Introduction and summary

In this article I review the history of French public debt during the “long” nineteenth century, from Napoleon Bonaparte’s accession to power in 1800 to the outbreak of World War I in 1914. I discuss the size of the debt, its evolution in relation to government surpluses, the array of financial instruments, and the main methods of debt management used by the French state.

The salient facts are the following:

- In 1802 the public debt was 10% of gross domestic product (GDP), after the events of the Revolution. Over the course of the nineteenth century, it grew to a maximum of 113% after the Franco-Prussian War in 1871, to fall back to 68% of GDP in 1914.

- Perpetual annuities remained the nearly exclusive financial instrument until 1870 and the main one after. The new instruments used after 1870 were bonds with defined maturities, ranging from six to 75 years.

- Short-term financing was provided by the Caisse des Depots, a State institution created to funnel small savings, rather than the central bank (Banque de France). Treasury bills were little used.

- The only default in the modern sense, little known, took place in 1848 when Treasury bills were converted involuntarily into perpetual annuities.

Definition and construction of the series

One can define and measure the public debt in various ways, depending on the question at hand. A debt is a promise of future payments, so one must first decide how to measure and value these future sums. The question is then: Who owes and why, that is, in exchange for what? If the question is the sustainability of the promises made, it will be necessary to take into account all future promises, whether they were made in exchange for recognized resources (e.g., bonds for cash), for services (e.g., pensions of State employees), or as compensation (e.g., indemnities to third parties). But if the matter at hand is fiscal, a narrower definition can be used: the debt that arises from budget deficits. In that case, only promises made for resources received and used in spending are taken into account. In this article, I try to be as broad as possible in accounting for future liabilities, but restrict myself to those than can be assigned a present value. This leads me to exclude all liabilities contingent on lives, namely life annuities1 left over from eighteenth century loans and the growing stock of civil and military pensions. Assigning a present value to such liabilities is conceptually feasible with the use of life tables but requires information on the age distribution of claimants that is not available.2

What do I include? Clearly, marketable debt (that is, tradeable debt sold to the public) must and can easily be included. It can also be assigned a market value based on market prices.3 There are in addition a variety of commitments to the private sector made in exchange for assets that were tangible but difficult to value (I am referring to the debt to railroad companies, which I will discuss), as compensation and indemnities of various kinds, and subsidies that are promised and delivered over time, etc. In principle, it is possible to review all items of the annual budgets and identify those that correspond to payments on past promises. Such payments mostly appear in the budget of the ministry of finance, but not always. Nicolas (1882), who gathered figures on State budgets in a coherent format from 1801 to 1880, has identified these various debt payments. From 1875 onward, the primary source I use4 provides more detailed accounts through which I can track the promises and the payments.

There are few existing series. Only one starts before 1880, but it is very incomplete before 1900 (France, Ministère du travail, 1921, pp. 152–153). Flandreau and Zumer (2009, table DB.7) provide a series from 1880 that is used by the International Monetary Fund’s historical public debt database and the Jordà–Schularick–Taylor Macrohistory Database. But they provide neither definition nor verifiable source.5 My nominal series varies between –3% and +7% of theirs.

The appendix describes in greater detail the sources used and the various types of securities.

A short history of the public debt

The start date of French public debt is traditionally given as 1522, when the French king issued the first perpetual annuities. In the eighteenth century the public debt consisted of perpetual annuities (which I explain in more detail below) and life annuities. In the mid-eighteenth century the royal government had often borrowed in the form of bonds bearing a fixed coupon and repaid by random draws according to a set schedule, so that the State’s required annual payment (interest and principal) was constant over the course of the loan, usually 15 years.6 At the end of the eighteenth century there was a growing use of life annuities. The floating debt consisted essentially in bills drawn by the Treasury on collectors of direct or indirect taxes. This floating debt usually accumulated until it became unmanageable and was forcibly converted into long-term debt (as happened in 1759, 1770, and 1788). It is well known that the French Revolution began with a financial crisis, as the State could not find fiscal resources to support a growing debt. The search for an assembly that would be authorized to accept new taxes led to the formation of the National Assembly, which began much wider reforms in 1789.

The debt problem was solved by nationalizing the assets of the Catholic church, whose value roughly matched the public debt (increased by the reforms undertaken, such as the abolition of feudalism, which led to compensation of the fief holders). To simplify the repayment of the debt, a currency was created (the assignats), denominated in the standard (metallic) currency of the time, and issued to creditors. Simultaneously, church lands were auctioned off, and purchasers could use the assignats to buy the lands. This can be thought of as a voucher system: A holder of 100 francs (F) debt is given a 100F voucher, which can be used to buy 100F of land at a price determined in the auctions.

A large part, about half, of the debt was indeed repaid, but the start of a European conflict in 1792 transformed the assignat into a fiduciary currency before the liquidation was over. It was still accepted for purchases of land, but to pay for the war it was issued in nominal quantities that vastly exceeded the value of the lands, which was its original backing, and eventually it depreciated to less than 1% of its face value.

Rather than take advantage of the inflation to wipe out the remaining debt, the government, perhaps surprisingly, chose to preserve it by converting the debt into a single perpetual annuity. All debtholders were credited on the general ledger of the public debt (Grand Livre de la Dette Publique). After the collapse of the assignat and the return to a metallic currency, this perpetual debt remained intact in value.7 The government was forced into bankruptcy in 1797, from which only one-third of the debt survived; the other two-thirds were repaid in worthless paper.

The so-called Two-Thirds Bankruptcy marks the start of the nineteenth century public debt. Napoleon did not borrow, at least not from the public. The war expenses were paid through improvements in the fiscal system and compensations extracted from the defeated parties. When the Bourbon king was restored in 1814, he found a debt much smaller than in 1789, but also sizable arrears, in other words Napoleon’s unpaid bills, as well as an indemnity imposed by the allies on France.

Evolution from 1801 to 1914

We have reasonably reliable series for the budgets of the Empire (1804–14), but only the perpetual debt is known. From 1815, it is possible to account for the floating debt as well. It surely existed before, but the existing accounts do not allow a reconstruction.

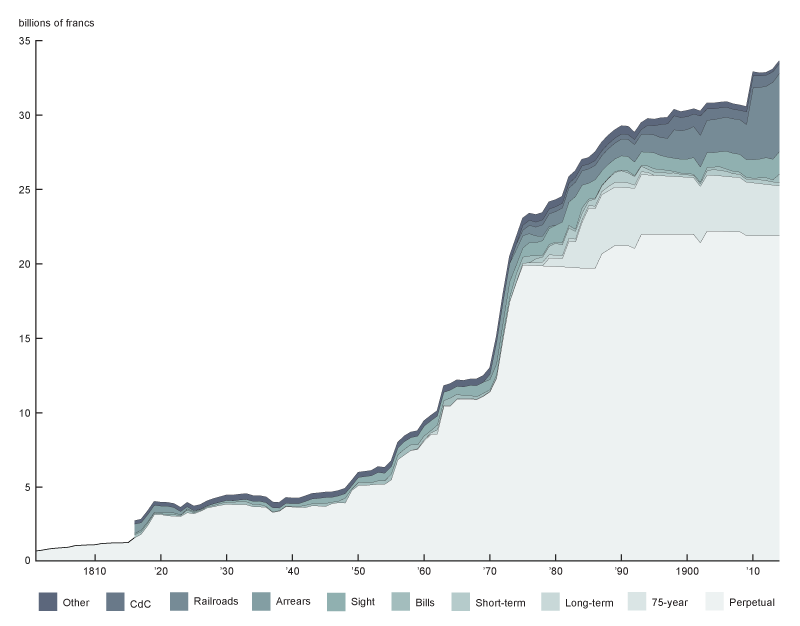

Figure 1 shows the public debt of the French state, therefore excluding local administrations. It is only domestic debt (no debt is issued abroad) and the amounts are nominal—meaning for the perpetual debt, the sum that would extinguish the liability, and for the term debt, the present value of remaining payments discounted at the rate of issue.8 We shall see later that this notion of face value is problematic mostly for the perpetual debt.

1. Public debt in France, 1801–1914 (on January 1)

The figure distinguishes different types of debt. From bottom to top, the debt runs from long term to short term, and the third and second from the top are long term but nonmarketable.

Overall, the stock of debt grows, except for a few periods from 1820 to 1840 and in the early 1900s. There are attempts at amortization, but they are small scale and are not sustained. The debt grows considerably since it goes from 2.7bF (billion francs) in 1816 to 33.6bF in 1914. What does “considerably” mean? I return to this question later, but we can already set aside inflation: The price level was the same in 1820 and 1914.

The century can be divided into three periods. From 1820 (after the arrears of the Napoleonic period are settled) to 1848, the debt increases modestly, from 4.0bF to 4.9bF, and without sharp movements. From 1848 to 1870, the rate of increase changes, as the debt reaches 12.7bF because of the wars of the Second Empire (1852–70) and the public works. Finally, the Third Republic (from 1870) increases the debt to 33.6bF in two stages: a near-doubling after the defeat of 1870 (to 22.8bF in 1876), followed by a sustained increase that slows briefly but picks up again in 1908.

Concerning the instruments, the watershed is 1870. Until then, the French state finances itself the old fashioned way: Only perpetual annuities are issued, and the floating debt consists of Treasury bills and demandable deposits. After the defeat of 1870, perpetual annuities do not increase much and settle at 235bF in 1893, while other instruments appear: mostly a 75-year bond, but also long-term (25 to 35 years) and mid-term (five to six years). Finally, the Third Republic increases enormously the nonmarketable debt, mostly debts to the Caisse des Dépôts and the railroad companies.

Comparing the weight of debt

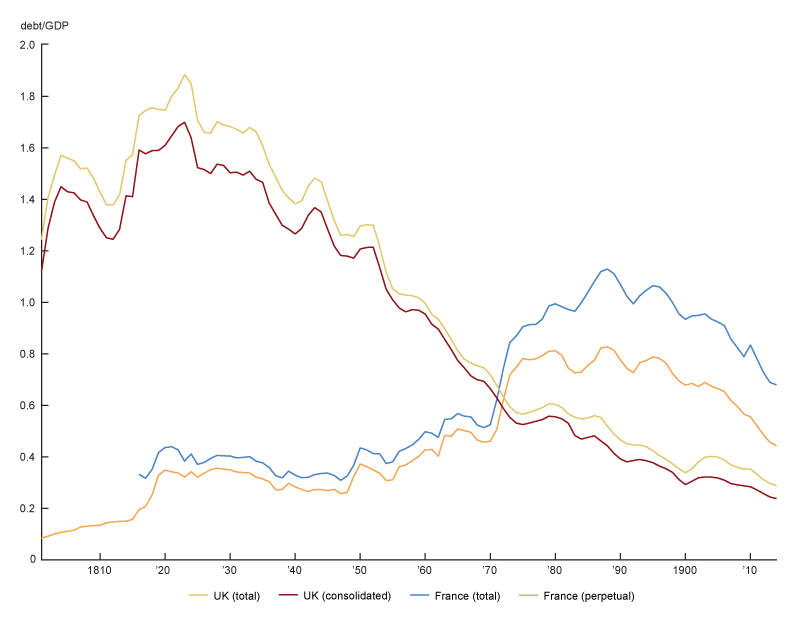

I come back to the question of size. Figure 2 compares the perpetual and total debt relative to gross domestic product (GDP), for France and the United Kingdom (UK).9

2. Debt/GDP ratios in France and the United Kingdom, 1801–1914

When the two nations were briefly at peace in 1802, the debt/GDP ratios were 9% for France and 128% for the UK. Recalling that they were at 65% and 135%, respectively, in 1789 (Sargent and Velde, 1995, p. 486), one can see the effect of selling the National Estates and the Two-Thirds Bankruptcy. By 1820, however, France is at 43% and the UK at 175%. What follows is striking. The UK reduces its ratio from 175% to 29% through a combination of repayment (which reduced the nominal amount by 20%) and (mostly) economic growth. Meanwhile, France seems to follow the same path, albeit slowly, during the years of constitutional monarchy (1815 to 1848). The two countries are also similar in their limited use of nonperpetual debt and their resorting to debt conversion (which I explain later). From 1848 to 1888, France’s ratio goes from 33% to 113%; then the slowdown in debt growth, strong economic growth (almost 2% per year on average), and a little inflation (0.9% per year) bring the ratio down to 68% in 25 years.

Debt and deficits

Debt, when defined from the fiscal point of view, is a cumulation of past deficits and surpluses. To understand its evolution, we turn to budgets.10

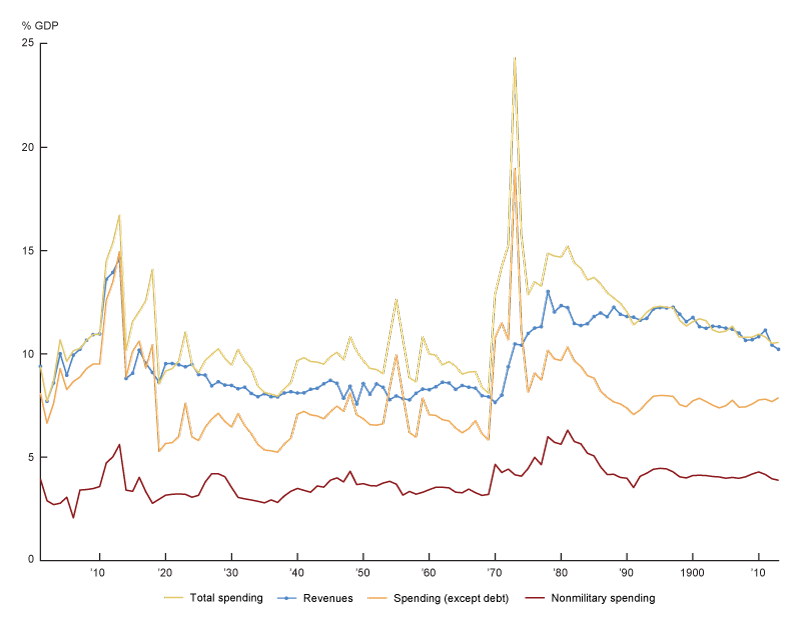

Figure 3 shows revenues and expenditures from 1801 to 1913, distinguishing several spending aggregates: nonmilitary spending, total spending (excluding debt service), and spending (including debt service). These aggregates are compared to revenues (excluding debt), and all series are normalized by GDP.

3. Revenues and expenditures, 1801–1913

As in the eighteenth century, the French state is small, around 10% of GDP. Nonmilitary spending is stable and ends at the same level as it began, about 4%. There is, however, an increase from 1870 to 1890, corresponding to the major investment programs of the Third Republic, notably railroads but also roads and schools. These investment expenditures seem to fade out, but I will shortly explain the reality.

The gap between nonmilitary and total spending is military spending, namely war, navy, and colonies to which I add the consequences of war, such as indemnities paid abroad and war damages compensated domestically.

Wars are clearly the main sources of deficits, as fiscal revenues do not react immediately except under Napoleon I. The 1825 spending spike due to compensation paid out for confiscations made during the French Revolution was completely smoothed out. The other spending spikes chart French foreign policy: the conquest of Algeria from 1830, the more aggressive stance from 1840, the Crimean War of 1855, and the Italian War of 1859. All of these reduce primary surpluses.

The shock of 1870 and the cost of a war is very legible: The fiscal effort that followed pushed revenues from 6% in 1869 to 13.3% in 1878, but the budget is brought into strict balance after 1892.

Yet we have seen that the debt continued to grow after that date. What is happening?

The Caisse des Dépôts and nonmarketable debt

The answer is that debt grows because of expenditures that appear neither in the ordinary budgets nor in the special accounts of the Treasury. There is nothing illegal here: These new debts are authorized by the annual budgetary laws, but they correspond to expenditures (past, present, or future) that now appear in the State accounts. There are two forms, which I discuss in turn.

First is the Caisse des Dépôts (Aglan, Margairaz, and Verheyde, 2006), a fund or bank created in 1816 at the same time as the Caisse d’Amortissement (sinking fund) to hold deposits mandated by law in cases of bankruptcies, disputes, inheritances, and property seizures; bond monies and deposits made by contractors of public works; and voluntary deposits made by those who sought safety, such as savings banks. After the mid-nineteenth century, it also managed various funds created by the State, such as insurance and retirement funds, and loans to local governments for construction of roads and schools. In effect, its deposits were “sticky.”

The Caisse invested the savings deposits it received in public debt, floating or perpetual. Thus, a sizable portion, up to 60%, of the floating debt consists of (usually interest-bearing) deposits made by the Caisse with the Treasury. It also lent to the various State funds it managed when necessary. For example, if the subsidies paid by the State to the fund for building local schools were insufficient for the planned constructions, the Caisse provided the missing sums. When the special funds were wound down, the loans made by the Caisse suddenly appeared in the national accounts as government debt, usually rescheduled in ten- to 20-year annuities computed at an administrative interest rate.11 Strangely, perhaps, the Bank of France was the central bank but not the State’s bank: the Caisse des Dépôts played the latter role, at short as well as medium and long term. The Bank of France lent only twice: in the most extreme emergencies of 1848 and 1870, and in the second instance, through a line of credit of 1.5bF. Rather than capitalists, small savers were knowingly or not enrolled into providing liquidity to the State, on terms they did not negotiate.

Investment in infrastructure

The second component of nonmarketable debt follows from the policy of investment in canals and railroads.

The first major program of investment in infrastructure started in the 1820s, when the government decided to push for the expansion of canals in France (Geiger, 1984). The plan was for the State to build and operate the canals with funds provided by the private sector. The State would borrow the necessary sums and pay interest on the loans until completion, after which revenues would be shared with the lenders (incorporated in joint-stock companies). The companies’ shares of the revenues were bought out in 1853 and 1863 in exchange for annuities, but the loans continued to be reimbursed until 1872.

Railways attracted the attention of the government in the 1830s, but it took several years to establish a legislative framework.12 The major question was the distribution of roles between the State and the private sector in financing, building, and operating railways. The compromise reached in 1842 was to grant fixed-term concessions to private companies: The State chose the lines and built the infrastructure (earthworks, engineering works, and buildings); the companies laid the rails, provided the rolling stock, and operated the railways under State supervision. At the end of the concessions, the railways would be at the State’s disposal, after the State had compensated the companies for the then-current value of their investments. Each party financed itself, and from 1840 to 1849 the State spent 0.5bF, about 4% of its fiscal revenues. In practice, there were some variations in the arrangements, with companies often accepting to build the infrastructure in exchange for longer concessions. There were also punctual loans and subsidies, but of limited importance.

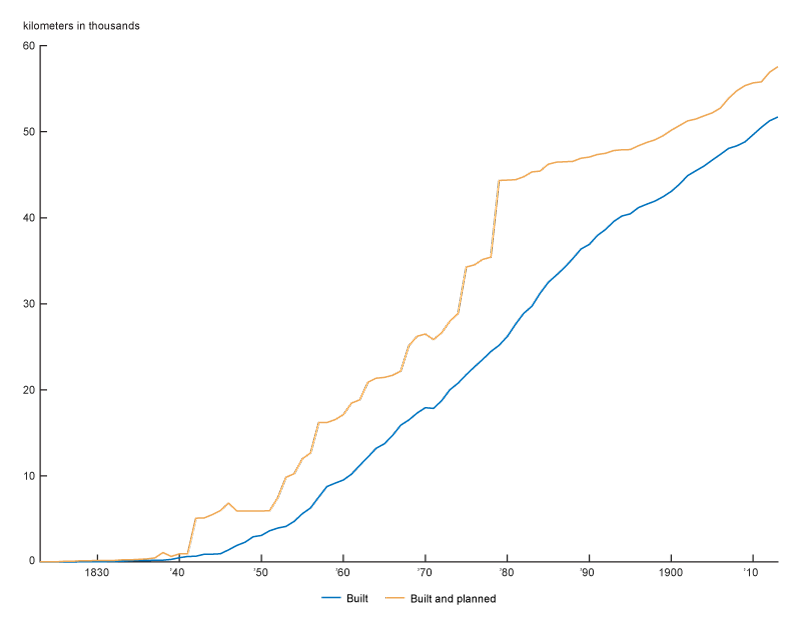

Growth stalled in the late 1840s, as seen in figure 4, because of a financial crisis and economic contraction in 1847–48 and the fall of the monarchy in 1848; it was replaced by a less business-friendly republican regime. Napoleon III came to power in 1851 with a view to expand the network massively, a desire that became more pressing with the free trade agreement with the United Kingdom in 1860. In a first stage, from 1852 to 1856, he encouraged the emergence of six principal companies controlling regional networks in exchange for their undertaking an expansion into less-profitable lines at their expense. The total planned size jumped from 6,000 kilometers (km) to 16,200 km from 1851 to 1857, but the commercial and financial crisis of 1856 showed that the companies needed support. A new deal emerged between the State and the six companies from 1857 to 1863. The companies saw their concessions extended to 99 years, into the mid-1950s. They confirmed their commitment to building secondary lines but received financial support of two forms.

4. Length of French railways, 1823–1913

The first form of support, put in place in 1859, was a rate of return guarantee scheme (garantie d’intérêt), a device used once in 1839: For a period of 50 years, the State would compensate the companies if their net revenues were insufficient to service their debt and pay a defined return on their equity. The guarantee only applied to future lines, and a complex formula was devised so that profits on the existing network (built first and more profitable) were used to cross-subsidize the new lines before calling on the State. This compensation was not a subsidy but an interest-bearing loan, repayable as soon as revenues started exceeding the guaranteed minimum, and at the latest at the end of the concession. Once the debt had been paid off, the State was entitled to a share of profits above the guaranteed return. The return guarantees were therefore contingent liabilities of the State.

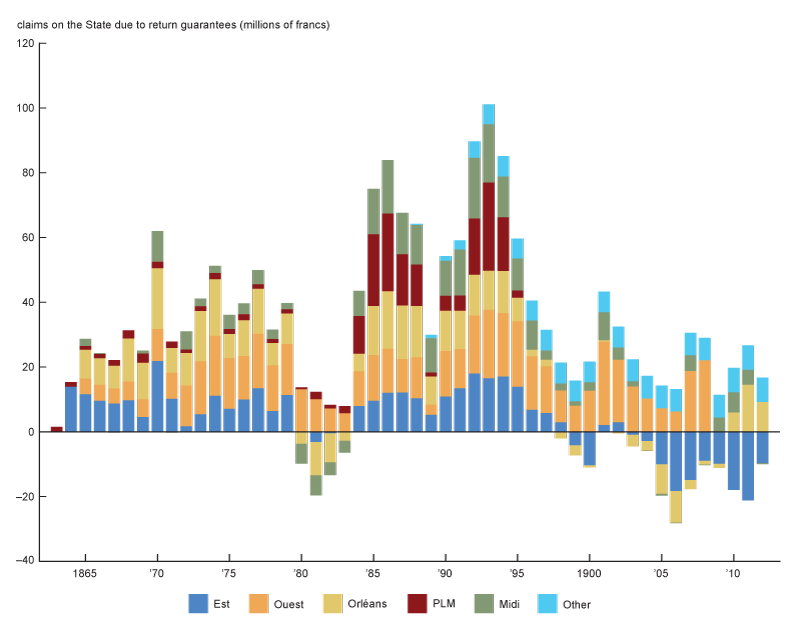

Figure 5 shows the claims made by the companies on the State pursuant to these guarantees from the inception of the scheme to 1913. In aggregate, the companies used the scheme almost all the time and were rarely in a position to repay the sums borrowed. But there were differences across the six companies. The Compagnie du Nord, to Belgium and the United Kingdom, was so profitable that it never made any claim. The Compagnie de l’Est (to Germany) and the PLM (to Lyon and the Mediterranean) both became solidly profitable in the 1890s.13 At the other extreme, the other three railways, which covered the west and southwest of France, never became profitable, and in fact the Compagnie de l’Ouest was bought by the State in 1908.

5. Claims of French railway companies under the return guarantee scheme, 1863–1913

Source: France, Ministère des travaux publics (1914, pp. 383–385).

The key point of figure 5 is that the contingent liability created by the scheme was both substantial and highly variable, the reason why I exclude it altogether from the public debt. In principle, this liability was netted out by the claims on the companies. In fact, as the example of the Compagnie de l’Ouest showed, those claims were bounded above by the value of the company, but the liability wasn’t. Effectively, by the time the French state nationalized the railway companies in 1938, it had already bought them.

The second form of support, experimented with in 1857 and generalized in 1863, consisted of straight-out subsidies, but paid over time rather than immediately. They were liabilities of the State, and I count them as part of the public debt. There were two variants: The first created marketable debt and the second did not. In 1857 the subsidies were paid in the form of government long-term bonds handed over to the companies, which could then sell them to raise funds. The State eventually realized the inherent hold-up problem and adopted a modified system in 1863. Companies were to build new lines at their expense: Once a line was completed, the corresponding subsidy was settled and an annuity was paid to the company until the end of its concession. Companies could use the expectation of the annuity to raise funds immediately.14

Two other events need mention. In the aftermath of the 1870 defeat, the Republican government decided to expand the network massively. The Freycinet plan, named after the minister who promoted it, increased the planned size of the railway network by 25% in 1879. This time, the companies were in a position to extract better terms from the government for their cooperation. The resulting conventions of 1883 extended the return guarantee scheme to all the companies’ lines. One improvement obtained by the government was that the rate used to convert the subsidies into annuities would be tied to market rates (based on the companies’ cost of financing).

Marketable debt

After discussing the nonmarketable debt, I turn to the negotiable instruments used during the century.15 The restored monarchy used the same instruments as the Old Regime, albeit with more rigorous accounting. After 1870 instruments become more diverse, however, without providing a modern yield curve.

Perpetual annuities

The main form of debt remained the so-called consolidated debt, which consisted of perpetual annuities.

The instrument is quite old, as it had been used for private credit since medieval times. The perpetual annuity, which results from an exchange of capital for a promise of constant annuities, always included a redemption clause for the debtor. This important option had been exercised several times, most recently in 1719 for the whole debt. In 1793 all existing debt, perpetual or not, was converted into a single type of annuity at 5% and entered as entries on the General Ledger of the Public Debt, which remained the basis of the public debt throughout the nineteenth century.

The perpetual annuities took various forms. Originally the annuity was registered: Each owner had an entry on the general ledger. In 1831 the first bearer perpetuals appeared, then in 1864 perpetuals whose coupons were to the bearer. Coupons were paid twice a year as under the Old Regime, then quarterly payments were phased in from 1862 to 1887. Payments were made in Paris or outside by tax collectors, and from 1897 by the Bank of France through its network of branches. Transferring ownership required a certificate signed by a broker or a proxy in the name of a Treasury official. Annuities enjoyed various legal privileges: They were exempt from seizure or attachment and taxes, except transfer taxes. The minimal size depended on the issue, but the annuity could be as low as 2F.16 Figure A1 in the appendix lists the issues of perpetual annuities that took place.

A similar instrument, the 3% amortissable (terminable annuity), was created in 1878. The bonds, of 300F minimum size, were allocated in 175 series that were to be redeemed over 75 years by random draws on a preset schedule. These bonds could not be redeemed ahead of schedule. A few more issues were made until 1884 on the existing schedule, but the bond won little favor and issues ended.

The 75-year term was chosen because the issue was intended to finance the Freycinet plan. The finance minister matched the term of the bond with the duration of the railroad concessions.

Until the Franco-Prussian War of 1870, the perpetual annuity was nearly the only instrument used. The only exceptions were two issues of 30-year bonds in 1859 and 1861, bearing 4% to raise funds for railroad construction. The State created the bonds and turned them over to the railroad companies. The 1850 issue was sold to the Caisse des Dépôts, but the 1861 issue was sold to the public. After the war of 1870, similar issues took place. The “Morgan loan” at 6% over 34 years was the result of an agreement with the U.S. bank J. S. Morgan and sold to the public. It was voluntarily converted into 3% perpetuals in 1875 once France’s credit had been restored: Bondholders were offered to keep the annual revenue but pay for the increase in face value. Then 25-year bonds of 500F each were issued in 1875, as well as other 30-year bonds from 1878 to 1885, to finance postwar reconstruction and compensations. All that remained were redeemed before maturity in 1890. Figure A3 in the appendix lists the issues of long-term debt.

Finally, six-year bonds with half-yearly coupons were first issued in 1875 to finance a rearmament special program and for another additional budget in 1878. Other issues followed in the 1880s, as well as rollovers of maturing issues. After an interlude from 1892 to 1902, more issues followed until 1908.

Aside from the choice of instruments, debt management raised several issues around the conversion of annuities, the issue of annuities at par or above, and strategies for sinking funds.

Conversions

The principle of annuity conversion, which the State as debtor could redeem them at par at any time, was beyond doubt from the legal point of view but difficult to implement. Figure A2 in the appendix lists the conversion operations that took place.

In 1825 the finance minister wanted to take advantage of the fall in interest rates to exercise the redemption option, but he could not defeat the opposition in the French House of Lords and had to limit himself to a voluntary conversion into a 3% annuity (keeping the annual income constant but increasing the capital) or into a 4.5% protected from redemption for ten years. Only in 1852, when a Senate appointed by Napoleon III replaced the House of Lords, was there a mandatory conversion of the 5% into cash or into a 4.5% annuity protected from redemption for ten years; the latter option was chosen by almost all annuity holders. When the ten-year protection expired, an optional conversion was offered into a 3% annuity, keeping the annuity constant and paying the market value of the difference. This was in effect a disguised loan, and one-third of the annuities were converted.

The War of 1870 depressed the price of annuities and only 5% annuities were issued, but as after the previous defeat, credit improved quickly and in 1883 the 5% annuities were redeemed or converted into 4.5% securities protected for ten years from redemption. In 1887 the existing 4.5% and 4% annuities were converted into cash, 3% with the same capital, or 3% with increased capital and payment of the difference. In 1894, when the ten-year protection expired on the 4.5% of 1883, it was converted into 3.5%. A final mandatory conversion took place in 1902, turning all perpetuals into a homogenous 3% title protected until 1910.

Conversions were hence used, either to lower the debt service or to keep it constant but allow the government to borrow more cheaply.

This overview shows that the exercise of the option inherent in the perpetual annuity was a reality. Even when the conversion was mandatory, it was not a default as sometimes thought. The only default, in the modern sense of the word, in the period under consideration took place in 1848, when the short-term Treasury bills were forcibly converted into perpetual annuities at face value.

New perpetual annuities were issued numerous times at different rates, which did not always match the market rate. Suppose that at a given time the very long-term interest rate was 5%, the 5% annuity was at 100F, and the 3% annuity at 60F. The State could sell a 5% annuity at par and receive 100F for every 5F of annuity redeemable at 100F, or sell a 3% annuity below par and receive 100F for each 5F annuity but redeemable at 167F. The trade-off for the buyer is to be more or less protected from a fall in interest rates: the 3% annuity will come up for redemption much later than the 5%, and only if rates fall enough that the value of the remaining annuity rises above 167F. In reality, of course, the price of the State’s option must be embedded in the market price, and the State will receive less than 100F by issuing a 5% annuity, because it will pay more to buy an option in the money.

It follows that the nominal or face value of a rent is not a very good measure of its burden: A 5F annuity at 5% will last less at 5F because it will be converted sooner, whereas a 3F at 3% will last longer before conversion. The market value measures the difference in value between these two streams of future payments.

Figure 6 clearly shows these differences. If the option had no value, in other words if the conversion risk did not matter, the price of a 1F annuity would vary over time but would be identical for a 3% or a 5%. Indeed, the prices of the different types of annuities fluctuate in tandem with interest rates and the State’s creditworthiness but with, at times, important spreads. Thus, on July 15, 1825, a 1F annuity of the 5% was at 20.68F while a 1F annuity of the 3% was at 25.42F. On that day, issuing 100F at par in 5% would cost the State 4.83F annually whereas issuing 100 F in 3% would cost 3.93F. The redemption price would be 96.60F for the former and 131F for the latter. The stream of payments associated with the 3% would be lower but longer and with a larger final payment.

6. Market price of a 1F perpetual annuity depending on the type of annuity de rente

Sources: France, Ministère des finances, 1818–25 and 1826–1914, and dfih.fr, accessed on May 18, 2022.

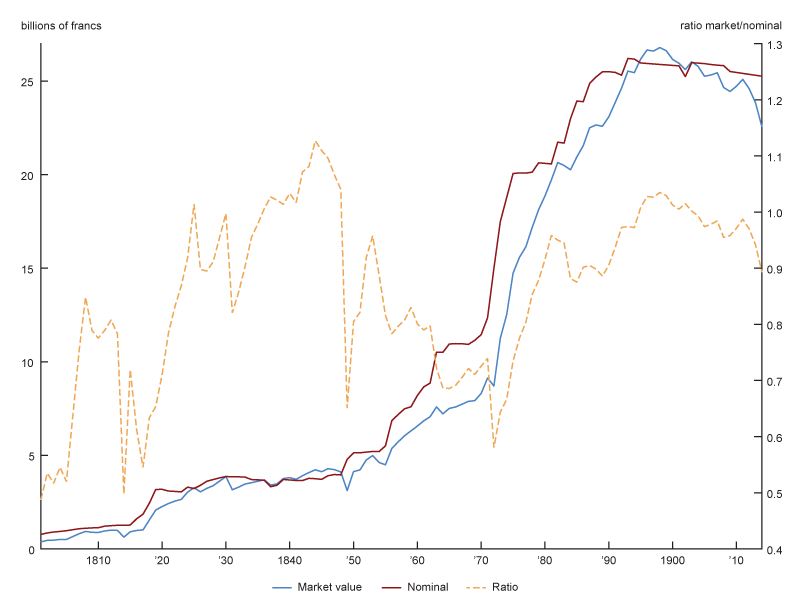

Nominal and market value

The nominal values were calculated as follows. Perpetual annuities are valued at their strike price, that is, the price at which the government can legally redeem them. The long-term and short-term debt are valued at their face value. The annuities are valued at their internal rate of return at issue (if the liability for which they are issued is stated) and depreciated over time. This is actually rather complicated in the case of the railway annuities. Those issued before the 1883 conventions had a stated rate of interest (usually 4.5%), but those created after 1883 were indexed to the market rate of railways obligations. Each year, as railway companies spent on construction, an addition to their annuities was calculated with its own rate of return. I use these rates to compute the depreciating value of the annuities over time.17

Consider now figure 7, which shows the market value of the perpetual annuities, 75-year terminable annuities, and long-term bonds. The secular evolution is similar but with large differences—of two kinds. Political events (defeats, revolutions) result in falling prices of the perpetual in 1814, 1830, 1848, and 1870, but these falls last three to six years. The spread between the two lines from 1825 to 1830 and from 1853 to 1880 is due to a composition effect: the State issues rents below par, which inflates the nominal value compared to the market value of future payments.

7. Nominal and market value of the perpetual annuities

The sinking fund obsession

The nominal weight of the debt was nevertheless a constant preoccupation. Here again, the roots go back to the eighteenth century and even earlier. Ruins of sinking funds are scattered throughout the financial history of France just like that of Britain. The idea of the sinking fund, popularized at the end of the previous century by Richard Price, consisted in endowing a fund with a constant annual sum. The fund used this annual sum, as well as the interest it collected on the debt it had bought back, to buy more debt. Mathematically, these buybacks increased exponentially if the fund spent all its income on debt buybacks. But the public debt as a whole would not shrink if the fund’s endowment did not come from actual surpluses.

Napoleon had created a sinking fund, but he used it as a rather opaque bank, and it was replaced by a sinking fund under parliamentary control in 1816 (Aglan, Margairaz, and Verheyde, 2006). It had an active role in the annuity market in the 1820s and its endowment did come from actual surpluses, but the 5% annuity soon reached par and it was illogical to buy it at a premium when it could be converted at par. Although (as we saw) the conversion did not take place, the fund was nevertheless forbidden from buying above par, but continued to be endowed even in times of deficits. That is, either the State borrowed to buy back its debt or it accumulated reserves, which it lent to itself. The pointlessness was eventually acknowledged, and the fund was abolished in 1871.18

The desire to sink the debt did not disappear and motivated the move from perpetuals to instruments with fixed terms noted earlier, with the disadvantage (or advantage, if a legislature can constrain its successors) of imposing a redemption calendar independent of fiscal circumstances. The inherent difficulty became obvious at the last attempt at redemption in 1902: Part of the perpetual debt held by the Caisse des Dépôts was converted into a 30-year annuity, but the following year the operation was undone and the converted perpetual annuity was recreated (hence the blip in 1902 in figure 6).

Conclusion

In 1802, the public debt had been brought down from 65% of GDP before the Revolution to 10% in two steps: Church lands paid off a part, and the bankruptcy of 1797 wiped out another. Napoleon’s regime was starting afresh.

Given the cost of his wars, he increased the debt only mildly, because pillaging worked as long as victory was on the right side. The restored monarchy that followed him adopted the British model, favoring economic growth and restoring public credit.

At the other end of our period, in January 1914, the debt was at 68% after having reached 113%. Many events had taken place in between, with two of them dominating. The defeat in the Franco-Prussian War was a catastrophe in many respects, including fiscal: The indemnity imposed by Bismarck was 2.5 times and all the war-related costs were seven times the annual budget.

France had to borrow, and although it had not been prepared militarily for the war, it had ample fiscal room.

The other factor was the railroad or, more broadly, infrastructure policy. The State’s financial commitment began in the 1840s and increased steadily, especially after 1878. Here fiscal space was used, not in an emergency to pay for a mistake, but deliberately with a long-term view.

For the rest, fiscal management was fairly prudent whatever the political regime. Let us leave the last word to the market: In spite of the secular increase in the debt, the French perpetual annuity had a yield of 11% in 1802 and 3.5% in 1914.

Note: This article is a translation and extension of work originally published in Velde (2022).Notes

1 A life annuity is a constant annual payment that lasts as long as the life of a named individual (or the last surviving of a group of named individuals). The annuity cannot be bought out by the debtor and there is no capital repayment, so there is no concept of face value. The French government sold life annuities extensively in the eighteenth century, but it never did after 1788.

2 I also exclude local government debt, which is only known from the 1880s (France, Ministère du travail, 1921, p. 171). Its size was about 12% of the central government debt in 1885 and 18% in 1914.

3 For this purpose, I use the price data in the Data for Financial History (DFIH) database, a comprehensive database on French stock markets since 1785, available online.

4 I rely on the official Comptes généraux de l’Administration des finances published annually from 1817 and described in the appendix.

5 Flandreau and Zumer (2009, p. 101), cite “a variety of sources, with the Lyonnais archives as a final judge.”

6 This works just like a fixed rate mortgage: The regular payment is constant but comprises a growing share of the capital repayment over time. But instead of repaying each bond a fraction of its capital every period, a lottery chooses which bonds are repaid fully.

7 Until 1801, the coupons were paid in a variety of paper rather than metallic currency, but at least the paper was accepted in payment of taxes.

8 Public accounts only use discounting systematically from the 1890s. Until then, the face value was computed as the undiscounted sum of remaining payments. I have corrected as much as possible.

9 The British data come from the Bank of England’s data set A Millennium of Macroeconomic Data, and French GDP from Toutain (1987). Before 1815, I use Toutain’s estimate for France in current borders for the 1803–12 decade, thus ignoring territorial changes. Debt on January 1 is divided by the three-year average of GDP centered on the previous year.

10 The sources for budgets are as in endnote 4. I include in spending the indemnity paid to the Allies from 1815 to 1818, the compensation paid to former emigrés from 1825 to 1841, the indemnity to Germany from 1871 to 1876, and the liquidation accounts (war compensations) from 1872 to 1882. These expenses were off budget but financed by debt. I deduct from revenues and spending the fonds spéciaux, which disappear from budgets in 1892. The 15-month budget straddling the Republican and Gregorian calendars (1805–06) is annualized. More generally, as explained in the appendix, the Treasury’s special services constituted a variety of side budgets that would need to be fully integrated into the budget numbers.

11 The rate, and hence the annuities, were subject to reductions when interest rates on the public debt fell, which will be explained further: The rate of 4% was lowered to 3.5% in 1892 and to 3% in 1896. The same was done on a debt difficult to classify, namely, the bond monies posted by various treasurers: The rate fell from 5% to 4% in 1816, 3% in 1844, and 2.5% in 1898. These bond monies had been a classic source of funds in the eighteenth century and still represented 7% of the public debt in 1816, but they became negligible over the century.

12 See Picard (1884–85 and 1918) for a contemporary account—written by one of the protagonists—and Caron (1997) for a modern synthesis.

13 In 1897 PLM made an arrangement with the government. The company’s outstanding debt was settled at 151mF (million francs) and it accepted an annual reduction of 6mF in its other annuities to pay it off. The company did not call on the scheme again. Losses it made in 1901 and 1902 were covered from reserves, and it shared profits in 1898 and 1906–08.

14 In a number of cases the companies made advances to the government to build lines, and the government repaid with annuities. This is financially equivalent to the subsidy method. The rate of interest was generally 4.5% for both subsidies and advances.

15 See Ducrocq (1904, tome 5) for an exhaustive and rigorous guide.

16 For comparison purposes, £1 = 25.22F and $1 = 5.18F.

17 I use the data in Le Trocquer and Doumer (1921, pp. 44–45, 70–71, 98–99, 121–122).

18 From time to time, the annuities held by the fund were canceled, which resulted in abrupt decreases in the public debt. Instead, I have netted the sinking fund’s holdings of annuities from the public debt.

Appendix: Data Sources

The major source for this article is the Compte général de l’administration des finances (France, Ministère des finances, 1818–25, 1826–1914)—an annual publication of France’s ministry of finance that started by covering the year 1817.i Although political regimes varied through the nineteenth century, oversight of public finances by the legislature remained a constant: Taxes and loans required laws, budgets were voted by the legislature every year, and the accounting division of the ministry of finance submitted this report every year. The main part of the publication contains general accounts: receipts and expenditures, budgets, cash management, and the balance sheet of the Treasury (Trésor), as well as special services, which I will discuss more shortly. The remainder of the publication consists of special accounts, including those related to various items of the debt. The budget law of 1898 mandated a complete account of the public debt, which was henceforth contained in a second volume of the publication and became more comprehensive than earlier reports.

The Treasury was the financial representation of the State and served as its cashier (Say, Foyot, and Lanjalley, 1894, Vol. 2, p. 1442). Its balance sheet contained assets and liabilities, but only financial assets were counted, namely, cash and securities (valeurs de caisse et portefeuille) as well as claims on various parties. Thus, the Treasury’s balance sheet did not represent that of the State as a whole—which would require the value of all its assets and the capitalized value of all its liabilities and which France never attempted to establish (France, Ministère des finances, 1914, Vol. 1, p. 557, covering the accounts for fiscal year 1913). Instead, the Treasury kept accounts with various outside entities (tax collectors and payers, local governments, the Banque de France, and the Caisse des Dépôts et consignations). It also used kept accounts to track various services it undertook for the State, namely, the service of the budgets and the special services, which I describe next.ii

The service of the budgets consisted of keeping track of ways and means and appropriations (authorizations to collect revenues and carry out expenditures) as determined by annual budget laws. Each fiscal year (exercice) was tracked for two years and then closed, with the balance (deficit or surplus) to be settled by the legislature in a budget review act (loi de règlement). These acts, prepared by the ministry of finance, were supposed to be passed shortly after, but by 1913 the delays had reached five to ten years. In the meantime, the Treasury funded the deficit (or used the surplus) through the floating debt. Cumulated and unfunded deficits constituted Treasury advances, part of the assets of the Treasury (that is, claims on the State).

The Treasury’s balance sheet was complex. On the asset side, some claims were on the State, others were on other entities. The claims on the State arose from deficits, either on the service of budgets or on special services. The claims on other entities could arise from various reasons, essentially when the Treasury had advanced resources in expectation of future repayments. When examining the State’s financial position, I have noted that the claims on it were not assets of course. But claims on other entities might or might not have been assets, depending on the plausibility of the future repayments. The only item on the asset side that was unambiguous were cash and securities owned outright by the Treasury, and these could be subtracted safely from total liabilities. Handling the other assets required making judgments on their future performance. For this reason, I have preferred to compute the gross public debt, without any netting.iii

Special services

The services spéciaux du Trésor were separate accounts keeping track of various operations outside normal budgets. The practice originated in 1836, but these special services were not systematically reported until 1878. These accounts tracked financial operations that spanned a number of years, sometimes decades. Services were either creditors or debtors. An example of the former is the service created for the 3% amortizable bonds issued in 1884: Sums received from loan subscribers were credited to the account and debited over time as they were applied to successive budgets from 1883 through 1887, at which point the account was closed. An example of the latter is the service for loans to industry: A law of 1860 authorized loans up to 40mF (40 million French francs) to industrial firms, financed by Treasury bills. It was a debtor service from the start and was expected to be credited with reimbursed loans, although by 1913 it had remained a debtor.

The use of special services expanded after 1870, and was repeatedly criticized in parliament as creating ways for the government to spend (by increasing the floating debt) without parliamentary authority. By the 1890s the practice had been reined in, but a comprehensive account of spending would need to incorporate them as appropriate—something I have not done, with some exceptions.

Perpetual debt

The perpetual debt (dette inscrite, because it consisted in entries of the general ledger, or dette consolidée) was the main debt instrument.

The perpetual annuity could take three forms of securities: registered, bearer, or mixed. The registered security, originally the only form possible, was a certificate of the owner’s entry in the general ledger of the public debt (Grand Livre de la Dette Publique), with the owner’s surname, other names, description, and the amount. There were no coupons, and payment was made upon presentation of the security, which was then stamped on the back. Bearer securities were introduced in 1831, and had ten years’ worth of coupons payable to the bearer. Mixed securities, introduced in 1864, were registered, but with bearer coupons. Annuities could be converted from one type to another on demand. By 1914, 70% of the annuities (by value) had been registered. The minimum size in 1914 was 2F. Coupons were paid at the offices of tax collectors twice a year until 1862; after that date, coupons of new issues or conversions were paid quarterly.

Figure A1 lists the issues of annuities during our period.iv There were three main ways of issuing new debt: Early on, the government sold directly to bankers; from 1821 on, it asked for bids from banking syndicates; and from the 1850s on, public subscription became the norm. In addition to these primary methods of issuing debt, annuities were also created to settle liabilities of various forms. Instead of issuing debt to raise cash and pay off liabilities, the State created new annuities and gave them in payment. The most substantial were as follows. Under Napoleon I, 27.8mF of 5% annuities were created to pay off arrears or debts, with another 6mF to replace the public debt in annexed territories. The 1815 War indemnity was payable in cash and had to be funded by issuing annuities, but another 27.8mF of 5% annuities were created between 1816 and 1822 to settle various domestic and foreign debts. In 1820, 26mF in 3% annuities were created to compensate people who had fled France during the Revolution for confiscated property. A railway was bought in 1848 with a 6.8mF 5% annuity; the Treasury bonds on which the government defaulted the same year were converted into 2.2mF 23% annuities, and the abolition of slavery in French colonies resulted in 5.8mF in 5% and 4.5% annuities (capital value of 120mF). Finally, 5.7mF in 3% annuities were created in 1868 to compensate holders of Mexican debt after the collapse of the imperial regime established in that country by France.

A1. Issues of perpetual annuities

| Purpose | Fund (%) | Size (mF) | Date | Price (F) | Mode of issue |

|---|---|---|---|---|---|

| Arrears | 5.0 | 6.0 | 1816, 1817 | 57.26* | Open market |

| Arrears | 5.0 | 30.0 | 1817–18 | 57.51* | Open market |

| Arrears | 5.0 | 14.9 | May 1818 | 66.50 | Various subscribers |

| War indemnity | 5.0 | 12.3 | Oct 1818 | 67.00 | Banks |

| War debts, arrears | 5.0 | 9.6 | Aug 1821 | 85.55 | Banks (auction) |

| Arrears, deficit 1823 | 5.0 | 29.1 | Jul 1823 | 89.55 | Banks (auction) |

| Deficits 1829–30 | 4.0 | 3.1 | Jan 1830 | 103.075 | Banks (auction) |

| Deficits 1831–32 | 5.0 | 7.1 | Apr 1831 | 84.00 | Various lenders |

| Deficits 1831–32 | 5.0 | 7.6 | Aug 1832 | 98.50 | Banking syndicate (auction) |

| Public works | 3.0 | 5.7 | Oct 1841 | 78.525 | Various lenders |

| Public works | 3.0 | 7.1 | Dec 1844 | 84.75 | Banks (auction) |

| Public works | 3.0 | 2.6 | Nov 1847 | 78.35 | Banks (auction) |

| National loan | 5.0 | 1.3 | 1848 | 100.00 | Various subscribers |

| Deficit 1848 | 5.0 | 13.1 | Jul 1848 | 75.25 | Various subscribers |

| 250mF loan (Crimean War) | 4.5 | 4.6 | Mar 1854 | 92.50 | Public subscription |

| 250mF loan | 3.0 | 7.2 | Mar 1854 | 65.15 | Public subscription |

| 500mF loan | 4.5 | 8.1 | Jan 1855 | 92.00 | Public subscription |

| 500mF loan | 3.0 | 15.9 | Jan 1855 | 65.15 | Public subscription |

| 750mF loan | 4.5 | 4.4 | Jul 1855 | 91.15 | Public subscription |

| 750mF loan | 3.0 | 31.7 | Jul 1855 | 65.15 | Public subscription |

| 500mF loan (Italian War) | 3.0 | 25.2 | May 1859 | 60.00 | Public subscription |

| 500mF loan | 4.5 | 0.6 | May 1859 | 90.00 | Public subscription |

| Conversion of 30-year bonds | 3.0 | 12.1 | 1862 | 66.49* | |

| 300mF loan | 3.0 | 14.2 | Jan 1864 | 66.30 | Public subscription |

| 429mF loan | 3.0 | 19.5 | Aug 1868 | 69.25 | Public subscription |

| 750mF loan | 3.0 | 39.8 | 1870 | 60.60 | Public subscription |

| 2,000mF loan | 5.0 | 140.0 | 1871 | 82.50 | Public subscription |

| 3,000mF loan | 5.0 | 207.0 | 1872 | 84.50 | Public subscription |

| 500mF loan | 3.0 | 18.9 | May 1886 | 79.80 | Public subscription |

| Loan | 3.0 | 28.2 | Jan 1891 | 92.55 | Public subscription |

| Conversion of 4.5% annuities | 3.5 | 0.0 | 1894 | 106.93 | |

| China expedition | 3.0 | 8.0 | 1901 | 100.00 |

Source: France, Ministère des finances, 1920, Vol. 2, p. 16, covering the accounts for fiscal year 1914.

Figure A2 lists the conversions of annuities (Ducrocq, 1904, pp. 121–129). The conversion of 1825 was voluntary after a bill for a mandatory conversion was defeated in the House of Lords. The offer was to exchange 75F face value of 5% for 100F face value of 3% (thus reducing the coupon, but increasing the face value), or 100F of 5% for 100F of 4.5% with protection from conversion for ten years. The offer had a limited success, as only a quarter of existing annuities were exchanged. Further attempts at mandatory conversion were repeatedly defeated in the upper house of parliament, and only under the more authoritarian regime of Napoleon III was it possible to push a law through a docile parliament. The 1852 conversion gave the choice between the face value in cash or a reduction in the coupon to 4.5%, but with a protection from conversion for ten years; the vast majority of annuitants opted for the latter. The 1862 conversion was voluntary: Annuitants had the option to a 1F annuity at 4.5% or 4% into a 1F annuity at 3% (increasing the face value) by making a cash payment; effectively, it was an unofficial loan. The 1883 conversion, like the 1852 conversion, gave the choice between cash or a reduction in the coupon from 5% to 4.5% with a ten-year protection. The 1887 conversion was mandatory, but like the 1862 one, it was also a way to raise funds: Holders of 4.5% and 4% annuities who did not want to receive cash could receive new 3% annuities at set ratios (0.833F 3% annuities for 1F in 4.5% or 0.937F for 1F in 4%) and the option to make up the reduction in coupon by buying more 3% at a slight discount over market rates. The 1894 conversion took place when the ten-year protection given to convertants in 1883 expired, giving the choice between cash or a reduction from 4.5% to 3.5% with an eight-year protection; the new 3.5% annuities were converted when that term expired, again with a choice between cash or a reduction in interest (but with a 1% premium added to the next coupon payment) and an eight-year protection.

A2. Conversions of perpetual annuities

| Date | Conversion from | to | Size (mF) | Note |

|---|---|---|---|---|

| (- - - - percent - - - -) | ||||

| May 1, 1825 | 5.0 | 4.5 | 1.0 | Voluntary |

| May 1, 1825 | 5.0 | 3.0 | 24.5 | Voluntary |

| Mar 14, 1852 | 5.0 | 4.5 | 158.1 | |

| Feb 12, 1862 | 4.5 and 4.0 | 3.0 | 135.2 | Voluntary |

| Apr 27, 1883 | 5.0 | 4.5 | 306.2 | |

| Nov 7, 1887 | 4.5 and 4.0 | 3.0 | 37.6 | |

| Jan 17, 1894 | 4.5 | 3.5 | 237.6 | |

| Jul 9, 1902 | 3.5 | 3.0 | 203.6 | |

Source: France, Ministère des finances, 1920, Vol. 2, p. 16, covering the accounts for fiscal year 1914.

Terminable 75-year annuity of 1878

The 3% amortissable (terminable annuity), was created in 1878 (Ducrocq, 1904, pp. 161–173). Annuities could be either registered or to the bearer at the buyer’s choice—in the latter case taking the form of bonds ranging from 500F to 100,000F, in the former case in multiples of 500F (see figure A3). All annuities were allocated in 175 series, which were to be redeemed over 75 years by random draws on a preset schedule. These annuities could not be redeemed ahead of schedule; that is, they were not callable.

A3. Long-term debt instruments

| Date | Size (mF) | Rate | Term (%) | Note |

|---|---|---|---|---|

| Dec 1858 | 100.0 | 1889 | 4.0 | trentenaires |

| Aug 1860 | 100.0 | 1889 | 4.0 | trentenaires |

| Jul 1861 | 150.0 | 1889 | 4.0 | trentenaires |

| Oct 1870 | 250.0 | 1906 | 6.0 | J. S. Morgan loan, callable |

| 1874 | 137.6 | 1899 | 5.0 | bons de liquidation |

| 1874–76 | 32.0 | 1889 | 4.0 | quinzenaires, never circulated |

| 1878 | 79.3 | 1907 | 4.0 | trentenaires travaux publics 1876 |

| 1885–90 | 240.0 | 1907 | 4.0 |

Source: Ducrocq (1904, pp. 161–173).

The initial issue in 1878 took various forms: Some were sold on the stock market, some in public offices, and some to bankers, at varying prices. Further issues to finance deficits were authorized by various budget laws. They were either sold by public subscription at a set price (in 1881, 1884) or sold to the Caisse des Dépôts (in 1882, 1884). The new issues were on the existing schedule; hence, each was of a slightly shorter maturity at issue.v

The 75-year term was chosen because the issue was intended to finance the Freycinet Plan. The finance minister matched the term of the bond with the duration of the railroad concessions.

Long-term debt (15 to 34 years)

Thirty-year bonds (obligations trentenaires) were first authorized by a law of June 23, 1857, to provide subsidies for railway companies. The minister of finance was authorized to issue bonds of 500F bearing 4% interest and turn them over to the companies, which then sold them to the Caisse des Dépôts.vi The bonds were reimbursed from 1860 through 1889 by random draws. Another issue was authorized by a law of June 29, 1861, to finance the State’s own expenditures on railways and sold to the public at 440F; the new issue carried the same interest and was reimbursed on the same schedule as the previous one. The bonds were not callable, but were included in the conversion of 1863—that is, they were accepted in exchange for 3% perpetual annuities at par of revenues (a 500F bond was exchanged for a 20F annuity). Most were converted, with the remainder reimbursed on schedule.

During the Franco-Prussian War, the provisional government negotiated with J. S. Morgan & Co. a loan of 250mF in the form of 500F bonds paying 6% and reimbursed by random draws from 1873 through 1906. Morgan bought some at prices of 400F and 415F, the public bought the rest at 425F. The bonds were callable, and the option was exercised in 1875: For each bond, which had a coupon of 30F, a 3% perpetual annuity of 30F was offered in exchange for one bond (with a coupon of 30F) and a payment of 124F.vii In other words, bondholders could exchange a finite annual stream of 30F ending with a payment of 500F at date T with an infinite stream of 30F. The 124F represented the difference between the expected value of the infinite stream starting at T + 1 and 500F, discounted back from T to the present.

As of May 1875, when the operation began, the price of a perpetual annuity of 30F was 650F, an annual interest rate of 4.6%. Since 1.046−4 ∼ 124/150, bondholders expected to be reimbursed four years hence.

In 1873 the government made another attempt to pay subsidies that it owed to the railroad companies in the form of 15-year bonds (the so-called quinzenaires); their issue was authorized, but the railroad companies refused to take them at the price set by the government. The bonds remained in the Treasury’s portfolio and were reissued as 30-year bonds in 1878 (France, Ministère des finances, 1881, pp. 695, 706, covering the accounts for fiscal year 1878).

Indemnity bonds (bons de liquidation) were authorized by two laws of April 7, 1873, and July 28, 1874, for use as compensation for losses incurred during the Franco-Prussian War. The bearer bonds of 500F carried a 5% interest payable twice yearly, reimbursed by lottery draws twice a year from 1875 through 1899.

The 1877 budget (law of December 29, 1876) authorized another issue of 30-year bonds, again to finance public works. The format was similar: bearer bonds at 4% with twice-yearly coupons, reimbursed by lottery draws twice a year from 1878 through 1907. These were mostly bought by the banker Rothschild at 463.10F and the rest sold to the public at 478F (France, Ministère des finances,1880, p. 651, covering the accounts for fiscal year 1877; and France, Ministère des finances, 1893, p. 766, covering the accounts for fiscal year 1892). From 1885 to 1890 this issue was reopened to finance construction of roads and schools by local governments, for a total of 240mF (France, Ministère des finances, 1895, p. 703, covering the accounts for fiscal year 1894). The 1891 budget (law of December 26, 1890) ordered the reimbursement of the long-term bonds of 1873 and 1876 at face value. In 1893, the remaining bonds issued since 1885, all held by the Caisse des Dépôts, were exchanged for an annuity to the Caisse.

Short-term debt (one to six years)

The first experiment with short-term debt came at the start of the Franco-Prussian War, with the bons du Trésor called “two and ten,” “three and ten,” and “five and ten.” In imitation of U.S. securities, the first number was the number of years before the bonds could be redeemed, and the second number was the number of years before which the redemption had to happen. The bearer bonds had twice-yearly coupons. They were not successful and were soon accepted in exchange for other loans.

Thereafter, short-term debt was issued with a fixed redemption date. In 1875 a special budget was created for the rearmament of the country after the War of 1870. The laws simply stated that the expenses would be financed by Treasury obligations of maturity no longer than six years. The minister of finance created bearer bonds of six years or less (hence, their name sexennaires). The coupons were twice-yearly, with the rate set at issue and depending on the maturity (generally 4% or 4.5% early on). The same method was used to finance several other special budgets in 1885, as well as budget deficits from 1885 through 1890. The practice stopped in 1892, but resumed from 1898 through 1908; the bonds’ maturity at issue varied from two to six years.

Floating debt

The term floating debt (dette flottante) originally meant the part of the debt that had not been definitely established by way of legislation. In 1815, that meant the debt that was not consolidated in 1797 into perpetual annuities. Later increases to the consolidated debt always took place by way of legal authorizations (new loans or settlement of other debts). The later-term annuities and short- and long-term obligations were all created by law. The remainder of the Treasury’s liabilities constituted the floating debt, which absorbed all the day-to-day variations in the Treasury’s balance sheet.

One special element of the floating debt was Treasury notes (bons du Trésor) issued by the minister of finance at his discretion subject to a legal limit. These notes were issued at rates set every month by the minister of finance and were held by the public, so they were part of the marketable debt. The maturity varied between one and 12 months, and there was no coupon: The interest was added to the face value upon repayment.

The rest of the floating debt took the form of advances from fiscal officials (tax collectors and payers, who acted as private bankers), financial institutions (Banque de France and Caisse des Dépôts), and a variety of entities such as local governments and others. Some of these deposits were mandated by law: The local governments were supposed to leave their excess balances on deposit, earning interest at an administrative rate.

Appendix Notes

i Retrospective accounts were published for the period from April 1, 1814 (end of Napoleon’s regime). The predecessor publications, the Administration des finances de la République française (1802–08) and the Compte de l’administration des finances (1809–14), were much less complete.

ii The actual banker for the Treasury was the Banque de France.

iii The one netting I do is for the holdings of the sinking fund, as explained in note 18 of the main body text.

iv A few minor issues for the purposes of consolidation are omitted.

v The amortization schedule consisted in numbers of series to be withdrawn in each year: one per year until 1907, two per year until 1925, then rising to six per year by 1951. The total debt service for these rents was therefore backloaded.

vi Two series were issued in December 1858 and August 1860, at prices of 444.49F, 445.75F, and 447.04F.

vii The State borrowed the annuities from the Caisse des Dépôts in exchange for a 39-year annuity representing 4% interest and amortization. The interest was lowered by law to 3.5% in 1892 and 3% in 1895, thus lowering the annuity.

References

Aglan, Alya, Michel Margairaz, and Philippe Verheyde (eds.), 2006, 1816 ou la genèse de la Foi publique: La fondation de la Caisse des dépôts et consignations, Publications du Centre d’histoire économique internationale de l’Université de Genève, No. 19, Geneva, Switzerland: Droz. Caron, François, 1997, Histoire des chemins de fer en France, tome premier, 1740–1883, Paris: Fayard. Ducrocq, Théophile, 1904, Cours de droit administratif et de législation française des finances, Tome cinquième: L’État, Eugène Petit (ed.), 7th ed., Paris: A. Fontemoing. Flandreau, Marc, and Frédéric Zumer, 2009, The Making of Global Finance 1880–1913, OECD Development Centre, monograph, October 30. Crossref France, Ministère des finances, 1826–1914, Compte général de l’administration des finances, rendu pour l'année 1825 [–1913] par le ministre secrétaire d'État des finances, Paris: Imprimerie royale. France, Ministère des finances, 1818–25, Compte rendu par le ministre secrétaire d’État des finances, pour l'année 1817 [–24] . Paris: Imprimerie royale. France, Ministère des travaux publics, 1914, Statistique des chemins de fer français au 31 décembre 1912, 2 vols., Melun, France: Imprimerie administrative. France, Ministère du travail, 1921, Annuaire statistique, Vol. 36, Paris: Imprimerie nationale.Geiger, Reed, 1984, “Planning the French canals: The ‘Becquey Plan’ of 1820–1822,” Journal of Economic History, Vol. 44, No. 2, pp. 329–339. Crossref

Le Trocquer, Yves, and Paul Doumer, 1921, Compagnies des chemins de fer liées vis-à-vis de l’Etat par des conventions financières: Comptes des dépenses d’établissement au 31 décembre 1912, Paris: Imprimerie nationale.

Nicolas, Charles, 1882, Les budgets de la France depuis le commencement du XIXe siècle, Paris: A. Lahure.

Picard, Alfred, 1918, Les chemins de fer: Aperçu historique, résultats généraux de l’ouverture des chemins de fer, concurrence des voies ferrées entre elles et avec la navigation, Paris: H. Dunod et E. Pinat.

Picard, Alfred, 1884–85, Les chemins de fer français, 6 vols., Paris: J. Rothschild.

Sargent, Thomas J., and François R. Velde, 1995, “Macroeconomic features of the French Revolution,” Journal of Political Economy, Vol. 103, No. 3, June, pp. 474–518. Crossref

Say, M. Léon, Louis Foyot, and A. Lanjalley, 1894, Dictionnaire des finances, 2 vols., Paris: Berger-Levrault et Cie. Toutain, Jean-Claude, 1987, Le produit intérieur brut de la France de 1789 à 1982, Grenoble, France: Presses universitaires de Grenoble.Velde, François R., 2022, “La dette publique en France au XIXe siècle,” Revue d'économie financière, Vol. 146, No. 2, April, pp. 85–100. Crossref