The global economy has reached record levels of indebtedness, to the concern of researchers and policymakers. On the one hand, debt can be beneficial by smoothing out consumption and accelerating capital accumulation, and thus contributing to economic output. On the other hand, rising debt increases debt service costs and can potentially expose countries to financial risks and lower output. In particular, a large expansion of debt can be associated with a significant economic contraction that can last for years.

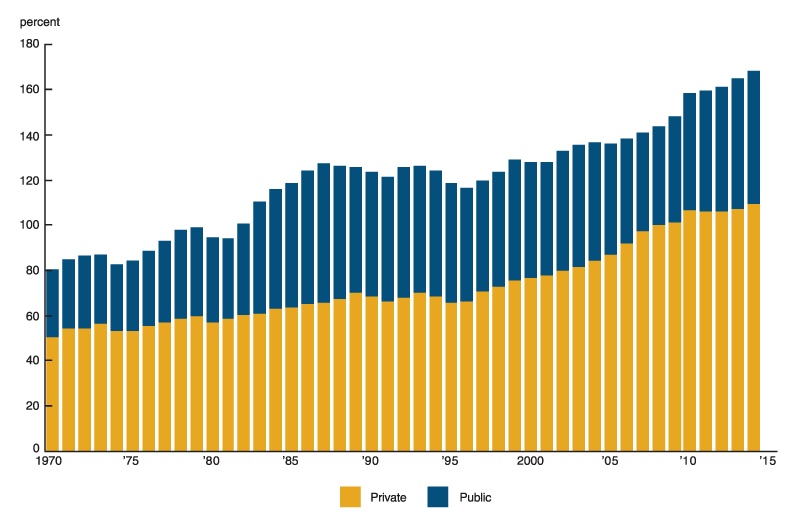

Global debt as a share of gross domestic product (GDP) has been on an upward trend for decades (see figure 1). Rising debt levels are occurring across developed and developing countries in both the public and private sectors. Despite the overall global trends, patterns of debt vary by sector and a country’s level of economic development.1 For example, in the private sector—comprising firms and households—developed countries borrow significantly more than developing countries. Public (government) sector debt relative to GDP is also higher in developed economies. Nevertheless, public sector debt in developing countries accounts for a disproportionately larger share of total debt than in developed countries. Also, foreign debt represents a larger share of total debt in developing economies.

1. Global debt to GDP

Sources: International Monetary Fund, Global Debt Database and Historical Public Debt Database.

In their paper, “The relationship between debt and output,” Yun Jung Kim and Jing Zhang study the dynamic interaction between debt and output over more than four decades.2 The authors consider whether various types of debt relate to economic output in dissimilar ways. For example, the researchers ask, will future output respond to a public sector debt shock the same way it responds to a private sector debt shock? Moreover, they examine how the relationship between debt and economic growth varies depending on a country’s level of economic development, debt financing sources, and exchange rate regime.

There is an extensive literature on the relationship between debt and output and its implications. A study by Reinhart and Rogoff (2010) shows that public sector debt of more than 90% of GDP is associated with notably slower economic growth.3 Other studies have yielded mixed results when attempting to identify the impact of corporate and household debt on output.4 A study by Bernardini and Forni (2017) that focuses exclusively on emerging economies concludes that both private and public sector debt buildup worsens the intensity and duration of economic recessions.5

There is also a considerable literature on the implications of external debt burdens on growth in developing countries. Notably, high external debt levels occurred during the Latin American public debt crisis in the 1980s and the Asian financial crisis of 1997–98 (driven by the private sector’s high exposure to foreign debt). A study by Pattillo, Poirson, and Ricci (2002) indicates that in a country with average levels of external debt, the doubling of external debt relative to GDP will lower the annual GDP growth rate by 0.5 to 1 percentage points.6 Other studies find that the impact of foreign debt on economic output depends on the effectiveness of macroeconomic policies and the degree that debt is transformed into investment.7

Modeling debt and economic output

Kim and Zhang’s research relies on examining the impact of debt shocks on output as well as the reverse relationship—that is, output shocks on debt. These shocks reveal themselves in significant changes in output and debt levels observed in the data, which are brought about by unpredictable economic events. Examples of output shocks include the Organization of the Petroleum Exporting Countries (OPEC) oil embargo in the early 1970s and the Covid-19 pandemic, while long-term credit and liquidity shocks fueled the Great Recession of 2008–09. In response to such shocks, two key components of GDP—investment and consumption—play an important role in influencing the dynamic relationship between debt and economic output.

As a first stage of Kim and Zhang’s analysis, they test the relationship between the total debt-to-output ratio and output across developed and developing countries using a standard model first proposed by Aguiar and Gopinath (2007).8 Total factor productivity (TFP) shocks are the driving force behind both output and debt dynamics in this simple (“frictionless”) model, which does not distinguish between types of debt. Aguiar and Gopinath argue that the difference in underlying TFP shocks across developed and developing countries leads to their contrasting patterns in business cycles. Specifically, shocks are mainly on transitory components of TFP in developed countries but are mostly on permanent components of TFP in developing countries.

Next, the authors test the relationship between debt and output using a data-driven predictive technique (vector autoregression or VAR). They rely on data from 72 developed and developing countries for the period 1970–2014.9 With the understanding that “not all types of debt are created equal,” the VAR approach allows them to examine the connection between debt and output in particular sectors: households, firms, and government. They also study the debt-output association in terms of whether the debt is domestically or externally financed and how it relates to a country’s level of economic development and its exchange rate regime.

Research findings: Standard model versus VAR

Based on the authors’ empirical work employing VAR, they discover two important findings that run counter to those predicted by the standard model. First, they demonstrate that following a debt shock, output declines in both developed and developing countries, while the standard model predicts higher output for both country groups. Second, they show that a positive output shock leads to a decline in debt for developing countries lasting several years, while the standard model predicts a multiyear expansion of debt in developing countries. (In both the standard model and the VAR, a positive output shock leads to a relatively large decline in debt in developed countries.) The authors discuss that the discrepancies between the results from the VAR and the standard model highlight the importance of capturing relevant factors in the data made possible using VAR through its ability to pick up real-world rigidities (frictions), which are absent in the standard model.

Sectoral findings

Kim and Zhang show by using VAR that the relationship between debt and output varies substantially by sector. In response to a positive output shock, public debt declines in both country groups, while private debt (firm and household) rises. By contrast, a private debt shock decreases future output in both country groups, while a public sector debt shock decreases output in developed countries and increases output in developing ones. In terms of magnitude and duration, a shock to private debt, rather than public debt, has a greater impact on output growth in both country groups. Furthermore, the outcome of a debt shock on output depends on the origin of the debt (household or firm) and a country’s level of economic development. Given the mixed results across sectors and country groups, the authors suggest that it is important to distinguish between public and private debt when analyzing the connection between debt and output.

The dynamic relationship between output and debt is also influenced by a country’s exchange rate regime. For example, the authors demonstrate that a rise in private sector debt (both firm and household) does not negatively affect output in countries with a floating exchange rate, while the effect of private debt on output was large over the medium term in countries with a fixed exchange rate regime.

Furthermore, the link between debt and output is influenced by whether the debt is from domestic or foreign sources. Kim and Zhang find that a shock to foreign debt tends to have a greater suppression effect on output than does a shock to domestic debt in both developed and developing countries. Since foreign debt is typically denominated in foreign currency, the exchange rate regime a country uses influences how debt affects output. When a country has a floating exchange rate, a shock to either domestic or foreign debt has a minimal impact on output. However, in countries with a fixed exchange rate, a foreign debt shock can expose countries to severe economic contractions and currency crises.10 Thus, having a fixed exchange rate system has large implications for countries holding foreign debt.

Conclusion

Given the ramifications of indebtedness for global growth, researchers and policymakers are keenly interested in the mechanisms underlying the linkages between debt and economic output. Kim and Zhang find strikingly different results using the VAR methodology as compared to the standard model. A key finding is that a debt shock adversely affects future economic output, and the impact is most pronounced in developing countries and in countries with a fixed exchange rate regime. This information and related results from the study are useful for policymakers considering appropriate levels of debt as well as an exchange rate regime that is most conducive to economic growth. Another important finding is that the way debt affects economic output depends on the sector, suggesting the importance of separating public debt from private debt when undertaking future empirical studies.

Notes

1 Total debt as a share of GDP is growing much faster in developed countries than in developing countries (the average annual growth rates for the period 1970–2014 are 3.8% and 1.9% for developed and developing countries, respectively). Moreover, on average, developed countries have double the total debt as a share of their output as compared to developing countries.

2 Yun Jung Kim and Jing Zhang, 2020, “The relationship between debt and output,” Federal Reserve Bank of Chicago, working paper, No. 2020-30. Crossref

3 Carmen M. Reinhart and Kenneth S. Rogoff, 2010, “Growth in a time of debt,” American Economic Review, Vol. 100, No. 2, May, pp. 573–578. Crossref

4 See, for example, 1) Moritz Schularick and Alan M. Taylor, 2012, “Credit booms gone bust: Monetary policy, leverage cycles, and financial crises, 1870–2008,” American Economic Review, Vol. 102, No. 2, April, pp. 1029–1061, Crossref, and 2) Stephen G. Cecchetti, M. S. Mohanty, and Fabrizio Zampolli, 2011, “The real effects of debt,” Bank for International Settlements, working paper, No. 352, September, available online.

5 Marco Bernardini and Lorenzo Forni, 2017, “Private and public debt: Are emerging markets at risk?,” International Monetary Fund, working paper, No. WP/17/61, March. Crossref

6 Catherine Pattillo, Hélène Poirson, and Luca Ricci, 2002, “External debt and growth,” International Monetary Fund, working paper, No. WP/02/69, April. Crossref

7 For example, see 1) Muhammad Ramzan and Eatzaz Ahmad, 2014, “External debt growth nexus: Role of macroeconomic policies,” Economic Modelling, Vol. 38, February pp. 204–210, Crossref, , and 2) Xuan Changyong, Sun Jun, and Yan Chen, 2012, “Foreign debt, economic growth and economic crisis,” Journal of Chinese Economic and Foreign Trade Studies, Vol. 5, No. 2, pp. 157–167, Crossref.

8 Mark Aguiar and Gita Gopinath, 2007, “Emerging market business cycles: The cycle is the trend,” Journal of Political Economy, Vol. 115, No. 1, February, pp. 69–102. Crossref

9 The authors’ large panel data set comprises 21 developed and 51 developing countries. The source of the GDP (output) data is the World Bank’s World Development Indicators database; debt statistics are from 1) the International Monetary Fund’s Global Debt Database and Historical Public Debt Database, and 2) the database published in Philip R. Lane and Gian Maria Milesi-Ferretti, 2007, “The external wealth of nations mark II: Revised and extended estimates of foreign assets and liabilities, 1970–2004,” Journal of International Economics, Vol. 73, No. 2, November, pp. 223–250. Crossref

10 High domestic debt with a fixed exchange rate regime does not carry these same risks to output.