Solid Economic Growth Expected in 2011 and 2012, According to Chicago Fed Atomotive Outlook Symposium Participants

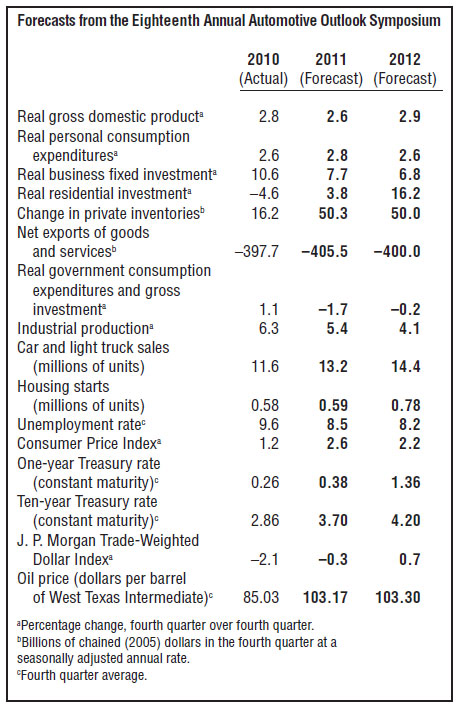

The eighteenth annual Automotive Outlook Symposium was held in Detroit on Thursday and Friday, June 2–3, and drew more than 90 participants from manufacturing, banking, consulting and service firms and academia. This year, 24 individuals provided a consensus outlook—forecasts for major components of real gross domestic product (GDP), as well as several key statistics for the U.S. economy. The median forecast results are presented in the table. According to the median forecast of symposium participants, the nation’s economic growth rate in 2011 is expected to be a bit slower than in 2010, inflation is predicted to rise, and the unemployment rate is anticipated to move lower. The pace of economic growth in 2012 is expected to edge higher, with inflation easing and the unemployment rate continuing to head lower. Real GDP, after having increased 2.8% last year, is forecasted to rise by 2.6% this year and 2.9% in 2012. After rising 1.2% last year, inflation, as measured by the Consumer Price Index, is expected to rise 2.6% this year and then ease to 2.2% in 2012. The unemployment rate, after having averaged 9.6% in the fourth quarter of 2010, is forecasted to fall to 8.5% in the final quarter of 2011 and then move further down to 8.2% in the last quarter of 2012.

Most of the major components of real GDP—particularly consumer spending and business fixed investment—are expected to expand at a solid pace in 2011. The pace of economic growth is forecasted to edge higher in 2012, in large part because of an anticipated expansion in spending in residential investment. Industrial production is forecasted to increase at a strong pace in 2011 and then increase at a solid rate in 2012. Net exports are predicted to remain flat 2011 and 2012. Car and light truck sales are projected to improve in 2011, with sales at 13.2 million units; and they are expected to improve to 14.4 million units in 2012. Interest rates (one- and ten-year Treasury rates) are anticipated to rise this year and next year. Oil prices are expected to average $103 per barrel by the end of 2011 and then remainat that level through the end of 2012. The trade-weighted U.S. dollar is expected to edge lower this year and edge higher in 2012.

A summary of the eighteenth annual Automotive Outlook Symposium will be published in an upcoming special issue of the Chicago Fed Letter.

William A. Strauss • Senior Economist and Economic Advisor • (312) 322-8151