Research by Abdoulaye Ndiaye,1 summary by Lisa Camner McKay

Changing the income tax system and increasing the benefit to delaying retirement may preserve the social insurance guarantee to retirees.

The biggest social safety net in the United States is the Social Security program, which provides retirement benefits totaling almost $900 billion to 54 million individuals.2 When planning when to retire, individuals consider not only their health and personal savings but how their Social Security retirement benefits compare with their after-tax income when working: When can they afford to retire?

It is a concern for all but the wealthiest, then, that Social Security faces insolvency. The U.S. Social Security Administration predicts that in 2020, the costs of the program will exceed its income.3 This suggests it is critical for policymakers to evaluate whether there is a path for Social Security reform that will improve people’s welfare both before and after retirement while restoring the program’s solvency.

The goal of social insurance is to provide compensation to individuals with low incomes. The program must be funded by taxes, however, which can act as a disincentive to work and thus may reduce economic growth. These two elements, social insurance and economic efficiency, must be balanced in order to restore solvency to Social Security. Furthermore, in the case of Social Security specifically, the costs of the program are affected by the age at which workers retire. In a system in which workers can decide for themselves when they will retire, this decision is a function of how much the worker would receive in retirement benefits compared with how much the worker earns in after-tax income. The income tax, in other words, affects the retirement decision. For these reasons, it is useful to look at Social Security and tax reforms together.

Reforming income taxes and retirement benefits

This is the approach of Abdoulaye Ndiaye, a research economist at the Federal Reserve Bank of Chicago. In his paper “Flexible retirement and optimal taxation,”4 Ndiaye analyzes both tax reforms and Social Security reforms in the context of a system that allows individuals to choose for themselves when to retire. He finds that enacting two specific changes simultaneously to the tax system and the Social Security system would improve economic welfare, that is, the overall level of financial satisfaction and prosperity experienced by participants in the U.S. economic system.

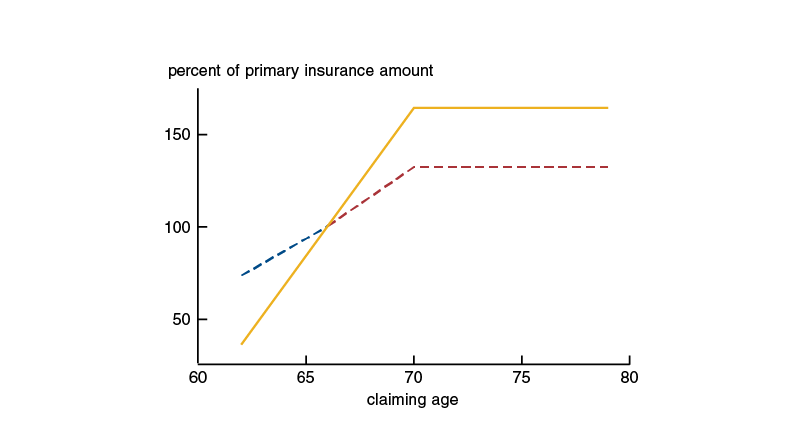

First, Ndiaye’s research suggests that Social Security should be reformed so that benefits vary more depending on when an individual retires. Currently, Social Security sets the “normal” retirement age at 66. Individuals who retire early receive slightly less than their full benefits and those who retire later receive slightly more. To increase economic welfare overall, Ndiaye finds the early retirement penalty and the late retirement benefit need to be much larger, perhaps twice as large as in the current system (see figure 1).

1. Social Security benefits as a function of claiming age

Source: Abdoulaye Ndiaye, 2018, “Flexible retirement and optimal taxation,” Federal Reserve Bank of Chicago, working paper, No. 2018-18, November 5. Crossref

At the same time, Ndiaye argues that the income tax should be changed so that the tax rate depends on the worker’s age. In the current U.S. system, an individual’s marginal tax rate depends only on income. Older workers who have the option of retiring, however, are more sensitive to the tax rate than are younger workers. Ndiaye finds that a tax rate that is hump-shaped in age—first increasing as workers age and then decreasing—would achieve higher welfare than the current tax system (see figure 2).

2. Optimal average marginal labor tax rate by age

Source: Abdoulaye Ndiaye, 2018, “Flexible retirement and optimal taxation,” Federal Reserve Bank of Chicago, working paper, No. 2018-18, November 5. Crossref

Together, these two reforms should cause highly productive individuals (who have high incomes) to remain in the workforce for longer than they do now, because their taxes would go down as they approach retirement age while the benefit to working a few extra years would go up. This would allow the government to continue to collect taxes on their income to fund Social Security. Workers with low salaries, meanwhile, could retire earlier and collect benefits. In this way, these reform proposals balance social insurance and economic efficiency.

An economic model of retirement

The process by which Ndiaye reaches this conclusion involves several steps. First, he builds a life-cycle model of the economy in which workers receive an income and then choose how many hours to work, how much to consume, and when to retire so as to maximize their utility. (Economists usually assume people get positive utility from consumption and negative utility from labor.) A life-cycle model looks at workers’ choices over their life span, from the time they enter the workforce until death.

Importantly in this model, income varies over time through idiosyncratic shocks to workers’ productivity. When workers enter the labor force, they are fairly similar in their abilities and are paid similar wages. Over time, however, some workers become more productive and others less productive. They are compensated accordingly, which causes incomes to diverge. Thus, Ndiaye’s model captures the real-world fact of income inequality.

Because people do not know whether they will turn out to be highly productive or not, they have a reason to remain in the workforce and not retire, say, at age 45: If they do become highly productive, they will earn a high income. This uncertainty means there is an advantage to staying in the workforce.

The purpose of building this model is to solve what economists call “the planner’s problem.” The idea here is to ask, if there were an economic planner who jointly maximized everyone’s utility, how much would people work, how much would they consume, and when would they retire? To do this, the planner is able to make transfers among workers and retirees. Once Ndiaye knows this optimal plan, he can then analyze different tax systems and Social Security programs to see how close they get to achieving it.

Before solving the model for the optimal plan, Ndiaye first confirms that when real-world data are used as inputs, the model’s predictions align with what we actually see happen. For instance, when the current Social Security system is fed into the model, the model’s predictions align with what we observe in terms of the heterogeneity in retirement behavior—in other words, the frequency of retirement at different ages. This serves as a check on the model’s accuracy.

So what does the optimal plan look like? Ndiaye calculates that the average retirement age would be 69.6 years and the labor force participation rate for individuals aged 65–69 would be 78%. In comparison, in the U.S. today, the average retirement age is 66.5 years and the labor force participation for 65–69 year olds is 32%. So the average retirement age increases by about three years—significant yes, but small compared to the increase in life expectancy since the Social Security Administration was created.

When Ndiaye quantifies what these changes would look like in terms of welfare, he finds that it is equivalent to an increase in consumption of almost 2% for everyone: both high and low productivity workers, both before and after retirement. This is a significant increase in the context of what macroeconomic policy can accomplish.

Two is better than one

The final step in Ndiaye’s analysis is to evaluate how close various reforms of the tax system, the Social Security system, or both can get to achieving that theoretical 2% increase in consumption that occurs with the optimal labor force participation rates described above.

For instance, what happens if only the tax system is reformed to make taxes hump-shaped with age, leaving the Social Security system as it is? It turns out this produces only half of the welfare gains of the optimal plan because this actually induces workers to retire even earlier than they do under the current system.

Ndiaye also compares three different types of reforms of Social Security to see which has the biggest impact: one, lower total benefits for everyone; two, make benefits more progressive; and three, change the adjustment rate to Social Security benefits depending on retirement age. Of these, it is the last one that impacts welfare the most because it has the biggest influence on when people choose to retire. Ndiaye calculates that the adjustment rate for Social Security benefits must be around 16% a year (so retiring a year early reduces benefits by 16% and retiring a year late increases benefits by 16%). This is about twice what the current adjustment rate is. However, reforming only Social Security while the income tax system stays the same produces only a third of the welfare gains of the optimal plan.

Ultimately, what Ndiaye finds is that implementing both reforms at once—marginal income tax becomes hump-shaped with age, Social Security benefits have a larger adjustment rate—produces the largest welfare gains of any of the reforms that he looks at. These two changes together capture almost all of the welfare gains of the optimal plan.

Conclusion

It is an astounding fact that since the Social Security Administration was created in 1935, life expectancy in the United States has increased by almost 30 years. It is a welcome problem, then, that the U.S. government is paying retirement benefits to its citizens for decades rather than months, causing the Social Security Administration to eventually run out of money. Solvency could perhaps be restored by raising the retirement age or decreasing overall benefits. Ndiaye’s research suggests another avenue that proves more fruitful, however, while still preserving individuals’ ability to choose when to retire. If benefits are steeper in claiming age, providing more benefit to delaying retirement, while taxes decline for older workers, productive older workers will have an incentive to remain in the workforce. Ndiaye’s research indicates that these policy reforms could preserve the social insurance guarantee without sacrificing economic productivity.

1 Abdoulaye Ndiaye was a research economist at the Federal Reserve Bank of Chicago until mid-2019, when he took up a position as an assistant professor of economics at the Leonard N. Stern School of Business, New York University. (@Abdounomics)

2 U.S. Social Security Administration, 2018, “Fiscal year 2019 budget overview,” report, Baltimore, February 12, available online.

3 Alan Rappeport, 2019, “Social Security and Medicare funds face insolvency, report finds,” New York Times, April 22, available online.

4 Abdoulaye Ndiaye, 2018, “Flexible retirement and optimal taxation,” Federal Reserve Bank of Chicago, working paper, No. 2018-18, November 5. Crossref