The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

States compete for business. The stakes are high and the game is rough. Among the bargaining chips that states can use, selective tax incentives and fiscal inducements are favorites.

Competition among local and state governments can sometimes result in a bidding frenzy. For example, 25 states (and an untold number of localities) offered generous packages of tax abatements, special services, and improvements to infrastructure in an attempt to land General Motors’ Saturn auto facility. State governors made personal visits to GM headquarters and appeared on national television to plead their cases in public.

In another instance, the State of Illinois reportedly offered a package worth over $80 million in its successful effort to bring the Chrysler/Mitsubishi Diamond-Star auto production facility to the Bloomington/Normal area. The value of this package has become a matter of keen interest because the private investment at that site was only expected to be $500 million.

These selective incentive policies must be distinguished from more general efforts to make a state’s overall fiscal and tax structure favorable to business and development. Such incentive packages are offered by state and local governments to individual companies, or industries, and not on a uniform basis to all businesses within the community. They are selectively negotiated by public officials in hopes of snaring additional business activities that will pay a return on investment in terms of added jobs, income, and tax revenues.

As one commentator has noted, the resulting competition to attract industry has become a dog-eat-dog, Indiana-eat-Ohio affair.

This Letter looks at the value of these abatements and inducements—Let’s call them tax breaks and be done with it. What evidence we find is so uncertain and so difficult to assess, we conclude that any case for tax breaks for relocating or expanding business is unproved at best.

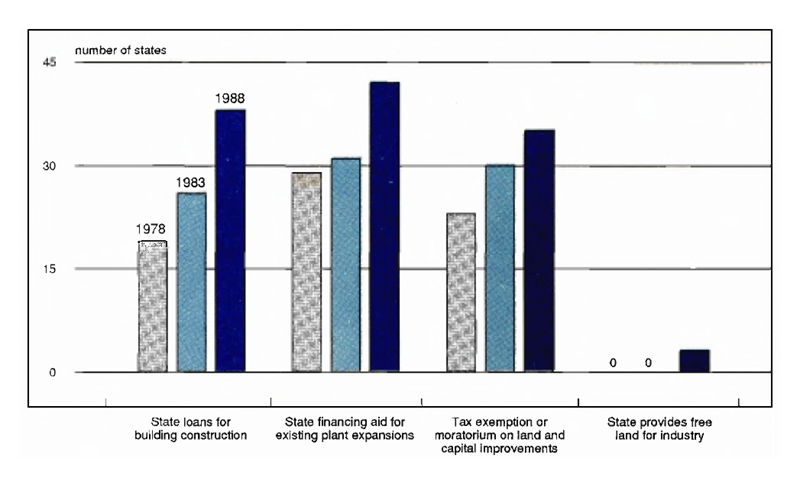

1. States step up breaks

The community’s perspective

In granting tax incentives, states and localities expect that the return will be greater than the cost. This benefit may not be achieved. To the extent that tax breaks and fiscal inducements merely reshuffle rather than reduce the overall tax burden, state and local governments may be doing more harm than good.1

Unlike general competition between localities in providing appropriate public services at a reasonable price, selective tax breaks do not necessarily redress any inefficiencies in the delivery of public services. Accordingly, the capricious and uncertain assignment of tax burdens—the hallmark of a selective incentives program—may actually repel businesses that have a long-term perspective on community investment. And, it is just that type of commercial neighbor that can be most valuable to a community.

From a community’s perspective, the appropriate way to evaluate its incentive program is to ask whether the benefits to the community exceed the costs. There has not been adequate research to measure the effectiveness of these programs in general for every community. Yet, given what is known, along with careful attention to the logic behind the programs, there are basic questions that public policymakers must answer before engaging in a costly and widespread program of selective industry fiscal inducements.

Are tax breaks a good lure?

A steady stream of studies on the relationship between overall state and local tax burdens and business growth has emerged over the past 35 years.

Most early studies suggested that taxes were not related to state and local economic growth.2 Accordingly, policy advice warning local communities against the use of tax breaks became widespread.3

However, as the sophistication of studies increased, new evidence seems to indicate that, at the margin, taxes can indeed help attract businesses to specific localities. Studies of firm location decisions within a metropolitan area have suggested that, once the supply of properly zoned and available land is accounted for, local taxes become important in siting decisions of manufacturing plants.4 Indeed, studies considering the location of economic growth have suggested that tax burdens, tax structure, and the choice among types of state and local public expenditures and services can all be significant in location decisions.

These findings reopened debate among analysts of state and local fiscal incentives policy. But, while it seems that taxes do matter, this hardly implies that taxes are a significant consideration for each investment decision.5 Questionnaires directed at plant or company officials have been used to determine the extent to which relocating or investing business would have undertaken the investment without the selective tax break. Responses certainly are influenced by the firm’s reluctance to bite the hand that feeds it. But, nonetheless, the survey findings suggest that the success rate of incentive programs tend to be very low.6 Firms will unfailingly ask for incentives if they are available, but state and local communities find it difficult to distinguish those firms that ask from those firms that need.

For this reason, the debate has shifted to ask when and where selective tax breaks will be effective. More importantly, it is not clear whether the state and local officials who grant breaks at their own discretion can distinguish situations in which tax breaks are successful in gaining new business from those in which tax abatement could have been avoided. Clearly, judgments on the net benefits or costs of fiscal inducement programs will depend on such considerations.

The main consequence of a low success rate is that states and local communities must heavily discount the jobs and income that are said to result from incentive programs, in deciding whether or not to engage in a broad policy of selective tax breaks.

Do breaks crowd out as they bring in?

Even if a tax break does promote investment, direct economic benefits can be wholly or partly offset if existing businesses or residential activities are crowded out of the community, or investments by local businesses are discouraged. For example, when the tax break policy allows the incoming firm to gain a competitive advantage over a local firm engaged in the same service or product, it may thereby drive away investment dollar for dollar.

Most evidence of this effect is anecdotal. For example, a maker of hydraulic equipment, Abex Corporation, Denison Division, announced plans to close a Columbus, Ohio, facility in the late 1970s. This was in response to a generous tax break by the Columbus City Council to its direct competitor, L. Schuler GMBH, of West Germany, to locate a facility in Columbus.7 To the extent that state and local governments cannot foresee such situations, tax uniformity rather than selective tax breaks is a better policy choice to maintain the community’s stability.

Even when potential firms do not compete directly in final markets with existing community firms, they do compete in the community for other factors of production, such as labor and infrastructure. We do not know the extent to which “invited” businesses raise some local factor costs to the point where other activities are crowded out of the community. The tax relief and generous upgrading of infrastructure that was offered to Volkswagen to locate its production facility in New Stanton, Pennsylvania, was loudly protested by some local businessmen who foresaw their tax burdens being hiked without attendant benefits. A careful cost-benefit analysis would require that such costs be considered.

Finally, a community policy of selective tax breaks may further crowd out potential business investments that would otherwise occur in the absence of the program. Some potential firms may feel that a community with large scale incentive programs cannot be counted on for a stable and efficient fiscal climate in which to conduct business. (Of course, a business that has already decided to locate or reinvest in a community will ask for a tax abatement if it is available or if they believe they can extract a subsidy—to do otherwise would not be a rational economic response by the firm.)

Moreover, a firm’s prior assessment of the tax policy of a community with an extensive incentive program may also recognize that its own future tax burden will depend on the development decisions of the next government in office. Future officials may grant even larger breaks to the next footloose investor, thereby increasing the tax burden on the community’s existing businesses.

Opinions obtained from many companies indicate that, when assessing a community, firms look for a long-term record of fiscal stability and efficiency in providing public services. Such a fiscal climate will ensure that a large private investment will not be ultimately soured by deteriorating public services or unexpected and undesirable changes in tax policy.

Are gains in business activity long-term?

In evaluating potential benefits, communities must also recognize that promises of long-term jobs and future investments by incoming firms do not always materialize. Amidst much fanfare, Volkswagen’s assembly plant in New Stanton, Pennsylvania, opened in 1978. It shut down in 1988. Auto production by Chrysler Corporation at AMC’s former plant in Kenosha, Wisconsin, will cease this December following a two-year run. The State of Wisconsin will probably recoup its investment because Chrysler has responded to public opinion or public needs (many other companies are not so responsive).

Unlike many European countries, states in the U.S. have been slow to adopt “clawback” provisions, which allow communities to regain subsidies when promised jobs are not realized from firms receiving public subsidies. However, one recent court decision (subject to review) has placed limits on the ability of a firm to close a plant and relocate operations when the firm had been a recipient of a subsidized loan to expand in its original location.8 Other judicial tests are now in progress.

Administrative costs

In addition to answering these questions, communities must consider the high administrative costs of incentive programs. The community must study who will be favored by tax breaks and special service inducements; what the costs and benefits are of each type of facility; who will be benefited in the community; and who will be hurt. It must also analyze what public services and facilities will need to be expanded because of the investment and to what degree it can be expected to expand employment and population.

Conclusions

Communities are usually aware of the direct costs and benefits of attracting businesses with tax breaks and other fiscal inducements. The lost tax revenues or reshuffled tax burdens are highly visible from news accounts of plant negotiations between state officials and big-name corporations. The attendant benefits of employing the unemployed are readily accepted and highly valued by the general public.

But, beyond these obvious considerations, a broad community policy of selective tax breaks can be risky. The success rate of tax incentive programs in actually inducing firms to relocate or expand is difficult to gauge for both the general public and public officials alike. In addition, the extent to which incentive programs crowd out other potential investment, thereby creating uncertainty as to the community’s fiscal stability and business climate, is hard to assess.

Better economic analysis and information on these impacts will be required before the utility of incentives policy can be determined for every community. Meanwhile, given the potential pitfalls, public officials should be cautious in making selective incentive programs—tax breaks—a keystone of state and local development policy.

MMI—Midwest Manufacturing Index

Manufacturing activity in the nation edged up only 0.2 percent in September, fueling speculation that the economy is beginning to slow down. The nonelectrical machinery industry, reflecting the strength in business equipment, continued to post solid gains, as did the transportation equipment industry. However, production of consumer durables (except autos) and nondurables declined along with basic metal materials, such as steel.

Manufacturing activity in the Midwest fared slightly better than the nation, rising 0.3 percent in September after experiencing no growth in August. Midwest manufacturing was aided by a relatively strong performance in its primary metals and electrical equipment industries, when compared to those industries nationally.

Notes

1 This article does not argue that general competition between state-local governments in providing low-cost, high-quality public services, financed through a well-structured tax system, should be discouraged. See John Shannon, “Interstate Tax Competition—The Need For a New Look”; and “Tax Competition: Is What’s Good For the Private Goose Also Good For the Public Gander?” in Reform Or Revenue, Symposium, National Tax Association/Tax Institute of America, Arlington, VA., May 19-20, 1986, Vol. XXXIX, No. 3.

2 The seminal works in this area are: C.C. Bloom, State and Local Tax Differentials and the Location of Manufacturing, Studies in Business and Economics, The University of Iowa, No. 5, 1956; and John Due, “Studies of State and Local Tax Influences on the Location of Industry,” National Tax Journal, Vol. 14, June 1961, pp. 163-173.

3 See Gary C. Cornia, William A. Testa, and Frederick D. Stocker, State-Local Fiscal Incentives and Economic Development, Academy For Contemporary Problems, Columbus, Ohio, 1978; and Michael Kieschnick, Taxes and Growth: Business Incentives and Economic Development, Council of State Planning Agencies, Washington, D.C., 1981.

4 See Robert J. Newman and Dennis H. Sullivan, “Econometric Analysis of Business Tax Impacts on Industrial Location: What Do We Know, and How Do We Know It?” Journal of Urban Economics, Vol. 23, pp. 215-234.

5 James A. Papke has constructed a micro-simulation model that estimates the after-tax rates of return for hypothetical capital investments at alternative sites. All else is held constant except for state and local tax effects, their interaction with each other, and their interaction with the federal tax system. A 1985 study among sites in 15 states revealed that there were significant differences in after-tax rates of return for a hypothetical investment, which was patterned after the Saturn Corporation subsidiary of GM. However, and not surprisingly, the state where the investment was finally located, Tennessee, did not have the most favorable profit rate (based on tax structure and incentives alone). See James A. Papke, The Taxation of the Saturn Corporation: Intersite MicroAnalytic Simulations, Center for Tax Policy Studies, Purdue University, West Lafayette, Ind., March 1985.

6 For example, a recent study by George W. Morse and Michael C. Farmer found that, out of 23 investment decisions in rural Ohio communities, in only one was the deciding factor found to have been the tax abatements according to onsite interviews. However, all 23 companies received tax abatements.

See Roger J. Vaughn, “A New Look at State Tax Incentives.” The Entrepreneurial Economy, July 1984, pp. 8-9. Under New York City’s “Job Incentives Program,” tens of millions of dollars in exemptions and abatements were granted to New York firms in an attempt to attract and retain firms. Vaughn cites, as an example of an incentive that was probably a give-away, a ten-year, $8 million bonus to Tiffany’s for the rehab of two floors of its building at 57th St. and 5th Ave. in New York City (arguably one of the most valuable pieces of real estate in the country even without the tax incentive).

7 Columbus Dispatch, Thursday, September 7, 1978, p. 3.

8 The case involves the City of Duluth, Minnesota, versus Triangle Corporation, Stamford, Connecticut, and its attempt to move Diamond Tool and Horseshoe Co. For reference to other judicial challenges see “Factory Towns Start to Fight Back Angrily When Firms Pull Out”, Wall Street Journal, March 8, 1988.