Market Resiliency: Evidence from Money Market Mutual Fund Reform

Introduction

Good morning. I would like to add my warm welcome to everyone who is here today to that of President Evans and Secretary-General Tang. We are proud of the collaboration between the People’s Bank of China and the Federal Reserve Bank of Chicago that has resulted in today’s symposium and what I hope will be a lively and informative discussion.

Before I get started, I would like to emphasize that my remarks represent my own views and not necessarily those of the Federal Reserve Bank of Chicago or the Federal Reserve System.1

Today I’m going to talk about change and resilience. Financial markets are continuously changing and adapting—to new opportunities (and the demise of old ones), to new information, and to new technologies. Developments in financial markets are intricately linked to developments in the real economy. Financial markets provide important signals to firms and to individuals that guide change in the real economy. For example, when the price of wheat increases, farmers plant more. And when the cost of financing increases, firms invest less. When financial markets are resilient, they can adapt quickly to change, and this makes the real economy more productive because funds are allocated more efficiently.

The financial crisis and its aftermath have brought considerable change to financial markets and institutions. There have been a host of new regulations, but there has also been organic change driven by a renewed appreciation of risk and interconnectedness and the many ways things can go wrong.

In my talk today, I am going to concentrate on one specific change to financial markets and what we can learn from this episode about market adaptability and resilience more generally. I will focus on post-crisis reform to the $3 trillion money market mutual fund industry in the United States. In particular, I will discuss the new requirements that went into effect in October 2016, which resulted in a shift of about a trillion dollars from prime money market mutual funds (which invest in a wider variety of assets) to government funds over the course of less than a year. You can see the magnitude of this change on slide 1.

Slide 1

First, I will provide some background on the money market mutual fund industry and on the events that led to the October 2016 reform. Then I will describe the changes that market observers expected from the reform. I’ll also look at futures prices as another measure of what the market anticipated. Next I’ll compare what actually happened with what was expected to happen and draw some conclusions about market adaptability and resiliency.

To cut to the punch line, I find that markets are both more and less adaptable than they think they are. The market expected modest changes in the relevant interest rate spreads, but we actually saw large changes. Once spreads widened, the market expected them to stay this way, but spreads instead returned to more typical levels quite quickly.

Background and the reform

Let’s start with some background. The U.S. money market mutual fund industry is large and important. It links financial institutions, hedge funds, broker-dealers, and institutional investors, including derivatives clearing organizations and futures commission merchants. At the end of 2014 and prior to the reform, the money market industry had about $3 trillion in assets under management. Prime money market mutual funds were key players in bank funding markets, holding 40 percent of outstanding commercial paper (CP), 60 percent of outstanding certificates of deposit, and significant shares of both nontraditional and government repurchase agreements, or repos. Prime money market mutual funds and government funds are critical players in money markets; their purchases, repurchases, and sales activities influence prices of various short-term instruments, which are in turn important indicators of financial conditions. And, more fundamentally, money market mutual funds transform the savings of millions of households into investments in firms and in communities.

To understand the reform implemented in October 2016, as with many post-crisis regulations, we need to go back in time to September 15, 2008, when Lehman Brothers filed for bankruptcy. When Lehman failed, its commercial paper became worthless, leading to heavy losses for the Reserve Primary Fund—a large money market mutual fund that had invested heavily in Lehman’s CP. The losses were so large that the Reserve Primary Fund “broke the buck,” meaning the net asset value of its shares fell below one dollar.

This brought a sharp end to the belief that money market funds were safe substitutes for insured bank accounts that just happened to earn a higher return. Panic ensued. The Reserve Fund blocked withdrawals. And investors, especially institutions, rushed to pull their money out of other money market funds: $15 billion dollars was withdrawn on September 15, and another $78 billion on September 16. Three days later, in an effort to contain the panic and its harmful effects on other markets, the government stepped in to backstop the money market industry and continued to do so for a year.

Making money market mutual funds less vulnerable to runs was an important priority for post-crisis regulatory reform. However, as these things do, it took a while to deliver. On July 23, 2014, the U.S. Securities and Exchange Commission voted to amend rule 2a7, which governs money market mutual funds under the Investment Company Act. According to the new requirements, prime institutional funds are no longer allowed to guarantee a share value of one dollar. In addition, they must put in place measures that could slow down withdrawals—through some combination of liquidity fees and gates on redemptions. Funds aimed at retail investors are still allowed to guarantee a share value of one dollar. However, if liquid assets fall below certain regulatory minimums, these funds have an option to impose liquidity fees or suspend redemptions—and if liquid assets fall even further, they are required to do so. Money market funds that invest solely in government securities are exempt from these new requirements.

The money market mutual fund industry had to comply with the new regulations by October 16, 2016—eight years, one month, and one day after Lehman’s failure. The money market industry, the borrowers whose paper the funds bought, and the institutional and retail investors who had invested $3 trillion in money market funds had a little over two years to adapt.

Expectations and reality

What did market observers expect the impact of the reform to be? The potential impact of money market reform generated a lot of market chatter beginning in early 2015. Market observers anticipated significant changes in the industry, including a potentially large shift from prime institutional funds, which then had about $1 trillion in assets, to government funds. This shift would lead to increased demand for government securities and repo backed by government securities. This increased demand was expected to put downward pressure on interest rates on government securities. With less demand from prime funds, repo rates on nontraditional collateral were expected to increase, as were the costs of borrowing through commercial paper and certificates of deposit. These anticipated changes would potentially make it more difficult for banks to fund themselves.

The new regulations led to changes for derivatives clearing organizations and their members as well. They were prohibited from investing customer funds in prime institutional money market funds and from using prime institutional money market shares as collateral. These follow-on changes in regulation likely contributed to the magnitude of the shift from prime to government funds.

Other factors influenced speculation about the impact of money market mutual fund reform as well. The likely increase in the demand for safe, liquid assets due to the reform would be happening at a time when these assets were in relatively short supply. Short-term government securities were down $600 billion from their 2009 peak, and banks and dealers were shrinking their repo books in response to other regulatory changes.

Initially, many observers expected the shift from prime to government funds to be primarily driven by institutional prime fund investors switching to government funds. But in early 2015, it became clearer that some prime retail customers would also shift to government funds. Apparently, retail customers were more averse to liquidity fees and gates on redemptions than had been anticipated. This meant that the magnitude of the shift from prime to government funds would be larger than originally expected. There was considerable uncertainty about the magnitude of the shift: In the middle of 2016, just a few months before the October implementation date, one survey estimated that $400 billion would shift from prime to government funds. Ultimately, about a trillion dollars shifted from prime to government funds. This meant that banks that had routinely sold CP to prime funds had to make some difficult choices: They could try to find new buyers for their paper, they could try to find new sources of funding, or they could shrink.

So, there was quite a lot of change for the market to absorb.

In addition to market commentary, we can look at prices to get a sense of how the market expected the reform to play out. Market participants generally expected bank funding costs to increase and returns on short-term government debt to decrease as investors shifted away from prime funds that bought commercial paper from banks. This increase in bank funding costs was reflected in the LIBOR–OIS spread.2

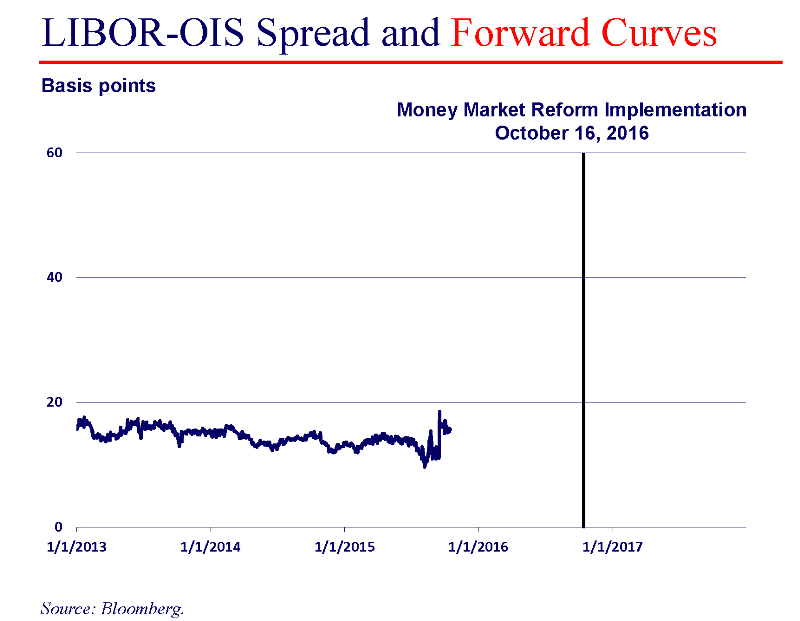

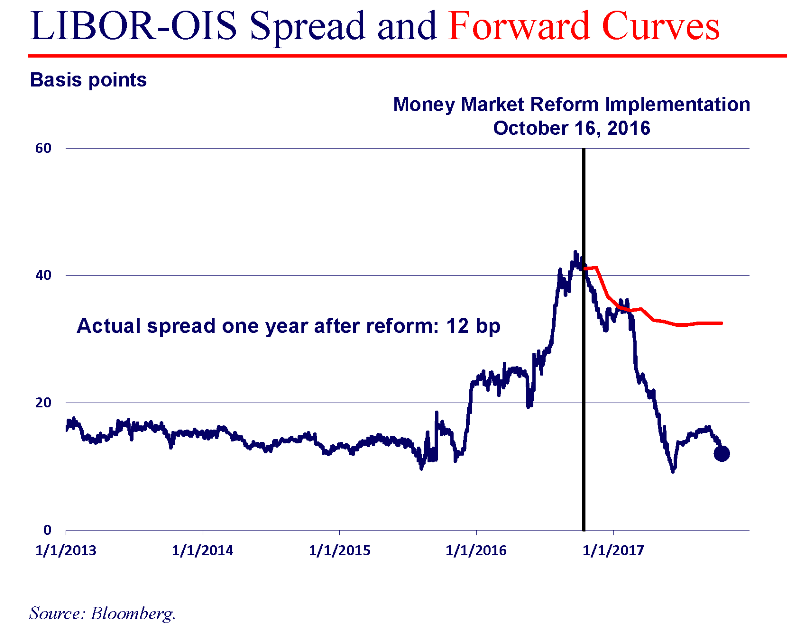

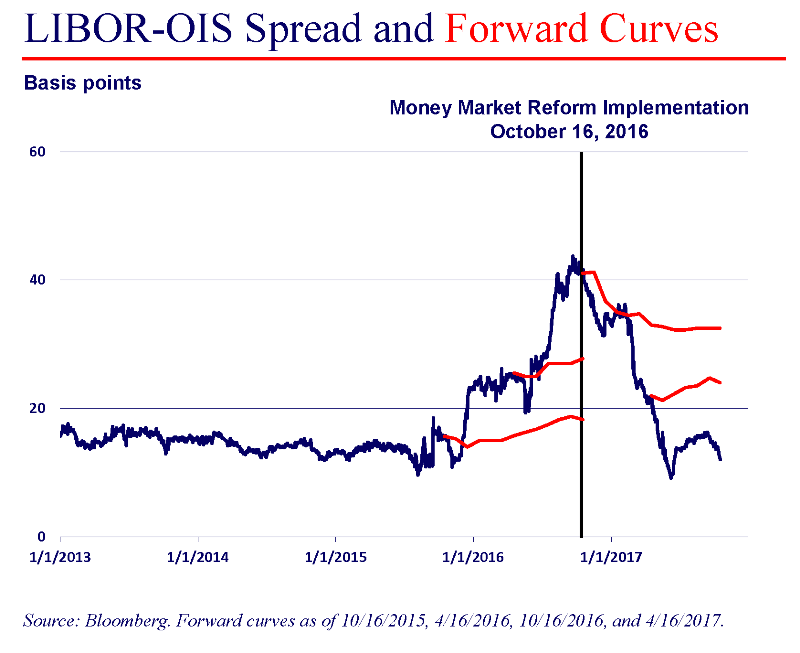

Let’s look at slide 2. The blue line on the graph is the LIBOR–OIS spread on any given day—what actually happened. The vertical line on the graph is October 16, 2016, the date that money market mutual funds had to comply with the new regulations.

Slide 2

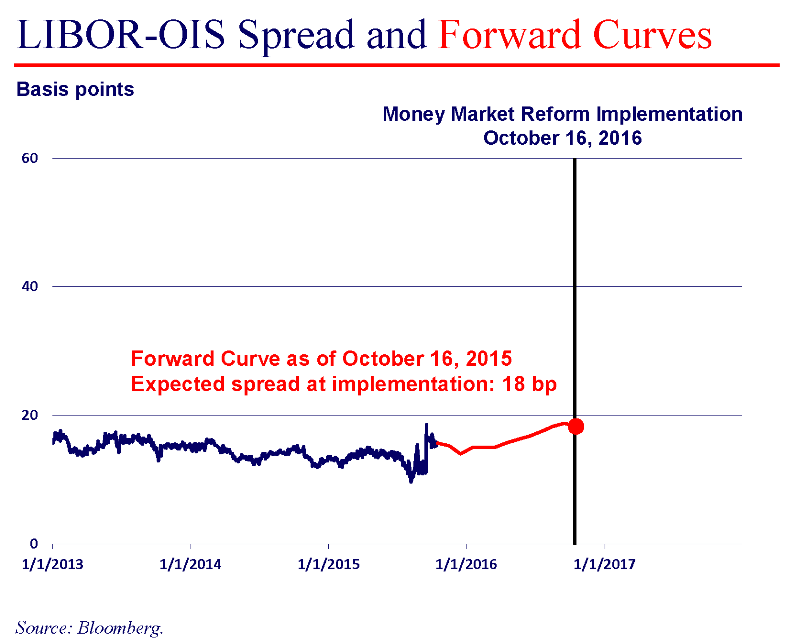

Turning to slide 3, note that each point on the red line corresponds to the LIBOR–OIS forward rate—what the market predicted the LIBOR–OIS spread would be. This forecast is as of October 16, 2015, the day the red line begins. So, for example, the last point on the red line shows that on October 16, 2015, the market expected the LIBOR–OIS spread would be 18 basis points a year later—on October 16, 2016, when the reforms went into effect.

Slide 3

Of course, these forward rates take into account everything else that might influence the LIBOR–OIS spread over the next year and not just money market reform. But by looking at the spread, we are removing many other factors that affect interest rates in general. Changes in monetary policy, for example, would be expected to affect both OIS and LIBOR, but not the spread.

So we can treat the red line as a proxy for the market’s estimate of the price impact of the money market mutual fund reform. And the blue line is the realized price impact—what actually happened.

Slide 4

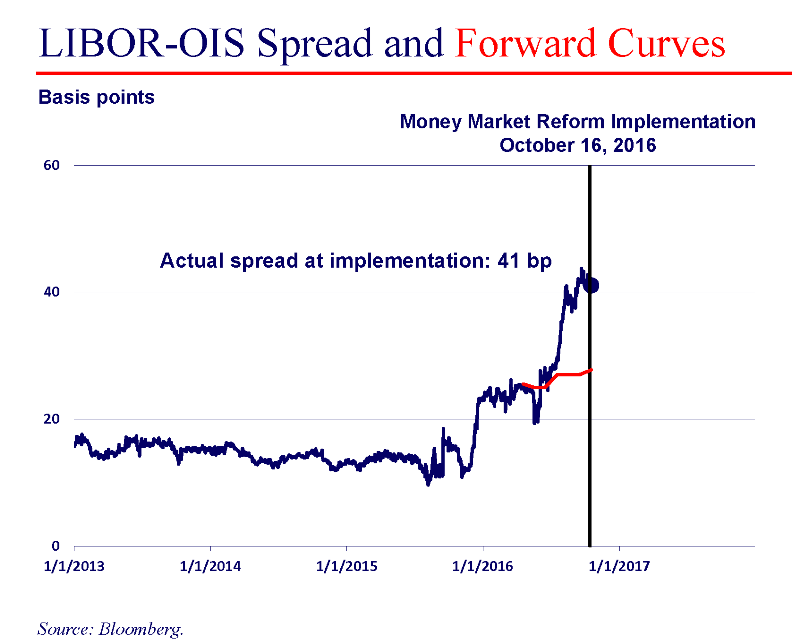

So what does the picture tell us? Let’s fast forward to slide 4 and April 16, 2016—six months before the reform implementation date. On that date, the market anticipated that the LIBOR–OIS spread would be 28 basis points on October 16. Instead the spread turned out to be 41 basis points on October 16, as you can see from the blue line on slide 5.

Slide 5

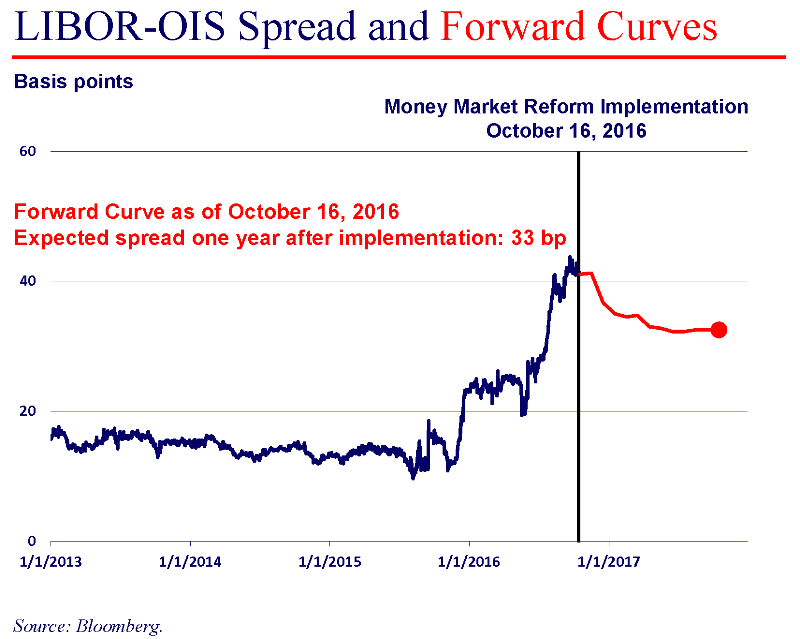

What did the market think would happen after the reform date? We can again look at forward rates. The red line on slide 6 tells us that the market anticipated the LIBOR–OIS spread would drop a little bit, but generally remain elevated, reaching 33 basis points a year after the reform date. What actually happened? In fact, the spread declined sharply following the reform date, as you can see from the blue line on slide 7. Six months after reform implementation, the spread actually fell to 21 basis points; and a year after the implementation, the spread reached 12 basis points, or about the same level that had prevailed before the reform.

Slide 6

Slide 7

So what adjustments happened to allow the LIBOR–OIS spread to come down? How did banks replace the trillion dollars in funding they had been getting from prime money market mutual funds? How did the market cope with new demand for government assets? An important part of the adjustment came through the Federal Home Loan Banks. These are U.S. government-sponsored entities that make collateralized loans to banks, called advances. The Federal Home Loan Banks fund themselves by issuing debt securities. And because they are government-sponsored entities, government money market funds can buy these securities.

So the Federal Home Loan Banks were in a position to solve two of the key challenges created by money market mutual fund reform: higher demand for government securities and banks’ need for funding to replace CP. Banks were able to fund themselves with Federal Home Loan Bank advances, and government money market funds were able to expand by investing in Federal Home Loan Bank securities. We often think of government-sponsored entities as being slow to change and not very attuned to market conditions, but in this case the Federal Home Loan Banks were pretty nimble. They increased advances to banks and financed this increase by issuing securities with duration characteristics that made them attractive to government money market mutual funds.

Slide 8 puts the whole picture together and suggests that prior to the reform implementation date, the market underestimated how hard it would be to adapt to money market mutual fund reform. The market was less resilient than it thought it would be, and change turned out to be harder than anticipated. One intriguing possibility is that the market underestimates the impact of changes, even changes that it knows are coming, in part because institutions and markets rely on price signals to fully adapt and these signals aren’t available until change actually occurs.

Slide 8

But after the reform requirements were in place, the market appears to have overestimated the difficulty of adjusting to them. The market turned out to adjust more quickly than futures prices indicated.

This makes me think about going to the doctor when I know I am going to get a shot. I try to convince myself that it won’t be too bad—that the shot won’t hurt too much and that my expectations should look like the red line prior to the implementation date. Then I get to the doctor’s office, the needle goes into my arm, and it hurts like crazy. Now I am worried that the pain will never stop. My expectations are a little like the red line after the reform implementation date. Then I surprise myself when on the way out of the office to the car, I realize the pain is basically gone.

Implications

What does all of this mean for the resiliency of financial markets more generally? First, even though the money market fund industry is fairly simple and well understood and markets and institutions had a lot of time to prepare for reform, they were still surprised. They were surprised by the magnitude of the shift from prime to government funds, by the behavior of the relevant interest rate spreads, and by the role of the Federal Home Loan Banks. This outcome suggests that changes involving more complicated institutions and markets may generate even bigger surprises. And here I am thinking, in particular, about changes to derivatives markets.

We can also draw on the lessons from this episode when thinking about other changes that are coming to financial markets—for instance, balance sheet normalization in the U.S., the end of asset purchases in Europe, Brexit (once the details are worked out), and the regular exchange of margin for uncleared derivatives. Based on the response to money market mutual fund reform, we might expect markets to anticipate some of the effects of the change, but to still be considerably surprised along the way and then to adjust quickly to the new reality once it’s in place.

Change is both harder and easier than we think, and markets are both more fragile and more resilient than they think.

Notes

1 I am grateful to Stefania D’Amico, David Kelly, and Sam Schulhofer-Wohl for their help in preparing these remarks and to Nahiomy Alvarez, Cindy Ivanac-Lillig, Rebecca Lewis, and Robert Steigerwald for helpful feedback.

2 LIBOR stands for the London interbank offered rate—a benchmark rate that many leading banks charge each other for short-term loans; it is considered a gauge of credit market conditions. OIS stands for the overnight index swap rate—which is based on contracts in which investors swap fixed- and floating-rate cash flows; it is viewed as a proxy for where a given country's central bank rate (in the U.S., the federal funds rate) is headed. A widening between these two rates can indicate rising financial stress.