How Do High Gas Prices Impact Detroit Vehicle Producers?

The Detroit automakers (Chrysler, Ford, and GM) appear to be making headway in their market shares during this era of high and volatile fuel prices. If so, this represents something of a turnabout.

When the price of gasoline rises quickly, Detroit usually tends to struggle in the marketplace. It is not surprising that increases in the price of oil can lower the demand for automobiles. But the Detroit automakers feel the pinch more than their foreign-headquartered competitors. Those companies produce a more fuel-efficient mix of vehicles, not least because their home markets face much higher taxes for gasoline and, therefore, they need to focus on fuel efficiency all the time, not just when gas prices go up.

Let’s take a closer look at the two most recent episodes when the price of gasoline in the U.S. rose quickly and to similar levels. Between October 2007 and July 2008, the price of gasoline rose by 45%, topping out at $4.06 per gallon in the summer of 2008 (see figure 1). Just over two years later, after giving back all of its increase and then some during the second half of 2008, the price of gas rose in a similar fashion from September 2010 to May 2011, when it peaked at $3.91 per gallon. (Figure 1 also includes a third episode of rising gasoline prices. It is shorter in duration than the other two, ending in April 2012 with gasoline topping out around $3.90.)

Figure 1. U.S. retail gasoline price: regular grade

Source: Energey Information Administration / Haver Analytics.

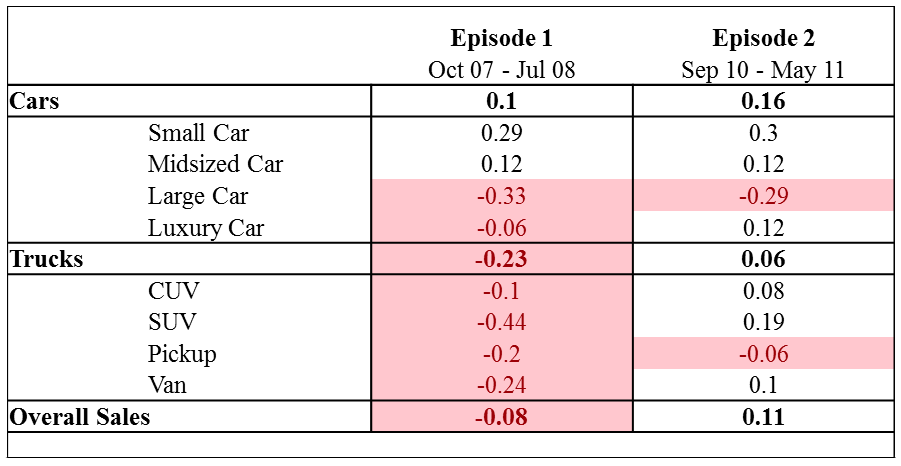

Note that these two episodes took place at different points of the business cycle. During the first half of 2008, the U.S. economy was in a deep recession: GDP was contracting, and light vehicle sales were falling fast. The second period takes place after the recession ended. At that time, vehicle sales were rising, albeit slowly. During both periods of rising gasoline prices, consumers purchased an increasing share of cars versus trucks, especially small and midsize cars (see table 1).1

Table 1. Percent increase in sales by segment group

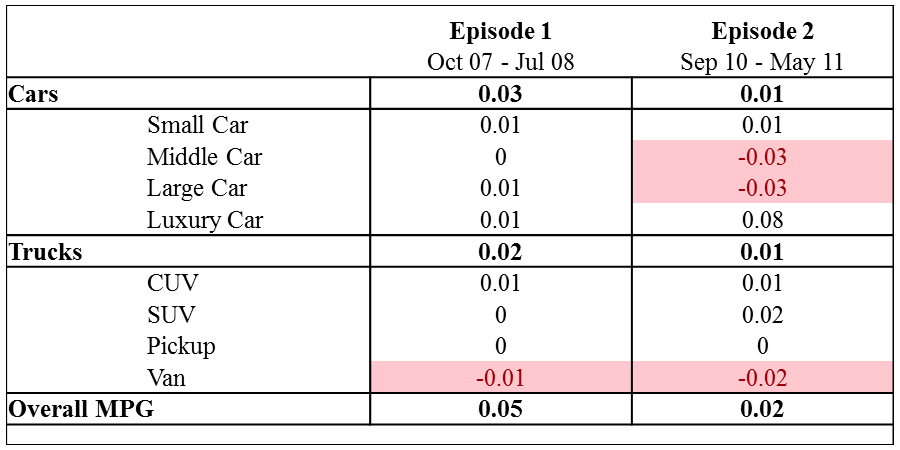

In combining data on vehicle fuel efficiency (available online) with vehicle sales, we can calculate the change in the fuel efficiency of all new vehicles purchased during the respective periods (see table 2). Not surprisingly, we find that during periods of high and rising gasoline prices, consumers on balance favor cars over trucks. This effect was more pronounced during episode 1, which mostly took place during the recession. In both episodes, consumers purchased a more fuel-efficient mix of vehicles. That effect was stronger during episode 1 when the sales-weighted fuel efficiency of light vehicles rose by 5%, and fuel efficiency increased in seven of the eight vehicle segment groups.

Table 2. Percent increase in sales-weighted fuel efficiency

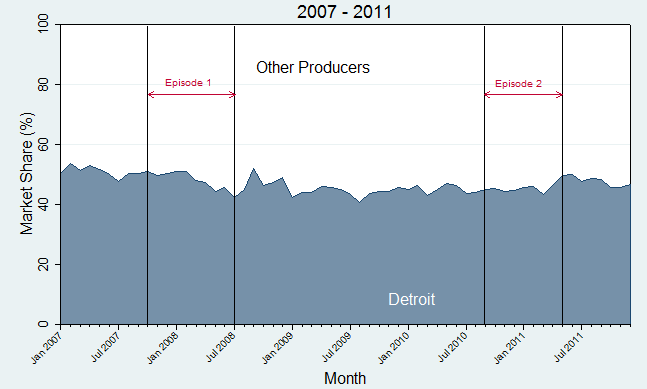

How well did the Detroit producers fare in the market place during these two episodes? Overall the Detroit producers lost market share during the first episode, but gained market share during the second episode (see figure 2).

Figure 2. Detroit share of light vehicle sales

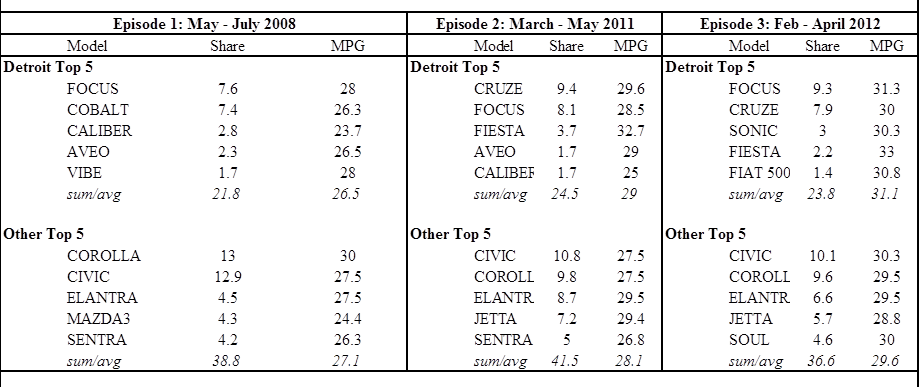

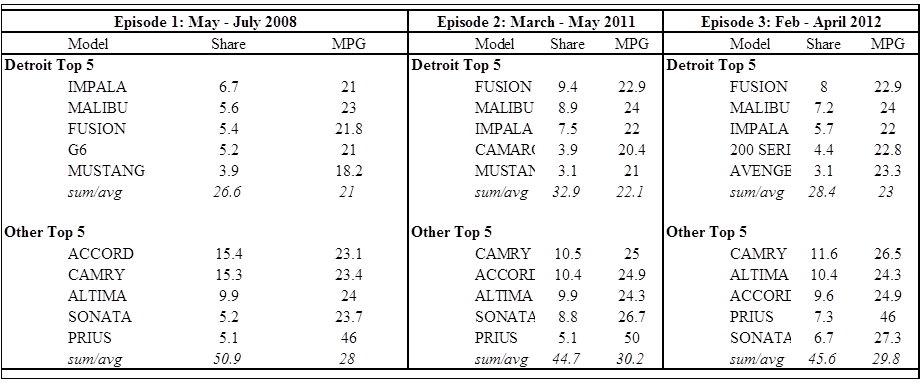

Given that consumers purchased a more fuel-efficient mix of vehicles in both episodes, it is possible that the improved market share gains of the Detroit automakers reflect improvements in the fuel efficiency of their products. To explore this hypothesis, we focus on the small and midsize car segments, the part of the market in which Detroit has traditionally not done well during periods of high gasoline prices. Tables 3 (small cars) and 4 (midsize cars) tell the story. During the second episode of rising gasoline prices, Detroit’s product offerings, even among the small cars, fared noticeably better than during episode 1. The tables highlight only the top five selling small and midsize models, measured in units sold, for both the Detroit producers and their competitors. For each model, the tables report the market share and fuel efficiency (averaged across individual trim lines and combinations of engines and transmissions on offer).

Note that all continuing Detroit models listed became more fuel efficient over time. In addition, new models, such as the Chevy Cruze, were successfully launched. But not only did the fuel efficiency of the Detroit carmakers’ products improve, so did their market share. In both segment groups, the five best-selling Detroit models as a group picked up market share—nearly 3 percentage points in small cars and just over 6 percentage points among midsize cars.

Table 3. Top 5 selling small cars

Table 4. Top 5 selling middle cars

The previous two tables suggest that it was indeed improved product offerings that resulted in market share gains for the Detroit producers. There is, however, a caveat to this interpretation: Episode 2 took place shortly after the March 2011 earthquake and subsequent tsunami in Japan, which severely affected its manufacturing sector. It is possible that Detroit’s gains in this period were related to supply constraints among Japanese competitors.

We try to get some additional insight by looking at a more recent, though less sustained, episode of gasoline price increases. Between December 2011 and April 2012, the price of gasoline rose quickly to $3.90 per gallon. While episode 2 took place shortly after the earthquake, episode 3 covers a period that includes the recovery of the Japanese producers, notably Honda and Toyota, from production constraints related to the earthquake. (The industry press suggests that both companies had returned to full production by September 2011; see for example a story from Automotive News).2

Tables 3 and 4 also provide information from the last three months of episode 3, and we can see that a couple of trends continued: All of Detroit’s continuing models became more fuel efficient, and Detroit’s market share continued to be higher than in episode one in both segments, despite the abating supply constraints for the Japanese producers. On the other hand, the Japanese producers regained market share, especially for the midsize car segment. Note the strong increase in market share for the Toyota Prius, a vehicle exclusively produced in Japan, between episodes 2 and 3. Four of the five top-selling midsize cars not produced by the Detroit carmakers were produced by Japanese carmakers. The share of those four dropped by nearly 10 percentage points between episodes 1 and 2, likely reflecting supply constraints. By April 2012, it had recovered 3 percentage points. In small cars, the market share rebound of Japanese models was smaller in magnitude, with Detroit’s share barely falling back between episodes 2 and 3.

We conclude that, on net, the evidence suggests that the relative improvement in market shares of small and midsize vehicles produced by the Detroit automakers during the first half of 2011 was due to both product improvements in fuel efficiency and supply constraints experienced by their Japanese competitors.

Much has been written about renewed consumer interest in the fuel efficiency of vehicles (see for example here). Detroit appears to have taken note of this trend—leading to positive results in the marketplace.

Footnotes

1 Consumers tend to substitute vehicles subject to the utility they expect to obtain from a specific vehicle, such as transporting a family, towing a boat, or mainly commuting to work. Substitutions across specific vehicle models likely involve vehicles within the same or closely related segment groups (Table 1 distinguishes four segment groups each for cars and trucks). Trucks tend to be less fuel efficient as a group. For example, in 2011 the sales weighted average fuel efficiency for cars was 26.0 mpg; for trucks it was 19.2 mpg.

2 We do not have evidence of changes in the relative price of Detroit’s versus the Japanese companies’ products during this time. Note, however, that episode 3 includes the Chevrolet Sonic, the only subcompact currently being produced in the U.S. Its production is supported by a special labor agreement with the UAW that provides for a much higher share of entry-level wages being paid at the Orion, Michigan plant, where the car is being produced (see, for example, the following story in the New York Times).