Introduction and summary

If news of higher future interest rates reflects a shift in the stance of monetary policy, then we expect it to lower projections for real gross domestic product (GDP) growth and raise projections for unemployment. However, the data point to quite different conclusions. When market participants raise their estimates of future interest rates after a meeting of the Federal Reserve’s monetary policy committee, the Federal Open Market Committee (FOMC), private forecasters tend to raise their projections of real GDP growth and lower their projections for unemployment. Campbell, Evans, Fisher, and Justiniano (2012) documented this fact, and we labeled it the “event-study activity puzzle” in our NBER Macroeconomics Annual chapter (Campbell, Fisher, Justiniano, and Melosi, 2017).

In this article, we summarize an empirical exploration of the effects of FOMC statements on financial market expectations of future interest rates and private forecasters’ expectations of future macroeconomic performance that appeared in Campbell et al. (2017). Our work resolves the event-study activity puzzle by demonstrating that the FOMC moves market expectations of future interest rates in part by transmitting its views of future macroeconomic fundamentals. When these are strong, private forecasters revise their projections accordingly, while market participants mark up their expectations of future interest rates.

How does the FOMC transmit macroeconomic expectations?

The FOMC releases a statement after each of its meetings that announces any desired changes to the federal funds rate and other policy tools, describes its assessment of current macroeconomic circumstances, and possibly describes how further developments could influence its future policy choices. This discussion of possible future actions is called forward guidance. Perhaps the most prominent example of forward guidance from before the Great Recession was the use of “the Committee believes that policy accommodation can be removed at a pace that is likely to be measured” in the FOMC’s post-meeting statements from May 2004 through November 2005.

After the FOMC set its target for the federal funds rate to its effective lower bound in December 2008, it turned to forward guidance as one way to deliver additional monetary accommodation.1 As demonstrated in the theoretical work of Krugman (1998) and Eggertsson and Woodford (2003), expansionary forward guidance can improve current macroeconomic outcomes if it lowers households’ desired savings by increasing their expectations of future inflation and output. According to the theory, such changes in expectations can be induced by the FOMC making a credible commitment to keep the future federal funds rate lower than it would otherwise do given the prevailing macroeconomic conditions. Campbell et al. (2012) called this Odyssean forward guidance.2 After its August 2011 meeting, the FOMC stated that macroeconomic conditions “are likely to warrant exceptionally low levels for the federal funds rate at least through mid-2013.”3 Similarly, it stated after its December 2012 meeting that interest rates would remain exceptionally low “at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee’s 2 percent longer-run goal, and longer-term inflation expectations continue to be well anchored."4 Both statements could be viewed as Odyssean forward guidance.

While the theoretical possibility for appropriate forward guidance to improve current macroeconomic outcomes is clear, the evidence does not unambiguously support this conjecture. Ben Zeev, Gunn, and Khan (2015) and D’Amico and King (2016) both use econometric models and money market futures prices to identify unexpected movements in expected future interest rates caused by FOMC forward guidance; they both find that output and inflation rise presently and in the future when expected future rates fall. This is exactly as the standard New Keynesian model predicts when changes to expected future interest rates represent exogenous adjustments to the stance of monetary policy. On the other hand, Campbell et al. (2012) measure unexpected movements in future interest rates with changes in money market futures rates on the dates of FOMC meetings. When they relate revisions in private sector forecasts of output growth and unemployment to these “forward-guidance shocks,” they find that decreases in future expected interest rates lower expectations of output and raise expected unemployment. This is the event-study activity puzzle mentioned above.

Quantifying the puzzle

To quantify the event-study activity puzzle, we related changes in private sector forecasts for GDP growth and unemployment over months containing an FOMC meeting with the change in the expectation of the federal funds rate four quarters into the future, on the day of the FOMC announcement. By construction, this event-study of how monetary policy announcements affect expectations of future monetary policy controls for all information available to market participants at the close of business on the previous day. Since FOMC announcements are usually the most important financial news on the day they occur, they should dominate our measured changes in expectations of interest rates. Our measures of private sector forecasts come from the Blue Chip Economic Indicators, a monthly survey of private forecasters. We use its “consensus” forecast, which averages all submitted forecasts. Its respondents provide quarterly forecasts for real GDP growth and the unemployment rate for the current and next calendar years. Therefore, the survey reports private forecasts for the current and next four quarters within one month of every FOMC meeting. For each of these observables, we estimate the coefficients of a simple linear model,

![]()

Here, ∆met is the change in the Blue Chip forecast for some variable over the month containing a particular FOMC meeting,  is the change in expectation of the federal funds rate four quarters hence on the day of the FOMC meeting, and εt is a residual that accounts for all movements in ∆met that are unrelated to

is the change in expectation of the federal funds rate four quarters hence on the day of the FOMC meeting, and εt is a residual that accounts for all movements in ∆met that are unrelated to ![]() . We estimated the model’s unknown coefficients α and β using data from all FOMC meetings between 1994 and 2010 inclusive.5

. We estimated the model’s unknown coefficients α and β using data from all FOMC meetings between 1994 and 2010 inclusive.5

For each of the private expectations, we estimated the unknown coefficients α and β using the method of ordinary least squares. This method makes the sum of the squared implied values for εt as small as possible. Table 1 reports the estimated coefficients multiplying  . When these are positive, the data indicate that increases in the interest rate expected four quarters in the future are associated with increases in the given expectation. Of course, sampling error could make any of our coefficient estimates non-zero even though the coefficient’s true value is zero. For each regression, we tested the null hypothesis that the true value of β equals zero against the alternative that it is non-zero using methods described in Campbell et al. (2017). When the test rejects the null hypothesis at the conventional levels of statistical significance of 5 percent and 1 percent, we mark the associated estimate of β with ** and ***, respectively. A smaller level of statistical significance means that the chances of a model with a true coefficient of zero generating the estimated non-zero coefficient are lower. Next to each estimated coefficient is the model’s R2 measure. This varies between 0 and 1 and gives the fraction of variance in ∆met that the model assigns to movements in

. When these are positive, the data indicate that increases in the interest rate expected four quarters in the future are associated with increases in the given expectation. Of course, sampling error could make any of our coefficient estimates non-zero even though the coefficient’s true value is zero. For each regression, we tested the null hypothesis that the true value of β equals zero against the alternative that it is non-zero using methods described in Campbell et al. (2017). When the test rejects the null hypothesis at the conventional levels of statistical significance of 5 percent and 1 percent, we mark the associated estimate of β with ** and ***, respectively. A smaller level of statistical significance means that the chances of a model with a true coefficient of zero generating the estimated non-zero coefficient are lower. Next to each estimated coefficient is the model’s R2 measure. This varies between 0 and 1 and gives the fraction of variance in ∆met that the model assigns to movements in ![]() .

.

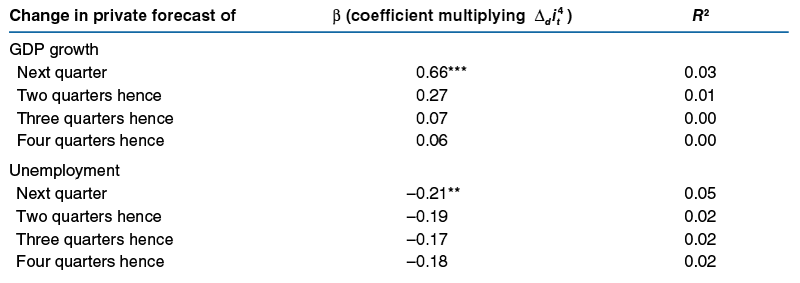

The results in table 1 illustrate the event-study activity puzzle. Raising the expectation of the federal funds rate four quarters hence raises private sector forecasts of GDP growth and lowers unemployment forecasts for the next four quarters. For example, a 1 percentage point increase in ![]() raises the expectation of annualized GDP growth in the next quarter by 66 basis points and lowers the expectation of next quarter’s unemployment rate by 21 basis points. Only the changes in expectations for the next quarter are statistically significant at conventional levels. For expected GDP growth, the coefficients’ estimated magnitudes at horizons of two to four quarters vary from 27 to 6 basis points. For unemployment, the coefficient estimates for those longer horizons are comparable to those for the next quarter, but the coefficients are measured relatively imprecisely. The R2 measures in table 1 all indicate that most variance in expectations revisions is due to factors other than changes in expected interest rates. That is, these estimates indicate that FOMC forward guidance was not a key driver of private expectations during the sample period.

raises the expectation of annualized GDP growth in the next quarter by 66 basis points and lowers the expectation of next quarter’s unemployment rate by 21 basis points. Only the changes in expectations for the next quarter are statistically significant at conventional levels. For expected GDP growth, the coefficients’ estimated magnitudes at horizons of two to four quarters vary from 27 to 6 basis points. For unemployment, the coefficient estimates for those longer horizons are comparable to those for the next quarter, but the coefficients are measured relatively imprecisely. The R2 measures in table 1 all indicate that most variance in expectations revisions is due to factors other than changes in expected interest rates. That is, these estimates indicate that FOMC forward guidance was not a key driver of private expectations during the sample period.

Table 1. The event-study activity puzzle

Sources: Authors’ calculations based on data from the Board of Governors of the Federal Reserve System and Blue Chip Economic Indicators.

Campbell et al. (2012) speculated that their results arose from a failure of their measured shocks to represent truly exogenous changes in the stance of monetary policy. In general, the FOMC could surprise market participants in two distinct ways. First, it might truly change the stance of monetary policy based on its members’ judgments about commonly observed macroeconomic fundamentals. Second, it could signal that it has received information about future macroeconomic developments that is unavailable to market participants. Although FOMC participants have very little access to macroeconomic data that are unavailable to the public, the Federal Reserve System’s staff might give the FOMC proprietary interpretative information. If this is so, then transmitting information that the economy would “run hot” in the near future, for instance, would lead market participants to increase their forecasts of both interest rates and output. Campbell et al. (2012) labeled such forward guidance that simply reports information on future macroeconomic developments and discussed possible FOMC reactions to those developments as Delphic.6 If most FOMC forward guidance is Delphic, then the event-study activity puzzle can be understood as the optimal reactions of market participants and private forecasters to prognostications about future macroeconomic developments in FOMC statements.

Although this Delphic resolution to the event-study activity puzzle seems plausible, Campbell et al. (2012) provided no evidence to support it. In Campbell et al. (2017), we subjected this hypothesis to empirical scrutiny using measures of the FOMC’s private information about short-run macroeconomic performance. For this, we proceeded in two steps. First, we inferred the change in interest rates that can be directly explained by these measures of private information, and we attributed this estimate to FOMC short-run Delphic forward guidance. Second, we quantified the extent to which short-run Delphic forward guidance explains the event-study activity puzzle by estimating how this measure influenced changes of private sector expectations of GDP growth and unemployment.

We constructed our measures of FOMC private information by subtracting consensus private sector forecasts for Consumer Price Index (CPI) inflation, real GDP growth, and the unemployment rate for the current and next four quarters from analogous forecasts prepared by Federal Reserve Board staff for the FOMC. These forecasts are made available to FOMC participants (Governors of the Federal Reserve System and the 12 Reserve Bank presidents), but they are kept out of the public domain for five years after their creation. Therefore, any measurable effect these have on innovations to financial markets’ expectations of future interest rates should operate only through the content of the FOMC statement.

To examine the influence of these forecast differences on changes in financial market expectations of the federal funds rate, we estimated the coefficients of a simple linear model:

Here  ,

, ![]() ,

, represent the differences between the Board staff and Blue Chip forecasts for output growth, unemployment, and inflation, respectively. These include differences for the current meeting and from the meeting that preceded it. We included this seemingly stale information because FOMC participants might require time to form the consensus about the meaning of new information required for its discussion in a meeting statement.7 We estimated the model’s unknown coefficients γy, γu, and γπ with the method of ordinary least squares, as described earlier.

represent the differences between the Board staff and Blue Chip forecasts for output growth, unemployment, and inflation, respectively. These include differences for the current meeting and from the meeting that preceded it. We included this seemingly stale information because FOMC participants might require time to form the consensus about the meaning of new information required for its discussion in a meeting statement.7 We estimated the model’s unknown coefficients γy, γu, and γπ with the method of ordinary least squares, as described earlier.

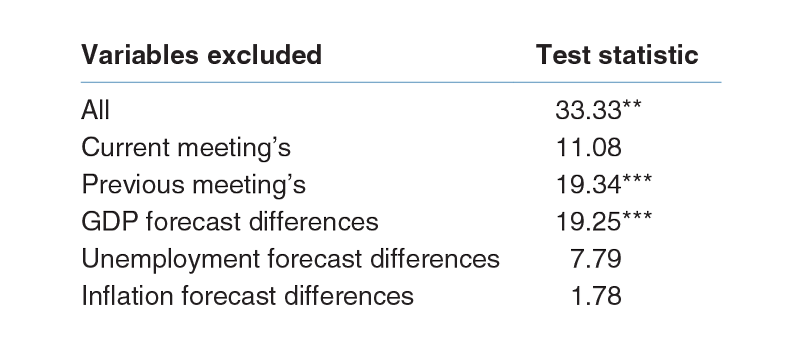

Table 2 gives the results of this estimation. For the sake of parsimony, it reports the results of exclusion tests rather than the estimated coefficients themselves. These test the null hypothesis that the coefficients multiplying each variable in a group all equal zero. For example, the exclusion test for all FOMC private information about GDP growth uses the null hypothesis that all elements of γy equal zero. Just as before, the superscripts ** and *** indicate that a test rejects the null hypothesis at the 5 percent and 1 percent level, respectively.8 The exclusion test rejects the null hypothesis that all of the forecast differences are irrelevant at the 5 percent level. Interestingly, the test does not reject the null hypothesis that the forecast differences associated with the current meeting are irrelevant. Instead, it is the previous meeting’s forecast differences that help explain the change in expected future interest rates following the current meeting. As suggested earlier, we interpret this result as reflecting the time required for FOMC participants to process new information. Among the three macroeconomic variables included, the exclusion tests indicate that it is differences between the Board staff and Blue Chip forecasts for near-term GDP growth that have the most influence on financial market participants’ expectations of future interest rates.9

Table 2. Revelation of Greenbook forecasts: Exclusion tests

Sources: Authors’ calculations based on data from the Board of Governors of the Federal Reserve System and Blue Chip Economic Indicators.

These empirical results strongly suggest that the FOMC routinely transmits the Board staff’s view of future macroeconomic conditions to the public through FOMC statements. Additionally, they provide the ability to control for these transmissions when assessing the influence of statement-induced changes in expected future interest rates on private macroeconomic forecasts. For this, we use the estimated values of γy, γu, and γπ to construct the change in private interest rate expectations expected given the differences between the Board staff and Blue Chip forecasts. Call this estimate of the FOMC’s short-run Delphic forward guidance ![]() :

:

![]()

Here, the hats indicate that the linear model's coefficients are estimated from data. With this, we can write

![]()

The model's estimated residual term is ![]() . By construction, its correlation with

. By construction, its correlation with ![]() in our sample equals zero. It represents all influences on

in our sample equals zero. It represents all influences on ![]() that are not due to short-run Delphic forward guidance. These include long-run Delphic forward guidance and any Odyssean forward guidance.

that are not due to short-run Delphic forward guidance. These include long-run Delphic forward guidance and any Odyssean forward guidance.

We can now assess how these two components of ![]() shape revisions to private sector expectations. There is no good ex ante reason to expect the short-run Delphic forward guidance in

shape revisions to private sector expectations. There is no good ex ante reason to expect the short-run Delphic forward guidance in ![]() to influence private macroeconomic expectations in the same way as the various messages embodied in

to influence private macroeconomic expectations in the same way as the various messages embodied in ![]() do. To account for these possible differences, we can generalize the linear model used to create table 1 by allowing these two components of

do. To account for these possible differences, we can generalize the linear model used to create table 1 by allowing these two components of ![]() to have distinct coefficients. That is,

to have distinct coefficients. That is,

![]()

Table 3 reports the results of estimating this model with the method of least squares. Each row reports the model’s estimated coefficients and R2 measure for one macroeconomic expectation. The superscripts ** and *** indicate the statistical significance of the coefficient estimates at the 5 percent and 1 percent level, respectively. The estimates clearly indicate that the FOMC’s short-run Delphic forward guidance moves interest rate expectations and projections of GDP growth in the same direction. A 1 percentage point increase in ![]() is associated with a 2.88 percentage point increase in expected GDP growth next quarter, a 1.75 percentage point increase two quarters hence, and a 0.66 percentage point increase three quarters hence. All of these responses are statistically significant at conventional levels. Similarly, the FOMC’s short-run Delphic forward guidance moves expected future interest rates and unemployment projections in the opposite directions. For example, a 1 percentage point increase in

is associated with a 2.88 percentage point increase in expected GDP growth next quarter, a 1.75 percentage point increase two quarters hence, and a 0.66 percentage point increase three quarters hence. All of these responses are statistically significant at conventional levels. Similarly, the FOMC’s short-run Delphic forward guidance moves expected future interest rates and unemployment projections in the opposite directions. For example, a 1 percentage point increase in ![]() decreases the expected unemployment rate in four quarters by 1.18 percentage points. The R2 measures for these linear models are between 0.17 and 0.21. That is, the FOMC’s short-run Delphic forward guidance accounts for about one-fifth of the monthly revisions to unemployment expectations.

decreases the expected unemployment rate in four quarters by 1.18 percentage points. The R2 measures for these linear models are between 0.17 and 0.21. That is, the FOMC’s short-run Delphic forward guidance accounts for about one-fifth of the monthly revisions to unemployment expectations.

Table 3. Blue Chip forecasts’ responses to decomposed monetary policy

Sources: Authors’ calculations based on data from the Board of Governors of the Federal Reserve System and Blue Chip Economic Indicators.

The estimated residual term ![]() should be free of (measurable) short-run Delphic forward guidance. The estimated coefficients indicate that this is indeed so. All but one of them has the “intuitive” sign associated with exogenous changes to the stance of monetary policy. That is, these estimates are consistent with the prediction that expectations of economic activity fall when the FOMC signals a tightening in future monetary policy beyond what the private sector would ordinarily forecast given the incoming macroeconomic data. However, they are relatively small in magnitude and none of them are statistically significant. Therefore, there remains considerable scope for future research to investigate this hypothesis.

should be free of (measurable) short-run Delphic forward guidance. The estimated coefficients indicate that this is indeed so. All but one of them has the “intuitive” sign associated with exogenous changes to the stance of monetary policy. That is, these estimates are consistent with the prediction that expectations of economic activity fall when the FOMC signals a tightening in future monetary policy beyond what the private sector would ordinarily forecast given the incoming macroeconomic data. However, they are relatively small in magnitude and none of them are statistically significant. Therefore, there remains considerable scope for future research to investigate this hypothesis.

Conclusion

In Campbell et al. (2017), we present a more detailed analysis of these results, including a discussion of whether forward guidance substantially affects Treasury term premiums. Overall, we find that accounting for the FOMC’s transmission of short-run Delphic forward guidance in its meeting statements resolves the event-study activity puzzle of Campbell et al. (2012). This result is important in itself for designing central bank communications policy, and it clears the way for future research into Odyssean forward guidance.

NOTES

1 In a speech at the London School of Economics on January 13, 2009, Chairman Ben Bernanke was explicit about the value of forward guidance when policy is constrained by the effective lower bound: “Although the federal funds rate is now close to zero, the Federal Reserve retains a number of policy tools that can be deployed against the crisis. One important tool is policy communication. Even if the overnight rate is close to zero, the Committee should be able to influence longer-term interest rates by informing the public’s expectations about the future course of monetary policy. To illustrate, in its statement after its December meeting, the Committee expressed the view that economic conditions are likely to warrant an unusually low federal funds rate for some time. To the extent that such statements cause the public to lengthen the horizon over which they expect short-term rates to be held at very low levels, they will exert downward pressure on longer-term rates, stimulating aggregate demand.” Read the complete text of the speech at https://www.federalreserve.gov/newsevents/speech/bernanke20090113a.htm.

2 Odyssean forward guidance consists of central bankers’ statements that bind them to future courses of action. Just as Odysseus bound himself to his ship’s mast so he could enjoy the sirens’ song without succumbing to the temptation to drown himself while swimming toward them, a central banker can improve economic outcomes by publicly committing to a plan that uses expectations of suboptimal future outcomes to improve current economic conditions.

3 See https://www.federalreserve.gov/monetarypolicy/fomcminutes20110809.htm.

4 See https://www.federalreserve.gov/monetarypolicy/fomcminutes20121212.htm.

5 Our sample begins with 1994 because the FOMC issued statements only intermittently before then, and it ends in 2010 because the Greenbook forecasts we used to measure the FOMC’s private information (discussed in the text) were not in the public domain thereafter.

6 Like the oracle of Delphi, the forward guidance predicts the future but promises no specific policy actions.

7 For each FOMC meeting, we compare Board staff and Blue Chip forecasts for the current quarter and the next four quarters. Since we also include forecast differences from the previous meeting in our model, this would make for 30 coefficients to estimate. There were only 148 FOMC meetings during our sample period, so including all of these variables would put us in danger of “overfitting” the model. To avoid this danger, we reduced the forecast differences for each meeting and each variable to two variables using a statistical procedure called factor analysis. We give the details of this procedure in Campbell et al. (2017).

8 See Campbell et al. (2017) for the details.

9 As a point of comparison, we showed in Campbell et al. (2017) that our measures of FOMC private information have no statistically detectable influence on the current policy rate.

REFERENCES

Ben Zeev, Nadav, Christopher Gunn, and Hashmat Khan, 2017, “Monetary news shocks,” Carleton Economic Papers, Carleton University, CEP 15-02, revised February 27, 2017 (originally issued March 2015).

Campbell, Jeffrey R., Charles L. Evans, Jonas D. M. Fisher, and Alejandro Justiniano, 2012, “Macroeconomic effects of Federal Reserve forward guidance,” Brookings Papers on Economic Activity, Spring, pp. 1–54.

Campbell, Jeffrey R., Jonas D. M. Fisher, Alejandro Justiniano, and Leonardo Melosi, 2017, “Forward guidance and macroeconomic outcomes since the financial crisis,” in NBER Macroeconomics Annual 2016, Martin Eichenbaum and Jonathan A. Parker (eds.), Vol. 31, Chicago: University of Chicago Press, forthcoming.

D’Amico, Stefania, and Thomas B. King, 2015, “What does anticipated monetary policy do?,” Federal Reserve Bank of Chicago, working paper, No. 2015-10, November.

Eggertsson, Gauti B., and Michael Woodford, 2003, “The zero bound on interest rates and optimal monetary policy,” Brookings Papers on Economic Activity, No. 1, pp. 139–233.

Krugman, Paul R., 1998, “It’s baaack: Japan’s slump and the return of the liquidity trap,” Brookings Papers on Economic Activity, No. 2, pp. 137–205.