The reduction of carbon emissions is a critical part of the transition to a more sustainable economy. Reducing carbon emissions is expected to lead to fewer natural disasters, lower energy transitions risk, and a lower impact on financial risks resulting from physical damage caused by climate change.

The tools available to policymakers to reduce carbon emissions include implementing incentives and putting a price on carbon. Reliable and transparent tracking of carbon will help drive reductions in emissions by providing a way for policymakers and other stakeholders to assess the effectiveness of incentives and to price carbon more accurately. In addition, there is a market in voluntary emissions trading that is expected to grow as efforts to reduce carbon emissions intensify.

In this Chicago Fed Letter, we build on nascent literature to illustrate how new technologies, such as distributed ledger technology (DLT), could lead to a more accurate assessment of the effectiveness of incentives and improve the accuracy of the pricing of carbon emission credits, resulting in the reduction of carbon emissions. To that end, we identify the challenges in carbon accounting and then explore whether DLT is a viable solution to ensuring accurate information is available to carbon markets.

Measuring carbon emissions

An accurate and reliable measuring of carbon emissions can contribute to a reduction in carbon emissions. Accurate and reliable carbon accounting enables policymakers and other stakeholders to assess the effectiveness of the steps they take to reduce emissions. For example, in August 2022 the U.S. Congress passed the Inflation Reduction Act of 2022 (IRA). The IRA is the largest step to address climate change in the United States in many years, and it focuses primarily on incentives. The goal of the act is to put the U.S. on a path to reduce emissions 40% by 2030. Measuring carbon emissions can be an important component of knowing whether this goal is being met.

As another example, the European Union, California, and an alliance of eastern and Mid-Atlantic states in the U.S. called the Regional Greenhouse Gas Initiative (RGGI), have adopted the approach of establishing a price on carbon, through a cap-and-trade approach, coupled with incentives. In a cap-and-trade system, also referred to as a “compliance” market or system, permits are issued to allow up to a specified total amount of carbon emissions for a given geographical area, and firms can trade these permits. This results in the market determining the price of carbon emissions, given a cap on permits determined by policymakers.

Market participants may also trade emissions allowances independently of a mandate by policymakers. This type of emissions trading activity is called “voluntary markets.” Here, the incentive is the desire by a corporation to comply with a commitment to sustainability. Typically, a corporation would acquire emissions allowances on a voluntary basis if it has pledged to reduce its emissions but is unable to achieve its own targets due to supply chain or other issues. The Taskforce on Scaling Voluntary Carbon Markets, an alliance of private sector participants, is working to increase the size of the voluntary markets over the next few years to create an alternative to compliance markets. According to one estimate, the voluntary market for carbon credits could be worth up to $50 billion by the end of this decade. Rules such as incentives for emission reduction or carbon pricing, as well as private sector efforts to reduce emissions, make it important to have a reliable and accurate way to track emissions.

The purpose of our research is to explore how DLT can be used to improve the accuracy and reliability of carbon accounting. More accurate carbon accounting would lead to a better understanding of the effectiveness of incentives, a more accurate understanding of the social cost of carbon, and a more accurate pricing of carbon offsets. In this context, it is essential to accurately measure firms’ carbon emissions as well as offsetting activities that absorb carbon, such as planting forests. This accounting is challenging because of a lack of transparency and reliability in the methods used to calculate the carbon footprint of a given product or service.

A common measure of the social cost of carbon is the monetary value of the economic damages that result from emitting an additional metric ton of greenhouse emissions in a given year. U.S. federal agencies use estimates of this measure to assess the likely impact of regulation on greenhouse gas emissions. The assumptions behind these estimates are detailed in technical support documents that have been issued and updated over the years. The common thread in the various U.S. federal estimates of the social cost of carbon since 2010 is that no matter what the assumptions are, all estimates predict a substantial increase of the social cost of carbon over the years to 2050. The 2021 estimate by the Interagency Working Group on Social Cost of Greenhouse Gases puts the social cost of carbon at $56 per metric ton of carbon dioxide (CO2) by 2025 and $85 per metric ton of CO2 by 2050 (in 2020 dollars, at a 3% discount rate). These consistently higher estimates for the future social cost of carbon are largely driven by expectations of increasing costs of climate-related damage.

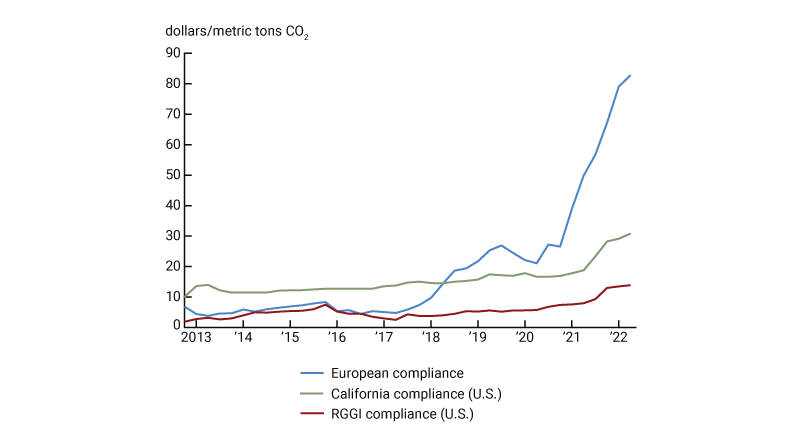

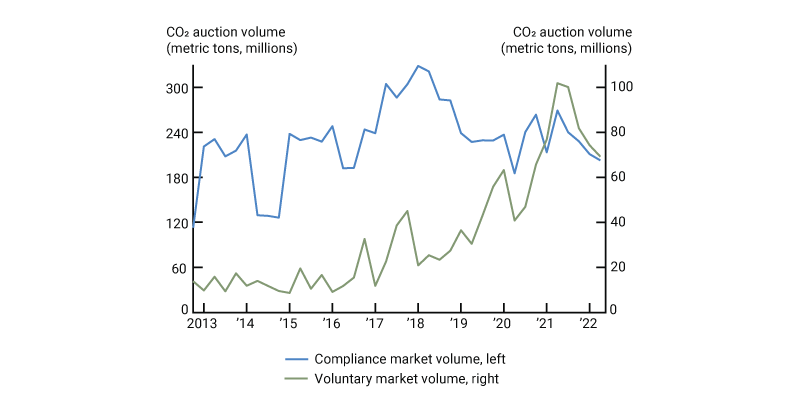

Financial markets can perform a price discovery and risk allocation function in determining the price of carbon emissions, whether in compliance markets or in voluntary markets. Many factors affect trading in a cap-and-trade system, including assumptions about the number of permits that policymakers will allow in a given geographical area at a given time. Another important factor in both cap-and-trade and voluntary carbon markets is the reliability of the data available. In order to properly function, financial markets need accurate and reliable data, allowing market participants to make informed decisions (Fama, 1970; and Morningstar). Prices (figure 1) and trading volumes (figure 21) for emission allowance trading in compliance markets around the world have risen over the past eight years. In figure 1, we track the price of carbon emission permits in the eurozone and in U.S. compliance markets. Figure 2 shows the auction volume for global compliance and voluntary carbon markets. What can be done to improve the transparency, quality, and reliability of carbon accounting?

1. Compliance markets auction prices

Sources: Bloomberg, California Air Resources Board, Regional Greenhouse Gas Initiative, and authors’ calculations.

2. Compliance and voluntary carbon markets by volume

Sources: Bloomberg, California Air Resources Board, Regional Greenhouse Gas Initiative, Verified Carbon Standard, American Carbon Registry, Climate Action Reserve, Gold Standard Registry, and authors’ calculations.

Supply chain transparency, carbon offsetting, and the trouble with carbon accounting

Determining the carbon impact of the various steps in the supply chain related to a given commodity or product is difficult. Firms that are part of the supply chain, consumers, and other market participants have limited visibility into the carbon impact of each step in the supply chain. Supply chain transparency is vital for understanding where materials come from and where they travel to. However, given that carbon emissions are interchangeable and homogenous products, it can be a challenge to confirm the carbon footprint of a given commodity or product, as multiple sources of carbon emissions may find their way to the same manufacturing facility or endpoint of consumption. Consider the production of a washing machine. The components of that washing machine may come from different sources, and each manufacturer of those components may have a different approach to carbon emissions. With diffuse production, and more centralized processing or consumption, companies may have incomplete information about how a given item was produced or sourced.

Global supply chains are facing growing scrutiny as investors and customers focus on better environmental, social, and governance (ESG) standards and demand improved supply chain transparency (Harvard Law, 2020; and Bolstad et al., 2020). Depending on the commodity, traceability and supply chain transparency are more or less difficult (Gardner et al., 2019). For example, the traceability of some energy sources is somewhat straightforward: Oil production from western Canada travels mostly via pipeline and rail between two countries (Canada and the U.S.), with well-established environmental and transportation laws, regulations, and tracking (Canada Energy Regulator, 2021; U.S. Energy Information Administration, 2020). For other commodities, such as cobalt, traceability is far more difficult (Harvard Business Review, 2016).

The embodied carbon in the products we consume or the services we enjoy is a commodity and the supply chains for that associated carbon can be even more complex than the product or service in the supply chain itself. The type of electricity in a manufacturing process, e.g., coal versus renewable energy (IPCC1), the mode of transportation (IPCC2), or the distance traveled from point of origin (Greene, Jia, and Rubio-Domingo, 2020) can all contribute to the carbon emitted for a given product or service. As a result of this complexity, accounting systems and professional sub-disciplines have been established to manage global carbon accounting (Ascui, 2014; and GHG Protocol). However, much progress has yet to be made in terms of both the accounting of carbon output and the auditing of that accounting (Csutora and Harangozo, 2017).

Policymakers could try to reduce carbon emissions by taxing them or requiring emissions permits at the source. However, if policymakers wanted to tax or impose permit requirements on utility companies, it would still be necessary to improve carbon accounting and transparency to determine accurately, defensibly, and with transparency how much carbon was emitted in the manufacturing and transport process. Improvements in carbon accounting and transparency could provide more reliable information that could be used by governments to better target a tax on carbon or a requirement for emissions permits. The consumer or investor may also want to know how much carbon is in a product or service, separately from a higher price induced by taxes or permit requirements, and that also requires reliable and transparent carbon emissions data.

Potential issues with carbon accounting can also manifest in other ways, such as in the case of carbon offsets. Carbon offsets are environmentally sustainable activities that result in avoiding, reducing, or sequestering carbon emissions and can be used to balance out a company’s carbon footprint. Some examples of carbon offsets are reforestation, investments in renewable energy, energy-efficient community projects, and waste-to-energy projects. Given that the value of a carbon offset derives from its ability to avoid, reduce, or sequester carbon emissions, accurate carbon accounting may improve on the chances of making sure a given unit of carbon offset is sold only once and not double-counted, making sure the carbon-offsetting activities actually happen, and preventing forgery of carbon offsets.

As investors and customers focus on sustainability, and as policymakers assess the impact of incentives like those introduced by the IRA, there are growing concerns about “greenwashing,” meaning the potential lack of accuracy of claims made by companies about the extent to which their products and services are environmentally sustainable. There is a need to develop a set of criteria to determine whether a product or service is environmentally sustainable, as well as a process to determine whether those criteria are met and whether a company’s statements about the sustainability of its practices are accurate.

Reliable carbon accounting and transparent carbon disclosures would enable markets to track carbon emissions accurately and enhance an economy’s ability to efficiently determine the cost to society and the market value of carbon emissions. An informational mismatch may exist between the actual emissions taking place throughout the global economy (by companies, countries, and individuals) and what is disclosed to markets, investors, and consumers. Reliable carbon accounting and disclosures are similar to public financial information issued by large companies. Investors need reliable financial information to make informed investment decisions. Similarly, reliable carbon emissions information would enable market participants to make better-informed decisions about the products they purchase or the environmental impacts of the companies they invest in.

The reliability of carbon disclosures and accounting could be improved in a number of ways. A central authority could issue disclosure rules and monitor compliance, and a recent proposed rulemaking by the Securities and Exchange Commission in the area of climate change disclosures for companies under its jurisdiction is an example of that central authority. Here, we explore whether technology could also offer a possible solution, either as an alternative to a central authority or as an additional check and balance on the sustainability of certain products and services.

Designing a system to improve transparency

Distributed ledger technology (DLT) is a potential solution to the issues with carbon accounting and disclosure that we have identified here. DLT refers to the digital transfer, storage, and management of transactional data across a decentralized network of computer servers, known as nodes. The servers share the same data records every time a node makes a change to the ledger and that change is agreed to by a predetermined consensus mechanism, allowing for computational integrity in a circumstance where there is no trusted central party. At its core, a distributed ledger combines technical protocols to validate transactions and ensure all participant submissions or linked individual ledgers are in agreement, therefore creating a single truth among decentralized participants. Moreover, DLT can ensure that data stored on the ledger is secure and tamper resistant through cryptography.

DLT presents two distinctive advantages: 1) a decentralized network of nodes sharing the same copy of the same data in a resilient and tamper-resistant digital infrastructure, and 2) a digital solution, which is suitable for leveraging automation, such as smart contracts to reduce the possibility for human error in processing, e.g., checking if a washing machine meets certain preset “green” criteria or whether a given “green bond” meets the eligibility criteria of a portfolio designed to meet certain preset sustainability standards.

Proponents of DLT for carbon accounting suggest that publicly available, traceable, tamper-resistant data can augment traditional markets and create usable information for those trying to track carbon emissions and offsets despite these constraints. In a world where there is no central authority to issue disclosure rules and monitor compliance, a mechanism for the transparency of information is paramount to successful carbon pricing. DLT could provide the underpinning of a transparent accounting process, where parties are able to submit their data onto a shared tamper-resistant ledger. Additionally, this ledger could be cross-jurisdictional, alleviating the possibility of siloed information based on different jurisdictional requirements. Leveraging DLT could enhance the reliability of the information and the resiliency of the system. Given increased concerns over cybersecurity, having several copies of the same ledger housed in several different nodes is more reliable than housing a single copy in a centralized location, although the system is only as reliable as its components. Finally, allowing for automated inputs onto a distributed ledger may facilitate additional efficiencies, such as allowing satellites and sensors to upload the data into a distributed ledger through an application programming interface (API) without the need for manual intervention.

DLTs face an inherent constraint: The technology itself can only be as transparent and tamper resistant as the data it is given. If several large organizations all band together and decide to report incorrect data, the ledger has no inherent enforcement mechanism to address that behavior. The success of DLT relies on the assumption that the risk of potential reputational harm will reduce bad behavior among data providers. However, additional safeguards may be necessary. There are certain assumptions supporting the notion that DLT will improve carbon accounting transparency and the functioning of global carbon markets. First, there is the assumption that everyone will be able to read the ledger to enforce accountability. However, some companies might not agree to letting competitors see their accounting statements. To provide incentives for companies to use the system and to prevent them from providing their own data only for the purpose of acquiring access to other companies’ information, the ledger may have to be designed so that not everyone can read it. This would represent a potential trade-off: enough transparency to ensure accountability versus enough privacy to ensure adoption. A successful system would need to achieve such a balance.

Another potential drawback of using DLT to track carbon emissions is the carbon footprint of the technology itself. Early developers used proof-of-work (PoW) as a consensus mechanism where the participants prove that they have expended the energy necessary to resolve computational challenges. Given the computational energy required to resolve these computational challenges, PoW has been shown to be a very energy-intensive mechanism and thus recent projects have chosen alternative consensus mechanisms. One common alternative is the proof-of-stake (PoS) approach, where participants in the consensus mechanism put a certain amount of a given cryptocurrency at stake and risk losing their staked currency if they do not behave in accordance with the rules of the consensus mechanism.

Conclusion

We have talked about how distributed ledger technology may help to improve climate outcomes by solving one piece of the puzzle—the need for verifiable, accurate, and transparent data on carbon supply chains. Technologies such as DLT may also help to assess the impact of carbon reduction incentives and to improve market efficiency and pricing. Moreover, as technologies continue to progress, it is not impossible to imagine a world where siloed processes in tracking climate activities are integrated into a more integrated digital ecosystem, possibly including wallets, universal resource identifiers, and distributed identifiers. Until then, there still may be a role for technology to make more incremental improvements in the pursuit of improving climate change transparency.

Many thanks to Jahru McCulley, Sophia Lansell, and Nahiomy Alvarez for research assistance in the preparation of this article.

Notes

1 In figure 2, the compliance market volume is the total quantity of carbon allowances auctioned and traded (in metric tons) on the Emission Trading Systems (ETS) operating in Europe and North America from 2012 to 2022 In Europe, the European Energy Exchange (EEX) is the main auction and trading platform for the EU ETS. The EU ETS accounts for about 90% of the global value in the compliance market for carbon allowances. In this calculation of compliance market volume, we also included volumes for RGGI and the California cap-and-trade program operated by the California Air Resources Board (CARB), which linked with the cap-and-trade system of Québec in 2014. The voluntary market volume is the total quantity of offset credits issued by carbon offset registries from 2012 to 2022. The voluntary registries currently in operation include the American Carbon Registry (ACR), the Climate Action Reserve (CAR), the Gold Standard Registry, and the Verified Carbon Standard (VCS) registry. These registries track offset projects and issue offset credits for each metric ton of CO2 reduced or removed. Other carbon registries in operation that are not included in the figure include the Plan Vivo Registry, Social Carbon Registry, and the Climate, Community & Biodiversity Standards (CCBS).