Minority depository institutions (MDIs) provide essential financial services to historically underserved communities. They are also often deeply ingrained in their local market areas, actively contributing to community development through small business lending, affordable housing initiatives, and support for economic revitalization. By facilitating access to credit and financial services, these institutions aid wealth creation for minority households, which may narrow racial wealth gaps and foster economic equity.

In a previous article, we analyzed the role of MDIs in their primary local service areas. We compared the location and performance of MDIs with non-MDI peers and found that MDIs are more likely to be mission-driven (i.e., community development financial institutions or CDFIs), which means their service areas tend to have higher poverty rates and other measures of distress. Moreover, even within similar markets, MDIs lend to customers with more economic and credit constraints than those served by non-MDIs. We found that MDIs were strongly affected by the housing market crash of 2007–10 and disproportionately failed due to losses on real estate and small business loans. We also documented MDIs’ challenges related to diminished funding sources, such as core deposits, high expenses relative to earnings, and lower capital compared to their peers over that period.

Here, we update some of those findings, highlight trends in the number of MDIs, and discuss some key performance measures to assess the state of the sector. Finally, we outline some initiatives by policymakers and others to support MDIs.

State of the MDI sector

The Federal Deposit Insurance Corporation (FDIC) provides two definitions of how FDIC-insured commercial banks and savings associations might qualify for MDI status: “(1) 51 percent or more of the voting stock is owned by minority individuals; or (2) a majority of the board of directors is minority and the community that the institution serves is predominantly minority. Ownership must be by U.S. citizens or permanent legal U.S. residents to be counted in determining minority ownership.”1 Regulators categorize minority ownership into five broad racial or ethnic groups: African American, Asian, Hispanic, Native American, and Multi-Racial American. As of 2021, the FDIC supervised more than 60% of MDIs ; the Office of the Comptroller of the Currency (OCC) supervised 24%, and the Federal Reserve supervised 10%, representing just 14 MDIs.

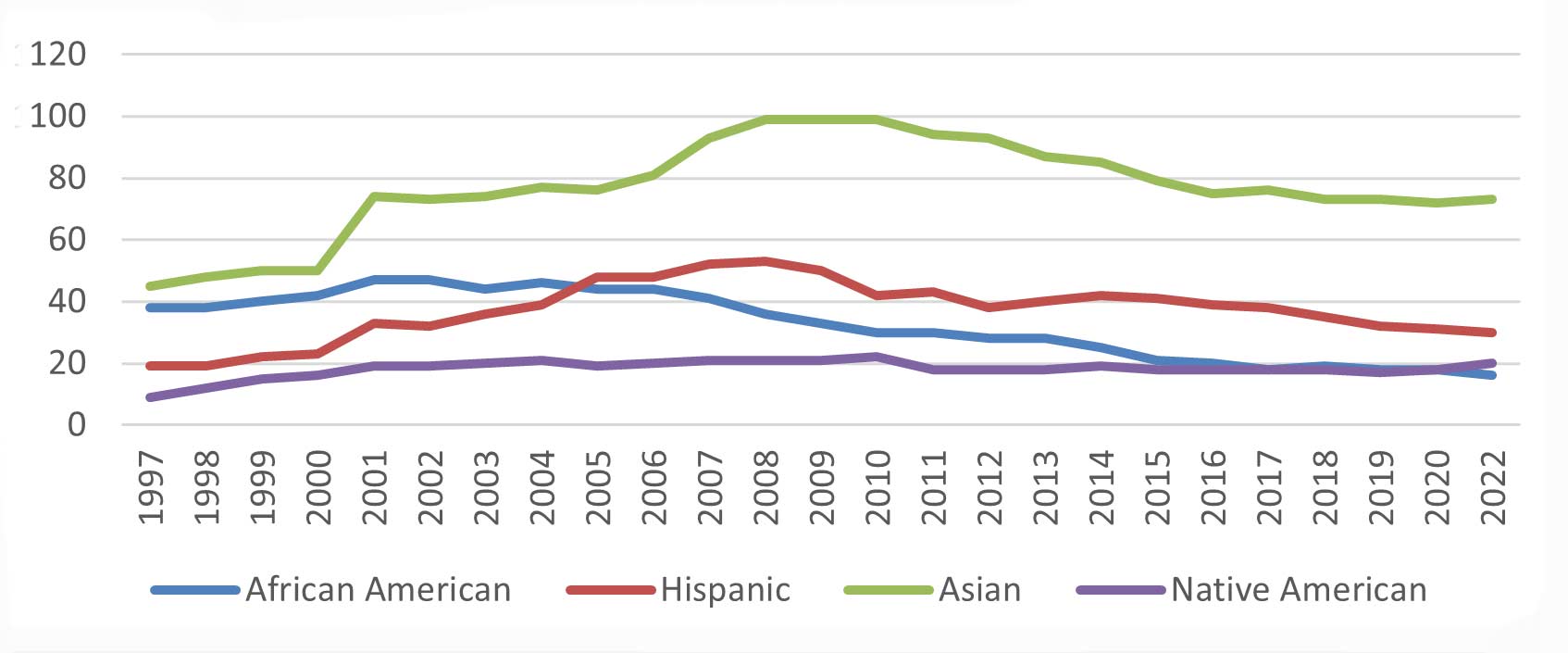

Figure 1 depicts the total number of MDIs disaggregated by racial or ethnic ownership. As of December 2022, there were 147 MDIs in the United States, a decline of 25% from 197 in 2010. Fifty percent of the MDIs were Asian American or Pacific Islander American, 20% were Hispanic American, 14% were Black or African American, 14% were Native American or Alaskan Native American, and 2% were Multi-Racial American. Since the 2008 financial crisis, all groups have seen declines in their ownership numbers, except in the case of Native American or Alaskan Native American MDIs, which was already a relatively small group. The number of branches has also declined by 16%, from 1,475 in 2010 to 1,243 in 2022. The shrinking of MDIs and their branches could mean less access to financial services in markets that are already underserved.

1. Banks by minority ownership

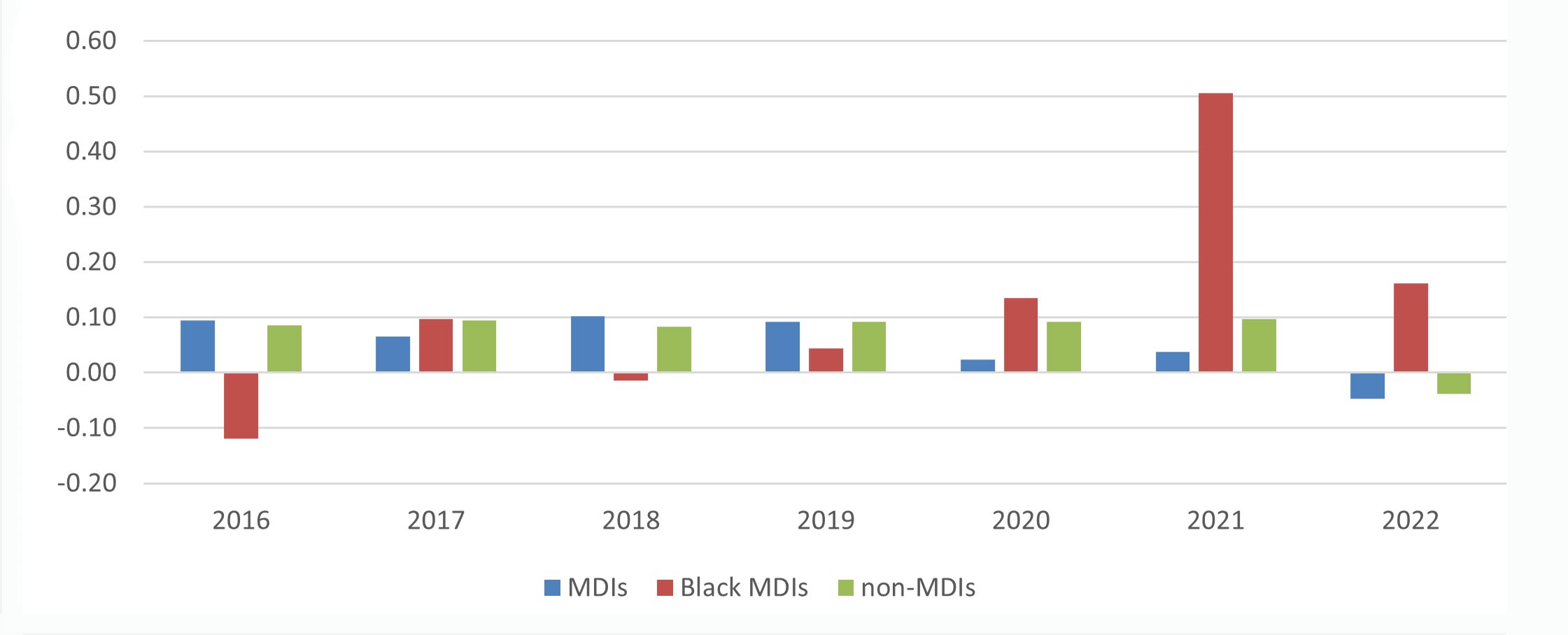

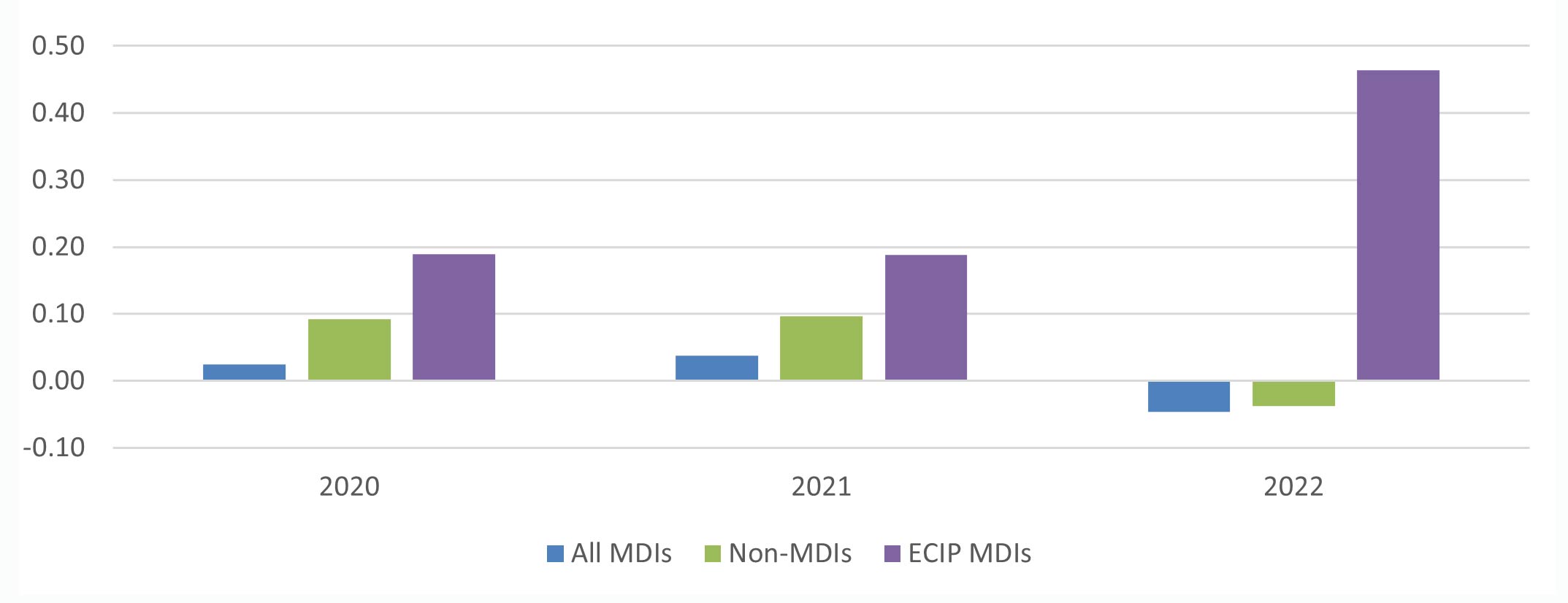

Even though the number of MDIs has fallen due to consolidation, the MDI sector collectively has seen a 79% increase in assets to a total of $330 billion in 2022, from $184 billion in 2010—a growth rate like that of all FDIC-insured institutions. 2 Average net income tripled from $11 million to $33 million between 2016 and 2022 for MDIs, a faster rate than for the banking sector as a whole.3 The average net income for African American MDIs went from negative $2.2 million in 2016 to a gain of $1.8 million in 2022. Participation in government programs, such as the Paycheck Protection Program (PPP) and the Emergency Capital Injection Program (ECIP), was particularly important in increasing growth in earnings and equity in 2021, when African American MDIs saw much faster growth in equity than the overall banking sector (figure 2). MDIs that were ECIP recipients had particularly strong growth in their equity in 2022 (figure 3).

2. Year-over-year percent equity change (average)

3. Year-over-year (December) percent change in equity (average)

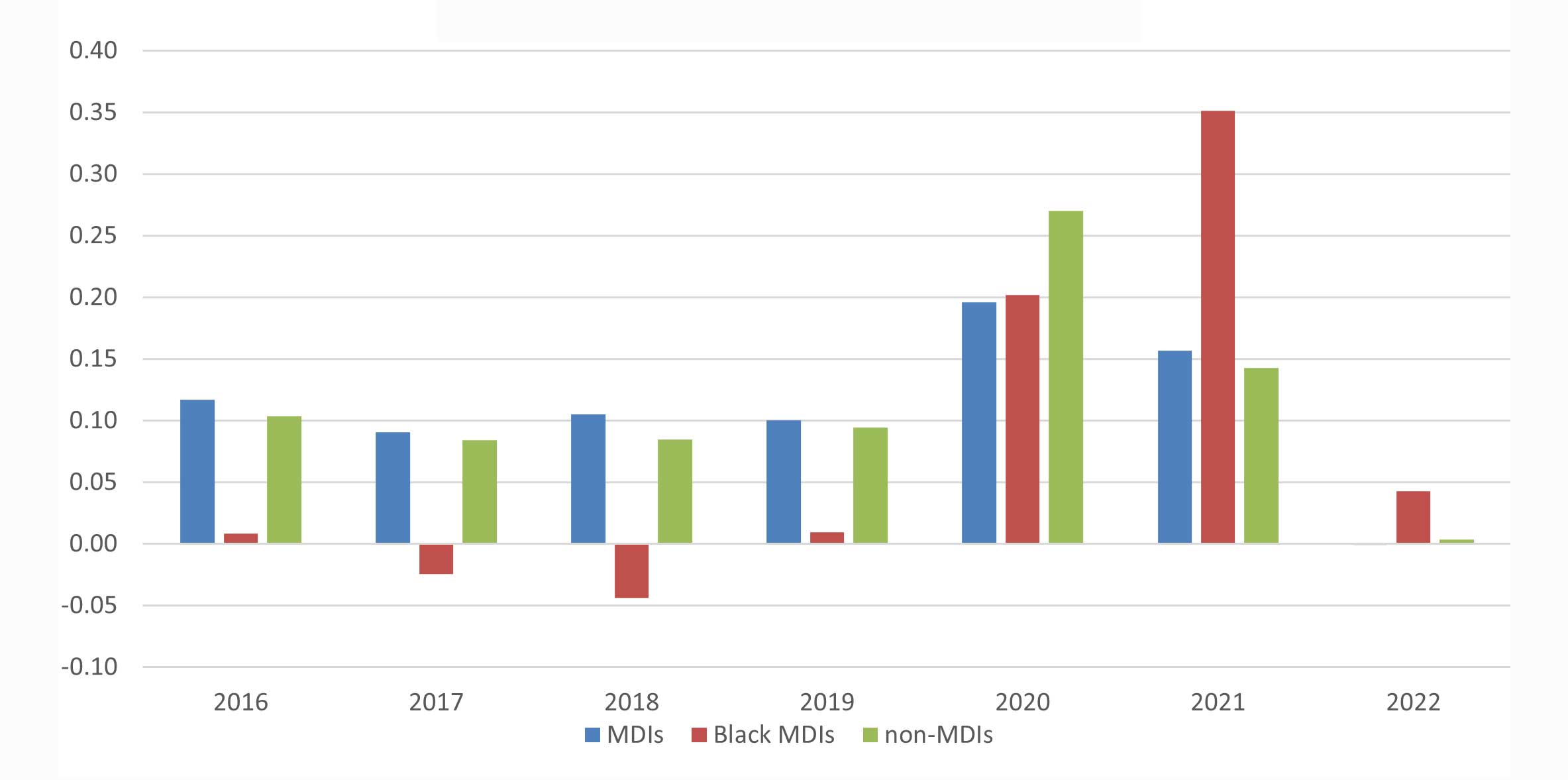

Deposits held at MDI branches grew by 68%, from $169 billion in 2016 to $284 billion in 2022, based on analysis of FDIC data. The increase in deposits (figure 4), which was particularly pronounced for Black or African American MDIs in 2020 and 2021, may have reflected in part the movement to #BankBlack. The police killings of George Floyd and Breonna Taylor had led to demands for racial economic equity, and as part of the movement, individual customers and nonprofit and community organizations opted to give their business to Black MDIs and credit unions. There have also been several cases of reported corporate support or intent to support.4 The total deposits for Black MDIs in 2010 was $5.4 billion (averaging $164 million for 33 banks). In 2016 the total was $4.8 billion (average of $198 million for the 24 Black MDIs), and in 2022 it reached $6.4 billion (averaging $305 million for the 21 banks). By comparison, in 2022 the total deposits for non-MDI community banks (as defined by the FDIC) was $2.2 trillion (averaging $537 million per bank).

4. Percent change in average deposits

The most recent FDIC report (2019) details the healthy position of the MDI sector since the end of the Great Recession.5 Credit quality (loan performance) has improved across the banking industry, including for MDIs. MDI interest income rebounded more quickly than at most non-MDI financial institutions, and higher loan-to-asset ratios boosted interest income at MDIs relative to the other bank groups. In addition, MDIs have benefited from higher loan servicing fee growth and net gains on loan sales since 2009, which has boosted their noninterest income.

Challenges faced by MDIs

Despite their importance, MDIs continue to confront challenges that hinder their ability to serve their communities. One of the main challenges is their vulnerability to financial shocks due to more limited ability to raise capital.6 The combined assets of $330 billion of the 147 MDIs represents just 1% of U.S. bank assets.7 As small banks they have historically been vulnerable, especially during periods of financial stress. For example, during and after the 2007–09 recession, as home prices dropped, the shocks tended to disproportionately affect markets with higher fractions of subprime borrowers.8 A number of these banks with exposures to subprime markets and relatively more nonperforming loans saw a steeper decline and even negative returns to their assets (ROA) and tier 1 capital ratio, leading to greater challenges in raising sufficient capital buffers. This led in some instances to extreme financial disintermediation, i.e., they were not able/allowed to lend, and some ultimately were closed by their regulators.9

Another challenge has to do with high expenses relative to earnings (efficiency ratio). Since MDIs tend to serve customers with lower and more variable incomes, their sources of funds are more limited. Because of lower operating income (relative to costs) the efficiency ratio, especially for the very small MDI banks (less than $100 million in assets) has been relatively high compared to larger MDI counterparts.10 As the FDIC report noted, although the expense ratios—salaries, premises and fixed assets, and other noninterest expenses, such as technology costs as a percentage of average assets—have improved for MDIs since 2013, the overhead expenses relative to average assets for MDIs are still above those of other institutions. As we found in our previous article, this higher efficiency ratio is particularly true for the small MDIs with less than $1 billion in assets, compared to non-MDI counterparts. The more limited resources for these smaller banks remain a hindrance for their capacity to invest in such improvements as technology to provide online and mobile banking services, making it more challenging for them to attract and retain customers.11

Programs to strengthen MDIs

The Community Reinvestment Act (CRA), enacted in 1977, requires bank examiners to evaluate favorably nonminority banks’ activities undertaken in cooperation with MDIs.12 In their October 2023 announcement of new regulations implementing the CRA, the three federal banking agencies stated that the new regulations are intended to build on and clarify the activities undertaken by nonminority banks in cooperation with MDIs that will receive consideration as part of the CRA evaluation.13

Historically, to address the liquidity needs of some MDIs, the Minority Bank Deposit Program (MBDP),14 established in 1969, encouraged the deposit of funds by federal agencies in select MDIs. The program, which was expanded in 1979 to include financial institutions either owned or controlled by minority individuals or owned, controlled, or operated by women, currently directs funds to 72 banks and credit unions. There could be mixed effect of deposits. While deposits help with liquidity, a sudden increase in deposits could present a problem for small banks that do not have the means to lend out a massive influx of deposits (and must pay interest, hence deposits could be a liability).15 This might adversely affect their capital (assets - liability).

To address MDIs’ limited access to capital, Congress in 2021 established the Emergency Capital Investment Program (ECIP),16 which authorizes the Treasury to make up to $9 billion in capital investments in banks and credit unions certified as MDIs or CDFIs. ECIP is intended to support the efforts of these institutions to provide loans, grants, and forbearance for small businesses, minority-owned businesses, and consumers in underserved communities that may be disproportionately affected by the economic fallout of the Covid-19 pandemic. As of October 2023, 22% (33 out of 147) of MDIs are ECIP recipients.

A recent public/government initiative, the Economic Opportunity Coalition (EOC)17 coordinates with corporations and foundations (e.g., private and social sector organizations) to align major investments in communities of color. The four priority areas include investing in CDFIs and MDIs, including launching a planning committee to explore the creation of a Community Equity Development Bank to expand financial services to low- and moderate-income communities. The EOC members have committed to move $1 billion in deposits to MDIs to increase affordable capital in communities of color.

Private sector groups have also been supportive of MDIs. The Black Bank Fund was launched by a group of Black financial services professionals and regulatory experts in 2020.18 The mission is to inject tier 1 capital through stock purchases. The Black Vision Fund approves and invests grants and loans in “Expanding Black Business Credit” member CDFIs that will then provide financing specifically to Black-owned small businesses.19 The fund is a part of the Expanding Black Business Credit (EBBC) initiative, which has a mission to create thriving business ecosystems that strengthen Black-owned small businesses, Black-led nonprofits, and the Black-led CDFIs that help them to succeed. EEBC was formed in 2016 initially as a CEO Peer Learning Network by leaders of Black-led/focused CDFIs to share best practices in lending to Black businesses.

In 2021, the Federal Deposit Insurance Corporation (FDIC) encouraged the development of the Mission-Driven Bank Fund (MDBF),20 a private capital investment vehicle to support insured MDIs and CDFIs. The MDB provides investors with an opportunity to support mission-driven depository institutions that support low- and moderate-income, minority, and rural communities. It also provides complementary strategic advisory services, in the form of financial or technical support, to such entities and promotes and encourages the creation of new MDIs and CDFIs.21 The fund seeks to improve mission-driven bank sustainability and build capacity and scale to enable these institutions to have a greater impact in the communities they serve.

Finally, there are opportunities for large banks to work with minority banks. For instance, few of the country’s largest banks have announced or engaged in equity investments into Black and Hispanic American banks. Such investments can help these institutions lend more and expand their market and have more resources to upgrade their technology infrastructure.

Notes

3 Net income is equal to net interest income plus total noninterest income plus realized gains (losses) on securities and extraordinary items, less total noninterest expense, loan loss provisions, and income taxes.

4 For example, Netflix announced it would put 2% of its cash deposits—$100 million—into Black financial institutions; available online. Square announced it would invest 3% of its cash and marketable securities—also $100 million—in support of minority and underserved communities, with much of the money earmarked for deposits and investments in MDIs and trade groups representing MDIs; available online. PayPal also announced it would invest $530 million in majority-Black communities and Black-owned companies; available online.

5 Federal Deposit Insurance Corporation, 2019, Minority Depository Institutions: Structure, Performance, and Social Impact, report, Arlington, VA, available online.

6 Allen N. Berger and Christa H.S. Bouwman, 2013, “How does capital affect bank performance during financial crises?,” Journal of Financial Economics, Vol. 119, No. 1, July, pp. 1169–1208. Crossref.

7 Assets for all banks as of December 2022 were $24 trillion.

8 Lower-income households are constrained in their ability to meet interest payments and sustain debt. As a result, when interest rates fall and the supply of credit increases, they take on disproportionately more debt than their higher income counterparts, who are not subject to that constraint. As such the surge in credit and house prices before the Great Recession was particularly pronounced in places with a higher fraction of poorer or subprime borrowers. During and after the recession, as home prices dropped, the shocks therefore tended to affect disproportionately markets with a higher fraction of households with other credit constraints, where MDIs may have exposures, given their mission and location. See Atif Mian and Amir Sufi, 2009, “The consequences of mortgage credit expansion: Evidence from the U.S. mortgage default crisis,” Quarterly Journal of Economics, Vol. 124, No. 4, November, pp. 1449–1496, Crossref, and Alejandro Justiniano, Giorgio E. Primiceri, and Andrea Tambalotti, 2016, “A simple model of subprime borrowers and credit growth,” American Economic Review: Papers and Proceedings, Vol. 106, No. 5, May, pp. 543–547, Crossref.

9 ROA is considered an indicator of how management uses its assets or resources to generate income. As a rule of thumb, ROA levels should be close to 1% for banks to cover their cost of capital. Under the FDIC Improvement Act definition for prompt corrective action by bank regulators, a bank is well capitalized if the ratio of tier 1 capital to total assets (tier 1 leverage ratio) is at least 5% and the tier 2 capital risk-based asset ratio is at least 6, (and the ratio of the sum of tier 1 and tier 2 is at least 10%). ROE helps gauge how the banks’ investments are generating income, while ROA shows how management is using assets or resources to generate more income. (ROA = (net income) / (total assets); ROE = (net income) / (total assets) × (total assets) / (shareholders’ equity). Generally, for banks to cover their cost of capital, ROA levels should be closer to 1%. (An ROE level closer to 10% is viewed as adequate from investors’ perspectives).

10 The efficiency ratio is the ratio of noninterest expenses to net operating income. Efficiency ratio = noninterest expense / (net interest income + noninterest income), where a higher efficiency ratio indicates an institution that is less efficient at generating revenue per dollar of noninterest expense. See our previous article.

11 See Miriam Cross, 2023, “The tech challenges facing minority banks and how they can solve them,” American Banker, January 4, available online. See also Anthony Barr, Stephanie Thomas, and Nicole Elam, n.d., “Navigating the digital frontier in banking: Challenges and opportunities for mission-driven financial institutions,” National Bankers Association, research brief, available online.

12 U.S.C. Title 12, Sections 2903(b) states that in assessing the record of a bank, the appropriate federal financial supervisory agency may consider as a factor capital investment, loan participation, and other ventures undertaken by the institution in cooperation with MDIs provided that these activities help meet the credit needs of local communities.

13 Available online, p. 274.

15 Edward C. Lawrence, 1997, “The viability of minority-owned banks,” Quarterly Review of Economics and Finance, Vol. 37, No. 1, Spring, pp. 1–21, Crossref, and Russ Kashian, Richard McGregory Jr., and Neil Lockwood, 2014, “Do minority-owned banks pay higher interest rates on CDs?,” Review of Black Political Economy, Vol. 41, No. 1, January, pp. 13–24, Crossref.

20 Available online, FDIC: Minority Depository Institution Program - Mission Driven Banks and MDBF Summary.