Summary

In the third quarter of 2018, farmland values for the Seventh Federal Reserve District were up 1 percent from a year ago. However, according to the 188 agricultural bankers who responded to the October 1 survey, District farmland values were 1 percent lower in the third quarter of 2018 than in the second quarter. This was the first quarterly decline for District agricultural land values since the fourth quarter of 2016 (nearly two years ago). Almost two-thirds of survey respondents expected the District’s farmland values to be stable during the fourth quarter of 2018, but 32 percent of them expected a decrease in farmland values in the final quarter of this year and only 2 percent expected an increase.

Agricultural credit conditions for the District deteriorated again in the third quarter of 2018. For the fifth quarter in a row, the availability of funds for lending by agricultural banks was down relative to a year ago. Yet, for the third quarter of 2018, the demand for non-real-estate farm loans was higher than a year earlier. These results helped explain how the average loan-to-deposit ratio for the District established a new record of 79.4 percent. Moreover, repayment rates for non-real-estate farm loans were lower in the third quarter of 2018 relative to the same quarter last year, and loan renewals and extensions were higher. Average interest rates on agricultural loans moved up some during the third quarter of 2018.

Farmland values

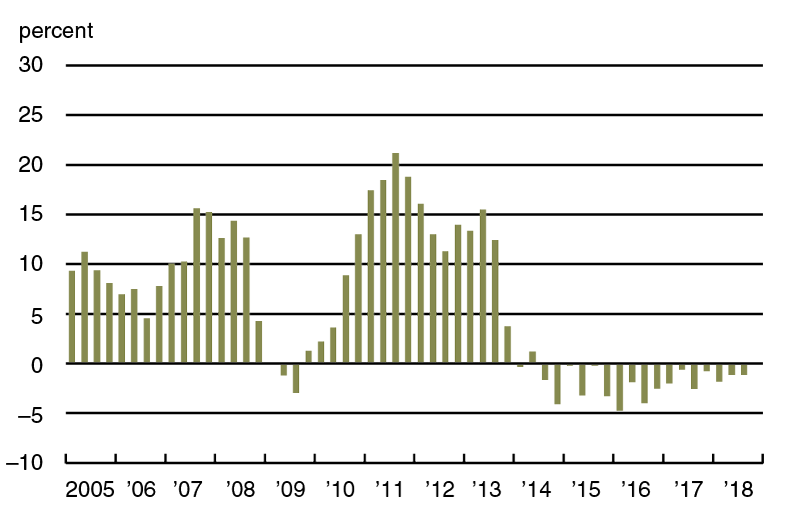

District farmland values saw a year-over-year increase of 1 percent in the third quarter of 2018 (see map and table below). The District did not experience a year-over-year decrease or increase in its agricultural land values greater than 1 percent for the eighth consecutive quarter. Furthermore, after being adjusted for inflation with the Personal Consumption Expenditures Price Index (PCEPI), District farmland values were down 1 percent in the third quarter of 2018 relative to the third quarter of 2017. The latest results were in line with recent trends: While nominal farmland values had remained fairly stable during the past few years, real farmland values had been eroding since the third quarter of 2014 (see chart 1).

1. Year-over-year real changes in Seventh District farmland values, by quarter

Sources: Author’s calculations based on data from Federal Reserve Bank of Chicago surveys of farmland values; and U.S. Bureau of Economic Analysis, Personal Consumption Expenditures Price Index (PCEPI), from Haver Analytics.

Agricultural land values would have experienced more downward pressure in the absence of exceptional crop yields. In 2018, District-wide corn and soybean yields jumped to all-time highs (198 bushels per acre for corn and 59 bushels per acre for soybeans). According to U.S. Department of Agriculture (USDA) forecasts, the five District states’ harvest of corn for grain in 2018 would increase by 1.5 percent from 2017, and their soybean harvest would surge by 8.7 percent from the previous year, setting a new record. The size of the corn crop, according to USDA projections, would be slightly smaller than the record set in 2016 because 5.6 percent less acreage was harvested in 2018 than in 2016. The USDA expected the country’s corn harvest in 2018 to be the second largest on record; moreover, the national soybean harvest was forecasted to set another record. The nation’s corn output in 2018 would be 0.2 percent higher than in 2017. And U.S. soybean output this year would be up 4.7 percent from last year’s level.

For the third quarter of 2018, corn prices were 1.9 percent higher than a year ago, based on USDA data. But soybean prices were 5.6 percent lower than a year earlier. Accounting for larger supplies of crops and trade tensions, the USDA revised its price estimates for the 2018–19 crop year to a range of $3.20 to $4.00 per bushel for corn and a range of $7.60 to $9.60 per bushel for soybeans. When calculated with the midpoints of these price intervals, the projected revenues from the 2018 District corn and soybean harvests would be up 8.8 percent and 0.1 percent from 2017, respectively.

Key livestock prices were lower in the third quarter of 2018 relative to the same quarter of last year. Compared with a year earlier, cattle, hog, and milk prices were down 2.6 percent, 17 percent, and 9.8 percent in the third quarter of 2018, respectively. Hence, livestock operations—particularly dairies—faced some challenges, according to several survey respondents. For instance, one Michigan agricultural banker reported that “dairy enterprises have been hard hit by milk prices.”

Credit conditions

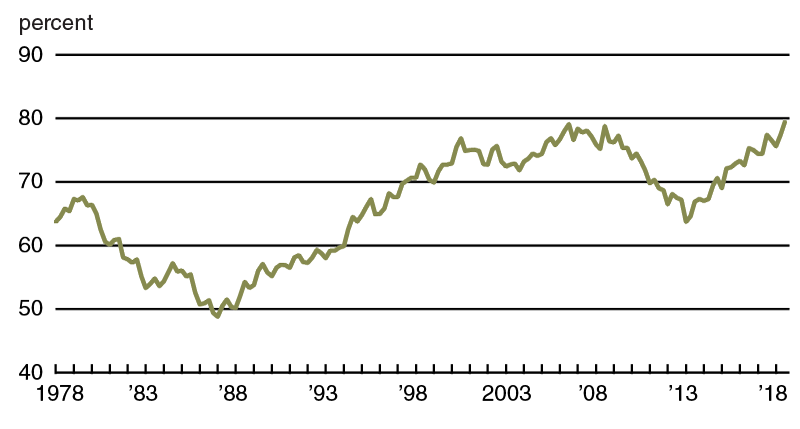

Once more agricultural credit conditions for the District seemed worse relative to a year ago. The availability of funds for lending by agricultural banks was lower than a year earlier for the fifth quarter in a row. At 82, the index of funds availability was last this low in the third quarter of 2000. Agricultural banks in the District had less funds for lending in the third quarter of 2018 than a year ago; 3 percent of the survey respondents indicated their banks had more funds available to lend, while 21 percent indicated their banks had less. In the third quarter of 2018, demand for non-real-estate farm loans was again stronger compared with a year ago. The index of loan demand edged higher to 128, as 41 percent of survey respondents noted higher demand for non-real-estate loans than a year earlier and 13 percent noted lower demand. The combination of decreased funds availability and elevated loan demand helped boost the District’s average loan-to-deposit ratio to a new record of 79.4 percent (see chart 2). (The previous peak had been in the third quarter of 2006.) Nevertheless, the average level desired by the responding bankers was 3.4 percentage points higher.

2. Quarterly average loan-to-deposit ratio for Seventh District

For the July through September period of 2018, repayment rates on non-real-estate farm loans were yet again lower than a year ago. The index of loan repayment rates was 63 in the third quarter of 2018, as 2 percent of responding bankers observed higher rates of loan repayment relative to a year ago and 39 percent observed lower rates. Furthermore, loan renewals and extensions on non-real-estate agricultural loans were higher in the third quarter of 2018 relative to the same quarter of 2017, with 43 percent of the responding bankers reporting more of them and just 1 percent reporting fewer. Collateral requirements for loans in the third quarter of 2018 tightened relative to the same quarter of last year, as 25 percent of the respondents reported that their banks required more collateral and none reported that their banks required less. As of October 1, 2018, the District’s average interest rates on new operating loans, feeder cattle loans, and farm real estate loans had risen to 5.86 percent, 5.93 percent, and 5.46 percent, respectively.

Looking forward

Nearly two-thirds of survey respondents predicted farmland values to be stable in the fourth quarter of 2018, while 32 percent of responding bankers expected farmland values to decrease in the October through December period of 2018 and just 2 percent expected farmland values to increase. Also, more respondents anticipated weaker rather than stronger demand by farmers and nonfarm investors to acquire farmland this fall and winter compared with a year earlier. Still, on the whole, respondents expected an uptick in transfers of available properties for sale. Twenty-six percent of the responding bankers forecasted an increase in the volume of farmland transfers relative to the fall and winter of a year ago, and 21 percent forecasted a decrease.

For the sixth year in a row, crop net cash earnings were expected to contract over the fall and winter from their levels of a year earlier, based on the predictions of survey respondents. Only 5 percent of survey respondents anticipated crop net cash earnings to rise over the next three to six months relative to a year ago, while 82 percent anticipated these earnings to fall. According to the responding bankers, hog, cattle, and dairy farmers were yet again expected to encounter diminished net cash earnings over the fall and winter relative to a year ago. Just 3 percent of the survey respondents predicted higher net earnings for hog and cattle operations over the next three to six months relative to a year earlier, while 65 percent predicted lower net earnings. Similarly, 1 percent of survey respondents anticipated higher net earnings for dairy operations this fall and winter compared with a year ago, while 66 percent anticipated lower net earnings.

Additionally, survey respondents expected loan repayment rates to decline this fall and winter from a year ago; only 2 percent of the responding bankers forecasted a higher volume of farm loan repayments over the next three to six months compared with a year earlier, while 57 percent forecasted a lower volume. Moreover, forced sales or liquidations of farm assets owned by financially distressed farmers were anticipated to increase in the next three to six months relative to a year ago, according to 61 percent of the responding bankers (only 1 percent anticipated a decrease). District non-real-estate farm loan volume in the October through December period of 2018 was expected to be higher compared with the same period of 2017, mainly because of increases in the volumes of operating loans and loans guaranteed by the Farm Service Agency of the USDA.

An Iowa respondent emphasized the “concern from row crop farmers regarding interest rate increases next year and low commodity prices.” This concern was echoed by livestock operators. So, there was a decidedly downcast outlook for agriculture based on the latest survey responses.

CONFERENCE REMINDER

Agricultural Technology’s Impacts on Farming and the Rural Midwest

On November 27, 2018, a Chicago Fed conference will be held to explore the prospects and challenges for implementing new agricultural technologies in the rural Midwest. To register, go to the event page.