Real interest rates on U.S. government bonds have declined persistently since the 1980s. U.S. government bonds are backed by the full faith and credit of the federal government and, hence, are considered one of the safest assets because the risk of default is extremely low. More broadly, interest rates on other safe assets, such as highly rated corporations, have also declined.

In stark contrast, the return on more risky assets does not appear to have declined significantly. For instance, the return on private capital, i.e., profit made per unit invested (for the economy as a whole), appears to have remained roughly stable.1 So the difference, or spread, between the returns on risky assets and the returns on safe assets has increased.

In this Chicago Fed Letter, we analyze why this spread has increased, based on a framework we developed in a recent research paper (Farhi and Gourio, 2018) and highlight some of our findings.

Why is it worthwhile to study the evolution of this spread? A lot of research has tried to explain why returns on safe assets are so low. One popular theory is that this reflects a higher desire to save related to an aging population and rising longevity. As the average worker in the U.S. (and elsewhere) gets older, they increase their savings rate to prepare for retirement.2 However, this theory cannot explain why the return on private capital has not fallen by the same amount. Hence, it is useful to consider explanations for the decline of the return spread.

Potential drivers of the return spread

In theory, one would expect businesses to expand investment up to the point where the return on capital equals the safe interest rate. Low interest rates should have stimulated investment, leading to an economic expansion until the return on capital is as low as the safe interest rate. This expansion of course did not happen. Why not? We consider four potential causes.

The first possible cause is that firms are underinvesting because of limited competition, i.e., monopolistic behavior. Facing limited competition, firms prefer to increase prices, which reduces demand for their product and, hence, the need for output; this in turn limits the need for new production capacity. We call this the rents story. This story has received significant support in recent studies (see Furman and Orszag, 2015; Barkai, 2017; Gutiérrez and Philippon, 2017; De Loecker and Eeckhout, 2017; and Eggertsson, Robbins, and Wold, 2018, among others).

The second possible cause is that investors have become more concerned about risk and, therefore, their preference for the safety of U.S. government bonds over investment in private capital has increased. Investing in private capital is undoubtedly more risky than investing in U.S. government bonds, leading investors to require a higher return to invest in private capital—a risk premium wedge. If investors perceive risk is increasing or become more risk averse, this wedge increases. We call this the risk premium story (see, for instance, Caballero and Farhi, 2018; Caballero, Farhi, and Gourinchas, 2017; Del Negro et al., 2017; and Marx, Mojon, and Velde, 2018).3

The third possible cause is that technological change is affecting the return on capital—e.g., through changes in the cost of buying new capital goods, changes in physical depreciation, or changes in the production process. For instance, a large share of capital now takes the form of information technology (hardware or software), which is becoming cheaper over time and tends to depreciate quickly. These trends tend to reduce the return on capital. We call this the technology story.

The fourth possible cause is that the difference between returns on safe assets and returns on risky assets is driven by mismeasurement, and that there would be no difference if we measured capital assets properly. The reason why mismeasurement may have grown is that capital assets have become more “intangible” over time. Historically, the majority of capital was made up of physical assets, such as plant and equipment used for production. These physical assets are rather well measured. But there has been a growing shift toward “intangible” forms of capital, such as patents, brands, and customer base, and firm-specific human capital, which are not so well measured. It is plausible that we underestimate the quantity of capital because we do not properly measure intangible capital, and it is also plausible that this underestimation bias has grown over time. In that case, we would overestimate the return on private capital (since we underestimate the denominator). Thus, the true return on capital may well be low, and in reality there may be no wedge between the return on private capital and the risk-free rate. We call this the intangible story (see, e.g., Crouzet and Eberly, 2018).

Accounting framework

In our 2018 research paper, we used a simple accounting framework to examine the first three stories: rents, risk premium, and technology. Then we adapted the model to account for the intangible story. Our framework builds on the standard neoclassical growth model, the backbone of modern macroeconomics, which is often used to describe the interactions of investment, output, capital, and labor. Economists often abstract from risk, i.e., uncertainty about future outcomes, when using this model. Our main innovation is to introduce risk in a tractable manner, which allows us to analyze the risk premium story. Besides investment, output, capital, and labor, the model can hence also be used to assess financial variables, such as the price–dividend ratio of the stock market or the safe (risk-free) interest rate in our model.

This model can be used to infer which of the causes accounts for the observed changes in the data—and, importantly, the lack of changes in some variables. In this paragraph, we summarize the technical details of our approach. Then we move on to discussing our findings. The first step is to note that our model embeds the Gordon growth formula, which is described in the box. We can use this formula to infer the risk premium on private capital from the observed growth rate of gross domestic product (GDP), the safe interest rate, and the price–dividend ratio of the U.S. stock market. In a second step, given this risk premium and the observed depreciation and cost of new investment, we can construct a measure that we call the frictionless user cost of capital. This measure represents the cost to rent capital for one year. If competition between firms were perfect, this user cost would equal the return on private capital, but if there is market power, the user cost will be lower than the return on capital. We can deduce the market power (or monopoly power) necessary to be consistent with the observed return on capital. Finally, in our third step we infer the technological bias required to match the labor share of national income. Technological change can be biased toward labor (i.e., make labor relatively more productive) or toward capital (i.e., make capital relatively more productive), or be neutral. Hence, our approach uses macroeconomic and financial data jointly to disentangle the rents (market power), risk premium, and technology stories.

We also incorporate other factors that are important to understanding the evolution of the economy: the increase in savings supply, change in productivity growth, investment prices, depreciation, and changes in population and employment. These factors affect the quantities we need to look at (such as the labor share or the return on capital) in order to study the spread.

Analyzing the sources of the rising return spread

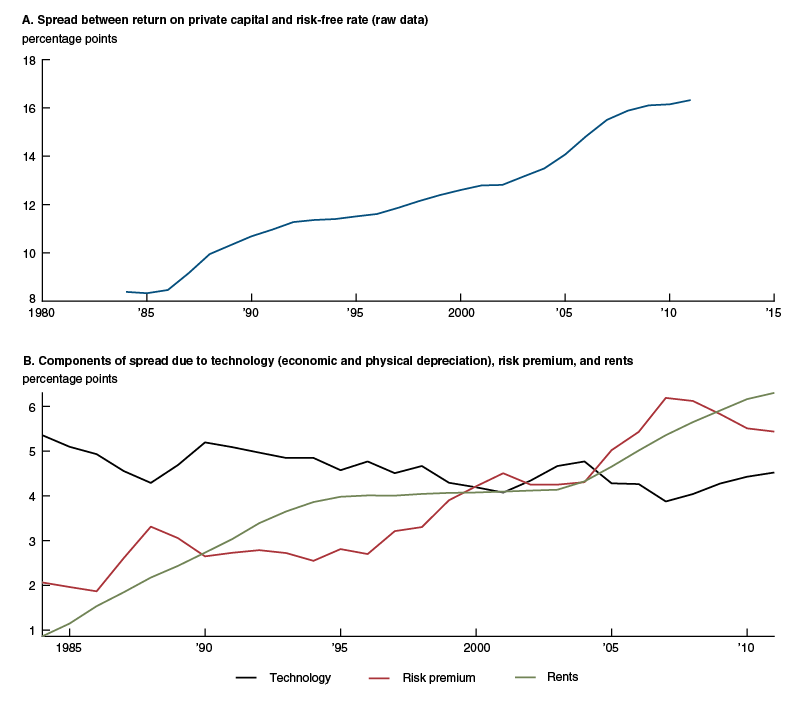

Our main finding, summarized in figure 1, is that the rents and risk premium stories are the most important in helping us to understand the return spread trends of the past 30 years. The top panel of figure 1 depicts the raw data: the spread between the rate of return on private capital and the safe (risk-free) interest rate. The bottom panel of figure 1 depicts the three components of the spread corresponding to technology, the risk premium, and rents, as inferred from our accounting framework. We find that the technology component is stable and, hence, does not account for the increase in the return spread that we observe during this period. But both the risk premium and rents stories play significant and roughly equal roles in accounting for the increase in the spread during the past 30 years. In figure 2 we compare the 1984–2000 and 2001–16 periods. We find that the spread increases by about 4 percentage points, with roughly half due to rising rents and half due to rising risk.

Figure 1. Sources of the return spread

Source: Authors’ calculations.

2. Rates of return

|

|

1984–2000 |

2001–16 |

Change |

|

Return spread |

11.2 |

15.2 |

4.0 |

|---|---|---|---|

|

– Component due to technology |

4.6 |

4.4 |

–0.2 |

|

– Component due to rents |

3.4 |

5.5 |

2.1 |

|

– Component due to risk premium |

3.1 |

5.2 |

2.1 |

|

Risk-free rate |

2.8 |

–0.3 |

–3.1 |

|

Expected stock return |

5.9 |

4.9 |

–1.0 |

Why do we reach this conclusion? As we mentioned, the risk premium on private capital is inferred from the Gordon growth model (using equation 3 in the box). In the data, the risk-free rate fell considerably more than the growth rate, while the dividend yield only fell modestly. Hence, the risk premium must have risen. This increase in the risk premium only accounts for about half of the measured increase in the profitability of capital, and so the rest must be explained by an increase in market power. This increase in market power is roughly consistent with the decline in the labor share, leaving little role for technological bias.

On the one hand, this method may seem exceptionally simple or even naive. However, we show in our research paper that these results are consistent with a broad set of results that also show the risk premium has increased (e.g., Duarte and Rosa, 2015). Still, we recognize that this increase in the risk premium ultimately needs to be explained and understood better.

On the other hand, if we had abstracted from risk, like many researchers before us, we would have reached some unsettling conclusions. First, without an increase in risk, the increase in market power needed to match the observed behavior of the return on capital is about twice as large, which seems implausible. Second, this increase in market power leads, by itself, to a huge decline in the labor share, so the model requires technology to become more labor biased to match the moderate decline in the labor share. This seems counterintuitive in light of the many studies that emphasize that technological progress has favored capital (machines) over labor (at least unskilled labor) over the past 30 years.

Finally, note that the total return on stock is the sum of the risk premium and the risk-free rate (as in equation 2 in the box). The risk premium increases by about 2.1 percentage points, but the risk-free rate falls by about 3.1 percentage points, so the overall expected return on the stock falls by about 1 percentage point.

Other implications of our results

Our model has a number of implications, in addition to the return spread. We illustrate these results in figure 3, which shows the average of some macroeconomic or financial variable statistics in the periods 1984–2000 and 2001–16, changes in these variables between the two periods, and how much of the change our framework attributes to each factor (rents, risk, savings supply, or other factors).

3. Decomposing the changes in observed macroeconomic and financial variables

|

|

|

|

|

Role of each factor: |

|||

|

|

1984–2000 |

2001–16 |

Change |

Rents |

Risk |

Savings supply |

Other factors |

|

Investment–output (percentage points) |

17.3 |

16.5 |

–0.8 |

–1.0 |

–0.9 |

2.2 |

–1.1 |

|---|---|---|---|---|---|---|---|

|

Output (%) |

-- |

-- |

–0.3 |

–1.9 |

–1.7 |

4.2 |

–0.9 |

|

Risk-free rate |

2.8 |

–0.3 |

–3.1 |

0.0 |

–1.6 |

–1.2 |

–0.3 |

|

Price–dividend ratio |

42.3 |

50.1 |

7.8 |

0.0 |

–13.2 |

30.1 |

–9.1 |

|

Tobin’s Q |

2.5 |

3.8 |

1.3 |

1.3 |

–0.5 |

1.0 |

–0.5 |

One key question is why investment did not rise, given the low safe interest rate. Figure 3 reports the share of output that is invested (the investment–output ratio). This ratio fell from 17.3% to 16.5%, a decline of 0.8 percentage points. Our model suggests that offsetting factors are at play. On the positive side, a rising savings supply (e.g., related to an aging population) increased the investment–output ratio by 2.2 percentage points. On the negative side, rising rents and risk lowered it by 1.0 and 0.9 percentage points, respectively, while other factors (such as growth, technology, and depreciation) lowered it by 1.1 percentage points.

Second, our model can shed light on the drivers of the decline in the safe risk-free interest rate. As it turns out, over half of the total risk-free rate decline is due to the higher risk premium. When investors are more fearful, they embrace safe assets, pushing their returns down. The higher savings supply is the other prominent factor affecting the risk-free interest rate.

Third, what explains the changes in stock market value? We can consider either the price–dividend ratio or Tobin’s Q, the ratio of the stock market value to the quantity of physical assets. The price–dividend ratio rose modestly from the first period, 1984–2000, to the second one, 2001–16; this rise was due to higher savings supply, offset by higher risk premiums, and lower growth. Tobin’s Q capitalizes the rents, so it rose significantly both because rents rose and also because of the decline in the discount rate at which these rents were capitalized.

Fourth, what about the overall effect on production, i.e., GDP? Higher rents and higher risk premiums depressed output because of lower capital accumulation (–1.9 percentage points and –1.7 percentage points, respectively), though here again, the offsetting effect of rising savings supply (plus 4.2 percentage points) led to a small overall effect (–0.3 percentage points).

Incorporating the intangible story

To incorporate the intangible story, we adapt our model to allow for mismeasurement in capital and assume that a growing fraction of investment is not measured. Specifically, we assume that during the period 1984–2000, 10% of investment was not counted, and this rose to 20% during the period 2001–16. With this assumption, we repeat our estimation and obtain the results in figure 4. A component of the spread is now due to mismeasurement, and this component rises over time, from 0.7 percentage points to 1.6 percentage points, so it accounts for about one-quarter of the increase. The importance of rents is then smaller in this analysis: Higher rents only account for 1.2 percentage points of the increase, which is less than the 2.1 percentage points in figure 2 (which abstracted from intangibles). In contrast, the components attributed to risk and technology remain constant. Hence, incorporating the accumulation of intangibles story reinforces our main conclusion that a higher risk premium plays a prominent role in explaining the evolution of the spread between the return on private capital and the risk-free rate.

4. Incorporating intangibles

|

|

1984–2000 |

2001–16 |

Change |

|

Return spread |

11.2 |

15.2 |

4.0 |

|---|---|---|---|

|

– Technology |

4.6 |

4.4 |

–0.2 |

|

– Rents |

2.8 |

4.0 |

1.2 |

|

– Risk |

3.1 |

5.2 |

2.1 |

|

– Intangibles |

0.7 |

1.6 |

0.9 |

Conclusion

Of the four stories we examined, we found that risk premiums and rents played the most significant roles in explaining trends in asset returns, savings, and investment over the past 30 years. One important question left open for future research is why risk premiums have risen. Indeed, it is not obvious that risk has risen. For example, there has been little increase in stock market volatility during this period. We conjecture that several factors might be at play. Some of these factors increased perceived risk, while others reduced investors’ willingness to bear risk (i.e., increased risk aversion). Perceived risk has likely been higher after the sequences of financial crises in emerging markets in the 1990s and in developed markets in the 2000s. Effective risk aversion may also be higher due to an aging population, heightened precautionary behavior of emerging market investors, or changes in regulation.

Box 1. The Gordon growth model

Financial economists posit that the price of a stock equals the present discounted value of its dividends. A special case of this is the Gordon growth formula, which is written as

$1)\text{ }\frac{P}{D}=\frac{1}{r-g},$where $P$ is the stock price and $D$ is the dividend, $r$ is the expected return on the stock, and $g$ is the growth rate of dividends. (This formula can be derived under the assumptions that dividends follow a random walk and that the expected return on the stock is constant.) We apply this formula to the entire U.S. stock market and equate $g$ with the growth rate of GDP. We can decompose the expected return on the stock as the sum of the safe (risk-free) interest rate $rf$ and a risk premium $rp$:

$2)\text{ }r=rf+rp,$and hence by manipulating equation 1, we can write:

$3)\text{ }rp=\frac{D}{P}+g-rf.$This equation allows us to infer the risk premium from the observed price–dividend ratio, growth rate, and risk-free rate.

1 For a measurement of this return, see Gomme, Ravikumar, and Rupert (2015).

2 For an example of this theory, see Carvalho, Ferrero, and Nechio (2016).

3 Relatedly, the compensation for the special liquidity of government bonds may also have increased. However, the quantitative magnitude of this increase is likely limited. We infer this from the limited increase in the spread between government bonds and other safe, but less liquid assets, such as highly rated corporate bonds.

References

Barkai, Simcha, 2017, “Declining labor and capital shares,” London Business School, working paper, available online.

Caballero, Ricardo J., and Emmanuel Farhi, 2018, “The safety trap,” Review of Economic Studies, Vol. 85, No. 1, January, pp. 223–274. Crossref

Caballero, Ricardo J., Emmanuel Farhi, and Pierre-Olivier Gourinchas, 2017, “Rents, technical change, and risk premia accounting for secular trends in interest rates, returns on capital, earning yields, and factor shares,” American Economic Review, Vol. 107, No. 5, May, pp. 614–620. Crossref

Carvalho, Carlos, Andrea Ferrero, and Fernanda Nechio, 2016, “Demographics and real interest rates: Inspecting the mechanism,” European Economic Review, Vol. 88, September, pp. 208–226. Crossref

Crouzet, Nicolas, and Janice Eberly, 2018, “Understanding weak capital investment: The role of market concentration and intangibles,” paper presentation at the Federal Reserve Bank of Kansas City Jackson Hole economic policy symposium, Changing Market Structures and Implications for Monetary Policy, Jackson Hole, WY, August 24, available online.

De Loecker, Jan, and Jan Eeckhout, 2017, “The rise of market power and the macroeconomic implications,” National Bureau of Economic Research, working paper, No. 23687, August. Crossref

Del Negro, Marco, Domenico Giannone, Marc P. Giannoni, and Andrea Tambalotti, 2017, “Safety, liquidity, and the natural rate of interest,” Brookings Papers on Economic Activity, Spring, pp. 235–294, available online.

Duarte, Fernando, and Carlo Rosa, 2015, “The equity risk premium: A review of models,” Federal Reserve Bank of New York, staff report, No. 714, February, available online.

Eggertsson, Gauti B., Jacob A. Robbins, and Ella Getz Wold, 2018, “Kaldor and Piketty’s facts: The rise of monopoly power in the United States,” National Bureau of Economic Research, working paper, No. 24287, February. Crossref

Farhi, Emmanuel, and François Gourio, 2018, “Accounting for macro-finance trends: Market power, intangibles, and risk premia,” Brookings Papers on Economic Activity, forthcoming.

Furman, Jason, and Peter Orszag, 2015, “A firm-level perspective on the role of rents in the rise in inequality,” paper presentation at the colloquium, A Just Society: Centennial Event in Honor of Joseph Stiglitz, Columbia University, New York, October 16, available online.

Gomme, Paul, B. Ravikumar, and Peter Rupert, 2015, “Secular stagnation and returns on capital,” Economic Synopses, Federal Reserve Bank of St. Louis, No. 19. Crossref

Gomme, Paul, B. Ravikumar, and Peter Rupert, 2011, “The return to capital and the business cycle,” Review of Economic Dynamics, Vol. 14, No. 2, April, pp. 262–278. Crossref

Gutiérrez, Germán, and Thomas Philippon, 2017, “Declining competition and investment in the U.S.,” National Bureau of Economic Research, working paper, No. 23583, July. Crossref

Marx, Magali, Benoît Mojon, and François R. Velde, 2018, “Why have interest rates fallen far below the return on capital,” Federal Reserve Bank of Chicago, working paper, No. 2018-01, January 25, available online.