The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Great natural disasters bring in their wake calls for government action to prevent, or at least lessen the impact of, the next occurrence. Earthquakes give rise to construction code changes and evacuation plans; floods, to new levees, dams, and runoff channels. Just so, the global stock market “break” of October 1987 generated many proposals for change in financial regulation and practice, designed to reduce the possibility and lessen the effect of another such event.

But preventive measures, whether for natural or economic disasters, are not without cost. Some may even be counterproductive. This Letter examines one such proposal—to federally regulate and raise margins on stock index futures to bring them in line with margins on stocks—and finds that its proponents have yet to make a convincing case for higher margins on these financial tools.

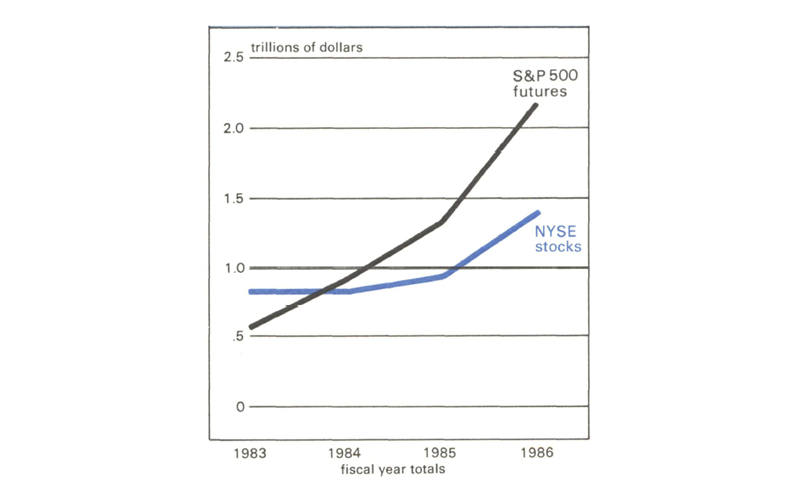

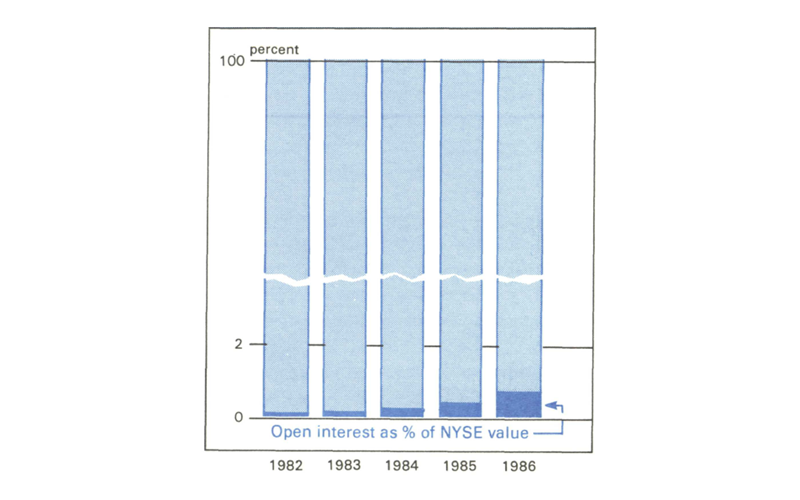

From earlier markets for such commodities as grains and livestock, futures markets have been extended to financial instruments in recent years. One of the most widely traded of the financial futures contracts, and the one discussed here, is the Chicago Mercantile Exchange’s (CME’s) Standard and Poor’s 500 Index contract which began trading in 1982. By 1984, the daily dollar volume of stock index contracts traded on the CME exceeded the daily dollar volume on the New York Stock Exchange, as seen in figure 1. However, this does not mean that the futures market has become more important than the stock market. A more relevant measure of the importance of stock index futures is the underlying value of the contracts outstanding, or open interest. Open interest in stock index futures contracts is a small fraction of the value of shares outstanding on the New York Stock Exchange—less than 1 percent (figure 2).

1. Dollar value of trading

2. Underlying market values

At the heart of the economic role of a futures market is risk transfer. Futures contracts provide a way of transferring risk from hedgers who seek to reduce risk to speculators who would bear risk in the hope of profiting by it. Attempts to curb speculative activity on these contracts by raising futures margins overlook the fact that such curbs would also reduce an investor’s ability to sell off unwanted risk by hedging.

Those who advocate higher, government-regulated margins on stock index futures, as outlined in the Brady Commission report and The New York Stock Exchange Report by Nicholas deB. Katzenbach, make two arguments. First, stock index futures and their underlying stocks are functionally equivalent instruments with similar profit and loss characteristics and, for this reason, margins for the two should be harmonized. Second, the current index futures margin, because it is lower than stock margin, promotes undesirable speculative activity. This results in excessive stock price volatility and undermines the integrity of the financial system. Harmonizing margins, it is argued, would stabilize prices by curbing speculation.

Not all margins are created equal

Despite some similarities in the underlying profit and loss characteristics of stocks and futures, futures and equity margins are not identical in purpose or function. Margin on a futures contract is a performance bond posted by both the buyer and seller of the contract and not a downpayment as in the cash market. Margins on futures are only one of many devices that ensure the financial integrity of the markets. Further, the risk of the stock index contract is not the same as the risk of holding an individual corporate stock. These differences warrant lower margins on futures relative to stocks.

Stocks and apples

A share of stock is an asset, a piece of a corporation. It gives its owner the right to vote on the operation of the corporation as well as a claim to any profits that the corporation pays out in the form of dividends. Investors who buy shares of stock may either pay cash or buy on credit extended by the broker. When investors buy on credit, they must make a downpayment. The minimum downpayment, which changes infrequently,1 is determined by the Federal Reserve. In the parlance of the equities markets, the downpayment is called “margin.”

Margin requirements on stocks are 50 percent of the market value of the stock for most investors. Stock margin is less for stock specialists, who are required to post only a maintenance margin, which is set by the New York Stock Exchange at 25 percent. If the amount of margin posted by an investor falls below 25 percent as a result of an adverse price move, then additional margin must be posted to restore the account to its maintenance level.

Federally regulated stock margins have been in effect for more than half a century. They are designed to protect investors from the risks of highly leveraged positions, to limit the role of credit in destabilizing stock prices, and to prevent the diversion of credit from more productive resources.

Futures and oranges

A stock index futures contract is an obligation to buy or sell the cash value of a portfolio of stocks at a future date for a price agreed upon today. It conveys no voting rights and pays no dividends. In addition, each party to the contract bears risk and must post a performance bond with a broker who is a member of the exchange on which the contract is traded. The amount of the bond is set by the exchange and can vary as warranted by market conditions. Brokers may impose higher margins if they wish. The purpose of the bond is to ensure that both parties are able to fulfill their obligations at the expiration of the contract. In the parlance of the futures exchanges, that bond is called “margin.”

The futures exchanges use margin requirements to preserve the financial integrity of the market. Unlike stock margins, the level of futures margins is primarily a function of price volatility. Initial margin is set equal to the maximum expected one-day price move plus a cushion. The minimum initial speculative margin (stated in a fixed dollar amount) on the S&P 500 futures contract is currently $19,000, roughly 15 percent of the total value of the contract. This is well below margin levels set for stocks.

Sometimes the value of the futures margin account falls below a certain level, known as the maintenance level. This occurs when there is an adverse price change. When this happens, the exchange requires that additional margin be posted in cash to restore the margin account to its original level.

In addition to overall margin levels, other details of margin policies help ensure that market participants fulfill their obligations. First, speculators have higher initial margin requirements than hedgers because hedgers have a cash market position that increases in value as the futures position declines in value. Second, the daily marking-to-market of positions reduces the default risk to the exchange clearinghouse to a one-day price movement. All margin payments are due prior to the start of the next trading day. This contrasts with the equity market regulations that require maintenance margin payments within seven business days, during which time additional maintenance margin calls could accrue if stock prices continue to fall. Further, the Chicago Mercantile Exchange makes daily intraday margin calls.

Market performance is also ensured by position limits that are set by the Commodity Futures Trading Commission. The limits are 5,000 contracts net short or long per owner. There are no position limits in the stock market.

These differences in institutional arrangements alone are sufficient to warrant different margins on futures contracts.

Baskets and eggs

There is an important distinction between the type of risk realized by holders of a stock and holders of an S&P 500 futures contract. The risk assumed by holders of an individual stock consists of market risk and firm-specific risk. In contrast, investors holding a futures contract on the S&P 500 Index realize only the market risk because the firm-specific component has been diversified away. Because less risk is assumed by the holder of an S&P 500 futures contract than by an individual holding equity in a corporation, the S&P 500 futures contract margin requirement should be lower to reflect this.

Margins and speculation

The second argument is that lower futures margins promote undesirable speculative activity, which results in excessive stock market price volatility. This argument makes two important assumptions. First, it assumes that speculative activity in the marketplace is undesirable, and second, it assumes that futures margins are an effective policy tool for limiting speculation and volatility.

Is speculation bad?

The first assumption ignores the important role of speculators in futures markets. Speculators absorb the price risk that hedgers do not want to bear. Speculators also increase the ease with which hedgers find trading partners and facilitate continuous price discovery by assuring that prices are competitively determined by frequent transactions of market participants.

Ironically, the single activity that is most frequently cited as exacerbating the market break of October 1987 was portfolio insurance—a dynamic hedging strategy.2 When stock prices are falling, portfolio insurers sell futures contracts to either hedgers or speculators to reduce their exposure to the stock market. Hedgers will buy futures contracts and simultaneously sell the underlying stock, thus locking in a rate of return. Speculators, however, will not offset their futures positions in the stock market, thus keeping sell pressure off the stock market.

Data compiled by the Chicago Mercantile Exchange indicate that on October 19 the speculative accounts were net buyers of S&P 500 futures contracts. If these speculators had not been in the market, portfolio insurers would have had to turn to the stock market to execute their strategies. By eliminating speculators, higher margin levels might thus have intensified the price break on October 19.3

Can higher margins reduce speculation? Raising futures margins increases futures market transactions costs.4 The empirical evidence shows that increasing futures margins causes some investors to leave the market, thereby reducing daily volume and open interest.5 However, the evidence does not indicate which investors will leave. Theoretically, traders—either hedgers or speculators—whose price expectations are closest to the currently quoted market price will be the first to exit, leaving only those traders whose price expectations diverge most from the market price. This might cause intraday price volatility to rise.6

There is also evidence that increases in margins are not effective in limiting the formation of speculative bubbles. During 1979 and 1980 silver prices rose rapidly. Futures margins were steadily increased to dampen speculative activity. However, high margins did little to stem the increase in silver prices.7 Margins appear to have provided no defense against excessive optimism.

Conclusion

The call for higher, federally regulated futures margins overlooks differences in the purpose and nature of futures and equities, and their margining systems. These differences alone would justify a lower margin on stock index futures contracts. Higher futures margins might be justified if the futures margins set by the exchanges were ineffective in preventing defaults in the futures market. But, the current system of exchange-determined margins served its purpose despite the massive sell-off in October; no CME clearing member defaulted and the financial integrity of the markets was preserved. The self-regulatory bodies responsible for setting margins in the futures markets reacted appropriately by increasing margins when it became apparent that price volatility had increased.

Thus, if a case is to be made for requiring higher margins on stock index futures contracts, it must be based on the desirability of reducing speculation. However, speculative activity in futures markets provides a useful function by allowing investors to shed unwanted risk at reduced cost. Increasing margins on futures would increase the cost of speculating in the futures markets, thus interfering with investors’ ability to manage risk. Proponents of higher futures margins have yet to provide evidence linking differential margins on stocks and futures and excessive price movements in the stock market. Increasing futures margins may satisfy the pressures to act in the wake of October’s near financial disaster. Yet this seems an insufficient justification for reducing the investor’s ability to manage risk.

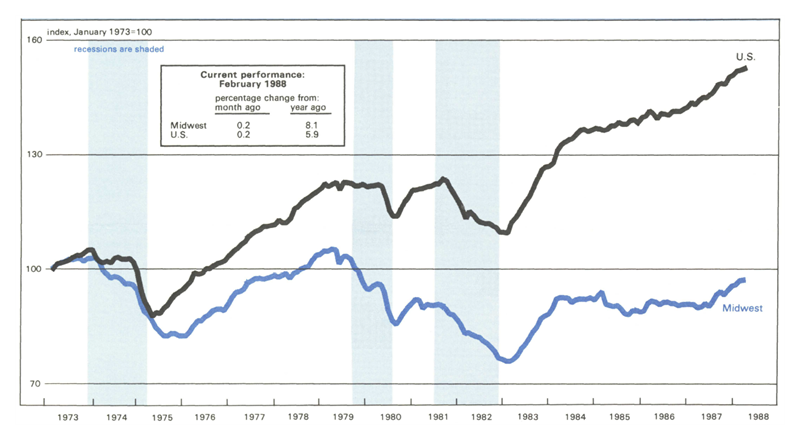

MMI—Midwest Manufacturing Index

Industrial production of manufactured goods nationally edged up 0.2 percent in February. Thus far, the first quarter has been advancing at less than half the pace set in the fourth quarter of 1987. Business equipment continues to be strong, but most durable-goods industries are weak. Transportation equipment and primary metals particularly have been running below their fourth-quarter levels.

Manufacturing activity in the Midwest also rose only 0.2 percent in February, following a pattern similar to the nation’s. A notable exception was the continued improvement in primary metals. Data revisions of both labor and capital inputs reversed declines in the previous two months. The revised data show the MMI outpacing the nation since December, continuing its strong 1987 performance.

Notes

1 The federally regulated minimum initial margin requirement has not changed since 1974.

2 Portfolio insurance activity has decreased due to its limited effectiveness during the market break.

3 See John M. Hawke, Burton Malkiel, Merton Miller, and Myron Scholes. Preliminary Report of the Committee of Inquiry Appointed by the Chicago Mercantile Exchange to Examine the Events Surrounding October 19, 1987. Chicago, 1987.

4 See Michael Hartzmark, 1986. “The Effects of Changing Margin Levels on Futures Market Activity, the Composition of Traders in the Market, and Price Performance,” Journal of Business, vol. 59, No. 2, pp. 147-180. Hartzmark contends that although margin can be posted in the form of Treasury Bills, the opportunity cost is not zero. His argument is that the investor incurs costs associated with the risk that he will be caught short of liquid assets and, therefore, may have to hold additional liquid assets, leaving less funds available to invest elsewhere.

5 Hartzmark finds that increasing margin requirements decreases volume in the futures markets. He also finds that increasing margin requirements decreases the level of open interest. Other studies also address the effects of margins on volume and open interest. These studies are referenced in his paper.

6 See Stephen Figlewski, 1984. “Margins and Market Integrity: Margin Setting for Stock Index Futures and Options,” Journal of Futures Markets, vol. 4 (Fall), pp. 385-416.

7 See Gary D. Koppenhaver, 1987. “Futures Market Regulation,” Economic Perspectives, vol. 11, No. 1 January/February: pp. 3-15.