The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

On November 12, 1999, banks received permission to become full-fledged financial service providers with the passage of the Gramm–Leach–Bliley (GLB) Act. The GLB Act permits banks and bank holding companies (BHCs) to convert to a financial holding company (FHC) structure and engage in a broader array of new activities, including merchant banking, as well as removing prior restrictions on their ability to offer insurance and securities products.

To be eligible to convert to FHC status, the firm must show both that it is viable and that it is meeting the needs of its community. The firm’s viability is demonstrated by meeting the “well-capitalized” and “well-managed” standards. Under the well-capitalized standard, all bank subsidiaries controlled by a converting BHC must have a 10% total risk-based ratio, a 6% tier 1 risk-based ratio, and a 5% tier 1 leverage ratio.1 The well-managed standard stipulates that all bank subsidiaries controlled by the converting BHC must have a rating of 1 (strongest) or 2 for their composite CAMELS ratings and the M component (a rating of management quality). A “satisfactory” Community Reinvestment Act (CRA) rating determines that the institution is meeting the needs of the community in which it operates.2

The CRA rating and the capital ratios have always been publicly available. In contrast, the composite CAMELS and M ratings are confidential. Access to these rating is limited to senior bank management and the regulatory agencies. However, since conversion to FHC status is public information, the public can infer regulatory ratings for banks and bank holding companies when they announce their FHC-conversion intentions.

On March 13, 2000, the first day applications for FHC status were approved, 117 banking firms converted. As of the end of December 2000, 342 banking firms had converted to FHC status. Of these, more than half (184) were small community banks having total assets under $500 million, and 41 were money center or superregional banks each with total assets exceeding $20 billion. Not surprisingly, most of the largest 30 BHCs had converted to FHC status as of year-end 2000.

The GLB Act created a unique opportunity for researchers to observe the market’s reaction to confidential regulatory information, which had never before been available to the public. This Chicago Fed Letter discusses findings from a study we coauthored with L. Allen, which examines how stock and bond markets react to this newly released information about regulatory ratings.3

The results of our study have a bearing on the market-discipline debate. This debate centers on a conjecture that market discipline may be more effective than regulatory discipline as the U.S. banking industry has become increasingly sophisticated. If so, then market discipline might be enhanced by making the results of bank examinations available to the public.

The decision to convert

In Allen et al. (2001), we examine characteristics that determine the decision to convert to FHC status. A variety of characteristics were considered as possible candidates, including the regulatory requirements for conversion (“well-capitalized” and “well-managed”). In addition, we find that asset size and measures of nonbank activities improve prediction accuracy.

Using these characteristics in a statistical model enables us to calculate probabilities for the likelihood of a banking firm’s conversion decision. Subsequently, by restricting the information in the statistical model to only publicly available information, we calculate probabilities that proxy for those that the market would assign for each firm’s conversion. We use these estimates to produce a two-by-two classification of what banks were expected to do versus what they did. Figure 1 summarizes the possible combinations and the number of BHCs included in the four categories.

1. Predicted vs. actual conversion

1. Converted (Predicted to convert)

22 BHCs

2. Nonconverted (Predicted to convert)

3 BHCs

3. Nonconverted (Predicted not to convert)

295 BHCs

4. Converted (Predicted not to convert)

46 BHCs

Source: Allen et al. (2001).

Placement in three of the four cells effectively releases regulatory information to the market. Converting banks release information about their “well-managed” ratings. The information released can be new or may confirm previously held opinions. For example, unsatisfactory regulatory ratings information may have been revealed by nonconverting banks that, based on public information, were expected to convert but did not convert. That is, suppose a bank can be observed to have acceptable capital ratios, CRA ratings, and current financial activities, yet it chooses not to convert. The market might reasonably infer from this choice that the regulatory rating proved to be an obstacle to conversion. Lastly, banks not expected to convert and not converting release no information about their ratings, because their decision not to convert could be based on the readily observable factors, e.g., CRA rating.

Evidence from the stock market

To gain an insight into how these decisions might affect market opinion, we constructed a sample of 366 BHCs. The sample is composed of BHCs with shares trading in the secondary market and with financial data available. The sample period begins 14 months before the earliest conversion date (January 1, 1999) and runs through the three calendar months in which conversion activity was the greatest, ending on June 30, 2000. As of June 30, 2000, 68 of these BHCs had converted to an FHC structure. Of these, our probability model assigned a high probability of conversion for 22 firms and a low probability for the 46 remaining firms. Of the 298 BHCs that had not converted by the end of June 2000, our probability model gave a low probability of conversion for 295 firms and a high probability for three firms.

To gauge the relevance of an inferred release of regulatory ratings, we examine their stock returns. We look at stock returns for three subperiods: a pre-conversion period, the conversion period, and a post-conversion period. Adjusting the BHC returns for market conditions separates the unique decisions of the individual BHCs from overall market conditions. Specifically, we adjust the BHC returns for overall stock market returns and returns on a banking index. Averaging the adjusted returns of BHCs classified according to our probability model and their actual conversion decisions allows us to assess the effects of the release of regulatory information. By looking at the three different subperiods, we can measure the excess (abnormal) returns to the shareholders of these BHCs during the pre-conversion, conversion, and post-conversion periods. Finally, we also separate the change in stock returns that may be a result of the change in risk exposure (due to the BHCs’ expanded nonbank activities after the FHC conversion) from the excess returns due to the release of regulatory information.

Our results overall suggest that the market does not use regulatory ratings to assess the quality of management of banking firms.4 The market seems to have already incorporated assessment of management quality into equity prices, and the market’s assessment does not differ from the regulatory assessment. This does not mean that the release of regulatory information was irrelevant. Rather, it appears that the market could infer from bank examination ratings the regulatory intent—what regulators know and how regulators would deal with the problems.

Regarding the risk effect, we find evidence suggesting that the new expanded bank powers increase the market’s estimate of the systematic (not diversifiable) risk of the banking firms. This may be related to concerns that, as banks expand their offerings of financial products, they may become more closely tied to the overall economy than when they focused on traditional lending products. Indeed, these results are also consistent with Allen and Jagtiani’s (2000) finding that universal banks (including a commercial bank, a securities firm, and an insurance company) face greater systematic market risk than commercial banks.5 Below, we discuss our findings for the specific groups within the BHC sample.

- Converted (predicted to convert)

This group comprises mostly large banks. Because of their publicly available capital ratios, CRA ratings, and current nonbank activities, according to our probability model the market appeared to “expect” these banking organizations to take advantage of the expanded bank powers offered under the GLB Act and to convert to an FHC structure.

There is no evidence of abnormal returns during the conversion period for this group. This is consistent with previous research, which finds that the stock market returns for BHCs with Section 20 subsidiaries (with nonbank activities) reacted positively to the passage of the GLB Act in November 1999. These banking firms were expected to convert and benefited from the GLB Act as soon as it was passed. There was no additional significant stock market premium when these banks actually converted.

- Nonconverted (predicted to convert)

Banks in this group are large, active in nonbank activities, and meet the conversion requirements in terms of capitalization and CRA rating but decided not to convert to FHC status.

There is evidence of abnormal stock returns for this group of banks during the conversion period. While this may seem contradictory, we offer a possible explanation. Consistent with Berger and Davies (1998),6 shareholders of these banks may take nonconversion as good news, since they are assured that regulators can limit the risk taking of these banking firms.

- Nonconverted (predicted not to convert)

Banks in this group are mostly small and not nationally known. These small banks were expected not to convert—possibly because they do not satisfy the well-capitalized criterion, do not have satisfactory CRA ratings, and do not currently engage in allowable nonbank activities. The fact that they did not convert, in this case, did not reveal any information on regulatory ratings to the market. Therefore, the stock market did not expect these banks to convert to FHC status and reacted positively, resulting in positive abnormal returns for these banks. However, the resulting positive abnormal returns on these banks were significantly smaller than those observed for group 2 above.

- Converted (predicted not to convert)

Similar to the previous group, most of the banks in this group are also small. These banks were not predicted to convert since they are smaller and had not participated in nonbanking activities in the past. However, these banks surprised the market by converting to FHC status, resulting in a somewhat negative reaction overall from the stock market.7

Evidence from the bond market

We also examine reactions from the bond market. Unlike shareholders, who could potentially benefit from the upside gain from a bank’s risk taking, bondholders are more aligned with bank regulators in their objectives. Thus, it is useful to observe reactions from both stock and bond markets.

The main drawback in this part of our analysis is that fewer banking firms issue publicly traded bonds, resulting in a much smaller sample of banks—down from 366 BHCs in the stock market sample to 43 BHCs in the bond market sample. The sample includes all the BHCs included in the stock market analysis that had publicly traded bonds outstanding as of June 30, 2000.

We calculated bond spreads (above those of maturity-matched Treasury securities) as of March 1, 2000, and June 30, 2000. The bonds were all subordinated, straight bonds with no calls, puts, or other options, large issues of at least $100 million, and rated by Moody’s and /or Standard & Poor’s.

We examined both bond spreads and the change in bond spreads from March 1, 2000 (just prior to the effective date of the GLB Act), to June 30, 2000 (the end of our sample period). We investigated how the spreads of BHCs in the four different groups were affected by their decision to convert to FHC structure, controlling for the risk of these banking organizations.

The empirical evidence suggests that the release of ratings had no significant impact on bond spreads. In addition, we find that spreads are smaller for converted BHCs than for those that did not convert. The FHC conversion, (although it increased systematic risk exposure to shareholders) lowered the overall credit risk exposure to bondholders— due to greater diversification across banking and nonbanking activities. Again, this is consistent with Allen and Jagtiani (2000), who find that while universal banks are exposed to greater systematic risk than commercial banks, they are more diversified and are subject to lower volatility of returns.

Conclusion

Whether regulatory information should be made publicly available is being debated. Governor Laurence Meyer describes the dilemma in the following terms:

“Public disclosure is not going to be easy for bankers because it may well bring new pressures that they may not like in the short run. … It is [also] not going to be easy on examiners because they will have to make some tough judgments. …”8

Our evidence contributes to this debate. Our finding that the market does not include examiner ratings in its valuations of bank operations suggests that instances where new information is revealed through examiner ratings will have little impact on stock values. This should assuage the concerns of bankers and lessen the likelihood of adding to the pressures placed on examiners.

We also find that markets value the restraints regulators can place on bank operations. The value of this restraint is evidenced in the positive market response to the nonconversion of banks which, based on public information, would have converted. This result sharpens our understanding of the value that can be added by bank supervision activities.

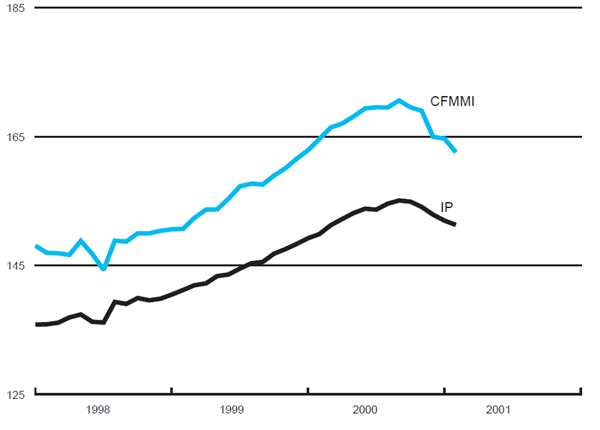

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| February | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 162.5 | 164.7 | 164.6 |

| IP | 151.3 | 152.0 | 149.9 |

Motor vehicle production (millions, seasonally adj. annual rate)

| March | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.1 | 4.8 | 5.8 |

| Light trucks | 6.1 | 5.6 | 7.1 |

Purchasing managers' surveys: net % reporting production growth

| April | Month ago | Year ago | |

|---|---|---|---|

| MW | 40.5 | 37.1 | 58.6 |

| U.S. | 42.9 | 42.8 | 58.2 |

Purchasing managers' surveys (production index)

The CFMMI declined for the fifth consecutive month in February to 162.5. This was a 1.3% decline from January’s revised level of 164.7. For the first time in five years, February’s index level was also lower than a year earlier. The Federal Reserve Board’s IP for manufacturing declined 0.4% in February after falling 0.6% in January. February output in the region was 1.2% lower than a year earlier, while output in the nation was 0.9% higher.

Auto production increased from 4.8 million units in February to 5.1 million units in March, and light truck production increased from 5.6 million units in February to 6.1 million units in March. The Midwest purchasing managers’ composite index for production increased to 40.5% in April from 37.1% in March. The purchasing managers’ index increased in Chicago and Milwaukee but decreased in Detroit. The national purchasing managers’ survey also increased from 42.8% to 42.9%.

Notes

1 These ratios are measures of the capital levels required by the regulatory agencies.

2 CAMELS is the acronym for capital, asset quality, management, earnings, liquidity, and sensitivity to interest rate risk. CAMELS ratings range from 1 to 5, with 1 being the highest. Banks are also required to adhere to the provisions of the CRA. These provisions require banks to supply financing that meets the needs of the communities in which they operate.

3 L. Allen, J. Jagtiani, and J. Moser, 2001, “Do markets react to regulatory information? Evidence of indirect disclosure of examination ratings through BHCs’ applications to convert to FHCs,” Federal Reserve Bank of Chicago, emerging issue working paper series, No. S&R-2000-9R.

4 We use a seemingly unrelated regression (SUR) analysis to estimate a system of equations.

5 L. Allen and J. Jagtiani, 2000, “The risk effects of combining banking, securities, and insurance activities,” Journal of Economics and Business, Vol. 52, No. 6, November / December, pp. 485–497.

6 A. Berger and S. Davies, 1998, “The information content of bank examinations,” Journal of Financial Services Research, Vol. 14, No. 2, pp. 117–144.

7 An exception is for those banks that converted immediately on March 13. For those banks, we observe positive abnormal stock returns during the post-conversion period, but not during the conversion period.

8 National Bureau of Economic Research, 2000, “Supervising LCBOs: Adapting to change,” paper presented at the conference on Prudential Supervision: What Works and What Doesn’t, Islamorada, FL, January 14.