Fossil Fuel Prospects and Location

In mid-November, the International Energy Agency forecasted that “extraordinary growth in oil and natural gas output in the United States will mean that … the United States becomes a net exporter of natural gas by 2020 and is almost self-sufficient in energy, in net terms, by 2035.” Similarly, the U.S. Energy Information Administration recently revised its long-term outlook, and reported U.S. energy production growing faster than consumption through (at least) year 2040. This startling turnabout is due, in no small part, to recent advancements in U.S.-born technologies in the drilling and recovery of hydrocarbon fuels—natural gas, gas liquids, and petroleum. Already over the past several years, U.S. production of these fuels has boomed due to commercial development arising from these technologies.

In the past month, two experts on emerging developments in this area reported at conferences held by the Federal Reserve Bank of Chicago. At the recent Economic Outlook Symposium, Loren C. Scott discussed U.S. and global energy developments. He presented a sanguine view on U.S domestic production from natural gas and petroleum resources.

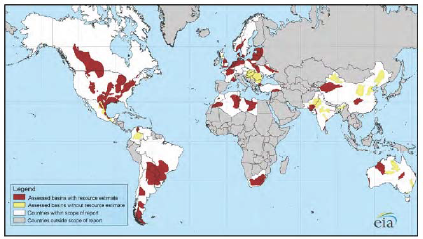

In fact, promising geological formations for gas and oil production can be found throughout the globe (See map). However, the U.S. has been far out in front in developing the technologies to extract these resources, as well as the commercial foundation that has enabled production enterprises to bring them to market.

On the production side, Scott argued that the recent development of these fuels has been aided by fortuitous conditions in the U.S.—conditions that will not soon be replicated elsewhere in the world. Not only were the technologies developed here, but necessary pre-conditions of development were in place. In particular, property rights for minerals located beneath privately held land belong to landowners here, and these can be readily sold and transferred to would-be developers. Such conditions do not hold in most other nations, where mineral rights may be ill-defined or owned by the government. Furthermore, opposition from environmental groups is far more vociferous in other nations, especially in many parts of Europe, which is also home to significant geological deposits.

1. Map of 48 major shale gas basins in 32 countries

The availability of a network of pipelines to transport natural gas is another pre-condition for development that has already been met in parts of the U.S. Owing to previous generations of energy exploration, development, and delivery of fossil fuels across the U.S., much of the pipeline infrastructure is already in place to transport gas from field to consumers.1

On the demand side, Scott said that expanding supplies of natural gas will in turn expand market usage by 2–3 trillion cubic feet annually, or about 10% of recent domestic consumption. In particular, natural gas will find two ready markets, possibly three.

For one, domestic manufacturers—especially in several chemical sectors—stand ready to absorb available natural gas at favorable prices. In particular, producers of ammonia nitrate fertilizers use natural gas as a primary feedstock. Similarly, ethylene is derived from natural gas liquids, and is used for plastics and vinyl in a wide range of products from housewares and toys to vinyl pipes. Currently, ethylene is derived from petroleum products in Europe, which puts producers there at a serious price disadvantage relative to U.S. producers.

Natural gas will also easily become a more important boiler fuel in electric power generation. Scott forecasted that natural gas will displace increasing amounts of coal-fired generation, especially two to three years from now when environmental regulation of coal-fired facilities begins to tighten in earnest.

A third source of possible market expansion is U.S. exports. Currently, global trade in natural gas (in liquefied form) is very small compared with petroleum, for example. One reason for that is that extensive infrastructure is needed to liquefy, load, and transport natural gas. Even so, such investment may be motivated by the wide price differentials between the U.S.’s output and that of potential importing nations. For example, Scott cited spot market prices at $2–3 per million btu in the U.S., versus import prices of $11 in Europe and $16 in Japan. Despite these favorable price spreads, the development of exports from the U.S. will be challenged by both costly new infrastructure need for global shipment, and by resistance from domestic gas users, who will likely push for statutory trade restrictions on exports.

With regard to legal impediments to shale field production and sale, Scott argued that the widespread location of resources across the U.S. will likely keep federal regulation and restrictions contained. At a November 27 conference on Farmland Leasing, Ross H. Pifer of Penn State University reported on the leasing of mineral rights in the Marcellus shale region of New York, Pennsylvania, Ohio, and West Virginia. As the map shows, shale deposits are widespread across the nation, including some deposit locations in each of the Seventh District states. The Energy Information Administration reports “active plays,” involving development or pre-development in parts of the Antrim Basin in Michigan and in the New Albany Basin of southern Indiana (and northern Kentucky).

2. Lower 48 states shale plays

Across the U.S., several areas of shale have been producing natural gas in recent years, ranging from Texas to North Dakota to the Northeast states. Looking ahead, however, Pifer cited a 2009 assessment of the location of recoverable gas reserves that reported a high geographical concentration in the Marcellus shales. In that report, the EIA estimated that the Marcellus shales contained 410 trillion cubic feet of natural gas (tcf), representing 54.7% of the Lower 48’s “reserves.” In contrast, the Antrim deposits (Michigan) were estimated to contain approximately 20 tcf, and the New Albany deposits (Indiana) 11 tcf.2 To put these quantities in context, the U.S. consumed approximately 24 tcf of natural gas in 2011.

Footnotes

1 One exception to this is the so-called Bakken Field located in western North Dakota, eastern Montana, and across the border in Canada. There, sufficient pipeline infrastructure to market is inadequate for carrying petroleum and other liquids to markets and refineries.

2 Note that estimates of reserves can vary widely and with great uncertainty. Note also that these reserves report on natural gas reserves only, excluding petroleum. Several formations also contain significant petroleum reserves.