The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

In mid-May 1997, the United States International Trade Commission (USITC) held public hearings as part of its investigation into the economic effects of the North American Free Trade Agreement (NAFTA) over the course of its first three years. The investigation, The Impact of the North American Free Trade Agreement on the U.S. Economy and Industries: A Three Year Review, was requested by the Office of the United States Trade Representative (USTR) as an outgrowth of the still unsettled debate over the benefits and costs of pursuing a free trade agreement with a developing country.1 Section 512 of the North American Free Trade Agreement Implementation Act requires President Clinton to report to Congress on the operation and effects of NAFTA in the agreement’s first three years. The USITC’s report, released in June 1997, was the main source for the Administration’s final report to Congress, released by the USTR on July 11, 1997.2 The NAFTA debate and the recent USITC and USTR inquiries have led economists to think carefully about how to measure the economic benefits of free trade agreements. This Chicago Fed Letter reviews economists’ long-established ways of evaluating the gains from trade liberalization and introduces some more recent innovations in the context of NAFTA.

“Trade policy” analysis can be classified as either short-run or long-run. Short-run analysis focuses on the transition period following the implementation of a new trade policy, in which factors of production, especially workers, are relocated across industries and countries, and new investment in productive capital is undertaken. In contrast, long-run analysis ignores the transition period from the old restricted trade environment to the new liberalized environment and studies the economy once the reallocation of factors and new capital investment are completed. Until recently, all trade liberalization analysis was of the long-run variety.

In 1817, David Ricardo performed a long-run analysis of the United Kingdom’s “corn laws,” which were a form of import restriction on agricultural imports. Ricardo was concerned that these import restrictions would hinder the U.K.’s ability to grow. In particular, he analyzed the impact of the U.K.’s corn laws on trade between the then less-developed, land-rich, Baltic countries and the more industrialized U.K. This is typically referred to as North-South trade analysis, that is, trade between industrial (northern) and developing (southern) economies. Ricardo successfully argued against the laws (they were later repealed). The exercise may seem distant to us because it was conducted over 150 years ago, but it remains very relevant to the NAFTA debate. Much like NAFTA, it involved trade liberalization between countries at very different stages of development. In this regard, Ricardo’s analysis established an analytical framework that is still useful today.

The centerpiece of Ricardo’s analytical framework was a mathematical model of international trade that shed light on the likely impact of trade restrictions. He was able to show that the corn laws had a negative impact on the U.K. economy, much akin to the effects that today’s trade restrictions have on national economies.

Ricardo’s analysis was instrumental in establishing the field of international trade and developing the basic tools of trade analysis. Through his work and the work of others, we understand that the value of international trade lies in its ability to expand economic opportunities. In the 1930s, Paul Samuelson added to this body of work by showing that, if a country chooses to engage in trade, then trade must lead to an unambiguous improvement in aggregate well-being of that country. However, Samuelson’s “gains from trade theorem” is an aggregate result, which leaves open the possibility that while trade makes the country better off, it may make some individual(s) in the country worse off. What is true about Samuelson’s result is that a country is deemed to be better off because the gains from trade are such that those who are made better off are able to compensate those who are made worse off and still have some of the gain left over. This is the sense in which trade improves the aggregate well-being of a country.

Another qualification is that policymakers are rarely faced with the choice between switching their country from no trade to trade (or vice versa). They must deal with moving from one restricted trade setting to a possibly less restricted trade setting. For example, the pre-NAFTA environment was more restricted than the post-NAFTA environment. NAFTA is still a restricted trade environment because Canada, Mexico, and the U.S. still have in place trade barriers to countries outside North America. The improvements in a country’s well-being are even more ambiguous in such instances. One of the more frustrating results in the theoretical trade literature is that moving from a restricted setting to either a less-restricted or free-trade setting may in fact make one of the liberalizing countries worse off. Only an open economy that is so small it cannot influence world commodity prices has been shown unambiguously to be better off following unilateral liberalization.

Overcoming the shortcomings of existing models

Ambiguous theoretical results on the effects of trade liberalization, along with technological developments in computer hardware and software and advances in theoretical economic analysis, have stimulated quantitative work that measures the international, macroeconomic, and microeconomic impact of trade policies. The dominant approach uses detailed simulation models with many households and firms to measure how different industries, household income groups, and countries are affected by changes in trade policy. In much the same vein as Ricardo’s analysis of the corn laws, this approach employs models that are designed to tell us something about the long-run impact of a trade policy change. These models ignore any transitional effects associated with the change in trade policy and are generally referred to as static trade models.

Although widely used, static models have a number of shortcomings, which in the aggregate understate the benefits of trade liberalization and overstate the sectoral or individual costs of trade liberalization. This has encouraged the development of quantitative dynamic models that tell us something about both the short- and long-run effects of trade policy. Dynamic models are more realistic than static models in three important ways. First, static models limit the world supply of physical capital to that available in the pre-liberalization period. Therefore, improvements in economic well-being and output gains associated with trade liberalization come from the reallocation of physical capital across sectors and countries in a static model. A reallocation of factors will mean that some sectors must contract as others expand. Static models ignore the fact that physical capital accumulation is easier under free trade and therefore understate the potential output gains that accrue from liberalization. In a dynamic model, production gains flow from greater investment in physical capital and a reallocation of factors across sectors and countries.

Second, traditional static trade models neglect trade in financial assets by restricting trade balances to zero. International capital flows allow households to maintain consumption levels while undertaking major physical capital investment. In the absence of international trade in financial assets, households are less likely to undertake large and rapid capital investment. Therefore, static models tend to underestimate the improvement in economic well-being that flows from trade liberalization.

Finally, static models, like a camera, record snapshots at different stages of time. In analyzing free trade policy changes, they record the state of the world before the trade policy is implemented and after the economy has adjusted to the new trade policy environment. These models offer no estimate of the length of time it takes to get to the new long-run path. Dynamic models provide this information.

A dynamic model is more like a video camera in that it records the sequence of events from the time the policy change is enacted to the point where the model settles down to its new long-run position. Dynamic models also allow one to build in anticipated policy changes. For example, NAFTA was discussed in the early 1990s, but not implemented until 1994. Most households and firms fully expected NAFTA to come into effect from the time the initial agreement was signed in December 1992. With a dynamic model, simulations can begin at some specific point in time that may precede the implementation of a policy.

In addition to quantitative theoretical models, researchers have made advances using time-series econometric techniques to measure the impact of liberalization policies such as NAFTA. Time-series analysis differs significantly from quantitative theoretical analysis. Quantitative models are generally fitted to data before the implementation of trade liberalization and then simulated forward to formulate a prediction about the likely impact of the trade policy. Time-series techniques try to measure the impact of the trade liberalization from data after the policy is implemented. The approaches are not completely independent, because time-series models need to have some structure imposed in order to draw inferences from the data. Typically, economists draw on the insights gained from quantitative theoretical models when imposing structure on a time-series model. One drawback associated with time-series analysis is that measures of economic well-being are theoretical constructs, which means that measures of the gains from liberalization can only come from a fully specified quantitative trade model, which time-series analysis cannot provide.

For example, one measure of the change in trade-associated well-being that can be obtained from quantitative trade models is a “compensating variation.” In the context of NAFTA, the compensating variation is that level of consumption you would have to give to the households in each country in the pre-NAFTA environment to make them indifferent to NAFTA. In other words, the compensating variation measures the amount of additional consumption goods households would have to have in the pre-NAFTA environment to make them as well off as under NAFTA.

Elsewhere, I have developed a dynamic North-South trade model to assess the gains from NAFTA.3 The simulations begin at the date of the signing of the initial NAFTA agreement (December 1992), a little over a year before the implementation of NAFTA. My simulation work takes NAFTA to be the joint free-trade agreement between the U.S. and Mexico, and Canada and Mexico, so there is no U.S.–Canada liberalization (because that was essentially agreed to in the Canada–U.S. Free Trade Agreement of 1989 [CFTA]). Simulations of the dynamic model suggest that the compensating variation, in terms of the percent change in pre-NAFTA consumption, required to leave households indifferent between the pre-NAFTA environment and NAFTA is 0.96% for Mexico, 0.12% for the U.S., 0.01% for Canada, and 0.01% for countries outside North America. Based on these results, NAFTA leads to improvements in economic well-being for all participants.

In addition, simulations of my dynamic model suggest that NAFTA leads to an expansion of output, investment, consumption, labor hours, and trade in all three North American economies from the time it comes into effect in January 1994. Mexico enjoys the largest expansion within the region (in percentage change terms). Under NAFTA, Mexico’s level of gross domestic product (GDP) is predicted to rise by 3.26% by December 2009. Underlying this increased output is greater capital accumulation and increased labor input. The expanded output is also reflected in an increased level of consumption of 2.52% and double-digit increases in export and import volumes. The model predicts NAFTA will also lead to capital inflows to Mexico. Over the simulation period (December 1992 to December 2009), Mexico’s ratio of net foreign assets to GDP falls by 8 percentage points. Most of the capital inflows are expected to come from countries outside North America. NAFTA has a smaller impact on the U.S., with the level of U.S. GDP rising by 0.24%. The level of aggregate U.S. trade is predicted to rise by about 1.5%. Trade with Mexico is expected to rise by almost 20%. Given the small volume of Mexican–Canadian trade, it is not surprising that NAFTA has a negligible impact on the Canadian economy, with the level of output expected to rise by 0.11%. According to the model, NAFTA will have a negligible impact on countries outside North America.

Although there is a wealth of quantitative research on NAFTA, outcomes are not altogether comparable because they generally consider very different policy experiments and measures of economic well-being. This makes policy evaluation extremely difficult for groups like the USTR and USITC. For example, my model’s calibration draws on the parameters used in Roland-Holst et al. (1992, 1994), which makes their study a logical static benchmark for my dynamic analysis.4 However, Roland-Holst et al. take a somewhat broader view by allowing NAFTA to include the CFTA. Brown et al. (1992) define NAFTA in roughly the same way as my dynamic analysis.5 Brown et al. offer a static analysis, in which North America is fully modeled as in my analysis, but they measure economic well-being in a different way, so comparisons between their work and mine can only be made for real economic activity.

Brown et al. find, as I do, that NAFTA has a large impact on the Mexican economy, but a negligible impact on Canada, the U.S., and countries outside North America by the time the agreement is fully implemented in December 2009. Their static model predicts that the level of Mexican GDP will rise by 2.2% and that Canadian and U.S. GDP will be 0.10% higher following NAFTA. Overall, the direction of change predicted by the static and dynamic models following NAFTA is the same. However, the predicted impact is significantly larger (roughly one and a half times in the case of Mexico) in the dynamic model. This is because the static models limit the world capital stock to its pre-NAFTA level and rule out international capital flows. Greater capital accumulation in the dynamic model explains roughly two-thirds of the change in the level of North American output. In particular, Mexico’s GDP is predicted to rise by roughly 3% of its pre-NAFTA level. Changes in Mexico’s capital stock alone explain roughly 2% of this change, while increased labor effort accounts for the remaining 1%.

Conclusion

The development of dynamic models is the first step toward developing a more realistic model of international trade for trade policy analysis. One of the inherent weaknesses of the current variety of dynamic models is that they assume an exogenous long-run growth rate. Future technological developments will be directed at developing dynamic models that allow for endogenous long-run growth rates. Current dynamic models suggest that the gains from free trade agreements are significantly larger than those of static models, but they ignore growth effects associated with trade liberalization. Changes in the growth rate accumulate over time. If endogenous growth models find that trade liberalization has a significant impact on growth rates, then the gains from liberalization will easily outweigh those predicted by current dynamic models.

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| July | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 121.1 | 120.8 | 117.4 |

| IP | 121.4 | 121.3 | 117.0 |

Motor vehicle production (millions, seasonally adj. annual rate)

| July | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.8 | 5.7 | 7.0 |

| Light trucks | 4.9 | 5.8 | 6.0 |

Purchasing managers' surveys: net % reporting production growth

| August | Month ago | Year ago | |

|---|---|---|---|

| MW | 60.5 | 58.7 | 63.0 |

| U.S. | 62.4 | 64.4 | 56.2 |

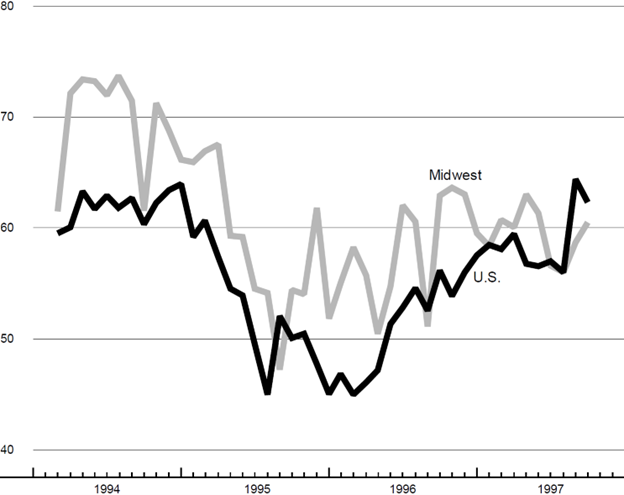

Purchasing managers’ surveys (production index)

The CFMMI increased 0.2% from June to July, following a 0.1% decline in June. By comparison, the Federal Reserve Board’s IP increased by 0.1% in July and 0.3% in June. The machinery sector had the strongest performance in the Midwest index, increasing by 1.3% in July. The steel sector recorded a 0.2% rise, following a 1.4% decline in June, its first decline in seven months. The resource sector’s output fell by 0.2%, its fourth straight monthly decline.

The Midwest purchasing managers’ composite index increased to 60.5% in August, its highest level since February 1995. The national purchasing managers’ composite index decreased from 64.4% in July to 62.4% in August, indicating that activity in the manufacturing sector slowed from the previous month. Motor vehicle production for July increased from 5.7 million to 5.8 million units for cars and decreased from 5.8 million to 4.9 million units for light trucks.

Notes

1 The Impact of the North American Free Trade Agreement on the U.S. Economy and Industries: A Three Year Review, No. 3045, July 1997.

2 The USTR’s report is titled A Study on the Operation and Effect of the North American Free Trade Agreement.

3 M.A. Kouparitsas, “A dynamic macroeconomic analysis of NAFTA,” Federal Reserve Bank of Chicago, Economic Perspectives, Vol. 21, No. 1, Jan/Feb 1997, pp. 14–35.

4 D.W. Roland-Holst, K.A. Reinert, and C.R. Shiells, “North American trade liberalization and the role of non-tariff barriers,” in Economywide Modeling of the Economic Implications of an FTA with Mexico and a NAFTA with Canada and Mexico, U.S. International Trade Commission, No. 2508, 1992, pp. 523–580. Also, D.W. Roland-Holst, K.A. Reinert, and C.R. Shiells, “A general equilibrium analysis of North American economic integration,” in Modeling Trade Policy: Applied General Equilibrium Assessments of North American Free Trade, J.F. Francois and C.R. Shiells (eds.), Cambridge, U.K.: Cambridge University Press, 1994.

5 D.K. Brown, A.V. Deardorff, and R.M., Stern, “A North American Free Trade Agreement: Analytical issues and a computational assessment,” The World Economy, Vol. 15, 1992, pp. 11–30.