Countering Downward Bias in Inflation

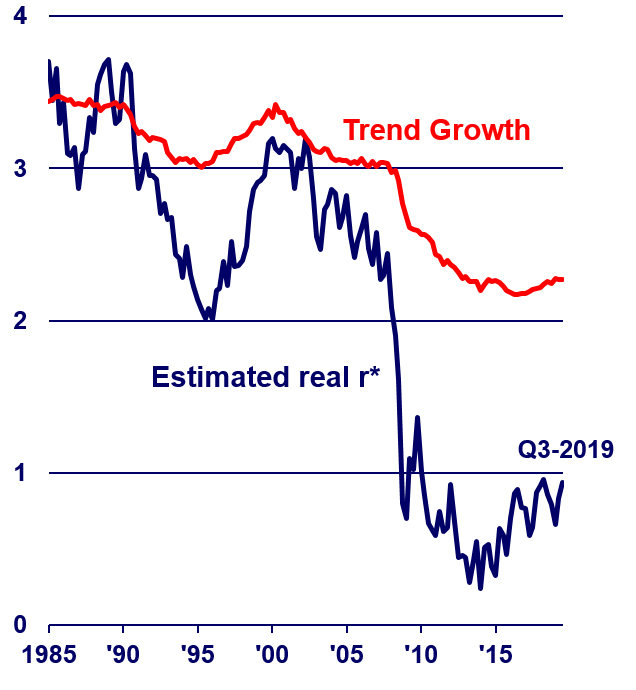

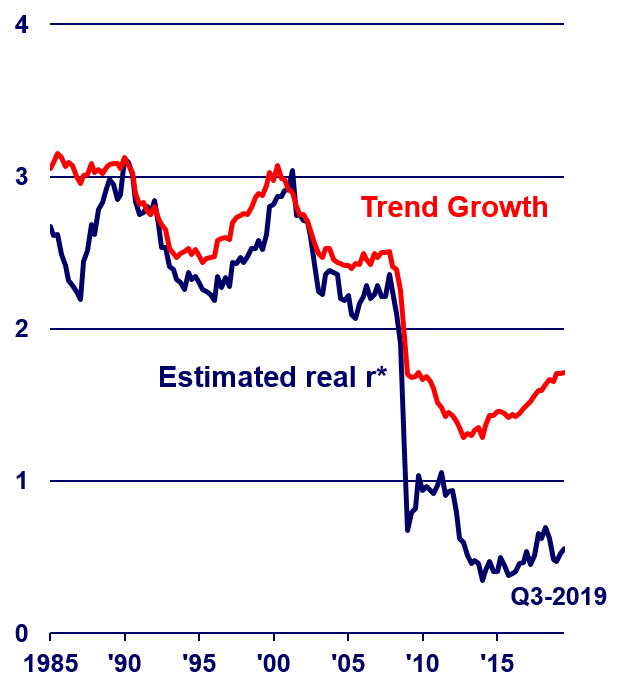

Low Trend Growth and Low Neutral Interest Rates (r*)

US (percent)

Advanced Economies (percent)

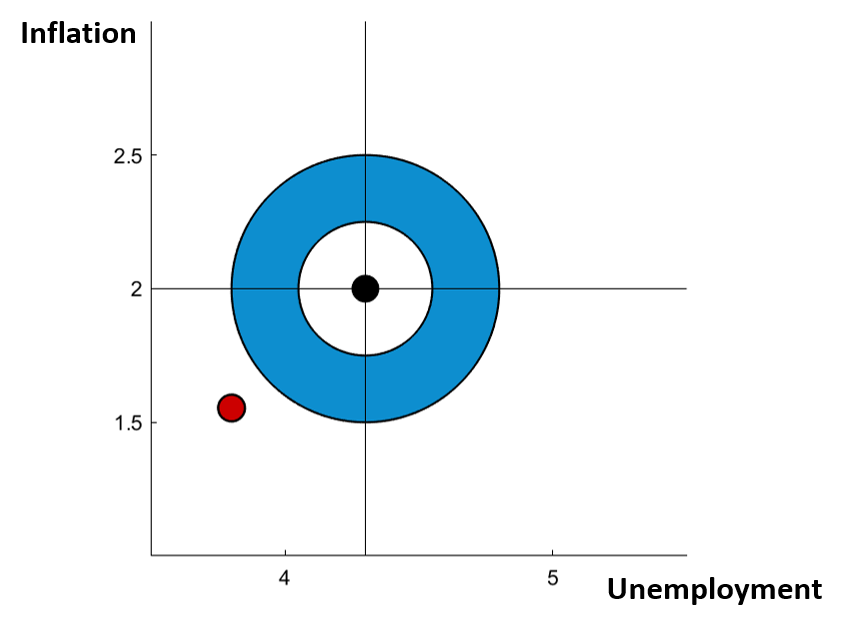

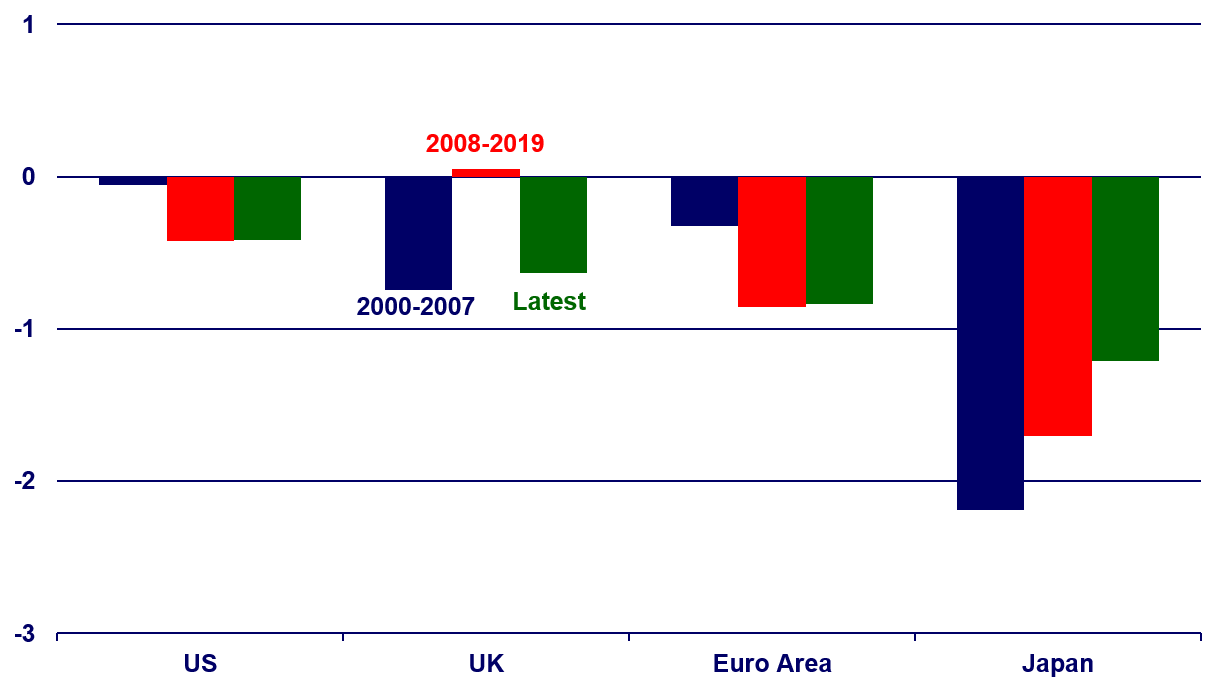

Undershooting Inflation Goals

Deviation from Central Bank Inflation Target

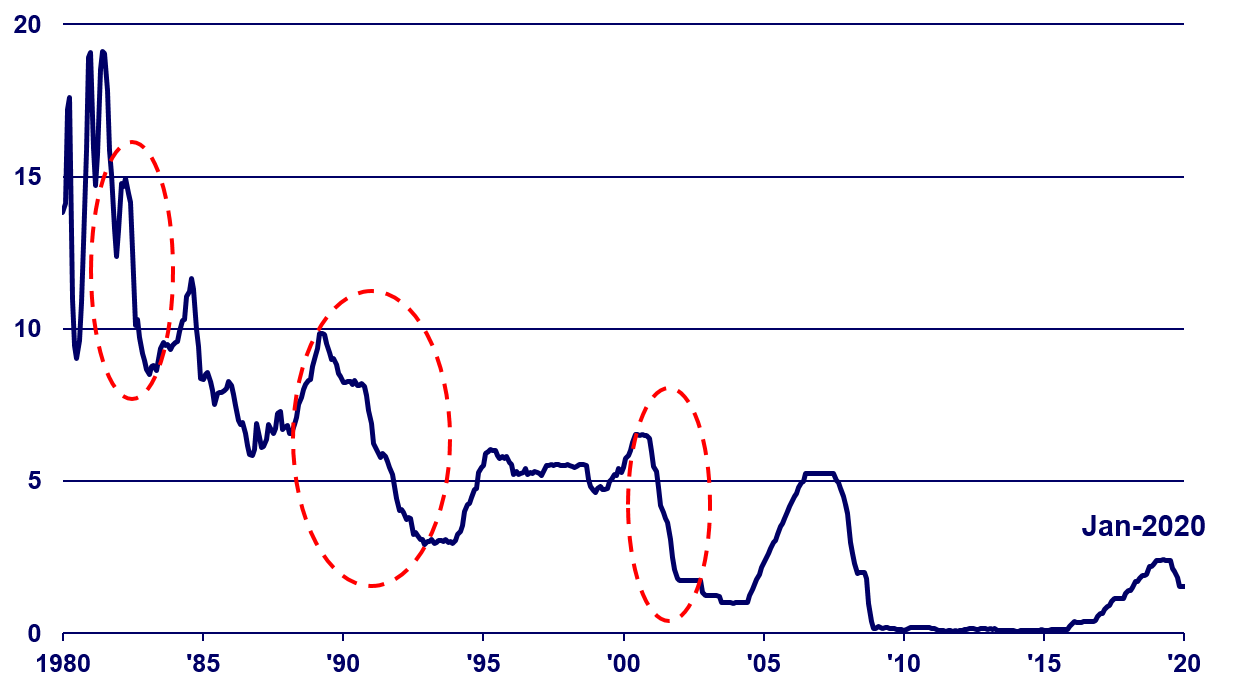

Conventional Monetary Policy Easing During Past Recessions

Federal Funds Rate (percent)

| Average easing during recessions | 500 bps |

| Current fed funds rate range | 150-175 bps |

| Long-run neutral rate | 250 bps |

Fed Funds Rate and a Traditional Benchmark

Federal Funds Target Rate (percent)

Taylor Rule (1999):

r(t) = r*(t) + π(t) + 0.5[ π(t) – π* ] + 2[ uLR(t) – u(t) ]

Source: Board of Governors of the Federal Reserve System from Haver Analytics

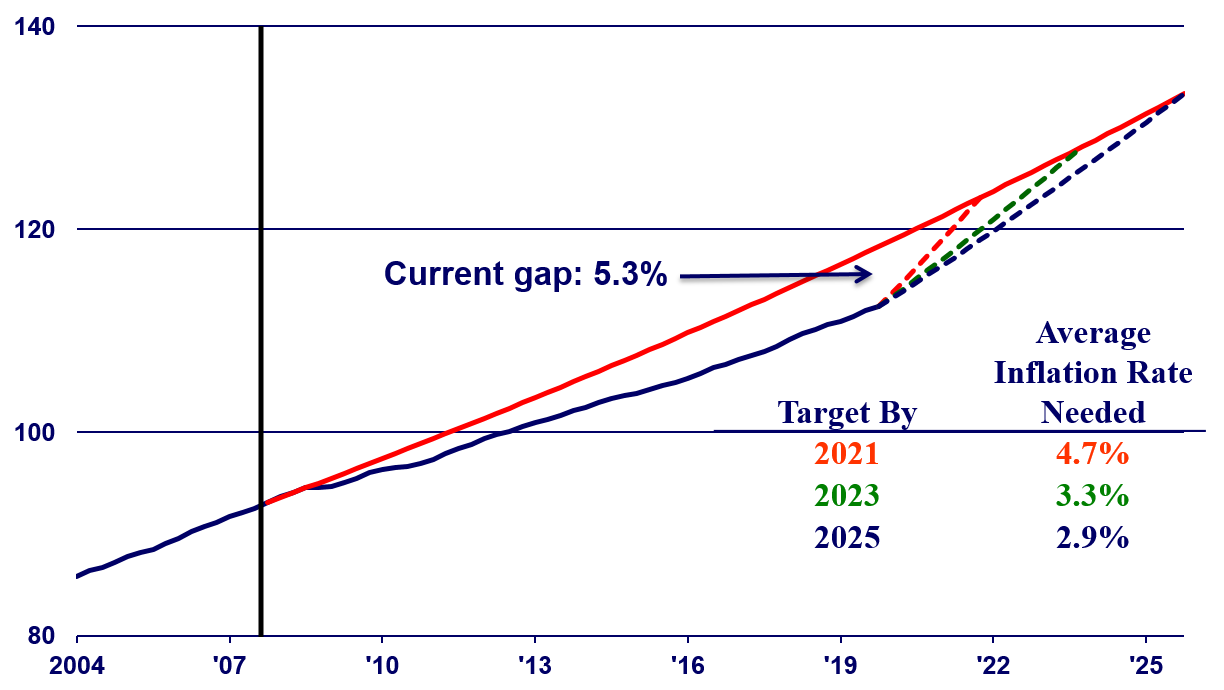

Example: State-Contingent Price Level Targeting

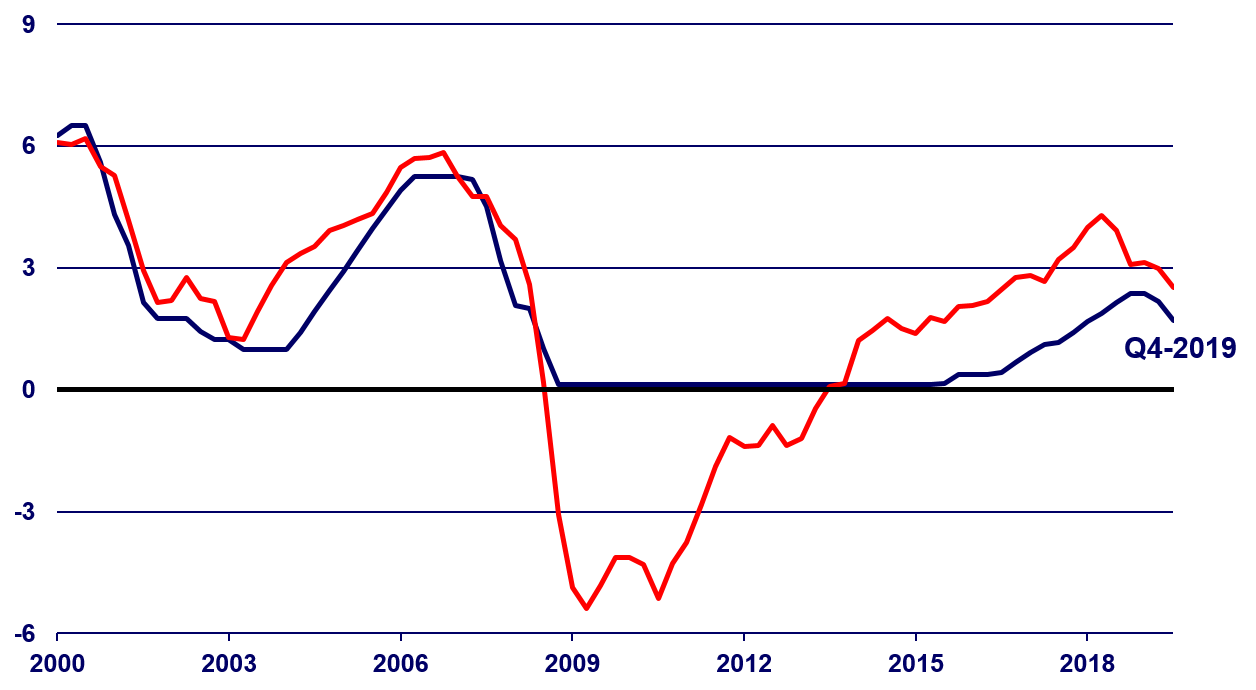

Core PCE Price Index