The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

In the Wealth of Nations, Adam Smith argues that one of the basic responsibilities of the “sovereign or commonwealth” is to provide an adequate structure of public works to “facilitate the commerce of society.” An extensive and well-maintained system of roads, bridges, highways, lighthouses, and canals is necessary to meet the needs of a vital, growing economy. The duty of constructing such public works falls to the government because their benefits accrue not just to particular individuals but to the economy at large, or because the cost reductions derived from economies of scale are best captured by direct, centralized public capital outlays.

This essay argues that current public capital expenditures are too low. The argument begins by examining recent trends in public expenditures, particularly public spending on the infrastructure of the economy, such as roads, sewers, bridges, and the like. It then shows that public sector investment ultimately increases the private capital stock by influencing the rate of return to private investment. Thus, public capital expenditures are a critical determinant of the nation’s long-run production potential.

Public expenditure trends

The accompanying table presents data on U.S. government spending at the federal, state, and local levels during the period from 1953 to 1984. The first column indicates that total public expenditure has trended upward over this period. Government sector expenditures rose from 26.1 percent of gross national product during 1953-59 to 33.9 percent during 1980-84. In 1982 dollars, public sector spending grew from $507 billion in 1953 to $1,174 billion in 1984. Despite the Gramm-Rudman Act and attempts to slash public sector budget deficits on the expenditure side, the rising pattern of government spending continues in the 1980s.

1. Public expenditure and the return to private capital

| Total government expenditure (% of GNP) |

Public net investment ($ of GNP) |

Profit rate (%) |

|

|---|---|---|---|

| 1953-59 | 26.1 | 1.9 | 10.8 |

| 1960-64 | 27.6 | 2.2 | 11.6 |

| 1965-69 | 29.1 | 2.3 | 13.3 |

| 1970-74 | 31.2 | 1.4 | 9.8 |

| 1975-79 | 32.1 | 0.7 | 9.1 |

| 1980-84 | 33.9 | 0.4 | 7.9 |

The second column shows the share of total output devoted to expanding the nation’s nonmilitary public capital stock. Net public capital formation—the level of investment in roads, bridges, and so forth, after accounting for physical depreciation—tumbled from a high of 2.3 percent of GNP the latter half of the 1960s to only. 0.4 percent during 1980-84. In terms of constant 1982 dollars, public net investment was $11.5 billion in 1984, down from $27.6 billion in 1953 and $62.8 billion in 1964.

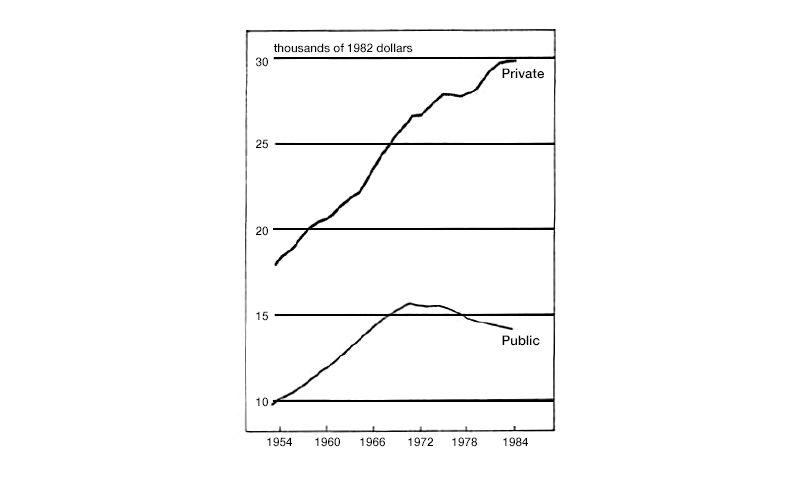

The graph illustrates the different behavior of the private as opposed to the public capital stock during the last three decades. During the earlier period, 1953-71, both the private and public net investment rates exceeded the growth rate of the workforce, producing rising private and public capital stocks per worker. However, since 1971 net public investment has lagged behind growth in the labor force and the amount of public capital per worker has contracted from $15,576 in 1971 to $14,224 in 1984. During the same period, the private capital stock per worker has expanded from $26,654 to $29,905. A dynamic, competitive world dictates that those with influence on the nation’s economic destiny be forward looking and prepare for the future in the present. Hence, it is now imperative to reassess our public investment policy.

2. Capital stock per worker

Public investment, private investment, and the rate of return

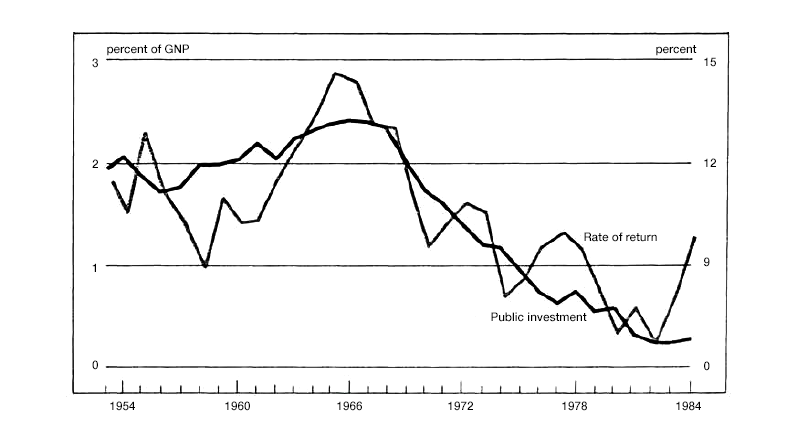

Changes in public investment can have significant impact on private investment. For the period from 1953 to 1984, net private investment in equipment and structures averaged 3.1 percent of GNP while net public nonmilitary investment averaged 1.5 percent. During this time private and public investment exhibited nearly the same amount of volatility. Net private investment ranged from a high of 4.6 percent of GNP in 1966 to a low of 1.3 percent in 1983, while public investment hit a maximum, 2.4 percent, in 1966 and a minimum, only 0.3 percent, in 1982.

3. Public investment and return to private capital

We can think of the impact of public capital accumulation on private investment as falling into two broad categories of effects, depending on whether the public investment “crowds out” or “crowds in” private investment.

Crowding out?

Higher levels of capital accumulation by the public sector arguably crowd out a substantial amount of private investment for several reasons. To the extent that publicly provided capital serves as a substitute for private capital in private production technologies, firms require less private capital to produce the same level of output. In addition, higher public sector demand in the capital goods producing sector raises the price of capital goods, thereby lowering the quantity of goods demanded by the private sector. Finally, the increased government demand creates a general scarcity of current resources, a rise in real interest rates, and a further contraction of capital spending.

In recent empirical work, I find that, holding fixed the rate of return to private capital, an increase in public investment expenditure of $1 billion crowds out anywhere from $1 to $1.5 billion of private investment expenditure.1 The crowding out appears to occur without the assistance of changes in the cost of capital. That is, firm managers appear to take directly into account the availability of public capital for use in private production.

This result indicates that the level of the public capital stock in the United States indeed may be too low. An efficient level of public capital is attained when the addition of an extra unit of either private or public capital has the same impact on the nation’s output. If the aggregate response of private firms to an expansion of public capital is to reduce private capital spending on a greater than one-to-one basis—and my empirical results suggest that this is presently the case—the marginal product of public capital may very well exceed that of private capital in private technologies. Further public capital accumulation is then required to drive down its productivity, on the margin, to equal that of private capital.

Or crowding in?

The above argument is based on an unchanged rate of return to private capital in the face of higher public capital accumulation. However, public capital devoted to infrastructure purposes is complementary to private capital in the production of goods and services. This implies that a rise in the public capital stock makes private capital more productive. New highways allow faster transportation of goods from factory to market; modern power plants cheapen energy and lower the cost of running machinery. Thus, higher levels of public investment filter into elevated profit rates for the nation’s businesses.

The third column of the table contains annual averages of the net profit rate of nonfinancial corporations in the United States.2 In a competitive marketplace, the net profit rate approximates the marginal productivity of private, nonfinancial corporate capital. As the table and graph illustrate, there is a striking tendency for the economy’s rate of profit—the private rate of return on invested capital—to be high when the level of public capital formation is high over the course of several years. In particular, the decade of the 1960s reveals the highest returns on the private sector capital stock as well as the highest rates of public sector capital accumulation.

The disturbing feature of the table, of course, is the evidence from the 1970s and early 1980s. The public investment rate during this time dwindled to less than 1 percent of GNP and the rate of return to private capital shrank to 8.9 percent, more than one and one-half percentage points below its post Korean War average of 10.8 percent and three and one-half percentage points below the average value of 12.5 percent for the 1960s.

I am not suggesting that deficient public capital formation alone is responsible for the recent low rate of return to the nation’s private capital stock and sluggish total investment. Low levels of capacity utilization in the economy’s factories, mines, and utilities brought on by oil price increases and real exchange rate appreciation helped diminish the net profits obtained per unit of capital. However, statistical analysis indicates that the level of public capital strongly influences the net return to private capital even after accounting for such cyclical effects. The empirical results show that a 10 percent increase in the capacity utilization frate from its 1984 value of 74 percent would have raised the profit rate from 9.9 to 11.4 percent. But, in the same analysis, a 10 percent increase in the public capital stock (five years of extra net public investment of $32.4 billion, or an extra 0.9 percent of GNP) would have increased the rate of return by a still larger amount to 12.6 percent.

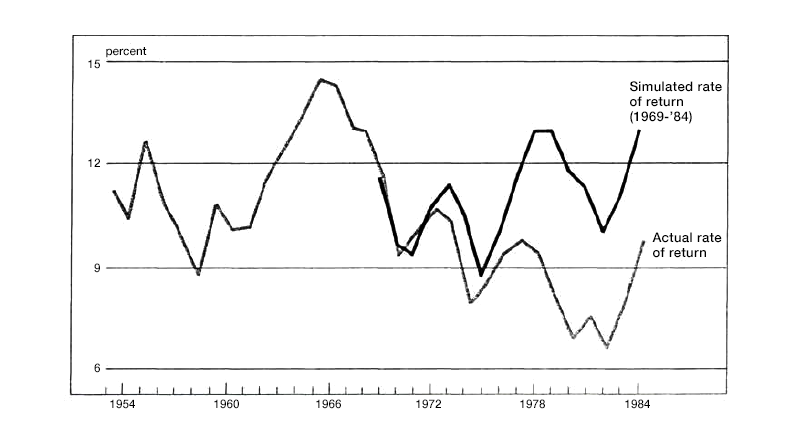

What would have been the effect on the rate of return to capital of maintaining a constant level of public investment of 2.1 percent of GNP—its 1953-to-1969 average—throughout the 1970s and early 1980s? The result of this experiment is depicted in figure 4. Evidently, holding public capital accumulation at this level would have eliminated the downward trend in the rate of return to private capital, although the substantial fluctuations resulting from changed currency valuations and capacity utilization still would have remained.

4. Effect of higher public investment on rate of return

The likely net effect

Given these conflicting influences, what appears to be the overall impact of public investment on private investment? The available estimates imply that a temporary surge of public investment of 1 percent of GNP ($34.9 billion in 1984) would first depress private investment by 1.2 percent of GNP ($41.9 billion). However, as the rate of return to private capital increases with the higher public investment, expenditures on private plant and equipment would be stimulated, ultimately inducing a cumulative rise in the private capital stock of roughly $39 billion over its 1984 level of $3,442.8 billion. The rate of return to private capital would rise from 9.9 percent to 11 percent and gradually fall back to its original level. The national (private plus public) capital stock would have risen from $5063.6 billion to $5137.6 billion, a rise of 1.5 percent. Thus, the net effect of temporarily increasing the public investment rate is a substantial increase in the national capital stock. Clearly, public investment policy has important consequences for the economy’s production possibilities.

Taking stock

The public capital stock appears to be too low relative to the private capital stock, thereby depressing the rate of profit to the nation’s stock of plant and equipment. Large public sector deficits of recent years have brought attention to the overall scale of government activity. Some argue that the government should spend less and others that it should tax more. Both of these responses to the problems posed by federal budget deficit are reasonable.

However, the evidence discussed here suggests that more attention should be paid to the composition of the government’s expenditure, and particularly its effects on the nation’s infrastructure needs. While total spending mounts, investment in public works slides. Indeed, the share of total public expenditure dedicated to net public capital formation declined from 8 percent in the 1960-64 period to a meager 1.2 percent between 1980 and 1984. By reorienting our public spending to upgrade and expand the public capital stock, we can heighten the productivity of our workforce and improve the competitive position of the United States in the increasingly open international marketplace.

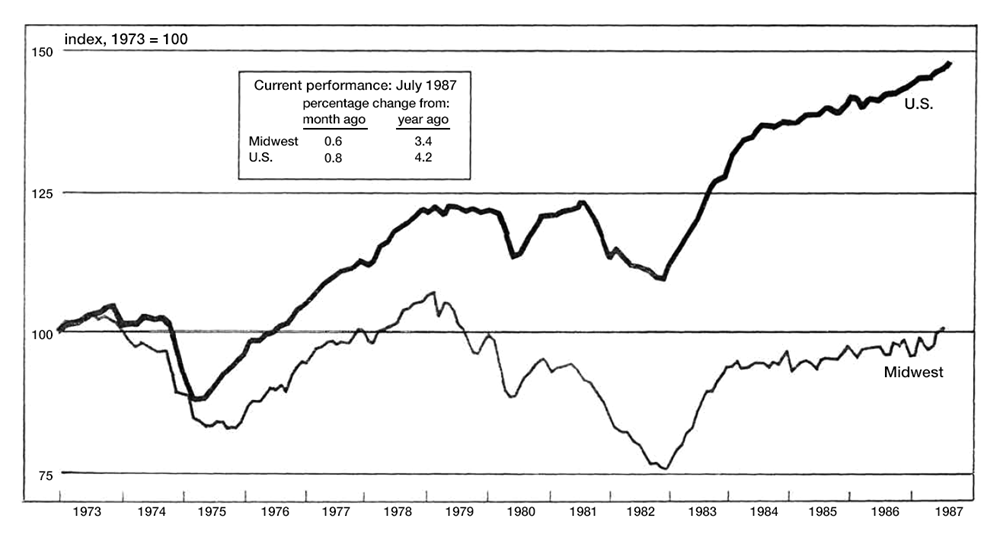

MMI—Midwest Manufacturing Index

Manufacturing activity in the Midwest (defined here as comprising Illinois, Indiana, Iowa, Michigan, and Wisconsin) rose 0.6 percent in July, following an upwardly revised jump of 3.6 percent in June. The July gains were heavily concentrated in the primary metals industry, but modest improvements were also recorded in other major industries in the Midwest, notably fabricated metals, nonelectrical machinery, and electric equipment.

Manufacturing activity in the nation (as measured by the Federal Reserve Board’s Index of Industrial Production) slightly outpaced the Midwest both in July and year-over-year (see above table). However, in the last two months the MMI has moved to its highest level since September 1979.

Notes

1 These estimates are contained in David Alan Aschauer, “Net Private Investment and Public Expenditure in the United States 1953-84.” Staff Memoranda, Federal Reserve Bank of Chicago, in press.

2 The rate of return to capital is measured as inflation-adjusted corporate income after depreciation plus net interest payments (as a return to debt claims on firms) relative to the current replacement value of the nonfinancial sector’s stock of fixed capital, land, and inventories.