The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

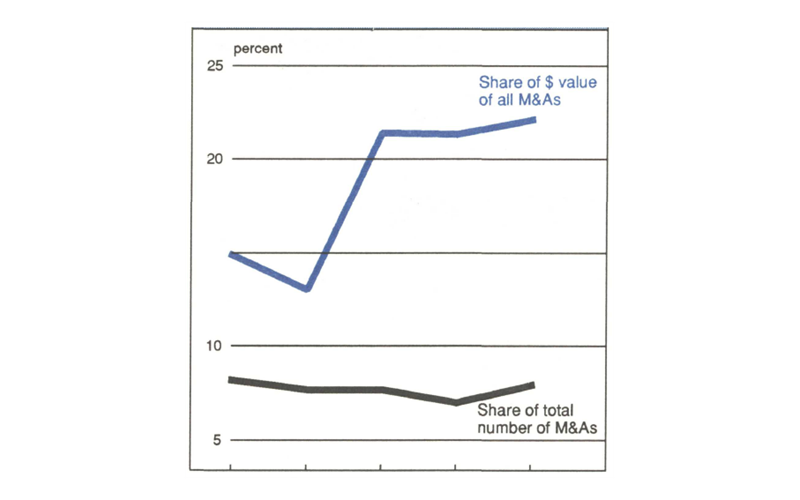

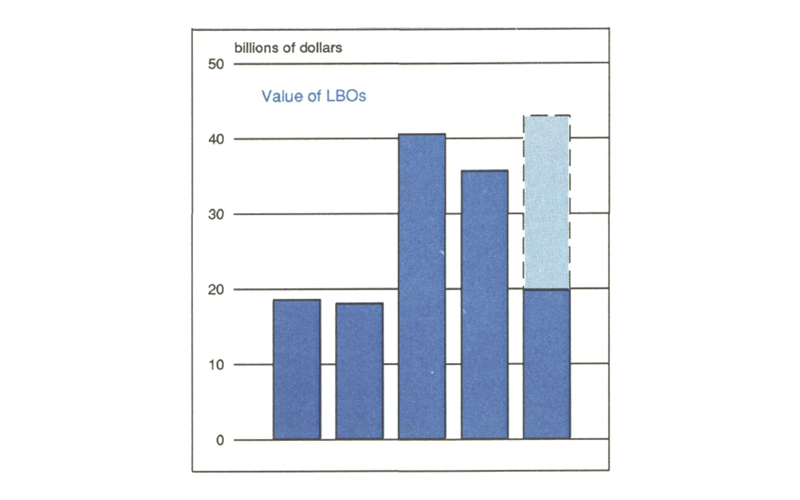

Leveraged buyouts (LBOs) are still only 7% to 8% of all merger and acquisition (M&A) deals done in the U.S. Yet, by dollar value they now constitute more than 20% of all M&A activity (see figure 1). The absolute and relative dollar values of LBOs increased significantly in 1986 and have continued at a high pace. Indeed, the recent RJR Nabisco LBO, at nearly $25 billion, exceeds the annual value of all LBOs for 1984 and 1985 (see figure 2).

1. LBOs: Bigger deals…

2. …And more bucks

Source: Mergers and Acquisitions, Almanacs of selected years.

The large and sometimes astonishing gains associated with these deals have put them in the spotlight, making LBO a newsworthy, market-moving acronym. Substantial profits accrue to shareholders, investment bankers, financial advisors, and attorneys. But has the luster of these gains obscured a darker side of LBOs? Are these proceeds derived from the creation of wealth or are they obtained at the expense of others? Is someone taking a hit? This issue of Chicago Fed Letter focuses on the wealth transfer from target company bondholders to target company shareholders.

What is an LBO?

In an LBO, an individual or small group of investors, often company management in conjunction with an investment banking firm, uses the company’s assets as collateral to borrow funds to take the company private by purchasing all of its outstanding stock at a premium.

It is common to sell high-yield, high-risk securities (junk bonds) to accumulate the cash necessary for an LBO. The resulting company is highly leveraged, with a significant debt burden. For 58 LBOs from 1980 to 1984, average long-term debt increased by 262% and the average debt-to-equity ratio jumped to more than 5 to 1. This was an average increase of more than 1,000%.

Why LBOs?

Taking a company private may protect it from hostile suitors. LBOs are often proposed to shareholders by management in an effort to save their company from a hostile takeover.

But even in the absence of a hostile takeover threat, there are several incentives for LBOs. Although the company is burdened with significant debt subsequent to the LBO, it is the debt that generates much of the cost savings and increased efficiency associated with the LBO. The debt results in tax savings in the form of interest deductions. LBOs can also increase wealth by reducing conflicts of interest created by the separation of management and ownership.

Who gains?

If an LBO is successful, there are gains to be made. Shareholders, on the whole, will not sell out for less than the market price. Thus, by the nature of an LBO, the buyout of shares must be at a premium over the market price.

Research clearly indicates that stockholders of firms acquired in M&As (including LBOs) gain. They benefit by receiving returns above those that would have occurred had the stock followed overall market movements. One researcher conservatively estimates the gain to target shareholders from takeovers of publicly traded companies between 1981 and 1986 to be 47.8%, or an estimated $134.4 billion.

The same studies find that bidder firm shareholders have equal probabilities of gaining or losing and at best receive modest gains. Yet, recent research concludes that the average successful tender offer results in a statistically significant positive revaluation of the combined firm. Thus, on balance, takeovers, including LBOs, enhance shareholder wealth.1

Sources of gain

But while M&As do enhance wealth, such wealth may not be derived entirely, or at all, from increased efficiency (e.g., resource reallocation, removal of inefficient management, or economies of scale or scope). The creation of value and gains from efficiency are even more suspect in LBOs which, by their nature, lack the usual synergistic gains of M&As.

Although easily measured, shareholder gains do not provide an accurate measure of welfare gains. If, for example, takeover and LBO gains are a result of wealth transfers, then the increase in share prices overstates the efficiency gains of takeovers and LBOs. This is because shareholder gains must be weighed against the losses of others.

Opponents of LBOs argue that gains from such transactions result primarily from wealth redistributions: one stakeholder’s gain—the target shareholder’s—is at the expense of another’s economic loss— such as the target company’s employees or its bondholders or the U.S. Treasury. In the extreme, such transactions are merely costly restructurings of corporations that provide no social benefits. Preventing such buyouts would, it is argued, improve economic welfare.

On the other hand, proponents argue that LBOs provide net gains to society by reducing the conflicts of interest between management and shareholders. This, in turn, improves resource allocation and efficiency and encourages value-maximizing behavior. Thus, attempts to prevent such transactions would have negative effects.

Research has been unclear concerning the sources of takeover gains. They may result from redistribution and increased efficiency. But the sources of gain vary from deal to deal, from industry to industry, and from year to year.

Studies have addressed the wealth transfers to target shareholders from: government (and, thus, taxpayers) in the form of tax savings; target labor in the form of lower wages and higher unemployment; and target bondholders in the form of reduced bond values.

Do target bondholders lose?

Corporate bondholders purchase bonds based on, among other factors, the bond’s rating, which reflects an assessment of the likelihood that the company will make timely interest and principal payments. Purchasers of high-grade bonds assume very little, if any, risk of corporate default. That is, they do so in a world without LBOs.

LBOs result in increases in the firm’s debt burden. If the additional debt increases the probability or cost of future default, then the value of the target’s bonds will decline.

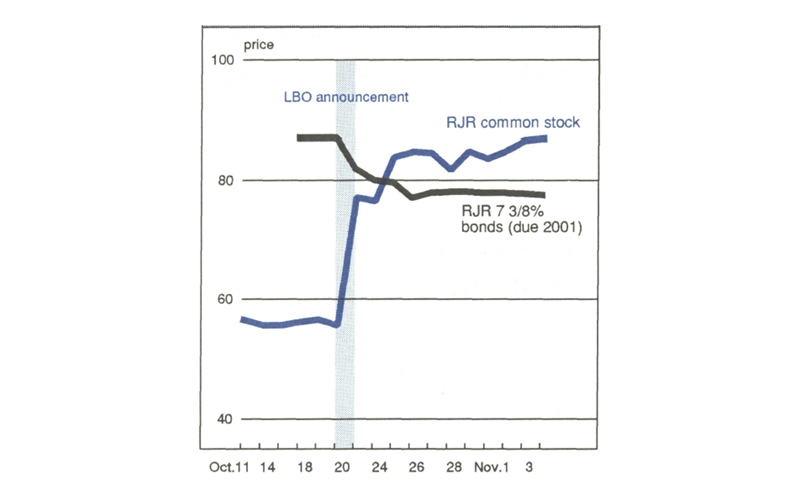

Among several recent examples of falling bond values associated with LBOs, the most notable is RJR Nabisco (see figure 3). Indeed, some RJR bondholders have filed suit against RJR. They argue that RJR management has failed in its duty to bondholders and that the LBO benefits others, including management, at the direct expense of the bondholders.

3. The stock soars, a bond drops

These highly publicized examples may be isolated instances of extremely risky ventures or of poorly written bond covenants that fail to adequately protect the bondholder. Or they may indicate that bondholder losses are sometimes the price paid for shareholders’ and others’ gains in LBOs—or more respectably, the price to be paid to obtain efficient management and allocation of resources.

Additional evidence

Prior studies have compared the returns on bonds of takeover targets either to bonds with similar characteristics of corporations not subject to takeover, or to changes in a selected bond index. These studies found that, on average, target company bondholders neither gain nor lose by a (statistically) significant amount in takeovers. Furthermore, there were no noticeable wealth transfers between bondholders and stockholders.2

The following analysis is specific to LBOs and looks solely at the change in bond value attributable to the announcement of the LBO. It does so by controlling for changes in the bond price caused by changes in interest rates on government securities of comparable duration.

Our study covered 20 LBOs, including some of the largest ones, from mid-year 1984 to mid-year 1988. All the organizations had corporate bonds outstanding at the time of the announcement of the LBO.3

Results for the entire sample are consistent with previous research using both monthly and daily bond data. Overall, the probabilities of a gain or a loss in bond values upon an LBO announcement are about equal. Moreover, on average the increases or decreases in bond values of LBO targets are not statistically significant. This is true across all bond grades. So overall, stockholders are not gaining at the expense of bondholders in LBOs.

However, this is not very consoling to the holders of approximately 50 percent of those issues that do lose value. Although the average change in bond prices across all issues in the sample is a statistically insignificant 0.50%, the difference between the minimum (−1.84%) and maximum (−15.39%) loss is great.

4. LBO target bonds: gains and losses (% of bond’s face value)

| All bonds (n=20) | Gainers (n=12) | Losers (n=8) | |

|---|---|---|---|

| Average | −0.50 | 5.87 | −7.54 |

| Range | −15.39 to 17.08 | −0.58 to 17.08 | −15.39 to −1.84 |

The reconciliation of these and previous results with the highly publicized negative returns (and less publicized gains) to bondholders of certain LBO targets is the recognition of the difference between individual and average results. Interestingly, the average data in this analysis hides the fact that the two highest-rated bonds (A+) each had losses greater than the two lowest rated bonds (B+) upon the announcement of their respective LBOs.

The aggregation of data also masks a major tax-related incentive of LBOs. The Tax Reform Act of 1986 eliminated the preferential tax treatment of capital gains. This has increased the incentives to issue debt. (Interest payments on debt are deductions from taxable income, but dividend payments are taxed at the corporate or personal tax rate.) Capital restructuring in the form of an LBO increases the value of the firm by reducing its tax burden.

A split of our LBO sample into those effective prior to and after January 1987 provides a suggestive, but not conclusive, bit of information. Bondholders of LBOs occurring prior to the tax law changes effective in 1987 received significant gains averaging 7.36%, while bondholders of LBOs effective in 1987 and later received significant losses averaging 5.10%. The statistically significant different experiences of the two groups coincides with the dramatic increase in size of LBOs and suggests that tax incentives have changed the nature of LBOs.

The guiding principle for the bondholder may be to judge each case individually, taking into account a firm’s exposure to an LBO. While changes in bond prices are certainly important to those buying and selling bonds, it may be argued that bonds are usually bought as a long-term investment to be held to maturity with relatively guaranteed interest payments.

However, the price of a bond today is affected by the probability and cost of default in the future. Right or wrong, a change in bond values today reflects the market’s best guess about the LBO’s long-term impact on default risk.

Assessment

Falling bond values for certain LBO targets represent the market’s downgrading of the bond quality prior to or in absence of an official downgrade. Several factors may play a role in the downgrading of individual bonds.

For current and prospective bondholders relevant factors to consider are: the size of the deal; the level of existing debt and the relative increase in leverage; expectations of the corporation’s future credit needs; whether the LBO group includes current management; the protective covenants of the bond agreement; the firm’s level of free cash flow; the degree of increase in stock values; the terms of the deal including plans to pay down the debt; the firm’s tax liabilities and the tax consequences of the deal; and the corporation’s bond rating history.

In short, with LBOs an increasing possibility, the bondholder needs to think more like a stockholder.

MMI—Midwest Manufacturing Index

Hopes of a continuation of August’s slowdown in U.S. industrial production that would ease inflationary pressures were further dampened by solid growth in October. Manufacturing activity in the nation rose 0.5 percent in October, up from 0.4 percent in September. Durable goods, led by business equipment and automotive products, provided the bulk of the growth.

Midwest manufacturing activity was unchanged from its September level, reflecting spot weaknesses in business equipment-related industries. While nonelectrical equipment continued to expand activity, instruments edged downward and electrical equipment declined after two strong months of expansion. Also, transportation equipment continued its downward trend as plants closed in Michigan.

Notes

1 For a review of the literature on gains and sources of gain in takeovers, see Diana L. Fortier, “Hostile Takeovers and the Market for Corporate Control,” Economic Perspectives, Federal Reserve Bank of Chicago, Jan./Feb. 1989. For evidence on the gains to shareholders from LBOs see Khalil M. Torabzadeh and William J. Bertin, “Leveraged Buyouts and Shareholder Returns,” The Journal of Financial Research, Vol. 10, No. 4, (Winter 1987), pp. 313-319.

2 LBOs used were listed in Mergerstat Review 1984-1987 (Chicago: W. T. Grimm & Co.) or in the quarterly Rosters of Mergers & Acquisitions 1985Ql-1988Q2. LBOs of subsidiaries or units of an organization were excluded. Also excluded were LBOs announced around the time of the October 1987 crash. Corporate bond data are from S&P’s Bond Guide January 1984-November 1988 (New York: Standard & Poor’s Corporation). If more than one issue of long-term debt was outstanding, the one used was the most highly rated issue with the longest term to maturity. STRIP data (Treasury 0% CATS prior to February 1985) are from Salomon Brothers Inc. Bond Market Roundup July 1984-November 1988.

3 Paul Asquith and E. Han Kim, “The Impact of Merger Bids on the Participating Firms’ Security Holders,” Journal of Finance, Vol. 37, No. 5, (December 1982), pp. 1209-1228 covers 50 conglomerate mergers from 1960-1978.; Debra K. Dennis and John J. McConnell, “Corporate Mergers and Security Returns,” Journal of Financial Economics, Vol. 16, No. 2 (June 1986), pp. 143-187 covers 132 mergers from 1962-1980.; and Kenneth Lehn and Annette Poulsen, “Leveraged Buyouts: Wealth Created or Wealth Redistributed?” in Public Policy Toward Corporate Takeovers, (New Brunswick, NJ: Transaction Books, 1988) covers 13 bonds of firms subject to LBOs.