater financial incentive to onboard the orphaned clients of a defaulting clearing member.

A junior tranche that is too large could also prevent clearing members from submitting reasonable bids in an auction of a defaulting member’s positions. Clearing members have an incentive not to bid so low that the CCP’s liquidation loss depletes the CCP’s junior tranche and penetrates the mutualized portion of the default waterfall, since some of the funds in the mutualized portion were contributed by the clearing member that won the auction. A large junior tranche insulates the clearing members from this risk, encouraging them to submit bids that could result in large liquidation losses, since those losses would primarily be borne by the CCP.

The predictability of prefunded CCP skin-in-the-game

A crucial question that industry observers should ask about CCP skin-in-the-game is “Where is it?” Said another way, is a CCP’s skin-in-the-game prefunded and, if so, where is it held? If it is not prefunded, then what measures would the CCP or its parent company need to undertake under possibly adverse circumstances in order to fund its skin-in-the-game commitment?

At times when the creditworthiness of a clearing member or of the CCP itself comes into question, it is best if the CCP’s default management processes operate flawlessly. Regardless of the ownership structure of the CCP, a CCP’s skin-in-the-game should be prefunded and on deposit with the appropriate central bank. This provides assurances to prudential authorities, clearing members, market participants, and the public at large that the CCP’s skin-in-the-game is not just a financial commitment that would need to be funded at a later date, potentially under the most adverse of circumstances.

CCP ownership structure and the default waterfall

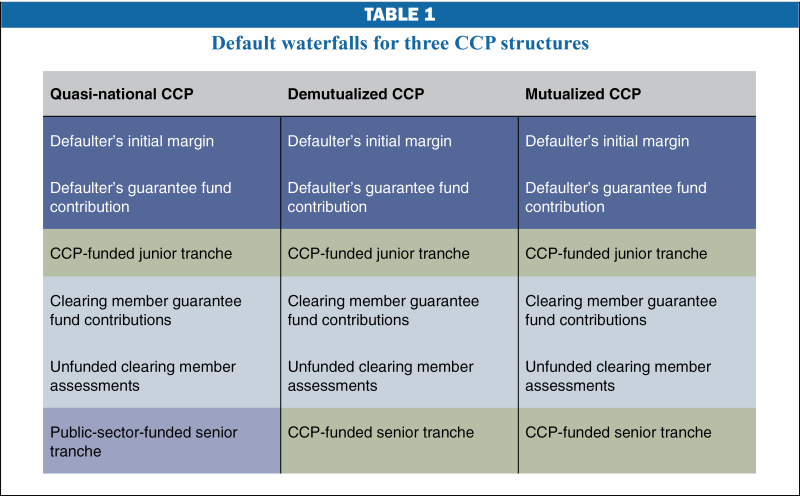

Although there are many features that should be present in all default waterfalls, the ownership structure of a CCP has important implications for the incentives created by the default waterfall’s design and, therefore, should be considered in discussions about waterfall composition and the size of various tranches. We now discuss default waterfall composition and incentives for three different types of CCPs: quasi-national CCPs, demutualized CCPs, and mutualized CCPs.

The quasi-national CCP 15

In some countries, notably emerging economies, the largest single stakeholder in an exchange or CCP is either the government or the central bank. This implicit public sector support typically has the benefit of instilling public confidence in an emerging market structure at precisely the time that public confidence is critical to achieving market acceptance.

Like all CCPs, a quasi-national CCP should have a junior tranche large enough to absorb the default shortfall of a modest-sized clearing member, preventing the clearing members from having to replenish their contributions to the guarantee fund after such a default.

Beyond the junior tranche of a quasi-government CCP, it is not clear what public policy objectives or public confidence objectives would be achieved by having the government or central bank prefund a significant portion of the default waterfall, provided that such financial support is overtly committed to the CCP in some other manner. CCP management is already accountable to the public sector stakeholder for performance, and it would appear that the incentives of the CCP, its management, and the clearing membership are aligned naturally. Clearing member contributions to the default waterfall should follow the junior tranche. This would provide an increased incentive for clearing members to bid aggressively during the auction of the open positions of the defaulter and an incentive for them to onboard clients of the defaulter, lest any liquidation of orphaned clients’ positions penetrate the mutualized clearing member tranche.

As a demonstration of the public sector’s commitment to support the CCP in times of dire need, a quasi-national CCP could include a senior tranche at the bottom of the default waterfall funded by the public sector. (For an illustration of this structure, see table 1.) The amount of the senior tranche could also serve as an indicator of the public sector’s willingness to provide financial support should the public sector desire to limit its financial support to a finite amount ex ante.

Demutualized CCP

A demutualized CCP is usually part of a for-profit corporation and is designed to pursue profit. Although the profits of the CCP accrue to benefit the shareholders of the larger corporation, clearing members continue to participate in the mutualization of default risk as a precondition of membership. Governance of risk-management procedures is typically shared between CCP management, clearing member representatives, and independent industry experts.

Like all CCPs, a demutualized CCP should have a junior tranche in its default waterfall. The junior tranche should be material enough to serve the dual objectives of being both an auction inducement and a nuisance-avoidance deductible. The junior tranche would be followed by the mutualized tranche of clearing member contributions, followed by a tranche of clearing member assessments, followed by the senior tranche (see table 1).

In a demutualized CCP, the senior tranche has a function beyond providing readily available funding to recapitalize the junior tranche. The presence of a material amount of a CCP’s skin-in-the-game at the very bottom of the default waterfall provides a financial incentive for the for-profit CCP not to undersize the upper layers of the default fund, lest the senior tranche be swept into the default shortfall. Such a loss would ultimately be borne by the shareholders of the for-profit corporation.

Mutualized CCP

In some regulatory jurisdictions, a public policy determination has been made that the public good is best served by having a single CCP utility, typically for a given asset class.16 In almost all of these cases, the CCP is owned and governed by its clearing membership and has little to no profit motivation.17 According to two industry experts, such CCPs “will likely have narrow ambitions for new product development and an acute focus on providing an efficient but low-cost service to members, consistent with a utility approach.”18

If the clearing members are the only shareholders of the CCP, then the ultimate funding source of every component of the default waterfall, CCP skin-in-the-game as well as member default fund contributions, is the same. It makes little sense to distinguish among these components of the default waterfall if the clearing members are funding all of them, directly as clearing members or indirectly through the retained earnings of the CCP they collectively own.

It may, however, still behoove the CCP to have a junior tranche to serve as an auction inducement and as a nuisance-avoidance deductible to spare the clearing membership from having to replenish their contributions to the mutualized guarantee fund should there be a default loss that penetrated the junior tranche. The mutualized clearing member tranche would be followed by the unfunded clearing member assessment tranche.

A senior tranche at the very bottom of the default waterfall would primarily serve to prefund necessary replenishments of the junior tranche were the junior tranche ever partially or wholly depleted. (See table 1.) In a mutualized CCP, the funding of both the mutualized default fund and the senior tranche ultimately come from clearing members (directly as members or indirectly as shareholders), and so the addition of a senior tranche below the default fund would not appear to otherwise affect the alignment of incentives.

Default waterfall tranche penetration probabilities

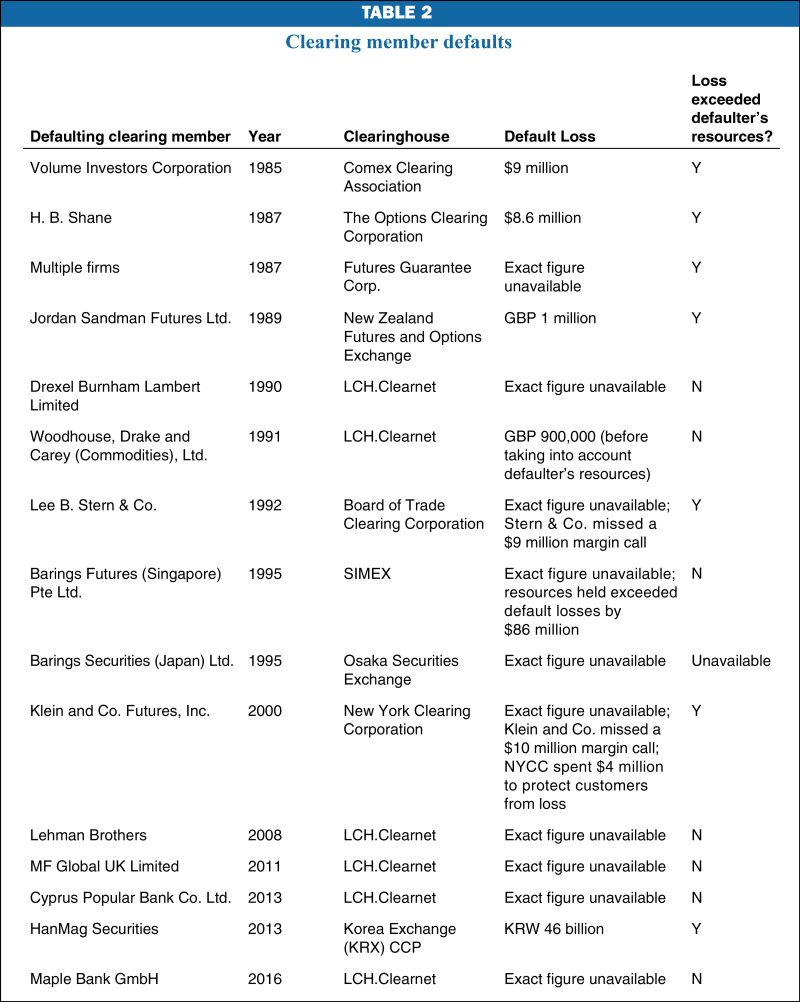

It is helpful when discussing default waterfall tranche sequences and the appropriate amount of CCP skin-in-the-game to have a sense of how likely it is that a clearing member default actually penetrates the default waterfall beyond the defaulter’s initial margin and default fund contribution. We provide evidence from actual clearing member defaults to demonstrate that defaults rarely penetrate the deeper layers of the default waterfall.

For broader context, we also include an appendix with a framework for calculating the probability of a loss that exhausts the entire default waterfall. We show that a default loss of this magnitude is highly unlikely.

Actual clearing member defaults

There have been relatively few clearing member defaults over the past three decades. Table 2 lists a representative sample. It is likely, given the size of the defaults involved, that the CCP’s junior tranche (as proposed) would have absorbed all of the default losses listed in the table. In about half of the defaults, the loss was entirely covered by the defaulter’s initial margin and contribution to the guarantee fund.

Conclusion

A CCP’s ownership and governance structure has an effect on the alignment of the incentives of the CCP’s management and its clearing members and, accordingly, on the appropriate amount of CCP skin-in-the-game and the justification for the skin-in-the-game’s waterfall position.

We argue that there are many elements that should be common to all CCP default waterfalls. All waterfalls should include junior and senior tranches. In every case, attention must be paid to the incentives created by the size of a CCP’s skin-in-the-game. Placing all of a CCP’s skin-in-the-game at the very top of the waterfall may create a perverse incentive for clearing members to decline to onboard the orphaned customers of a defaulting clearing member, potentially exacerbating the default shortfall and likely diminishing public confidence in centralized clearing.

In order for the default management process to be entirely predictable and transparent, it is our opinion that all CCPs should be required to prefund their skin-in-the-game obligations and deposit those funds with the appropriate central bank. Doing so should increase public confidence in centralized clearing.

Public policy discussions respecting the magnitude and sequence of CCP default waterfall tranches should be undertaken within a framework that recognizes the improbability of any default shortfall exhausting the higher tranches of the default waterfall, an improbability demonstrated by a historical review of actual clearing member defaults.

NOTES

1 For more on CCPs, see chapter 2: “Central counterparty clearing,” in the Chicago Fed’s online reference book, Understanding Derivatives: Markets and Infrastructure, https://www.chicagofed.org/publications/understanding-derivatives/index.

2 For a more detailed discussion of ownership and governance structures, see Cox and Steigerwald (2016).

3 The porting of client positions refers to transferring the open derivatives positions and initial margin assets of customers (presumably from a weakened or insolvent firm) to another firm in sound financial condition. The act of accepting these customers is often referred to as “onboarding.”

4 The problems with a completely mutualized waterfall discussed in this analysis are relevant for quasi-national and for-profit CCPs, for which a meaningful distinction can be made between the CCP’s owners and its clearing members. They are not an issue for mutualized CCPs, in which the members and owners are one and the same.

5 It has been reported that $10 million of the default loss was absorbed by Newedge, Morgan Stanley, JP Morgan, and Credit Suisse. See Cooper (2014).

6 This was the term used by the global head of OTC clearing at a major clearing member in an interview with John McPartland on April 24, 2014.

7 Volume Investors Corporation, Klein & Co. Futures Inc., Woodhouse, Drake and Carey (Commodities) Ltd., H. B. Shane, HanMag Securities, and Griffin Trading Company are examples of little-known CCP clearing members that have defaulted with relatively modest financial repercussions.

8 By modest-sized, we mean capable of absorbing clearing member defaults of the magnitude described in note 7.

9 The proposed exception being the quasi-national CCP, where we suggest that an optional senior tranche be funded with public funds, primarily as a symbol of public sector support.

10 See, for example, Fleming and Stafford (2014).

11 See JP Morgan Chase & Company, Office of Regulatory Affairs (2014); De Leon, Jordal, and Cantrill (2014); and BlackRock (2014). For reference, see also, International Swaps and Derivatives Association (2014).

12 While the opinions of market practitioners and academics may better frame the public debate on this subject, the CPSS-IOSCO’s Principles for Financial Market Infrastructures make it clear that the ultimate responsibility to ensure that CCPs have the appropriate financial resources lies with the relevant prudential regulator.

13 Otherwise the CCP would not have a matched book of positions.

14 A marginally profitable customer would be a customer whose account is profitable but reduces the brokerage unit’s return on equity after taking into consideration the Basel Committee on Banking Supervision (BCBS) capital requirements. The challenge of persuading surviving clearing members to onboard orphaned clients may be exacerbated by recent regulatory reforms. The BCBS has proposed capital requirements on banks and bank affiliates that offer client clearing of derivatives contracts. Some have expressed concern that these capital requirements will call into question the viability of porting (transferring) client positions from a clearing member in financial difficulty to other clearing members in good standing, especially clients that use nonfinancial derivatives contracts.

15 This type of CCP ownership structure at one time or another could be found in China, Russia, Egypt, and Singapore. In Singapore, Temasek Holdings, currently owned by the Singapore government, owns SEL Holdings, an intermediate holding company, which in turn owns 23.5 percent of the Singapore Exchange (SGX), making it SGX’s largest stakeholder.

16 The National Securities Clearing Corporation and The Options Clearing Corporation are good examples.

17 Alternatively, the ownership of the CCP might be shared among clearing members and the exchange(s) that the CCP services.

18 Cox and Steigerwald (2016).

APPENDIX: COVER-TWO DEFAULT PROBABILITIES OF CORRELATED FIRMS

Computation of a cover-two default loss probability

In this appendix, we provide a theoretical framework within which to consider the probability that a CCP’s entire default waterfall would ever be exhausted.

Systemically important CCPs are required by international standards to size their financial resources to withstand the contemporaneous demise of their two largest clearing members—the “cover-two” standard. Here, we calculate the probability of the largest and second-largest clearing members of a CCP defaulting in the same week of the same year. The two critical parameters of this equation are the credit rating of the two clearing members and the correlation of the two defaults.

Using the mathematical framework described below, we consider two clearing members with an initial credit rating of BB, which implies a default probability of 0.0094, based upon historical data from 1990 through 2014 provided by Fitch Ratings. If the default probabilities of the number one and number two clearing members are uncorrelated, the probability that, over the course of a year, they both default in the same week is 0.0000017. It is unlikely, however, that the default probabilities are uncorrelated. If we instead assume that the correlation between the default of the number one and number two clearing members (both BB rated) is 0.85, the probability, over the course of a year, of their joint demise in the same week is 0.0080.

Mathematical framework for computing a cover-two default loss probability

We would like to estimate the probability that the two largest firms in a clearinghouse default within a week of each other sometime in the next year, a “cover-two” situation, given their marginal probabilities of default and a measure of the correlation between their default probabilities. We only consider the first and second positions, regardless of which firms are currently occupying them. For example, assume firms A, B, and C are ranked from largest to smallest and identically rated. If A defaults in a given week, we simply re-label B to be the largest and C the second-largest firm, and continue forward in time with the new first- and second-largest firms. Here, we assume that all firms are equally rated to ensure that such a default event would not change the marginal default probabilities.

If an individual firm has probability pr of defaulting in a year, then the week in which it defaults can be represented by the geometric distribution with parameter p, assuming default events are independently, identically distributed; thus from the geometric cdf:

1) pr = 1 – (1 – p)52 → p = 1 – (1 – pr)1/52.

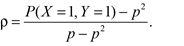

Let ρ represent the usual correlation coefficient between the random variables indicating the event that the first-largest firm, whichever firm it might be, and the second-largest firm default in a given week. Since both of the firms in this example are assumed to have the same credit rating, they have the same geometric parameter p. For any fixed week, let X and Y be random variables indicating whether the two firms default in that week. Then both X and Y are Bernoulli with parameter p. By the definition of correlation between Bernoulli random variables, the following equation holds:

Then by rearranging, the probability that a cover-two event happens in a given week, call it q, is given by:

2) q = ρ(p – p2) + p2.

Now, we can model the cover-two situation as a geometric random variable Z with parameter q, representing the week in which the first cover-two situation happens. In essence, we flip a coin with probability q of heads every week of the year; if we get heads, a cover-two situation happens that week. Then the probability of observing a cover-two event in the next year is equivalent to evaluating the geometric cdf at 52:

3) P(Z ≤ 52) = 1 – (1 – q)52.

REFERENCES

BlackRock, 2014, “Central clearing counterparties and too big to fail,” ViewPoint, New York, April 7, https://www.blackrock.com/corporate/en-cl/literature/whitepaper/viewpoint-ccp-tbtf-april-2014.pdf.

Commodity Futures Trading Commission, Division of Trading and Markets, 2001, “Report on lessons learned from the failure of Klein & Co. Futures, Inc.,” report, Washington, DC, July.

Cooper, Jonathan, 2014, “The Korea Exchange: A cautionary tale on CCP waterfalls and non-defaulting members taking the loss,” Securities Finance Monitor, March 18, http://finadium.com/the-korea-exchange-a-cautionary-tale-on-ccp-waterfalls-and-non-defaulting-members-taking-the-loss/.

Corcoran, Andrea M., and Susan C. Ervin, 1987, “Maintenance of market strategies in futures broker insolvencies: Futures position transfers from troubled firms,” Washington and Lee Law Review, Vol. 44, No. 3, pp. 849–915, http://scholarlycommons.law.wlu.edu/wlulr/vol44/iss3/5.

Cox, Robert T., 2015, “Central counterparties in crisis: The Hong Kong Futures Exchange in the crash of 1987,” Journal of Financial Market Infrastructures, Vol. 4, No. 2, December, pp. 73–98.

Cox, Robert T., and Robert S. Steigerwald, 2016, “Incomplete demutualization and financial market infrastructure: Central counterparty ownership and governance after the crisis of 2008–9,” Journal of Financial Market Infrastructures, Vol. 4, No. 3, March, pp. 25–38.

De Leon, William G., Tracey Jordal, and Libby Cantrill, 2014, “Setting global standards for central clearinghouses,” Viewpoints, Pacific Investment Management Company, October, https://www.pimco.com/insights/viewpoints/viewpoints/setting-global-standards-for-central-clearinghouses.

Feder, Barnaby J., 1992, “Clearing firm is suspended by Chicago Board of Trade,” New York Times, October 24.

Fleming, Sam, and Philip Stafford, 2014, “JPMorgan tells clearers to build bigger buffers,” Financial Times, September 10, available by subscription, https://www.ft.com/content/48aa6b02-38f9-11e4-9526-00144feabdc0.

International Swaps and Derivatives Association, 2014, “Principles for CCP recovery,” report, New York, November 25, http://www2.isda.org/attachment/NzExMw==/Principles%20for%20CCP%20Recovery%20FINAL.pdf.

Jouzaitis, Carol, and Laurie Cohen, 1987, “$8 million loss for options guarantor,” Chicago Tribune, December 5.

JPMorgan Chase & Co., Office of Regulatory Affairs, 2014, “What is the resolution plan for CCPs?,” Perspectives, New York, September, https://www.jpmorganchase.com/corporate/About-JPMC/document/resolution-plan-ccps.pdf.

Lim, Michael Choo San, and Nicky Tan Ng Kuang, 1995, Baring Futures (Singapore) Pte Ltd: Investigation Pursuant to Section 231 of the Companies Act (Chapter 50); The Report of the Inspectors Appointed by the Minister for Finance, Singapore: Ministry of Finance.

Norman, Peter, 2011, The Risk Controllers: Central Counterparty Clearing in Globalised Financial Markets, Chichester, West Sussex, UK: John Wiley & Sons.

Vaghela, Viren, 2014, “Korea clearing structure in question after HanMag trading error,” Risk.net, March 5, available by subscription, http://www.risk.net/exchanges/2331225/korea-clearing-structure-question-after-hanmag-trading-error.