Detroit’s Revenue Structure: Part 1, Funding Sources

This is the first of two posts on the City of Detroit’s revenue structure. These posts build on the discussion at our recent Project Hometown virtual event, Charting Detroit’s Fiscal Future. In this post, we discuss Detroit’s municipal finances, specifically the city’s general fund, and how its sources of funding have evolved over time, including during the post-bankruptcy period, 2014–19. In a follow-up post, we discuss how the Covid-19 pandemic has impacted—and will likely continue to impact—those revenue sources.

What was Detroit’s fiscal position before the pandemic began in 2020? The bankruptcy process that began in July 2013 had led to debt reduction and reduced payments and obligations to retired city workers, and by 2019, city officials were pointing to improvements in Detroit’s fiscal management. According to the city’s annual fiscal report, “In the five years since bankruptcy, the City has stabilized and strengthened its fiscal position. The City has completed five fiscal years with a balanced budget, increased recurring income tax revenue by 26%, significantly improved property tax collection rate (from 69% to over 83%), and created a budget reserve fund at nearly 10% of annual expenditures.”

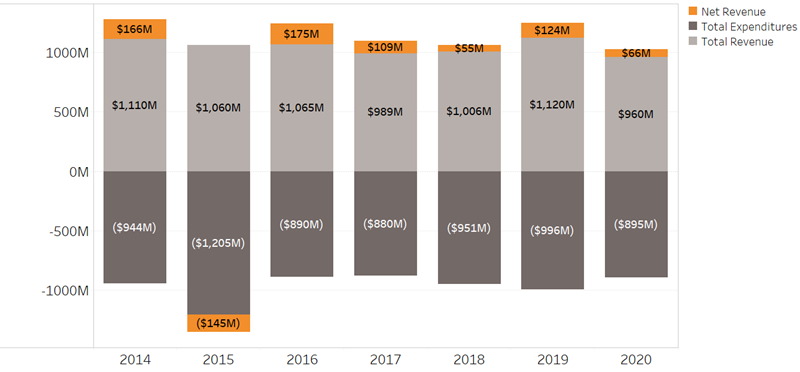

Chart 1 shows recent trends for the City’s general fund revenues and expenditures, reflecting a narrow annual surplus since 2016.

1. Trends for Detroit's Revenues and Expenditures

Note: Detroit's fiscal year begins on July 1 and the State of Michigan's fiscal year begins on October 1, so data for Detroit in 2020 are for the first six months of the year.

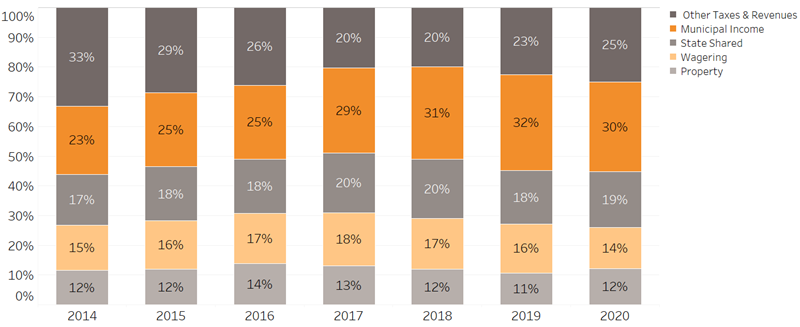

Chart 2 shows the trends in Detroit’s tax revenue structure, reflecting the increasing dependence on the municipal tax as a source of revenue. According to the city’s fiscal report, during FY 2019, Detroit had total revenues of $1.12 billion and total expenditures of $996 million.

The City’s efforts to address its budget issues has had the impact of diversifying its revenue structure. Prior to the 1960s, the city’s revenue sources consisted of state revenue sharing and property taxes. Since then, the city added a municipal income tax in 1962, a utility tax in 1971, and a casino revenue tax in 1999.

In this post, we explore the current structure of the city’s four largest sources of general fund revenue, in order of oldest to newest, to understand their implications for ensuring Detroit’s fiscal health into the future.

2. Detroit's General Fund Tax Revenue Trends

Municipal Income Tax and Wagering Tax represented more than a 40% share of total general fund revenue.

Note: Detroit's fiscal year begins on July 1 and the State of Michigan's fiscal year begins on October 1, so data for Detroit in 2020 are for the first six months of the year. The Other Taxes and Revenues Category represents the sum of additional revenue streams in Detroit's General Revenue Fund not specifically listed.

State revenue sharing

State revenue sharing is currently the city’s second largest source of revenue. The State of Michigan collects a 6% sales tax. One-third is dedicated to the state’s School Aid Fund. Some of the remaining two-thirds is distributed to cities, villages, and townships (CVTs) as revenue sharing. Some of that revenue sharing, called constitutional revenue sharing, is distributed on a bimonthly basis based on a community’s population and sales taxes collected for the prior two months. So if a community’s sales tax and/or population are declining, its total revenue-sharing receipts from the state will also decline.

Another portion of the state’s revenue sharing, statutory revenue sharing, is based on a formula that the state legislature has modified repeatedly. The resulting statutory revenue sharing payments to CVTs are subject to the state’s annual appropriations processes. (For more on the complexities of Michigan’s revenue sharing, see Jill Roof and Miranda Vetter, 2020.)

According to a report from the Michigan Municipal League, the state legislature has tended to direct a growing portion of statutory revenue to the state’s own budgetary needs. “From 2003-2013, sales tax revenues went from $6.6 billion to $7.72 billion. Over that same period, statutory revenue sharing declined from over $900 million annually to around $250 million.” The report further notes that from 2003 through 2013, the state withheld over $700 million in statutory revenue payments from Detroit, in order to balance the state’s books.

As reflected in chart 2, state shared revenue was approximately one-fifth of Detroit’s general fund revenue in FY2020. This share has remained relatively constant since FY2015. However, as referenced above, sustaining (or increasing) this level depends on local conditions, as well as on decisions at the state level.

Property tax

In Michigan, the process for valuing properties and the rates at which they can be taxed are established by state law. In Detroit, these taxes represent the city government’s fourth largest source of revenue—at 12% of the total in FY2020.

Not all proceeds from Detroit property taxes go into the city’s general fund. The Downtown Development Authority (DDA) was created in 1976 to promote and develop economic growth in the city’s downtown business district. The DDA is a legally separate entity. The members of the DDA’s board of directors are appointed by the city’s mayor and confirmed by the Detroit city council, which approves the DDA’s budget. The DDA is financed by proceeds from a one-mill (0.1%) levy on the assessed value of the Downtown Development District and by capturing the tax proceeds on the increases in the assessed value on real and personal property within the district. Between 2015 and 2020, property tax revenue increased from $22.7M to $49.3M (or 117%). Funds raised by the DDA are restricted for use within the tax increment district.

When businesses and residents located outside Detroit’s business district pay their property taxes, they are funding not only the City of Detroit’s general operations and debt obligations, they are also funding Wayne County government, Detroit Public Schools, Wayne County Community College, Detroit Public Library, and the State of Michigan.

According to the Citizens Research Council, “Detroit residents face the highest property tax rate of any city in Michigan with a population over 50,000. ... Although Detroit’s property tax rate of 19.9520 mills [1.995%] for general operations is close to the statutory maximum of 20 mills [2%], Detroit has the third lowest per capita taxable property tax base of Michigan’s largest cities. As a result, Detroit’s property tax revenue per capita tends to be modest compared to other large cities in Michigan, ranking 18th highest of the 24 largest cities.”

Property tax collection was an issue for Detroit before, during, and after its bankruptcy. The failure to properly adjust property values is believed to have contributed to Detroit’s high levels of tax delinquencies, foreclosures, and vacancies.

In 2017, Detroit completed its first city-wide property appraisal in over 60 years. That event focused attention on how Detroit’s residential properties were assessed and taxed over varying time periods and how that had affected Detroit’s extraordinary rates of tax foreclosures. Research indicates that while, as expected, home values in Detroit fell steeply as a result of the city’s subprime mortgage crisis and the recession, tax assessments were not adjusted for the declining values. According to an investigation by The Detroit News, “Detroit overtaxed homeowners by at least $600 million after it failed to accurately bring down property values in the years following the Great Recession.”

Property tax revenue for Detroit has remained relatively stable since 2015. While city officials try to figure out compensation for the admitted failures to adjust assessments, continuing to collect sufficient property tax revenue (including delinquent taxes) is dependent on broader market forces affecting home values in Detroit.

Municipal income taxes

In 1962, Detroit enacted Michigan’s first local income tax that, according to Leonard Bronder (1962), “reduced the strain on the property tax, shifted some of the tax payment away from business, provided a more flexible local tax structure, and was a vehicle for requiring some reimbursement for the services provided… by the core city government” to commuting workers and their families.

The municipal income tax gradually became Detroit’s largest source of revenue. As of FY2019, Detroit levied an income tax of 2.4% for residents, 1.2% for nonresidents, and 2.0% for corporations—the highest income tax rates of any of the cities in Michigan that levy a local income tax.

The city’s municipal tax income revenue stream has become increasingly dependent on its commuter population. Between 2014 and 2019, revenue from Detroit’s municipal income taxes increased by 42%, despite its population declining from 682,669 to 670,031.

Recent reporting highlights the persistence of structural inequities in Detroit’s labor market. Specifically, of the more than 258,000 jobs in Detroit in 2014, “74% were held by employees commuting from the suburbs. In comparison, 108,000, or 61% of employed Detroit residents, had to travel outside the city for their jobs. Roughly 46% of those travel more than 10 miles from home.”

Furthermore, many Detroiters are traveling outside the city to jobs that pay significantly less than jobs within the city. According to research prepared as part of the City of Detroit University Economic Analysis Partnership: “In 2019, the average nominal wage at businesses and government establishments in Detroit was $68,803, while the average wage earned by city residents was barely half that amount, $35,048.” If more of the higher paid local jobs were held by Detroit residents, the impact of taxation at the resident rate would significantly increase municipal income tax revenue.

In 2016, the Corporation for a Skilled Workforce (CSW) produced two reports and a white paper (available here) to support efforts by the newly reconstituted Mayor’s Detroit Workforce Development Board in rethinking how to align the Detroit’s workforce development systems with the needs of Detroit’s residents. As some of the contributors to those reports reported to local media at the time regarding Detroit’s jobs landscape, “The crux of this challenge is that there are too few jobs in the city for its residents and too many barriers to employment.”

In addition to the daily commuters from surrounding suburbs and Windsor, Ontario, in Canada, Detroit’s nonresident income tax also applies to athletes and entertainers performing, competing, and otherwise working at venues throughout the city, including Comerica Park (Tigers), Ford Field (Lions), and Little Caesars Arena (Pistons and Red Wings). In the case of professional sports, the income tax applies to both the home and visiting teams and, in addition to the athletes themselves, includes “coaches, managers, trainers, analysts, assistants, and all other persons that are required to travel with and perform services for the teams.” As Little Caesars Arena was opening in 2017, a news report estimated that annual income taxes raised from the Detroit Piston’s return to Detroit, combined with musical performances anticipated in the new arena, would add $4 million to the city’s annual income tax revenue.

Moving forward, Detroit may face significant financial challenges as local income tax laws clash with the lingering Covid-19 reality of remote work. While the city has increasingly relied on municipal income tax revenue as its largest source of revenue, the city’s income tax is only collected from individuals who are paid for work performed while they are physically in the city, including nonresidents who work in Detroit. Covid-19 restrictions may have increased the demand for remote work among nonresidents who work in Detroit-based companies. As a result, the city must consider important questions, such as: How many remote workers will become permanent telecommuters? And how will that affect municipal income tax?

Wagering tax

In 1996, Michigan voters narrowly approved a measure allowing the establishment of three casinos in Detroit. Between July 1999 and November 2000, three casino licenses were issued and Detroit’s three casinos opened their doors. The “Total City Wagering Tax” is now the city’s third largest revenue source. The amount of tax revenue was smaller in 2020, likely affected by the Covid pandemic. On January 22, 2021, the State officially launched online sports betting. Internet sports betting is taxed at 8.4% of adjusted sports betting receipts. Casinos operated under Native American tribal jurisdiction pay the full 8.4% to the state. Casinos operated outside Native American tribal jurisdiction pay 70% to the state and 30% to the city of Detroit.

The Michigan Gaming Control and Revenue Act defined the uses to which Detroit’s gaming revenue could be directed, including, “public safety, economic development programs, anti-gang and youth development programs, and other programs designed to improve the quality of life in the city.”

Summary

Although Detroit had taken important steps toward fiscal health post-bankruptcy, the city has continued to face headwinds in the form of a declining population, fragile housing stock, significant racial economic disparities, and most recently, the pandemic. Our review of the primary sources of Detroit’s general fund tax revenue reveals that while these funding sources have been relatively stable—at least through the first half of the pandemic—future revenue streams may be negatively impacted by more consumers and workers leaving the city, state-level appropriations decisions, and the volatility of the housing market, among other factors.

In a follow-up post, we will explore the potential impacts of the Covid-19 pandemic on Detroit’s revenue streams.