Interpreting the Midwest Economy Index

On March 31, 2011, the Chicago Fed will begin releasing on a monthly basis an index designed to measure growth in nonfarm business activity in the Seventh Federal Reserve District states of Illinois, Indiana, Iowa, Michigan, and Wisconsin. This monthly index, called the Midwest Economy Index (MEI), will serve as a regional counterpart to the Chicago Fed’s National Activity Index (CFNAI), available here, and allow for a comparison of national and regional growth trends.

This blog serves as a source of background information on the MEI, detailing its construction and interpretation. In the future, this information will be available online. To receive email updates on the MEI as well as future releases, you can sign up online beginning March 31.

Background on the MEI

The MEI is a weighted average of 128 state and regional indicators encompassing the entirety of the five states in the Seventh Federal Reserve District. It measures growth in nonfarm business activity from four broad sectors of the Midwest economy: 1) manufacturing, 2) construction and mining, 3) services, and 4) consumer spending.

As with similar indexes of regional economic activity, the majority of the indicators in the MEI are based on data from the Payroll and Household Employment surveys and State Initial Unemployment Insurance claims.1 However, for the manufacturing and construction and mining sectors, the MEI also captures production indicators, while for consumer spending it additionally includes data on personal income and home and retail sales.

The MEI incorporates indicators that are observed at both a monthly and quarterly frequency. To express the monthly index at a quarterly frequency, we translate all 128 indicators into a common frequency by taking a three-month moving average of the monthly indicators. In this sense, the MEI’s closest national counterpart is the three-month moving average of the CFNAI (the CFNAI-MA3). Every indicator is then given a stationary transformation and standardized to have a zero mean and unit variance.

The weight each indicator receives in the MEI depends upon the relative degree to which it explains the overall variation among all the indicators. In this fashion, greater influence in the index is given to those indicators that are able to best explain broader fluctuations in the Midwest economy. The degree to which this is true for any individual indicator is captured in the absolute value of its weight. A full list of indicators and their weights can be found here.

To be able to incorporate indicators that differ in originating date and reporting frequency, we follow the estimation strategy outlined by Stock and Watson.2 This strategy is based on a statistical method called “principal component analysis” and is used to create a system of relative rankings, or weights, for the indicators. These weights are re-estimated each month, but in practice change very little given the substantial history of the index.

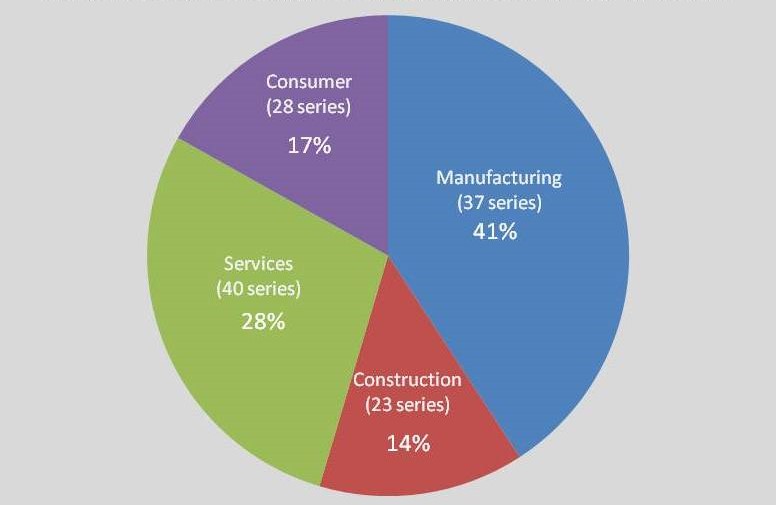

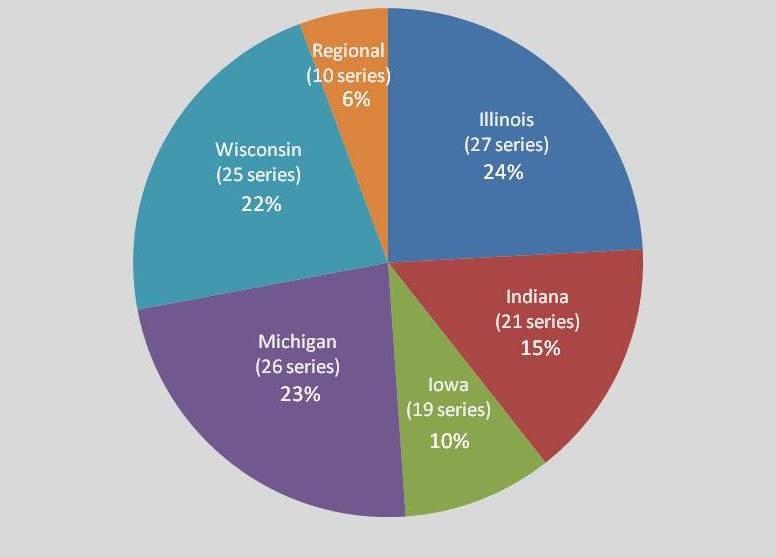

To illustrate the role played by each of the four sectors and five states, the pie charts below show what percentage of the variation in the 128 indicators explained by the MEI can be attributed to each sector (figure 1) or state (figure 2). Broad fluctuations in Midwest nonfarm business activity have historically been explained by the manufacturing sector and, to a lesser extent, the service sector, as well as by the three largest District states (Illinois, Michigan, and Wisconsin).

1. Sectoral decomposition of variance explained by the MEI

2. Geographic decomposition of variance explained by the MEI

Interpreting the MEI

Our motivation in creating the MEI is to better understand the relationship between growth in national economic activity and growth in Midwest economic activity. The MEI is a measure of regional economic activity in much the same way as the CFNAI is a measure of national economic activity. CFNAI values above zero indicate growth in national economic activity above its historical trend, and values below zero indicate growth below trend. Similarly, MEI values correspond to deviations of growth in Midwest economic activity around its historical trend.

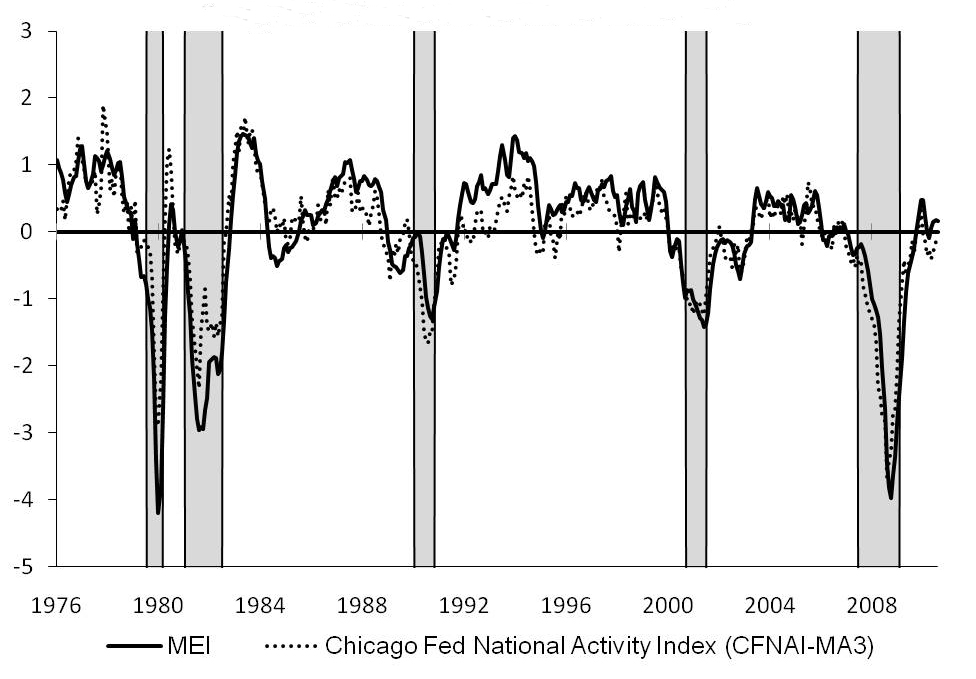

Over long periods, Midwest economic activity has tended to track national economic activity—as shown in figure 3, which compares the MEI and CFNAI-MA3. Both indexes in this figure have been expressed in standard deviation units, so that a value of –1 corresponds with growth that is 1 standard deviation below trend.

3. The MEI and CFNAI-MA3

However, over shorter periods this has not always been the case, particularly around the beginnings and ends of recessions (the shaded regions in the figure as defined by the National Bureau of Economic Research, or NBER). To highlight such differences, we construct two separate index values: an absolute value and a relative value. The MEI (absolute value) captures both national and regional factors driving Midwest growth, while the relative MEI (relative value) provides a picture of Midwest growth conditions relative to those of the nation.

A positive value of the relative MEI indicates that regional growth is further above its trend than would typically be suggested based on the current deviation of national growth from its trend, while a negative value indicates the opposite. To obtain this interpretation for the relative MEI, we use the standardized residuals from linear regressions of each of the 128 indicators on the CFNAI-MA3 to construct the index.3 This construction accounts for differences in national and regional growth trends and volatility that prohibit comparisons of magnitudes in the figure above.

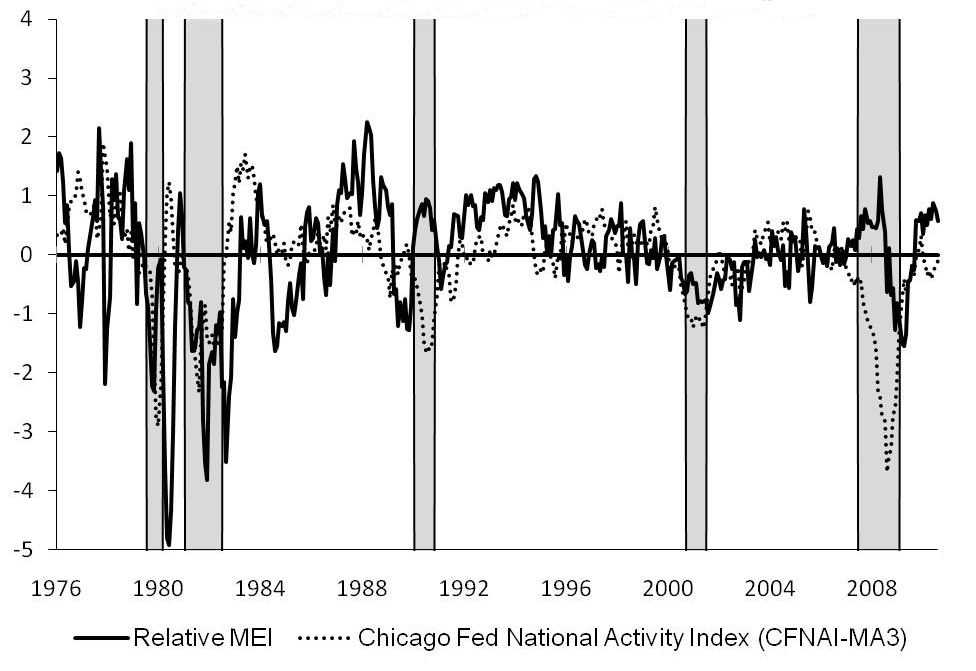

Figure 4 shows the relative MEI in comparison to the CFNAI-MA3. The unit of measurement is again standard deviation units, so that a value of 1 for the relative MEI indicates that Midwest growth is 1 standard deviation greater than would typically be suggested given the level of the CFNAI-MA3. This figure shows that the Midwest business cycle was particularly pronounced during and after the recessions of the late 1970s, early 1980s, and 2007–09.

4. The relative MEI and CFNAI-MA3

Other significant periods in which Midwest growth deviated substantially from national growth include the 2001 recession, which more adversely affected the Midwest region, and the 1990–91 recession, which was milder regionally but was preceded by a period of relative weakness.

Contributions to growth by sector and state

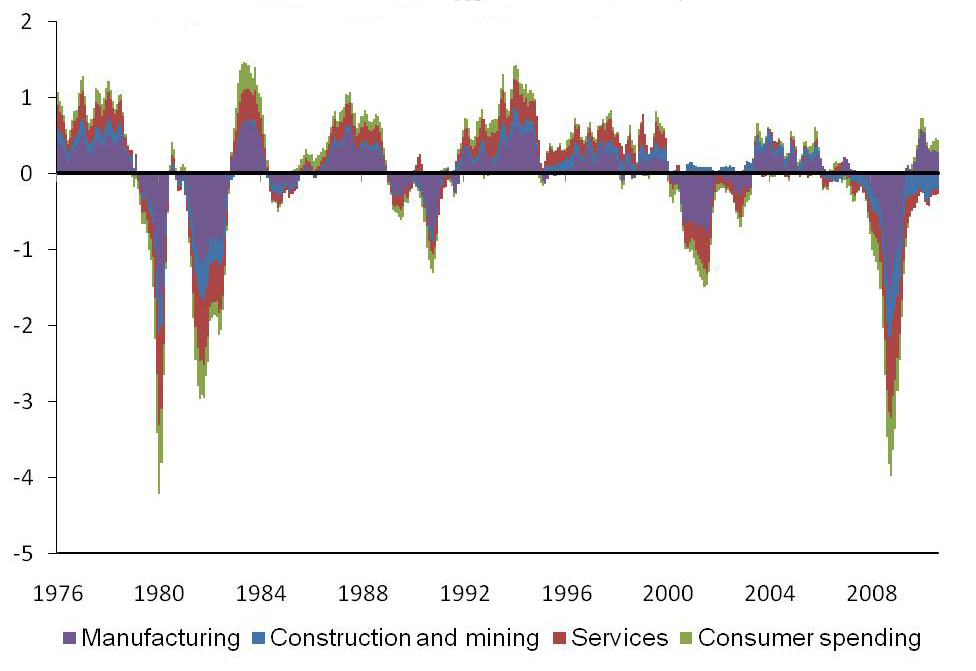

Additional information on the sources of growth in Midwest economic activity can be found by decomposing the MEI and relative MEI into contributions from the four broad sectors of the Midwest economy. The figure below plots the time series of these contributions over the history of the index.

5. Sectoral contributions to the MEI

Much of what we see in this figure can be summed up by the following: When manufacturing has thrived, so has the region. However, the contributions of the service sector to Midwest growth over time have become increasingly important. Consumer spending indicators show a similar pattern, making sizable contributions at business cycle peaks and troughs. Finally, the region has historically been less prone to large fluctuations in growth coming from the construction and mining sector than other parts of the nation.

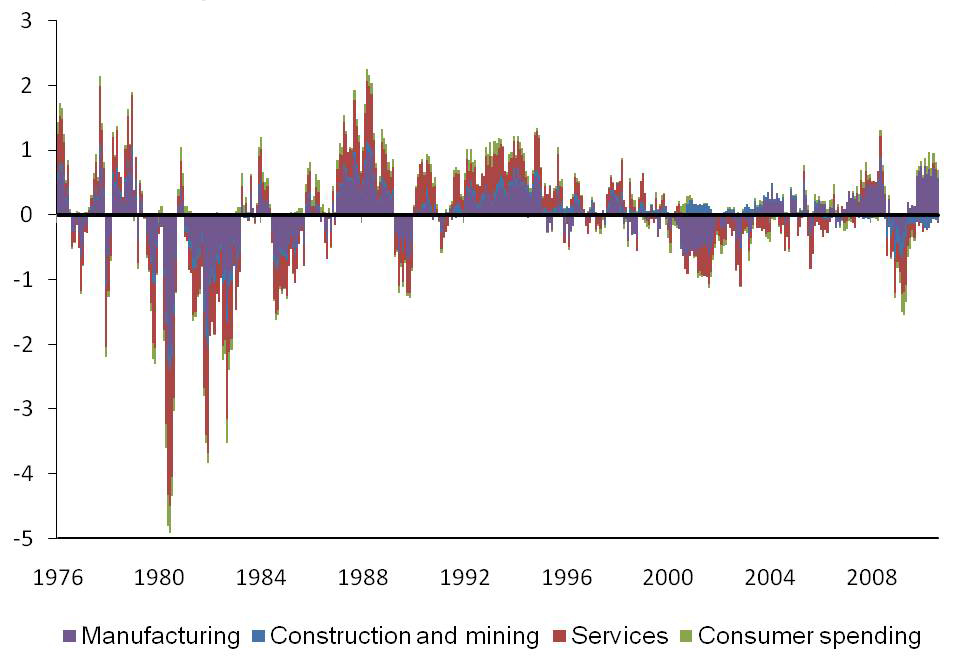

Looking at regional versus national growth, the manufacturing and service sectors explain the vast majority of movements in the relative MEI. However, the contribution of services to the relative MEI is larger than it is to the MEI and nearly equal to that of manufacturing. This feature of the relative MEI reflects the importance of the service sector during periods where the Midwest economy has expanded or contracted faster than the nation. A good example of the former is the early to mid-1990s, while the early to mid-2000s exemplify the latter.

6. Sectoral contributiosn to the relative MEI

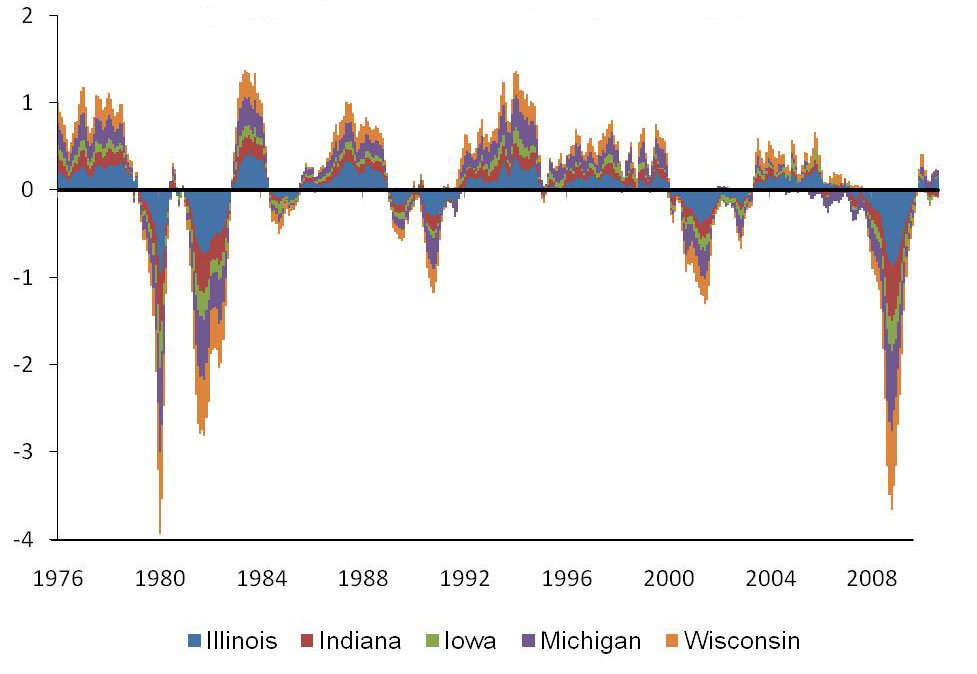

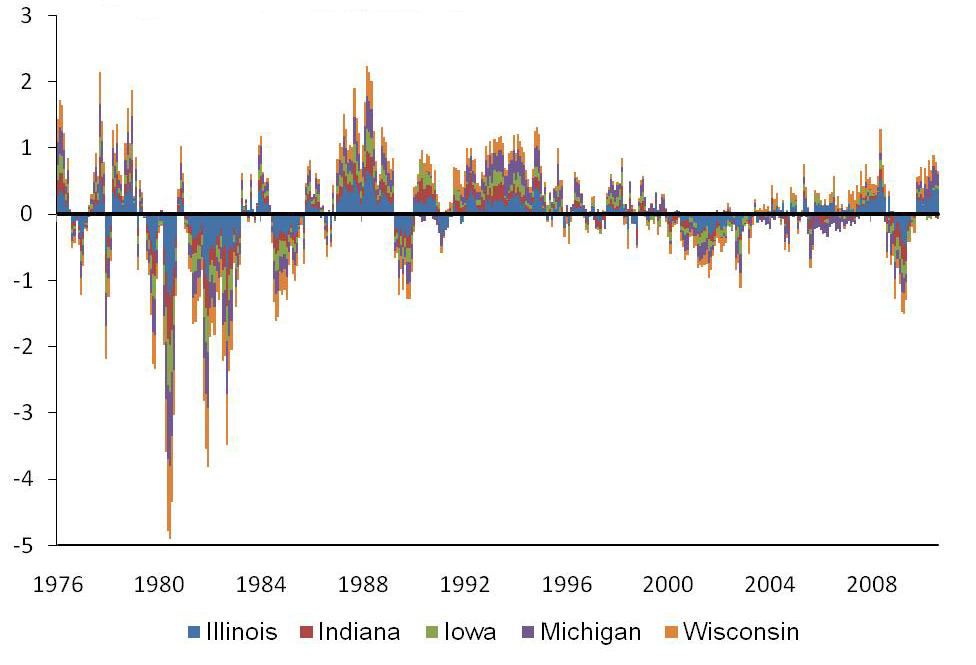

Using only the indicators for the respective states in the Seventh District, we construct state-level contributions to the MEI and relative MEI.4 Figure 7 plots the time series of these contributions over the history of the index. No single state dominates growth in Midwest economic activity, although Illinois tends to make the largest contribution to both; and growth trends in nonfarm business activity across states are similar, with the exception of the weakness of the Michigan economy over the past decade.

7. State contributions to the MEI

During the recent recovery, all five Seventh District states have made positive contributions at one time or another to the MEI and relative MEI, suggesting that the manufacturing-driven recovery has benefited the region disproportionately.

8. State contributions to the relative MEI

Footnotes

1 See, for instance, Theodore M. Crone and Alan Clayton-Matthews, 2005, “Consistent economic indexes for the 50 states,” Review of Economics and Statistics, Vol. 87, No. 4, pp. 593–603.

2 J. H. Stock and M. W. Watson, 2002, “Forecasting using principal components from a large number of predictors,” Journal of the American Statistical Association, Vol. 97, No. 460, pp. 1167–1179.

3 Every indicator is regressed on the contemporaneous value of the CFNAI-MA3. Some indicators are also regressed on the lagged value of the CFNAI-MA3. These indicators are chosen based on the Bayesian Information Criterion, which balances the explanatory power gained by including an additional lag of the CFNAI-MA3 in the regression against the uncertainty introduced from the estimation of an additional parameter.

4 A handful of indicators exist only at a regional level. To construct state contributions, we omit these variables. Therefore, the state contributions do not sum to the overall index in each period.