Can Central Counterparties (CCPs) Use Improved Buffers to Reduce Cyclical Funding Demands on the Market?

In this blog post, we investigate changes in margin at CCPs during the market stress of 2020:Q1 to show how reactive CCP funding demands were to the increase in market volatility.

“Save for a rainy day.” This famous old idiom is often used to encourage people to save money in good times in order to better manage through future, unforeseen difficult times. After the global Financial Crisis of 2008–09, the banking regulators at the Basel Committee on Banking Supervision (BCBS) established new guidelines in a similar spirit. BCBS required banks to establish countercyclical buffers1 to guard against procyclicality—or the pattern where banks’ balance sheets are stronger in good times but significantly deteriorate in volatile times. The buffers are excess capital that banks could draw down during periods of market stress. These capital buffers are funded during relatively benign credit cycles and ahead of market stress events, providing a build-up of reserves to deploy during volatile times. During the market stress related to the Covid-19 pandemic, many banking regulators have allowed banks to draw down their buffers in order to absorb potential losses as the credit cycle turned negative and financial markets became more volatile.2

CCPs are financial institutions that guarantee performance of a financial contract—typically the buying and selling of contracts related to securities or derivatives. Although CCPs are different from banks in many ways,3 they also have regulatory requirements to guard against procyclicality. In general, CCPs set funding requirements for two main purposes4—to cover current risk exposures and to cover potential future risk exposures. The main concern with these funding requirements is that CCPs increase funding requirements in times of market stress, potentially exacerbating market liquidity shortages. As part of the lessons learned from the Financial Crisis, procyclicality in funding requirements was identified as a macroprudential concern since it could further exacerbate risks in the financial markets.5 As a result, establishing funding requirements that are less sensitive to volatility is now codified in the Principles for Financial Market Intermediaries (PFMI).6 Despite these regulatory efforts to mitigate large increases in funding demands in times of market stress, a recent Futures Industry Association (FIA) white paper reported that CCP funding requirements increased when market volatility sharply increased in 2020:Q1.

CCPs have two types of funding requirements for clearing members—variation margin and initial margin. I will explain how these operate and how they responded to the market volatility in 2020:Q1.

Variation margin (VM)

VM is the settlement of losses and gains based on the current change in the valuation of the cleared contracts, i.e., VM is a net flow which is passed through the CCP based on losses and gains on cleared contracts. CCPs operate VM cycles daily and often on an intraday basis. In other words, based on the positions of clearing members, they calculate the required increase in variation margin payable to the CCP when the positions deteriorate (or receivable from the CCP when the positions improve in valuation) on a daily basis. The VM process minimizes the need for the CCP to carry debits and credits on its balance sheet. Since VM is driven by changes in positions and prices of cleared contracts held by clearing members, cyclical changes are driven by forces largely outside the control of the CCPs. However, this frequent reconciliation is still a necessary process in order to extinguish credit risk.

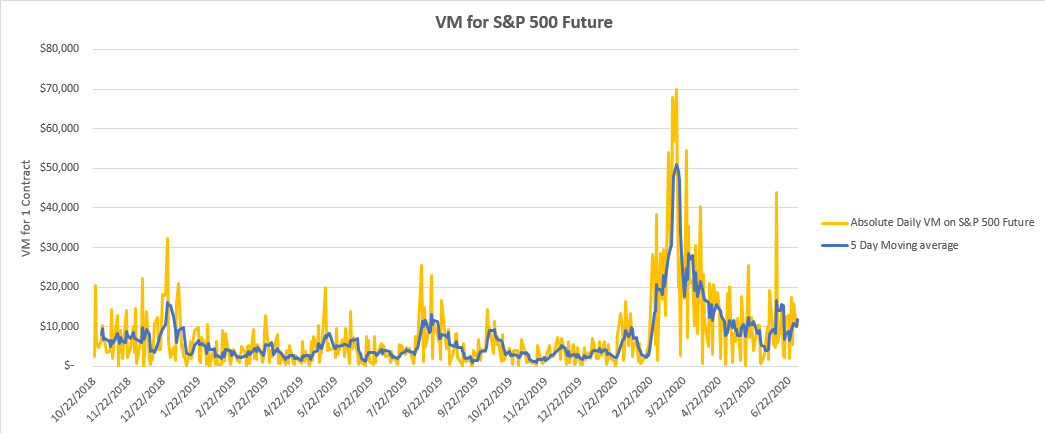

To provide an illustrative example, figure 1 shows the level of variation margin for one S&P 500 future7 contract cleared at the CME from late 2018 to mid-2020. The pattern in the figure shows how VM can fluctuate over time. The VM amounts are shown both as daily amounts and as a moving five-day average for the contract expiring in the nearest month to isolate VM amounts to changes in market volatility. The five-day average helps to show a trend. Both values peak as market volatility increased during March of 2020 in response to the Covid-19 pandemic, denoting large funding demands on CCP clearing members during this time of market stress.

Figure 1. S&P 500 variation margin

Initial margin (IM)

In order to cover future risk exposures, CCPs require collateral to cover the potential loss in the event that a member defaults. The collateral required is held at the CCPs.8 The requirement is referred to as IM and is derived by forecasting future valuation changes of the contracts cleared to a high degree of certainty—99% or higher. To forecast the risk, CCPs use a variety of risk models.9 Within these models, CCPs use techniques to manage procyclicality,10 so that the additional demands for collateral do not increase at the same pace as the increase in market volatility.

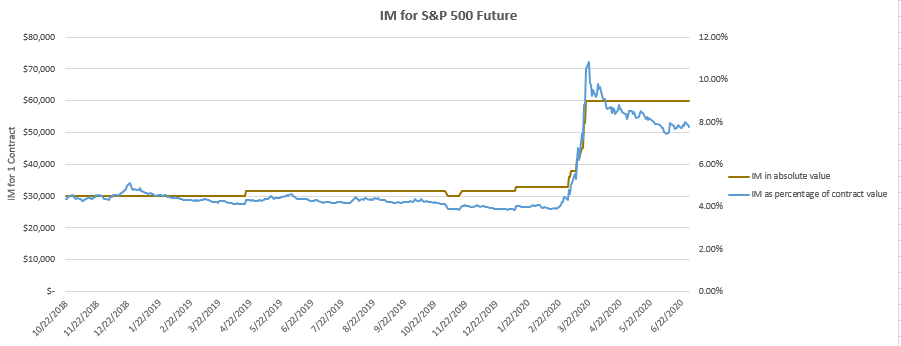

To provide an illustrative example, figure 2 depicts the IM for the same S&P 500 future contract as in figure 1. Unlike VM, the changes in IM are infrequent, because CCPs tend to adjust the IM requirement on a monthly or weekly schedule. Still, there can be ad-hoc changes in anticipation or in reaction to market volatility. Specifically, we can see that as market volatility increased in March of 2020, the IM requirements increased by 81.8% in dollar terms from $33,000 to $60,000 per contract and 108.8% in relative terms from around 4.5% to 9.3% per contract.

Taken together, the IM and VM show intense increases in funding requirements at CCPs during a time of market stress.

Figure 2. S&P 500 initial margin

Aggregate increases in CCP funding demands for IM and VM

Since one contract may not provide a broad enough view of cyclicality of VM or IM during the recent market stress, it is useful to consider aggregate margin data reported by the different CCPs in public disclosures. Table 1 shows the quarterly increase for average VM calls in 2020:Q1 relative to 2019:Q4 at CCPs that are designated as systemically important in the U.S.,11 as well as the quarterly increase in the maximum VM calls in 2020:Q1. Table 2 shows the quarterly increase in aggregate IM required and maximum IM called for a single day at the selected CCPs.

Table 1. Quarterly change in average total VM paid to the CCP and maximum VM

| CCP/Clearing Service | Quarterly change of average VM in Q1:2020 (percent) | Quarterly change of max VM in Q1:2020 (percent) |

|---|---|---|

| CME (all services) | 55 | 50 |

| DTCC Government Securities | 72 | 164 |

| DTCC Mortgage-Backed Securities | 243 | 616 |

| DTCC National Securities Corp | 294 | 411 |

| ICE Clear Credit | 421 | 839 |

Table 2. Quarterly change in total IM and maximum IM called

| CCP/Clearing Service | Quarterly change of IM in Q1:2020 (percent) | Quarterly change on max IM call in Q1:2020 (percent) |

|---|---|---|

| CME Base Product | 75 | 742 |

| CME Interest Rate Swaps | 37 | 721 |

| DTCC Government Securities | 9 | 11 |

| DTCC Mortgage-Backed Securities | 141 | 455 |

| DTCC National Securities Corp | 253 | 291 |

| ICE Clear Credit | 44 | 922 |

| Options Clearing Corp | 70 | 785 |

The tables denote that both levers that CCPs rely upon to demand funding from members increased substantially over the first quarter of 2020. Given that these demands were increasing during a time of market stress, would it make sense for CCPs to require higher collateral (in the form of buffers) during stable times that could be reduced during a period of volatility? Since, as noted above, VM cyclicality is inherent, CCPs would need to set such cyclical buffers on IM. If these buffers were designed with a countercyclical trigger, similar in spirit to the buffers established in banking regulations, the increase in funding required to cover VM payment could be partially offset by decreases in IM buffers. In theory, this could better support liquidity being available during a period of market stress.

However, these buffers would require trade-offs for the market. The buffers could potentially inhibit market depth if participants were less willing to transact due to the higher associated cost of funding. These potential concerns might be abated by CCPs accepting a broader range of high-quality liquid assets to be used as collateral for IM obligations. Still the merits of rainy day funding in the form of buffers could be considered in the context of supporting the broader resilience of the clearing ecosystem.

Notes

* I thank John Spence of the Financial Markets Group for his assistance and Federal Reserve colleagues for their helpful comments.

3 More information available online.

4 For this post, we did not focus on Default Fund contributions, which are assets provided to CCPs to fund a mutualized default pool in the event IM is not sufficient to cover missed VM payments.

6 Details available online, see 3.5.6.

7 Contract is valued at $250 x S&P 500 Index, so an S&P 500 Index level of 3,500 would equate to a contract value of $875,000. Please see additional details online.

8 CCPs may use a third party such as custodian, commercial, or central bank to hold the collateral provided by clearing members.

9 More details and examples available online, see section 5.1.

10 For more details, see LaSalle Street: Financial Markets Insights, podcast No. 2, available online.

11 OCC is not included as they do not separate VM calls in public disclosures since changes in valuations of premium style options are combined with changes in IM.