Research by Sarah Miller, University of Michigan, Luojia Hu, Federal Reserve Bank of Chicago, Robert Kaestner, University of Chicago, Bhashkar Mazumder, Federal Reserve Bank of Chicago, and Ashley Wong, Northwestern University

Summary by Lisa Camner McKay, economics writer

Low-income Americans who became eligible to enroll in Medicaid due to the Affordable Care Act saw their medical debt cut in half.

The Patient Protection and Affordable Care Act of 2010 (ACA) was signed into law with a simple but lofty goal: to give more Americans “the financial security of health insurance.”1 The fact is, paying medical bills is hard for many Americans—in 2014, nearly 20% had medical debt on their credit reports2—but it’s especially challenging for those who lack health insurance, because medical care is expensive. A hospital stay can run north of $15,000,3 while insulin, a drug to treat diabetes, can cost as much as $450 every month.4

One of the ways in which the ACA made insurance attainable for more Americans was to change the eligibility for Medicaid, a government program to provide health insurance to low-income Americans, to include all adults ages 18–64 whose income was less than 138% of the federal poverty level (in 2019, this came to $35,535 for a family of four). The result was one of the largest expansions of health insurance coverage in 50 years, with approximately 12 million new enrollees in Medicaid through 2015 (Hu et al., 2018). Now that several years have passed since this expansion occurred, it is worth asking: Has financial well-being improved for people who gained insurance as a result of the policy change?

This question has motivated Luojia Hu and Bhashkar Mazumder, senior economists at the Federal Reserve Bank of Chicago, who with their co-authors Robert Kaestner, Sarah Miller, and Ashley Wong have used variation in Medicaid expansion to estimate the effect that enrolling in Medicaid has on a variety of financial outcomes. Their results affirm that health insurance does indeed offer financial protection to individuals, most notably by reducing the amount of overdue debt sent to third-party collection agencies.

Medicaid expansion states versus nonexpansion states

In their first investigation, Hu, Mazumder, and their co-authors use the fact that Medicaid expansion was not universal across all 50 states to compare financial outcomes in expansion and nonexpansion states. A U.S. Supreme Court decision allowed each state to decide whether or not to expand Medicaid. As of December 2015, 29 states plus the District of Columbia had expanded Medicaid eligibility, while 21 states had not.

However, there is a methodological challenge here: When the researchers looked at trends in financial outcomes in the two groups of states prior to Medicaid expansion, they found notable differences. For example, in expansion states, the average amount of overdue debt owed by an individual that had been sent to collection agencies held steady between 2010 and 2013 at around $330. However in nonexpansion states, the average increased considerably, from $426 to $535. Because there were differences in financial outcomes before Medicaid expansion, it seems reasonable to assume there will be differences after expansion as well.

The authors’ solution is to adopt a strategy called the synthetic control method. Put simply, this approach uses a weighting strategy to adjust the pre-expansion outcomes so that the average values in the expansion states are similar to those in the nonexpansion states. Then the authors compare the adjusted outcomes in the two groups of states after Medicaid expansion.

The next challenge is that Medicaid enrollment data is private, so the authors were not able to identify specific individuals who enrolled in Medicaid. Instead, they looked at the 8,100 zip codes in the country (home to approximately a quarter of the population) with the highest rates of uninsured individuals and the lowest incomes, assuming Medicaid enrollment was most likely in these areas.

Because the authors are interested in financial well-being, they look at credit report data from Equifax, one of the three major credit bureaus in the U.S., which includes a variety of measures of individual debt. They find that by the end of 2015, two key indicators of financial health do show improvement: The number of bills in collections and the amount of debt in collections both go down, which is good news for Medicaid enrollees. Other financial outcomes also appear to improve, but the differences are not statistically significant. These results are suggestive that gaining health insurance improves financial health. Keep in mind, however, that these results include everyone ages 18–64 in the 8,100 zip codes, including many individuals who did not enroll in Medicaid. The next step, then, is to look at outcomes specifically for individuals who enrolled in Medicaid as a result of the ACA policy change.

Financial outcomes for Michigan’s Medicaid enrollees

Ultimately, identifying the change in financial outcomes for people who enrolled in Medicaid will be more reliable if the analysis can identify those who actually enrolled. This is what the authors were able to do in Michigan by obtaining Medicaid administrative data for 267,000 adults who enrolled in the state’s expanded Medicaid program, called the Healthy Michigan Plan, between April 2014 and March 2015.5

These new enrollees, who previously had no health insurance, tended to be poor, in poor health, and in dire financial straits. Their average household income when they enrolled in Medicaid was only 39% of the federal poverty level (about $9,500 for a family of four in 2015). About 70% had a chronic illness. They also had significant debt, with an average of $2,000 in overdue debt held by third-party collection agencies, of which $1,000 was medical debt. In comparison, these numbers are about twice as large as those of an average Michigan adult in 2015.

The authors analyze the effects of Medicaid enrollment in two ways. First, they use simple descriptive statistics to compare average financial well-being before enrollment with the average after enrollment. The results are positive: Every indicator of financial well-being that they look at improves. This means that individuals who gained insurance through Medicaid as a result of the ACA had less debt in collections, less debt past due, fewer public records (indicators of a negative financial event, such as a wage garnishment or eviction), and fewer bankruptcies. They were also overdrawn on their credit cards less often and fewer had a credit score in the “subprime” category (subprime borrowers are considered to be extremely high risk).

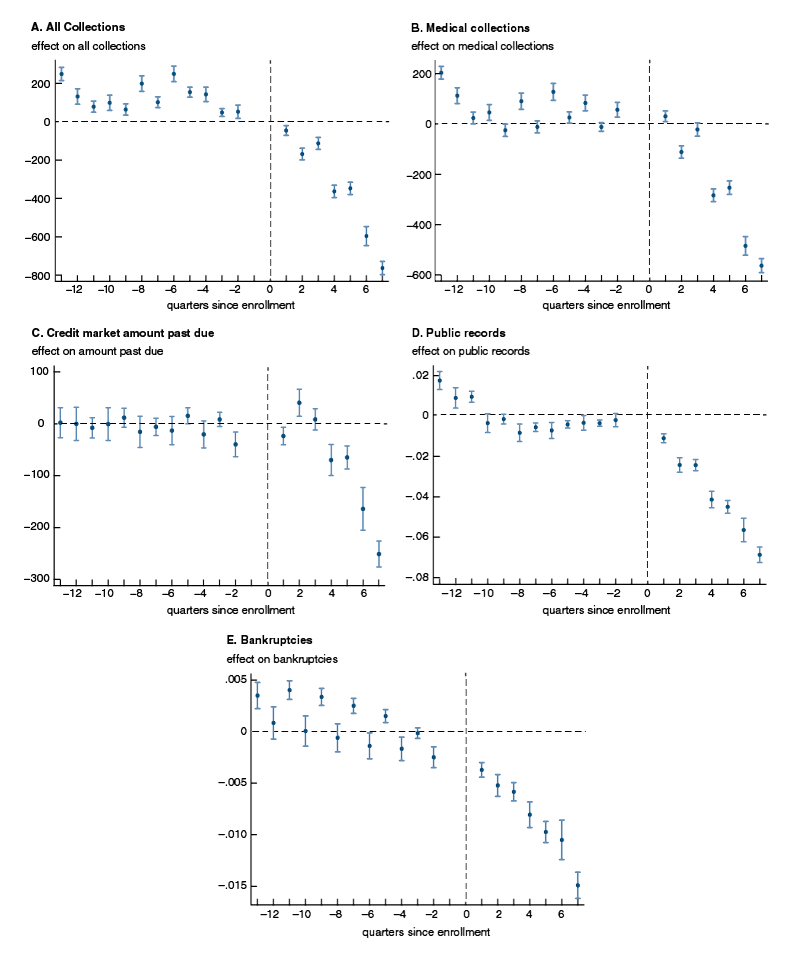

The authors then conduct an event study analysis, which lets them see how various indicators of financial well-being behave over time. The general idea of this approach is to compare financial outcomes after an individual enrolls in Medicaid (the “event”) to an estimate of what those outcomes would have been had the event not occurred. Using debt as an example, the authors look at the trend of an individual’s debt before enrollment—Is it going up? Down? By how much?—and carry that trend forward. Then they compare that estimate to what actually happened after Medicaid enrollment. Once again, the results support the conventional wisdom that having health insurance improves financial health: “In all cases, we see reductions in measures of delinquency, and these effects appear to grow over time” (Miller et al., 2018).

That the effects of enrollment grow over time is one of the paper’s significant findings. This trend is evident in figure 1; all panels show a decline that gets bigger over time. The event study analysis allows the authors to estimate just how much of an effect enrolling in Medicaid has 21 months (seven quarters) later, the date of the last credit reports in the data set. The numbers are large. Overdue debt sent to a collection agency falls about $740 per person, which is over a third of the pre-enrollment total, while medical debt in collections falls by about $511, half of the pre-enrollment value. Enrollees also have 10–15% fewer public records on their credit reports. And the number of bankruptcies for enrollees goes down by 10%.

1. Trends in financial outcomes before and after enrolling in Medicaid

Source: Sarah Miller, Luojia Hu, Robert Kaestner, Bhashkar Mazumder, and Ashley Wong, 2018, “The ACA Medicaid expansion in Michigan and financial health,” National Bureau of Economic Research, working paper, No. 25053, September. Crossref

The Medicaid enrollment data also allows the researchers to look at financial outcomes for different populations of enrollees. They are interested specifically in how individuals in particularly poor health fare after enrolling in Medicaid. Individuals who were hospitalized, visited the emergency room, or had a chronic illness had an even worse financial portfolio before they enrolled than the rest of the Medicaid enrollees. They also saw bigger improvements as a result of gaining health insurance, particularly for their total amount of overdue debt in collections and medical debt in collections. This analysis shows that those who need the most help—individuals in poor health with no health insurance—saw their debt, particularly their medical debt, go down substantially.The Medicaid enrollment data also allows the researchers to look at financial outcomes for different populations of enrollees. They are interested specifically in how individuals in particularly poor health fare after enrolling in Medicaid. Individuals who were hospitalized, visited the emergency room, or had a chronic illness had an even worse financial portfolio before they enrolled than the rest of the Medicaid enrollees. They also saw bigger improvements as a result of gaining health insurance, particularly for their total amount of overdue debt in collections and medical debt in collections. This analysis shows that those who need the most help—individuals in poor health with no health insurance—saw their debt, particularly their medical debt, go down substantially.

Establishing a causal relationship

One of the most challenging elements of social science research is establishing causality: Is the fact that two things happen at the same time actually evidence that one causes the other? In this case, the data show that financial outcomes have improved between 2011 and 2016. Is Medicaid really the cause? Yes, say Mazumder and Hu: “Because all individuals in our sample enrolled in HMP [Michigan’s Medicaid program], these estimates can be directly interpreted as the treatment effect of Medicaid coverage” (Miller et al., 2018). To add additional weight to this claim, the author team compared financial outcomes for the Michigan Medicaid enrollees to outcomes of low-income Michigan residents who did not enroll. By January 2016, their last credit report observation, Medicaid enrollees had less total debt in collections, less medical debt in collections, and fewer public records. This is strong evidence that enrolling in Medicaid did indeed result in improved financial well-being.

What’s more, the positive impact of Medicaid described in these studies may be just the beginning. Hu, Mazumder, and their co-authors find that the effect of Medicaid increases over time. However, their data ends at January 2016, less than two years after the Medicaid expansion took effect. It is very possible that debt, bankruptcies, and overdrawn credit have continued to decrease for Medicaid enrollees, making gaining health insurance even more valuable.

At a time of national debate over health care, it is useful to understand all the effects of obtaining health insurance. There is the immediate goal of improving individuals’ physical health. Some studies that have examined this question have found that health outcomes do indeed improve, often dramatically.6 But that is the beginning, not the end, of the story. Hu, Mazumder, and their co-authors use a range of data sources and economic methods to show that the financial health of new Medicaid enrollees, and by implication their financial security, improves in ways that have a real impact on their lives.

1 Barack Obama, 2016, “Remarks by the President on the Affordable Care Act,” Miami Dade College, Miami, Florida, October 20, available online.

2 Consumer Financial Protection Bureau, 2014, “CFPB spotlights concerns with medical debt collection and reporting,” press release, Washington, DC, Dec. 11, available online.

3 Luojia Hu, Robert Kaestner, Bhashkar Mazumder, Sarah Miller, and Ashley Wong, 2018, “The effect of the Affordable Care Act Medicaid expansions on financial well-being,” Journal of Public Economics, Vol. 163, July, pp. 99–112. Crossref

4 Katie Thomas, 2019, “Express Scripts offers diabetes patients a $25 cap for monthly insulin,” New York Times, April 3, available online.

5 Sarah Miller, Luojia Hu, Robert Kaestner, Bhashkar Mazumder, and Ashley Wong, 2018, “The ACA Medicaid expansion in Michigan and financial health,” National Bureau of Economic Research, working paper, No. 25053, September. Crossref

6 Sarah Miller, Sean Altekruse, Norman Johnson, and Laura R. Wherry, 2019, “Medicaid and mortality: New evidence from linked survey and administrative data,” National Bureau of Economic Research, working paper, No. 26081, July. Crossref