Assessing the Midwest Floods of 2008 (and 1993)

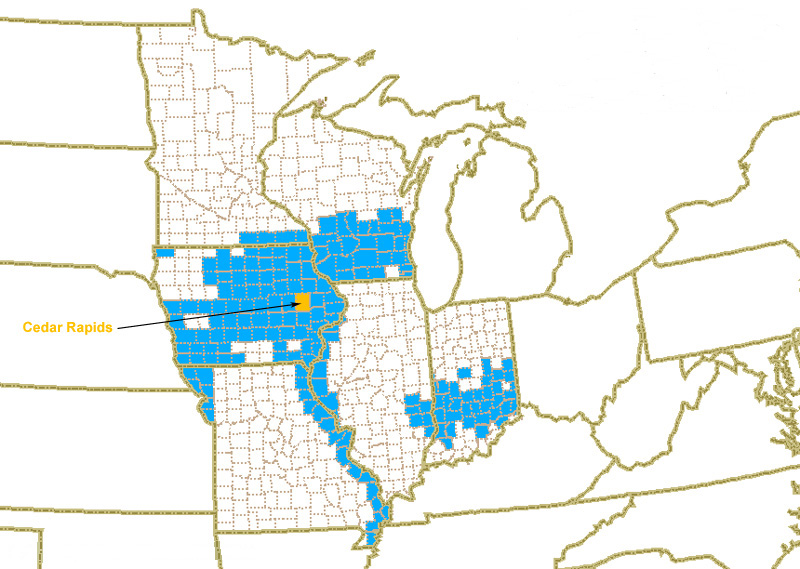

As water levels recede, the region is beginning to take stock of impact from some its worst flooding since 1993. The geographic footprint of this year’s flooding (depicted below) is less extensive than the nine states and 504 counties affected 15 years ago. And as always, an assessment of the short- and long-term impact of this natural disaster on the national and regional economy will be difficult. In this blog, I will look at the effect of natural disasters on economies and contrast current flood conditions with those the region faced in 1993.

1. June 2008 Midwest flooding

Source: Maptitude/FEMA/Office of the Governor of Iowa.

How to think about the losses to the U.S. economy

From a conceptual viewpoint of our economy, natural disasters impact our economic well-being in two basic ways. First, they destroy what we have produced in the past—our “capital stock”—including lives, homes, commercial buildings, public infrastructure and property. Second, they often interrupt normal commercial activity and production. Transportation and deliveries do not take place, people cannot get to work and work places become dysfunctional until normalcy is restored.

In a December 1993 Chicago Fed Letter, Bill Testa, Gary Benjamin and I wrote, “Perhaps the most meaningful definition of economic loss due to a disaster is the value of output of goods foregone—that is, the total net output that would have been produced had it not been for the disaster. Foregone output results for two reasons. First, natural disasters destroy productive capital stock such as roads, bridges and factories, thereby reducing output until such time as the capital stock is restored. Second, natural disasters can interrupt day-to-day business activity.”

As that article points out, the impact of the natural disaster tends to have a somewhat unusual affect on the national income accounts—the official way in which we measure the nation’s economic output and income from quarter to quarter. Following the 1993 floods, estimates for the third quarter reduced personal income by $9 billion and forecasted uninsured losses to be $2 billion. Losses to proprietors’ incomes were estimated at another $1 billion.

Remarkably, such initial losses soon appear to translate into economic gains as business and households rebuild. The rise in construction activity and the resumption of business activity often boost gross domestic product (GDP) estimates for future quarters, as households and businesses attempt to rebuild their physical capital and, in the case of businesses, to fill order backlogs. For example, following Hurricane Andrew, annualized GDP growth hit 5.7% in the fourth quarter of 1992, spurred by rebuilding activities.

However, such rebuilding does not reflect an actual economic gain in the broad long-term perspective. In most cases the rebuilding merely replaces lost capital stock—meaning that, in the long term, the nation’s product will not exceed what would have been produced without the disaster. While the immediate burst of economic activity is quite evident, the losses from the foregone output of interrupted and diminished business activity may go largely undetected because the diminished growth takes place in small amounts spread over many years.

Regional economic losses

The ultimate extent of the damage to the region’s economy will in large part depend on who pays for the rebuilding. If the losses are in large part covered by the national government and insurance companies, and if reimbursement is prompt, the region can conceptually restore output and even increase its levels of economic growth. However, if the 1993 flood experience is a guide, it is more likely that the region will absorb a significant share of the disaster-related cost. Because flood insurance was not extensively used, it was estimated that 15% to 25% of the flood costs were borne by state and local governments, not to mention the costs to uninsured homeowners who were forced to rebuild using their own resources. In the most recent floods, it was estimated that only about 1% of Iowans owned flood insurance. In hard hit Cedar Rapids, only 777 of the 4,000 homes damaged or destroyed by flooding were covered. Despite efforts after the 1993 floods to expand coverage, the cost of the policy and the limits of coverage still deter homeowners from purchasing polices. It is estimated that the average cost of a policy in Iowa is $500 per year with coverage only including direct flood damage and not related damage such as water that enters the house through a backed up basement drain. Even if property owners choose to be fully insured, insurance must be paid for. Thus, residents of these regions do bear at least some of the costs in choosing to live and work in disaster prone areas. Currently $2.7 billion in federal flood relief has been approved to aid 2008 flood victims. This does not include the value of low-interest loans and small business assistance as well as the value of crop insurance and private insurance.

Specific categories of losses–Agriculture

In both floods, the greatest concern focused on flooded crop land. In the 1993 floods, nine million acres were submerged by the flood. The lost acreage had been expected to produce 6% of the region’s harvest that year. The estimated crop losses were $7 billion. The states with the largest percentage loss were Missouri 12%, Minnesota 11%, South Dakota 8% and Iowa 7%. In this year’s flooding, damage is heaviest in Iowa where 2 million to 3 million acres of corn and 2 million acres of soybeans were flooded. The American Farm Bureau estimates crop losses at $8 billion for the region, with $4 billion of the total in Iowa. Other states with significant estimated losses are Illinois ($1.3 billion), Missouri ($900 million), Indiana ($500 million) and Nebraska ($500 million). The Bureau points out that it is not only the flooding that will impact crops but also the excessive rainfall that occurred this year.

A June 30 estimate by the USDA projected this year’s corn harvest to be down from 86.5 million acres to 78.9 million, or 8.7 percent. However, the impact on prices may be softened if a robust corn harvest occurs, since supplies should be sufficient to meet demand for food, feed and ethanol. Following the USDA report, corn futures fell from $7.55/bushel to $7.25/bushel, significantly off the $8/bushel price recorded on the Chicago Board of Trade in the immediate wake of the flooding. Still, this price is significantly elevated over the early June $6/bushel price.

One big difference between this year’s floods and that of 1993 was the preexisting stocks and prices of corn and soybeans. In 1992, a bumper crop had been harvested. For example, the stock-to-use ratio for corn hit 25% in 1992 and even in the flood year of 1993 ended at 11%. While prices rose, the increase was a modest hike from $2/bushel to $2.50/bushel. Today the corn stock-to-use ratio is only 6%; prices spiked accordingly to $8/bushel immediately after the flood before retreating to the current price. This tightness reflects the increasing demand for corn both for export and for ethanol. Given this, even if the number of acres lost is smaller than in 1993, the impact on prices will need to be closely monitored.

Spillover issues into other agriculture markets also need to be considered, as livestock feed prices are affected. The condition of the fields for next year’s planting will need to be assessed as well.

Structures

Given the smaller geographic footprint, the potential cost of rebuilding and the infrastructure loss is considerably less in this year’s flooding. While Cedar Rapids and parts of Iowa City were severally impacted, much of the flooding was contained within sparsely populated areas. In 1993, an estimated 45,000 to 55,000 private homes were destroyed, and between 35,000 and 45,000 commercial structures were damaged. Similar to today, most of the homes did not carry flood insurance, making uninsured losses the most significant issue. Estimated property and nonagricultural losses totaled $5 billion before insurance.

Another difference with the 1993 floods was the damage to infrastructure. In 1993, 1,000 miles of road were closed, and 500 miles of railroad track were underwater. Nine out of 25 non-railroad bridges were damaged and closed. This time, some highways were closed for several days due to flooding but damage to bridges, locks and other infrastructure was limited. The exception of course is in cities such as Cedar Rapids where infrastructure losses in the downtown are extensive. Cedar Rapids had 1,300 city blocks underwater, forcing 24,000 residents to evacuate. Preliminary damage estimates have been placed at $736 million or roughly $6,095 per capita. This must also be placed in the context of disruption to Iowa’s second largest city of over 120,000 people with a 2005 gross metropolitan product of $11.2 billion.

Transportation disruptions

One of the more immediate problems that flooding causes is transportation disruptions. The 1993 floods were so extensive that barge traffic on the Mississippi was halted for 2 months. In contrast, barge traffic is expected to be affected for 3 to 4 weeks this time. By July 5, the entire Mississippi was reopened to navigation. Railway disruptions were also more severe in 1993. The destruction of rail bridges added four days to rail shipping times for several months while this time rail disruption was minimal for almost all major freight lines. The effected lines caused temporary delays of 1 to 2 days for most shipments.

What happens next?

For towns that were most directly affected, the question is, what does the path to recovery look like? Unlike individual farms and factories, cities’ and towns’ economies are composed of complex interrelationships that have developed over many years. A natural disaster can upset, disrupt and even destroy those relationships so that restoration is often impossible and sometimes undesirable. And so, the form of rebuilding may require careful consideration and evaluation.

Following the 1993 event, many communities and individuals simply choose not to rebuild. Other communities used natural disasters to redefine themselves. An interesting example of a town rebuilding after a flood was Grand Forks, North Dakota. The Minneapolis Fed chronicled the rebuilding of Grand Forks in a September 2006 Fedgazette article. Grand Forks was the victim of flooding in 1997. In April of that year, 80% of the town was submerged. By 2006, the area was largely restored with the region’s economy growing at a faster pace than before the flood. This was due largely to the influx of $600 million in federal disaster aid (approximately $10,000 per resident).

After much painful disruption, lengthy deliberation and hard planning, the flood eventually spurred a new vision for the area. Roughly 1,200 homes in the 100-year flood plain were bought out by the Federal Emergency Management Agency as part of a flood protection plan. The population rebound remained slow until the Army Corps of Engineers finalized a flood protection plan in 2000. Once this occurred, a building boom was unleashed. The city supported this by providing $10,000 forgivable loans for people staying at the same address for a specific period of time. The new housing was more expensive than what it replaced, with the new larger homes carrying average price tags of $138,000 versus the $85,000 homes that had been destroyed.

For business, the greatest disruption was for restaurants, bars, hotels and any business where discretionary spending is important. Many of these businesses had to lay off workers. Other businesses such as banks, health care and manufacturing suffered lost sales but did not suffer drastic employment declines. In fact given the gains in construction jobs, employment in Grand Forks rebounded to its pre-flood level in five months. To some observers, the newly rebuilt Grand Forks with its improved infrastructure and new capital stock is better positioned for growth than before the flood, but this is only true because of significant government subsidies and 10 years of hard work. And of course, it is not true for every household and business impacted by the flood, as many chose to leave Grand Forks.

Conclusions

The 2008 flood may seem to be milder in its overall economic impact on the larger region and the nation, but it is just as devastating for those who have suffered it as it was for those in previous floodings. The ultimate costs and impacts can only be known over time as damages become known, as the extent of relief is determined and as households, businesses and towns decide how to respond to the disruption. Most though not all of the agricultural costs and recovery will be known by the end of the growing/harvesting season. In contrast, the recovery and rebuilding process for towns, businesses and households will be protracted and laborious.