Seventh District Housing Market Update

For several years running, the national pace of investment in housing greatly exceeded historic norms. Accordingly, housing market observers speculated that strong rates of home building and price appreciation would falloff markedly at some point in the near future. Nationally, real residential investment growth averaged 9 percent from 2003-2005; average home prices rose by 6.8 percent in 2003, 10.7 percent in 2004, and 13.1 percent in 2005.

During the first half of last year, the pace of home construction and home price appreciation finally slowed. Since then, home building activity and sales have declined sharply and, by some measures, changes in home prices are now running in negative territory. Since the fourth quarter of 2005, U.S. residential investment has been declining, averaging over 11 percent on an annualized basis. The growth of the OFHEO measure of national average home prices has slowed to 5.9 percent year-over-year for the last quarter of 2006 (new data will be released on May 31).

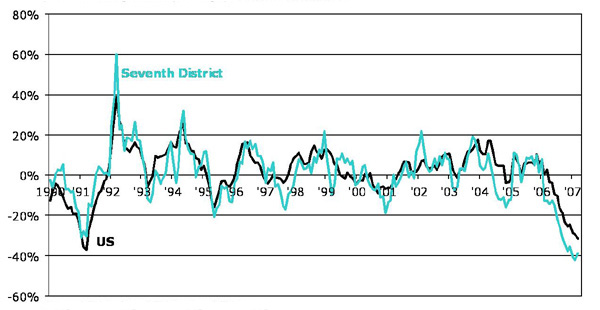

During the current decade, home prices appreciated in the Midwest as well, though less so than in the nation and much less so than several southern and coastal markets such as San Diego, Las Vegas, and many parts of Florida. For this reason, during the years of strong price appreciation, some observers believed that the Midwest would be spared the eventual price and building falloffs that would unfold in other regions. So far, this does not seem to be the case. Most major residential real estate indicators currently show the Midwest region with comparable or weaker fundamentals than the national average. The chart below illustrates the pace of new home construction starts in the Seventh District states versus the U.S. Measured on a year-over-year basis, home starts in the Midwest have been running below the nation since early 2006.

1. Housing starts — percent changed from a year ago, 3-month smoothed

For the most part, the weaker Midwest economy lies behind its weaker housing markets versus the national average. The current slowing of the U.S. economy has been accompanied by a marked slowing in manufacturing which has, in turn, softened the housing market in many local Midwest communities. In addition, ongoing structural upheaval in automotive-oriented communities is reflected in several housing market indicators including home purchases, home prices, and in foreclosures of existing properties.

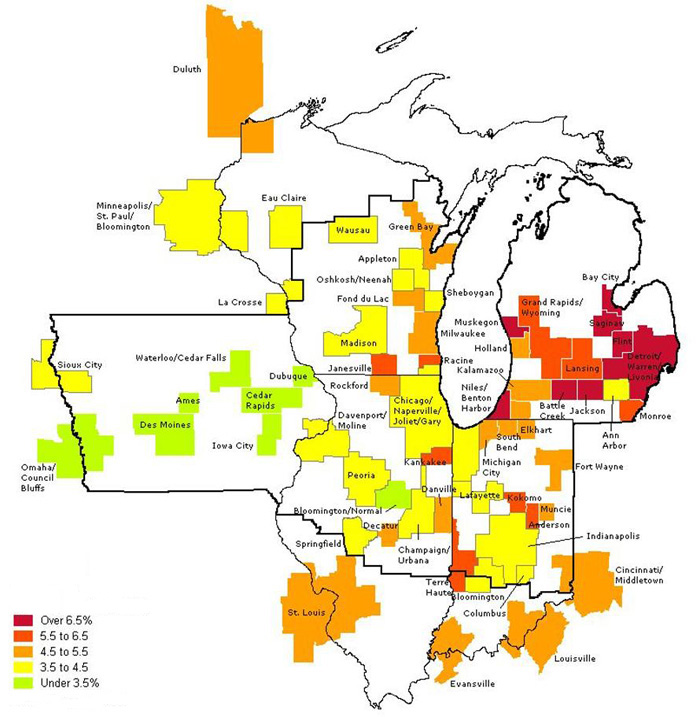

Residential real estate market conditions are highly local. The maps below juxtapose home price appreciation and unemployment rates in Seventh District metropolitan areas. Looking at the top map, unemployment rates in many Michigan communities are notably higher than the general pattern in the other Seventh District metropolitan areas. Retrenchment in domestic automotive assembly operations and suppliers in Michigan has resulted in significant work force upheaval. Automotive-oriented communities in other states of the Seventh District—such as Kokomo, Indiana—have had similar experiences. After Michigan, Indiana is the second most automotive intensive state in the Seventh District.

2. March 2007 unemployment rates (SA)

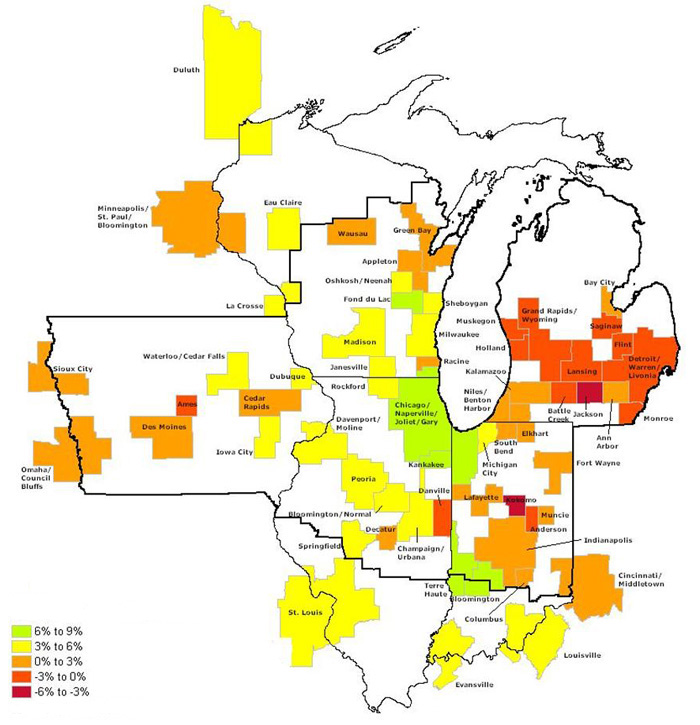

3. 2006 Q4 home price appreciation (year-over-year percentage)

The second map (above) displays year-over-year house price appreciation for the same metropolitan areas. To some degree, areas with a slack labor market are experiencing less home price appreciation. This is especially evident in Michigan and Northwest Indiana where the domestic automotive industry troubles are centered.

The linkage in these states between the local economy and the housing market is consistent with available information on home loans. The pace of loan delinquencies and mortgage foreclosures in both of these states are now running higher than both the nation and other states of the Seventh District.

Home price appreciation is stronger in Chicago and in many other metropolitan areas in Illinois and Wisconsin. In the Chicago area, job growth in business services, travel-tourism, and financial services industries have continued to expand. In other metropolitan areas to the west of Indiana and Michigan, manufacturing tends to be concentrated in more buoyant product lines, such as construction and farm machinery or food processing. As a result, home prices are generally holding up better in those areas.

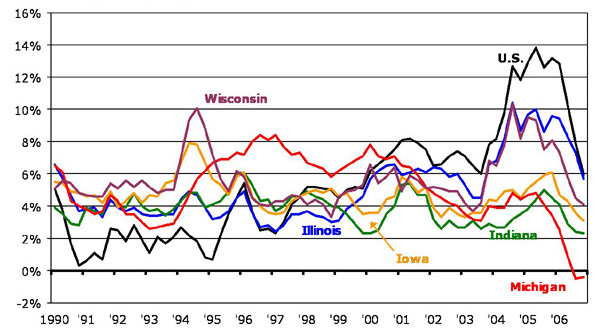

Labor market conditions fare well in many Iowa metropolitan areas. Yet, average home price appreciation there is generally tepid. To some degree, home price appreciation has been very steady in Iowa over many years and the current pace of appreciation does not differ markedly from the norm of the past 15 years (see below).

4. House price index (Office of Federal Housing Enterprise Oversight) — percent change from a year ago

Nationally, residential real estate activity continues to adjust downward to align with its rapid expansion of recent years. In particular regions and communities, the extent of adjustment varies with both the stock of existing housing and with local trends in economic growth which drive the demand for housing. Generally, new construction activity and price appreciation have softened in the Seventh District but local conditions can be seen to vary with local economic indicators.