Mid-year jobs report

Economists and policymakers often pay close attention to payroll job numbers because they are among the most current and wide-ranging economic indicators available for states and regions. However, payroll job numbers should be viewed with caution as they are subject to revision; that is, an annual revision is undertaken during early March for the data of the previous five years.

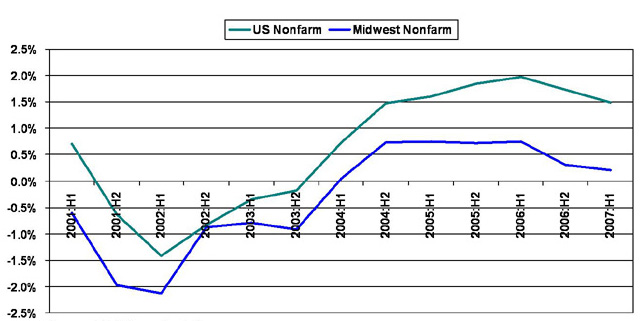

The Midwest—comprising Illinois, Indiana, Iowa, Michigan, Minnesota, Ohio, and Wisconsin—saw moderate year-over-year employment growth in the first half of 2007. The Midwest had 0.2% nonfarm employment growth, while the U.S. had a 1.5% gain (see the figure below). Each state in the Midwest posted growth in jobs, except for Michigan and Ohio.

Figure 1. Payroll employment (year-over-year percent change)

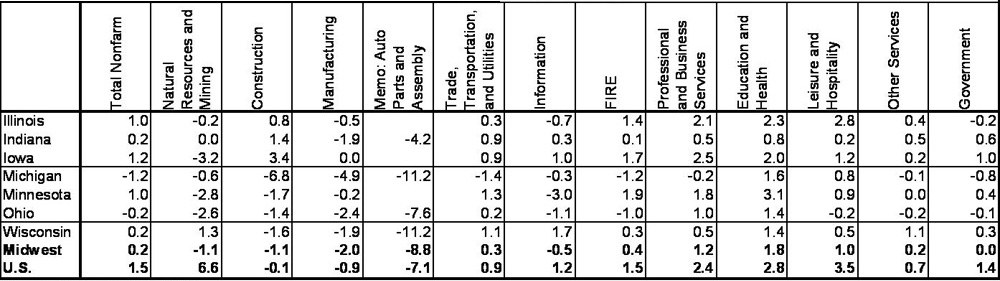

Most major industry sectors contributed to the Midwest’s sluggish employment growth (see the table below). The region’s manufacturing employment decreased, in large part due to the auto and housing industries’ troubles. Midwest employment expanded in the professional, education and health, and leisure and hospitality sectors, though at a slower pace than in the nation.

Table 1. Payroll job growth (2007 H1 / 2006 H1 percent change)

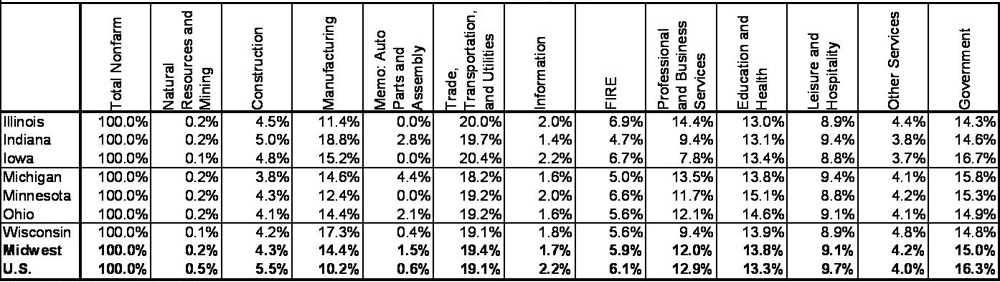

Rising by at least 1 percent, the professional, education and health, and leisure and hospitality industries led employment growth in the region. Because these sectors make up a good portion of the Midwest’s industry mix (see the table below), they offset declines or tepid growth in other industries.

Table 2. Payroll jobs — industry mix

The Finance Industry

The finance industry also helped sustain overall job growth during the first half of this year. Going forward, this sector’s performance could falter as financial firms react to changing credit conditions. In fact, some lenders have reportedly laid off staff in Chicago, Detroit, and Carmel, IN.

The Auto Industry

Indiana, Michigan, Ohio, and Wisconsin all reported declines in manufacturing; those states were heavily weighed down by the declining production activity in the automotive industry. According to the Chicago Fed Midwest Manufacturing Index, auto production in the Seventh District, which comprises all of Iowa and most of Illinois, Indiana, Michigan, and Wisconsin, declined 2% from the first half of 2006. Light vehicle sales and production in the U.S. decreased during the first half of the year (compared with last year) in part because of the ongoing struggles of the Detroit Three automakers (Chrysler LLC, Ford Motor Co., and General Motors Corp.). Payroll auto employment in Michigan reported an 11% drop year-over-year for the first half of 2007. Wisconsin also reported an 11% drop; however, the auto industry makes up a very small share of Wisconsin’s industry mix. Indiana’s auto employment reported a drop of 4%, and Ohio’s decreased by 7%. Automotive employment declines are not confined to production workers. Last month (on September 6), Volkswagen announced its plan to move its headquarters to Herndon, VA, which would shift 800 jobs away from the Detroit area.

Having discussed some of the major industries across the region, I now turn to the employment performance and outlook for the individual states.

Illinois

With strong growth in the professional, financial, education and health, and leisure and hospitality industries, Illinois reported about a 1 percent rise in nonfarm employment for the first half of this year compared with last year. These industries’ growth in jobs outweighed small contractions in manufacturing and government employment.

Indiana

Aside from the drop in manufacturing employment (and essentially no change in the number of jobs in the natural resources and mining sector), Indiana experienced growth in all other sectors. Based on the employment growth in most of its industries, Indiana reported a small increase in total nonfarm employment. Interestingly, the sector with the largest year-over-year growth was construction, even though housing starts and permits both decreased in the first half of the year. Recently, the relationship between housing construction activity and construction employment has remained murky in Indiana and elsewhere. Construction employment has held up better than some might have anticipated.

Iowa

Iowa reported above a 1% growth in total employment partly due to its strong professional and financial industries. For the first half of the year, Iowa also experienced greater than 1% growth in its construction, information, education and health, and leisure and hospitality industries. Similar to Indiana, Iowa recorded a significant increase in construction jobs, even as home building slowed.

Michigan

Michigan reported a drop of 1% in nonfarm employment, which is in line with the rate of decline it has experienced since the beginning of 2006. Job losses were widespread across major industry sectors, with the exception of solid growth in the education and health sector as well as the leisure and hospitality sector.

Minnesota

Minnesota reported a 1% growth in total employment largely because of its expansions in the professional and financial industries. While Minnesota saw some declines greater than 1% in natural resources and mining as well as in construction, these industries form only a small portion of the state’s industry mix. These declines were more than offset by the strength in the professional and financial sectors, as well as by the reported 3% gain in education and health and the smaller 1% gain in the trade, transportation, and utilities sector.

Ohio

Ohio’s overall nonfarm employment experienced a dip. However, this decline was partly offset by the strong growth in its professional as well as its education and health industry. The trade, transportation, and utilities sector also posted a small gain.

Wisconsin

Overall, Wisconsin reported a small increase in total nonfarm employment. Other than a decrease in manufacturing and construction, Wisconsin’s other industries expanded in the first half of the year. Manufacturing excluding the auto industry reported a decline of 1.7%.

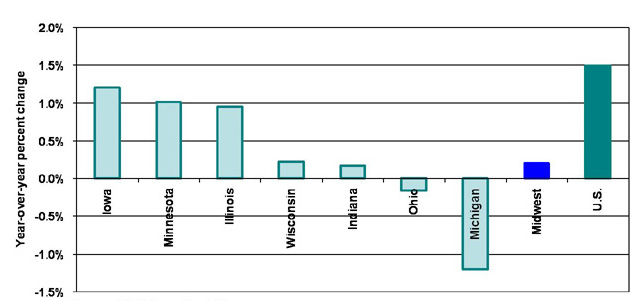

Figure 2. Payroll employment: 2006 H1 to 2007 H1

As measured by payroll employment growth, the Midwest economy continues to expand more slowly than the nation. A general pattern of increasing weakness is evident in contrasting the westward states of Iowa, Minnesota, Illinois, and Wisconsin with Michigan, Ohio, and Indiana in the east (see the figure above). Automotive restructuring there, along with flat nationwide sales in light vehicles, continues to account for a lagging pace of payroll employment.