The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Since the middle of the last century, the Chicago area has served as the business capital of the mid-continent. Chicago’s preeminence covers finance, retail trade, wholesale trade, business services, and manufacturing. Like almost every other major U.S. city, Chicago has seen its manufacturing base erode sharply over the last 40 years. For this reason, the Chicago area looks eagerly to other business sectors to replace lost jobs and income. This Chicago Fed Letter examines the concentration and growth of Chicago’s so-called FIRE industries—finance, insurance, and real estate.

FIRE spreads in Chicago

The Chicago area’s rate of economic growth has been diminished by industrial upheavals. Since 1969, the area has lost over 372,000 manufacturing jobs, a decrease of 37%. Fortunately, the area is having some success in reinventing itself. Over the past 25 years, service industries rather than manufacturing have stepped up to shoulder the burden of the area’s job growth, with FIRE industries showing the most dramatic growth. In 1969, the FIRE sector accounted for only 7% of employment. By 1992, it had created over 190,000 new jobs and accounted for almost one in ten Chicago-area jobs. FIRE employment in the nation also grew rapidly over this period, but by 1992 its share of total U.S. employment had not yet reached 8%. As a result of FIRE’s growing concentration in the Chicago area, the sector’s performance in coming years will help determine the region’s growth and welfare.

FIRE industries

Industries within the FIRE grouping are alike in that they are all financial intermediaries. Banks and securities brokers and underwriters gather capital (savings) from firms and households and transform it into the stock of capital used for business investment, household real asset acquisition, and consumption. By contrast, the insurance and real estate industries provide service outputs other than capital provision or returns from savings. Many real estate operations provide sales services on both business and residential property, while insurance firms add value by pooling and minimizing household and business risk. The futures exchanges, found under the finance industry banner, also deal in the market for risk, albeit in a different fashion. Futures exchanges create a market for risk, serving those who want to shed it and those who want to acquire it.

Some researchers have grouped the FIRE industries along with the so-called business services such as accounting, data processing, and computer services whose primary customers are firms rather than households. However, to a greater degree, FIRE activities include transactions with both businesses and households. Approximately 50% of the output of the finance and insurance industries is absorbed into further business production. By contrast, about two-thirds of real estate output is absorbed by the consumer sector through its sales services for residential properties. Nevertheless, grouping FIRE industries with business services may be sensible because they do tend to share another important feature: Many FIRE services do not require face-to-face delivery to the customer. Because capital is increasingly mobile, financial products are more frequently documented, bundled, and sold afar rather than locally. As a consequence, communities view FIRE industries as possible economic development targets, that is, as industries that can grow more rapidly than the community’s own population through the growth of external demand.

Occupation and employment

Because FIRE industries produce a wide range of products and services, they must employ two broad categories of workers: 1) business and finance professional personnel, and 2) administrative, clerical, and data entry personnel. Workers in these two categories need not operate at the same site for any individual firm or any particular industry sector. The highly skilled positions are typically located in large financial centers such as Chicago, London, and New York, where face-to-face communications with others in similar occupations and access to specialty services facilitate product development and sales.

In the Chicago area, over 22% of those employed in FIRE industries, or 66,000 workers, are in executive and managerial occupations. Another 17% are in marketing, sales, and professional specialty occupations, the latter including computer systems analysts, public relations specialists, writers and editors, and miscellaneous jobs. By far the largest category—administrative support—accounts for 58% of total FIRE employment in the Chicago area. Similar to the broader aggregate services sector, the FIRE industries include occupations with a wide range of salary and wage compensation.

Which FIRE industries have led the charge in Chicago? Personal income figures suggest that the sector’s surge has been almost universal across broad industry subgroups. Investment and holding company offices contributed by growing extremely rapidly from a somewhat modest initial base in 1969. Securities and commodities brokers grew strongly from a large relative base, and insurance industries grew strongly from a moderate base. Finally, credit institutions—both depository institutions such as banks and savings and loans, and non-depository institutions such as mortgage banks and household credit companies—grew modestly, but from a very large base.

For all of these reasons, the economic base of Chicago’s FIRE sector has become very wide. Figure 1 ranks major metropolitan areas by the concentration of their individual financial industries. The first column shows that the New York metropolitan area ranks first not by virtue of the absolute size of its FIRE sector but rather because of the relative importance of FIRE to the economy of the entire metropolitan area. The Chicago area ranks third, behind San Francisco and New York, as a result of its strength in securities and commodities brokerages, credit institutions, and insurance establishments.

1.Industry concentration, 1992

| Rank | Total FIRE | Credit institutions | Securities and commodities | Insurance | Real estate |

| 1 | New York | New York | New York | San Francisco | New York |

| 2 | San Francisco | Miami | San Francisco | Chicago | Atlanta |

| 3 | Chicago | Dallas | Chicago | Atlanta | Miami |

| 4 | Atlanta | Chicago | Dallas | Dallas | Denver |

| 5 | Miami | Los Angeles | Denver | New York | Chicago |

| 6 | Denver | Atlanta | Los Angeles | Denver | Pittsburgh |

| 7 | Dallas | Pittsburgh | Miami | Miami | St. Louis |

| 8 | Los Angeles | Detroit | St. Louis | St. Louis | Los Angeles |

| 9 | St. Louis | St. Louis | Atlanta | Los Angeles | Detroit |

| 10 | Pittsburgh | Denver | Pittsburgh | Detroit | Cleveland |

| 11 | Detroit | Cleveland | Cleveland | Pittsburgh | Dallas |

| 12 | Cleveland | San Francisco | Detroit | Cleveland | San Francisco |

Despite the long-term strength of Chicago’s FIRE industries, two of its growth engines face significant challenges ahead. Several of the area’s large banks are struggling, somewhat successfully, to emerge from unfavorable developments of the 1980s. At the same time, the banking industry has been wracked by mergers, acquisitions, and downsizings that have resulted from the new era of interstate deregulation. Meanwhile, Chicago’s financial hallmarks—its futures exchanges—face threats of tighter regulation and fierce competition from abroad, as well as the uncertainty of technological change.

Banking revival

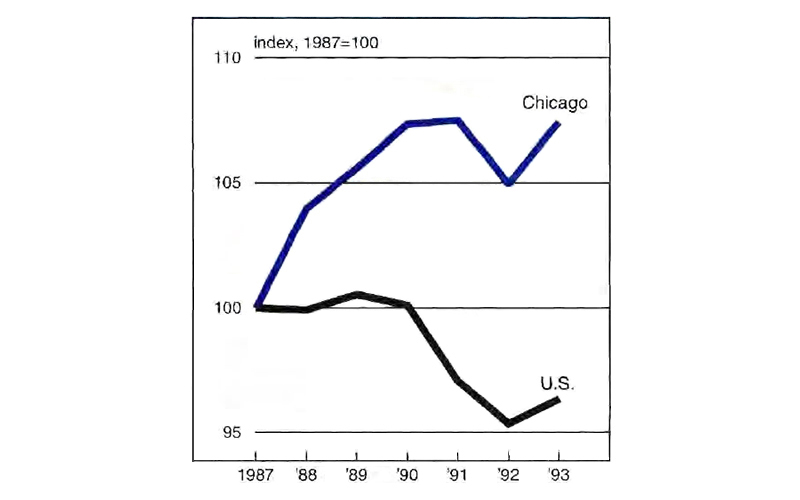

After struggling through the 1980s, Chicago’s depository and nondepository credit institutions are experiencing a resurgence in the 1990s (see figure 2). Before being purchased by BankAmerica Corp., Continental Bank changed course, and its debt-for-equity swaps recently returned its Latin American operations to profitability. Moreover, its continued presence in the southern hemisphere has proved valuable for Americans seeking to do business in the region as well as for Latin American businesses—a positioning that became more important with the passage of NAFTA. In 1994, Continental Bank was purchased by BankAmerica Corp. and renamed Bank of America Illinois. BankAmerica Corp. moved its corporate banking operations to Chicago, making Bank of America Illinois one of the most prominent commercial lending units in the nation.

2. Credit institutions’ employment

Chicago’s status as a top-tier banking center was further enhanced with the recently announced merger of its largest bank, First Chicago Corp., with Detroit-based NBD Bancorp. First Chicago’s success in recent years is due in large part to its rapidly expanding credit-card operations, the fourth-largest in the nation. The new bank, First Chicago NBD Corp., will be headquartered in Chicago and will be the seventh-largest banking concern in the nation. With NBD’s strong middle-market connections and First Chicago’s large corporate customer base and growing credit-card operations, First Chicago NBD Corp. expects to have the experience and resources needed to compete with the nation’s largest banks on both the commercial and consumer fronts.

Chicago-area investors have also organized at least 31 new bank ventures since 1986, and Illinois leads the nation with 11 newly chartered start-ups since 1992. This phenomenon can be partly attributed to the rash of mergers and acquisitions occurring in the banking industry. Since an acquiring bank typically pays a premium for the stock of the bank to be acquired (often as high as twice the stock’s book value), each acquisition frees up investor’s capital, which can be used to finance new ventures. In addition, the downsizing that generally accompanies bank consolidation leaves many talented and experienced managers available to lead new ventures. The result has been an increase in start-ups of smaller, niche-based banks or “de novos.” The Chicago area’s de novos have aggressively targeted niches such as middle-market companies unhappy with large bank service or seeking more personal contact with their banker. Others have targeted ethnic niches, family-owned enterprises, or affluent individuals who are also dissatisfied with larger commercial banks.

Chicago’s financial hallmark

Chicago’s financial hallmark is that it is the headquarters of major commodity, futures, and options exchanges. The Chicago Board of Trade (CBOT) and the Chicago Mercantile Exchange (CME) are the world’s two largest futures exchanges. The Chicago Board Options Exchange is the world’s largest stock options exchange. In sum, over one-third of the world’s options and futures are traded on Chicago’s exchanges.

The local impact of this market activity is clearly great, though difficult to estimate precisely. One study reported in the late 1980s that the exchanges were directly responsible for 33,000 jobs and indirectly for over 110,000 jobs.1 Related spending in the Chicago area on legal and other business services, rents, and communications is considerable. Since the time of the last Chicago impact estimate, the securities and commodities industries have continued to grow, outpacing the industry nationally and outpacing total employment growth in the area.

In recent years, events involving either the trading of futures contracts or so-called derivatives have caused some to question whether the regulatory environment should be modified. The debate has led to proposals to add regulations, tax more heavily, or otherwise restrict the use of risk-management products. The stock market crash of 1987 was followed by criticism of the role that stock index futures played in the event. In response, both the Securities and Exchange Commission (SEC) and Brady Commission subsequently recommended changing the regulatory framework, which would have involved both raising margin requirements and giving the SEC an oversight role in stock index trading. More recently, the image of derivatives trading may have been called into question by large losses in so-called derivatives instruments realized by corporations such as Proctor & Gamble and by governments such as California’s Orange County Treasurer and the Wisconsin Pension Board. Ironically, these events may ultimately improve the public perception of exchange activity, because the problems occurred in the largely unregulated arena of over-the-counter derivatives contracts, not in the regulated arena in which the exchanges operate. Nonetheless, the possibility of tighter state and federal controls, and the imposition of a federal transactions tax, may inhibit the continued expansion of the exchanges’ financial products.

Technological changes offer both opportunities and challenges to continued growth. Over-the-counter trading via computers located elsewhere has penetrated the markets and threatened Chicago’s trading mechanisms. Chicago’s exchanges have answered these challenges with innovations and new products of their own. For example, both CBOT and CME have proposed to offer transactional services to participants in the over-the-counter SWAPS market. The CBOT and CME have also established linkages with other exchanges, which may well protect or enhance market penetration. So too, the Chicago Stock Exchange recently applied for SEC approval to create a new electronic exchange for the increasingly lucrative off-exchange trading market. These products are still too young to allow any solid assessment of their effectiveness in meeting worldwide competition.

Conclusion

Chicago’s FIRE industries have been a bulwark in sustaining the area’s economic strength over the past 25 years. The Chicago area’s share of income and employment derived from FIRE industries now significantly exceeds that of the nation, and the gap continues to widen. This growth has been widespread within the financial services industries, extending across depository institutions, real estate, insurance, and securities dealers and brokers. As a result of its broad base of financial industry strength, the Chicago area has maintained its status as a regional and national center for financial services. Its international status, however, is confined to its specialization in a few markets, the most prominent being its futures and options exchanges.

Tracking Midwest manufacturing activity

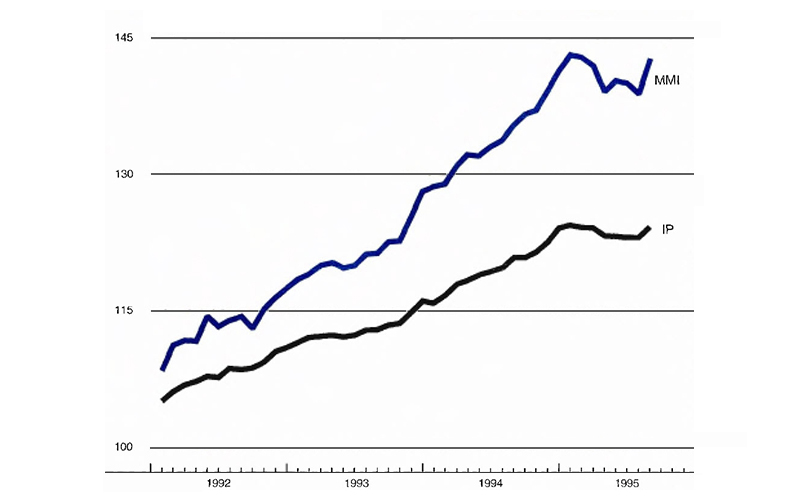

Manufacturing output indexes (1987=100)

| August | Month ago | Year ago | |

|---|---|---|---|

| MMI | 142.8 | 138.9 | 135.4 |

| IP | 124.3 | 123.1 | 120.9 |

Motor vehicle production (millions, seasonally adj. annual rate)

| August | Month ago | Year ago | |

|---|---|---|---|

| Cars | 6.1 | 6.1 | 6.4 |

| Light trucks | 5.8 | 4.6 | 5.9 |

Purchasing managers’ surveys: net % reporting production growth

| September | Month ago | Year ago | |

|---|---|---|---|

| MW | 54.5 | 52.3 | 70.2 |

| U.S. | 50.6 | 49.3 | 61.9 |

Manufacturing output indexes, 1987=100

Sources: The Midwest Manufacturing Index (MMI) is a composite index of 15 industries, based on monthly hours worked and kilowatt hours. IP represents the Federal Reserve Board industrial production index for the U.S. manufacturing sector. Autos and light trucks are measured in annualized units, using seasonal adjustments developed by the Board. The purchasing managers’ survey data for the Midwest are weighted averages of the seasonally adjusted production components from the Chicago, Detroit, and Milwaukee Purchasing Managers’ Association surveys, with assistance from Bishop Associates, Comerica, and the University of Wisconsin-Milwaukee.

One month may not constitute a trend, but Midwest manufacturing activity strengthened significantly in August. After languishing in the second quarter and into the summer, in August the Midwest Manufacturing Index posted its largest single monthly increase since January 1984. This gain was led by such cyclically sensitive output as motor vehicles, primary and fabricated metals, and industrial machinery.

Note

1 See “Economic Impact of the Chicago Exchanges,” Report of the Civic Committee to the Commercial Club of Chicago, 1987. Indirect jobs are estimated to derive from purchases by the industry of legal and other business services, as well as from expenditures in later rounds arising from payroll spending by Chicago employees.