Monetary Goals and Strategy

Introduction

Thank you Dimitri. Before proceeding with my comments today, I need to remind you that the views I express are my own and are not necessarily shared by my colleagues on the Federal Open Market Committee (FOMC) or within the Federal Reserve System.

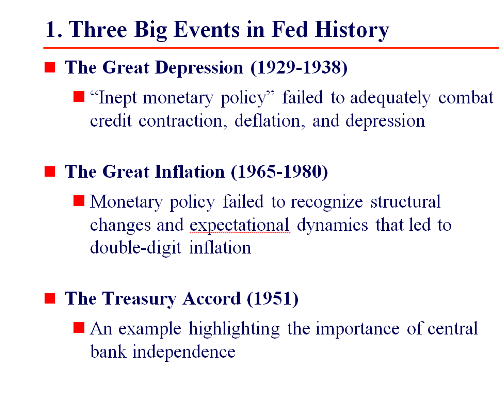

The U.S. Congress created the Federal Reserve System 100 years ago, largely as a way to provide an elastic currency that could mitigate the banking panics and other disruptions that impaired economic activity and contributed to deflations in the late 1800s and early 1900s. That mission has evolved into what is now known as our dual mandate — the Federal Reserve’s directive to help foster conditions that achieve both stable prices and maximum employment. Over the Fed’s 100 year history, three major historical episodes continue to provide lessons for today (chart 1). First, in the 1930s, the U.S. economy experienced a severe credit contraction and deflation during the Great Depression. Milton Friedman and Anna Schwartz argued persuasively that inept monetary policy failed to combat these destructive deflationary forces.1 Second, in the 1970s, U.S. monetary policy tried to do too much to stimulate growth and reduce unemployment when unrecognized structural factors stood in the way. Overly accommodative policy led to soaring rates of inflation. Third, the Treasury Accord of 1951 reminds us that an essential feature of good monetary policy is an independent central bank — one that is autonomous enough to make tough policy decisions. But, democratically elected authorities don’t just grant autonomy to unelected central bankers, nor should they. The price of autonomy is accountability. In order to maintain autonomy, we need to say what we are trying to accomplish and then honestly evaluate our progress in a way that the public and their representatives can judge clearly.

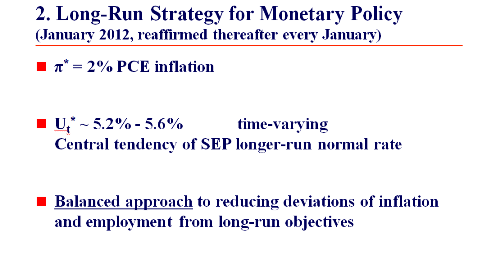

The FOMC has recently made great strides in this direction by explicitly expositing a strategy that reflects the three key lessons of its history. The Committee’s “Statement of longer-run goals and monetary policy strategy"2 was first made in January 2012 and has been reaffirmed each year since (chart 2). In it, the Committee indicates that price stability is understood to mean 2 percent inflation in the long run as measured by the annual change in the price index for total personal consumption expenditures (what we refer to as the PCE price index.) The 1930s’ deflation and the 1970s’ double-digit inflation clearly indicate that the nation is well-served by the Fed having a long-run inflation objective and making sure it achieves that objective within a reasonable period of time.

The employment mandate is more nuanced. Because maximum employment is determined by nonmonetary factors that affect the structure of the labor market, we can’t have a simple, time-invariant goal. We do, however, project where we think the longer-run normal, or “natural rate,” of unemployment is currently. Today, our estimates for this rate generally range between 5.2 percent and 5.6 percent. Such assessments can vary over time. However, the most important determinants of the natural rate change only slowly, so today’s assessment is an important input into policy. Being explicit about it contributes greatly to our accountability.

A clear articulation of the FOMC’s goals and an explanation of how it views its policy misses and plans to correct them help the public better anticipate the Fed’s policy actions. In turn, the public’s improved understanding of FOMC policy actions increases their efficacy by reducing uncertainty over future financial conditions and how those actions might evolve with changes in the economic environment. So, what we clearly need is a scorecard that communicates our accountability in a straightforward manner.

Keeping Score When There Are Two Goals

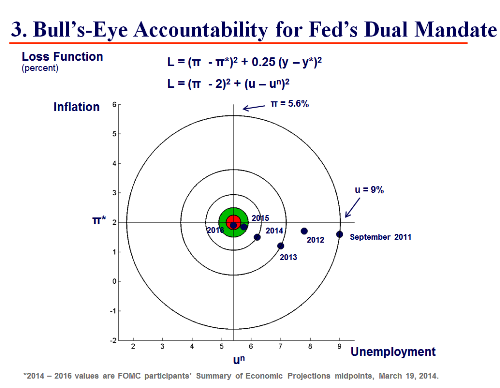

I like to illustrate our balanced approach to achieving our dual-mandate goals with what I refer to as a bull’s-eye scorecard (chart 3). The bull’s-eye in the center illustrates where we would like to be. In this case, the goals are 2 percent inflation over the medium term and unemployment at its natural rate, taken here to be 5-1/4 percent, which is my long-run projection. The scorecard shows an equal weighting of policy misses around our inflation and unemployment objectives; that is, each circular ring is a collection of unemployment and inflation rates that should be equally uncomfortable for FOMC participants.3 For example, it tells us how the 9 percent unemployment rate we faced back in September 2011 can be depicted in “inflation-loss equivalent units” by showing the inflation rate that gives an equivalent loss when unemployment is at its sustainable rate. The answer is 5-1/2 percent inflation! The greater the distance the circle is from the center of the target, the greater are our policy misses. And the greater our policy misses, the greater are the social gains from aggressive monetary and other public policy actions to correct them.

The bull’s-eye scorecard approach has three benefits. First, it provides accountability by clearly describing success and failure to achieve our mandated goals. Second, it renders operational the concept of the FOMC’s intent to take a balanced approach in achieving our goals. Third, the bull’s-eye guides the public’s judgment of the FOMC’s likely response to current economic conditions. While we have made considerable progress toward our goals since 2011, we still have some ways to go to reach the bull’s-eye.

Missing on the Full Employment Mandate

That’s certainly clear in the case of our employment mandate. While we’ve made much progress since the onset of the Great Recession when unemployment reached a high of 10 percent, 6.7 percent is still well above the 5-1/4 percent rate I think is the longer-run normal. Indeed, 6.7 percent is higher than the 6.3 percent peak unemployment rate in the previous recession.

Moreover, we have to ask ourselves if this gap is a good measure of the current degree of slack in the labor market. For example, some of the decline in the unemployment rate over the past four years reflects people dropping out of the labor force instead of finding jobs. Of course, certain demographic factors such as the increasing number of baby boomers reaching retirement age mean we should have expected to see a substantial drop in labor force participation for reasons unrelated to cyclical job prospects and the health of the labor market. But, when you take a detailed look, it appears that the labor force participation rate has recently declined more than can be accounted for by demographic trends and other such structural factors alone. In addition, the end of extended unemployment insurance benefits and other factors likely have decreased the natural rate of unemployment that is our target. So, the decline in the unemployment rate likely overstates to some degree the reduction of slack in the labor market over the past year.

This discussion illustrates how difficult it is to judge where the labor market stands relative to our full employment mandate. A while back, this wasn’t such a critical issue: When the unemployment rate stood at 9 or 10 percent, it obviously far exceeded the natural rate of unemployment. Now, as the unemployment rate falls closer to its natural rate, disentangling structural from cyclical changes becomes more important. Thus, at this juncture, it is prudent to consider a wide range of indicators of labor market activity to better gauge the overall health of the labor market. In the press conference following the March FOMC meeting, Chair Janet Yellen indicated that, in addition to focusing on the official unemployment rate, the Committee considers a wide range of data in assessing labor market conditions.4 These include quit rates, layoffs and a variety of wage measures, as well as broader measures of unemployment that include discouraged workers and those who would like to work more hours.5 Generally, the evidence points to a still weak labor market. We still have some ways to go to reach our employment mandate.

Below Target on 2 Percent Inflation Goal, Too

Let’s now turn to our price stability mandate. No one can doubt that we are undershooting our 2 percent target. Total PCE prices rose just 0.9 percent over the past 12 months; that is a substantial and serious miss. And, as the bull’s-eye chart shows, this undershooting has persisted for several years. Compounding these difficulties, below-target inflation is a worldwide phenomenon and it is difficult to be confident that all policymakers around the world have fully taken its challenge onboard. Persistent below-target inflation is very costly, especially when it is accompanied by debt overhang, substantial resource slack, and weak growth.

In the United States, the challenge of below-target inflation continues to be underappreciated in public commentary. Mistakenly, many greatly exaggerate the risks of overly high inflation. Before turning to inflation risks, let me mention one reason for some confusion. That is, some commentaries minimize the current below-target inflation experience by citing the slightly higher increases of the Consumer Price Index, or CPI. The CPI is the best-known single measure of inflation, and its underlying trend currently is running at a bit above 1-1/2 percent. Many commentators compare the CPI against our 2 percent inflation objective. Unfortunately, this is an apples and oranges comparison: The CPI tends to run about a quarter to a half of a percentage point higher on average than the PCE index because of its different market-basket composition and statistical construction. Accordingly, it is much more accurate to describe the Fed’s inflation objective in terms of the CPI to be roughly 2-1/2 percent. So, against this 2-1/2 percent benchmark, CPI inflation also is quite low relative to target. In any event, the PCE price index is the preferred inflation measure on a number of theoretical grounds and the one chosen by the FOMC as its policy target; therefore, we should judge the Committee’s ultimate inflation performance using that index relative to its 2 percent goal.

So, what is the inflation outlook in the current environment? Despite current low rates, I still often hear people say that higher inflation is just around the corner. I confess that I am somewhat exasperated by these repeated warnings given our current environment of very low inflation. Many times, the strongest concerns are expressed by folks who said the same thing back in 2009 and then in 2010 and, well, you get the picture. OK, five years later we still need to carefully assess this very serious question. Let me offer five reasons why I still see the economic environment as pointing to below-target inflation for several years.

First, many commentators see rising commodity prices as a harbinger of rising inflation pressures. Certainly, back in 2008 and 2010 there were instances when energy and commodity prices rose to high levels. This put pressure on inflation and also reduced aggregate demand. There is a lot of evidence that these types of relative price increases result in only transitory increases in consumer price levels.6 At the moment, even these transitory upward pressures are absent, and the current weak state of global demand contributes to downward pressures. Until something unexpected, and frankly positive, happens with the world economy, commodity prices seem like an even more unlikely propellant for strongly rising inflation than they usually would be.

Second, some say a classic warning sign of inflation is the enormous size of the Fed’s balance sheet and the greater than $2.5 trillion of excess reserves sitting on commercial banks’ books. Surely, they say, enormous increases in the monetary base are likely to be accompanied by substantial price level increases. The problem with this story is that the banks have not been lending these reserves nearly enough to generate big increases in broad monetary aggregates. And even if they did, as an indicator of inflation, the monetary aggregates lost their predictive content many decades ago. The evidence, again, is that inflation remains low. But what if? What if lending picks up? Well, that would be really terrific. Dramatically higher bank lending would surely be associated with higher loan demand and a generally stronger economy. Strong growth and diminishing resource slack would be part of this story, and a rising rate environment would be a natural force diminishing the rising inflation pressures. In the meantime, monitoring the entire state of the economy along with inflation seems like a sensible and appropriate safeguard against this currently low probability scenario.

Third, another potential source of inflationary pressures would be rising inflation expectations. Here, I mean a breakout of inflation expectations separate from any fundamentals that might accompany the previously discussed cases of rising commodity prices and stronger bank lending. One could think of this as the spontaneous combustion theory of inflation. The story goes like this: Households and businesses simply wake up one day and expect higher inflation is coming without any further improvement in economic fundamentals. Without appealing to esoteric economic theories of sunspots, these expectations don’t seem sustainable in the current environment. Higher inflation expectations would presumably get priced into higher bond-market yields and higher financing rates generally. Until inflation actually rises — remember, this story has expectations rising first — ex post real interest rates would be higher and that would presumably result in a higher debt burden for borrowers. This would reduce aggregate demand. Lower demand and lower growth would further reduce cost pressures, strongly suggesting that higher inflation expectations would not be ratified by inflation experience, and thus, would not be sustained. Frankly, this story just seems very unlikely.

Fourth, another more direct measure of potentially rising costs and hence inflation might be stronger wage growth. The economic story here is a bit involved. Most economic research indicates that rising wages are not a leading indicator of rising inflation, so wages are rarely an early warning signal for future inflation. However, higher inflation would lead to higher nominal wage growth. And the double-digit inflation experience of the 1970s suggests that inappropriately accommodative monetary policy can amplify rising cost pressures, creating a wage–price spiral. Clearly, unsustainably strong nominal wage increases would very likely be symptomatic of rising inflation pressures. In terms of the current situation, there is good news and bad news. The good news is that currently, wage increases are low and not symptomatic of high inflation. The bad news is that, currently, low wage increases are symptomatic of weak income growth and low aggregate demand. Stronger wage growth would likely result in more customers walking through the doors of business establishments and leading to stronger sales, more hiring and capacity expansion. During a normal and steady-growth business expansion, nominal wages would typically grow at the rate of productivity expansion plus compensation for inflation. If normal productivity growth is 1.5 percent and inflation is at our 2 percent target, this would suggest a steady labor compensation increase of 3-1/2 percent is sustainable without building inflation pressures. At today’s 2 to 2-1/4 percent compensation growth rates and labor’s historically low share of national income, there is substantial room for stronger wage growth without inflation pressures building.

Fifth, do we really know that the public’s expectations are for low inflation? Judging by today’s Treasury yield curve, inflation expectations remain below our target. If anyone was expecting inflation to accelerate in the future, surely individual and institutional investors would demand to be compensated for growing inflation risk. However, our Chicago Fed affine term-structure model implies that the three-year-ahead average inflation expectations priced into the Treasury yield curve currently are below 2 percent and remain so for quite a number of years to come. Given today’s unacceptably low inflation environment and the wealth of inflation indicators that point to continued below-target inflation, I think we need continued strongly accommodative monetary policy to get inflation back up to 2 percent within a reasonable time frame. After all, notice that the red and green regions of the bull’s-eye chart show modest inflation above 2 percent is much more acceptable than even 6 percent unemployment. The FOMC should be anxious to get to that bull’s-eye region as quickly as feasible given the long slow path to date.

The Fed’s Reaction Function

I’ve spoken so far about how we are missing on our policy objectives. Obviously, the aim of policy is to eliminate those misses. How do we hit the bull’s-eye? What do we do operationally in terms of policy tools? In normal times, the FOMC moves it’s traditional policy tool, the federal funds rate, in order to influence aggregate demand and with it economic growth and inflation and disinflationary pressures.

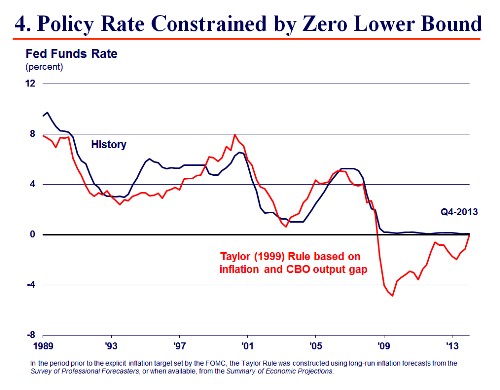

Many economists have studied the relationship between actual Fed actions and sensible, explicit policy rules that might capture the Fed’s policy reaction function (chart 4). Historically, Fed policy moves have been reasonably well described by simple policy rules, particularly the 1999 version of the so-called Taylor rule,7 that relate the federal funds rate to the differences of output (a proxy for employment) and inflation from their target levels and a constant term that is meant to capture the equilibrium real interest rate and the Fed’s inflation target. However, this rule does not always describe policy well. For example, given judgmental, but reasonable, choices for the Fed’s inflation objective before it adopted a 2 percent objective, the Taylor rule misses during the 1990s are big. Actually, in some cases they were bigger than those associated with the well-known and loud complaints lodged by John Taylor against the Fed for its 2003–06 deviations from the rule.8

Why do these misses occur? Well, the economy and the policies that optimally close deviations from our goals are more complicated than what can be captured by any simple rule. Taylor clearly recognized this in his 1993 article in which he stated: “While the analysis of these issues can be aided by quantitative methods, it is difficult to formulate them into a precise algebraic formula. Moreover, there will be episodes where monetary policy will need to be adjusted to deal with special factors. For example, the Federal Reserve provided additional reserves to the banking system after the stock-market break of October 19, 1987, and helped to prevent a contraction of liquidity and to restore confidence. The Fed would need more than a simple policy rule as a guide in such cases."9

In fact, during the most extraordinary times, such as the 2008 financial crisis and its aftermath, the Taylor rule completely breaks down. Its prescription would have been to set policy rates at something like –5 percent in 2009. Such rates are just not feasible for the simple reason that nominal interest rates cannot go below zero; that is, rates cannot breach what we refer to as the zero lower bound, or ZLB. Moreover, there is no emergency handbook that comes with the rule that says what to do in this event. An apparently unstated branch of the Taylor 1993 rule includes setting the federal funds rate to zero during these circumstances and then simply waiting and presumably smiling confidently in public while holding to zero rates. As a rigid policy prescription, we are thus left with inaction. And inaction looks like policy abdication because we are left doing nothing to try to make timely progress in reducing policy misses. This rule cannot be the be-all and end-all for monetary policy; for a policy rule that some say should be enshrined in the Federal Reserve Act explicitly to govern the implementation of U.S. monetary policy, its prescriptions under the recent circumstances we’ve faced are an absolute failure.

Furthermore, given that the Taylor rule has failed so badly and done so for so long, how can we be confident that its prescriptions will still be a good policy to follow once the rule says that the fed funds rate should rise above zero again? Indeed, that’s what many versions of the Taylor rule say today — that it’s time now to begin to increase the fed funds rate. How can we know if the policy prescriptions are from a reborn and healthy policy tool or perhaps instead from one still suffering from a zombie-like hangover in terms of its prescriptions?

It’s important to keep in mind that the Taylor rule’s theoretical underpinnings are loose, especially compared with the seminal 1979 John Taylor article10 on optimal monetary policy in a rational expectations model with sticky prices. Indeed, the Taylor rule parameters are not necessarily stable. In particular, consider the intercept term. The usual specification of the rule assumes that this intercept term is a constant 2 percent equilibrium level of the real interest rate. However, it is well known that equilibrium real rates of interest are not constant, and modern macroeconomic models of optimal monetary policy all take this into account. Assuming that the equilibrium real interest rate is constant is just as egregious an error as failing to account for the time-varying nature of the natural rate of unemployment. We all know that mis-specifying the natural rate of unemployment can lead to seriously inappropriate monetary policy outcomes like double-digit inflation in the 1970s. It certainly seems that the fallout from the financial crisis and persistent headwinds holding back economic activity are consistent with the equilibrium real interest rate being lower than usual today. Indeed, if you put any weight whatsoever on the secular stagnation hypothesis that Larry Summers and Paul Krugman have described,11 an appropriate analysis would recognize lower expected real rates of interest. In any event, the FOMC’s latest policy statement in March recognizes this possibility of lower real rates, as the Committee stated it currently anticipates that “even after employment and inflation are near mandate-consistent levels, economic conditions may, for some time, warrant keeping the target fed funds rate below levels the Committee views as normal in the longer run.”12

Conclusion

During Ben Bernanke’s eight years as Fed Chair, the FOMC worked hard to make the Fed’s policy intentions clear; and I am confident that the FOMC under Chair Yellen will continue along this same path. When the federal funds rate got stuck at zero and goal-oriented monetary policy said to do more, we did more! We implemented the following: the first quantitative easing program, or QE1, in March 2009;13 QE2 in fall 2010; the initial forward guidance on the federal funds rate in August 2011; Operation Twist in fall 2011; the open-ended QE3 in fall 2012; and the enhanced threshold forward guidance in December 2012. All of these were ways to go beyond the policy inaction that was the prescription of simple constrained policy rules, and do something to meet our policy mandates.

In conclusion, let me ask again, what is the accountability test? Much has been done; however, looking at the bull’s-eye scorecard, I would argue, if anything, the FOMC has been less aggressive than the policy loss function calls for. And to me, in the current circumstances, accountability and optimal policy mean we should be maintaining a large degree of accommodation for some time. Policies that would instead place us on a slow glide path toward our targets undermine the credibility of our claim that we will do our job and meet mandated policy goals in a timely fashion. Timid policies would also increase the risk of progress being stymied along the way by adverse shocks that might hit before policy gaps are closed. The surest and quickest way to reach our objectives is to be aggressive. This means, too, that we must be willing to overshoot our targets in a manageable fashion. Such risks are optimal if the outcome of our policy actions implies smaller average deviations from our targets over the medium term. We should be willing to undertake such policies and clearly communicate our willingness to do so.

Notes

1 Friedman and Schwartz (1963).

2 Federal Open Market Committee (2014c).

3 Putting equal weight on (squared) inflation and unemployment deviations is reasonably standard. Given Okun’s law, this is equivalent to a formulation that weights inflation deviations four times more heavily than output deviations. In his seminal 1979 analysis, John Taylor noted that any heavier weight on inflation would reflect “extremely uneven concerns about inflation.”

4 Federal Open Market Committee (2014b).

5 For example, the broadest measure of the unemployment rate, U-6, includes those workers who are marginally attached and those working part-time for economic reasons.

6 Evans and Fisher (2011).

7 Taylor (1999).

8 See, for example, Taylor (2013).

9 Taylor (1993), p. 197.

10 Taylor (1979).

11 See Summers (2013) and Krugman (2013).

12 Federal Open Market Committee (2014a).

References

Board of Governors of the Federal Reserve System, 2013, “What are the Federal Reserve's large-scale asset purchases?,” Current FAQs, December 19.

Federal Open Market Committee, 2014a, press release, March 19.

Federal Open Market Committee, 2014b, Transcript of Janet Yellen press conference, March 19.

Federal Open Market Committee, 2014c, “Statement on longer-run goals and monetary policy strategy,” as amended January 28.

Evans, Charles L., and Jonas D. M. Fisher, 2011, “What are the implications of rising commodity prices for inflation and monetary policy?,” Chicago Fed Letter, Federal Reserve Bank of Chicago, No. 286, May.

Friedman, Milton, and Anna J. Schwartz, 1963, A Monetary History of the United States, 1867–1960, Princeton, NJ: Princeton University Press.

Krugman, Paul, 2013, "Secular stagnation, coalmines, bubbles and Larry Summers," New York Times, opinion pages, November 16.

Summers, Lawrence, 2013, speech, Fourteenth Annual Research Conference in Honor of Stanley Fischer, International Monetary Fund, Washington, DC, November 8.

Taylor, John B., 2013, “A review of recent monetary policy,” testimony before the U.S. House Committee on Financial Services, March 5.

Taylor, John B., 1999, “A historical analysis of monetary policy rules,” Monetary Policy Rules, Chicago: University of Chicago Press, pp. 319-341.

Taylor, John B., 1993, “Discretion versus policy rules in practice,” Carnegie-Rochester Series on Public Policy, Vol. 39, Vol. 1, December, pp. 195–214.

Taylor, John B., 1979, “Estimation and control of a macroeconomic model with rational expectations,” Econometrica, Vol. 47, No. 5, September, pp. 1267–1286.