The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

There are a number of ways to keep account of the gas in your car. The best way is to consult the gas gauge. It will tell you how much gas you have, and how much gas you have used since the last fill-up.

Absent a working gas gauge, you could keep a logbook, tracking the amounts of gas you have put into the car. This is a good deal trickier because you must also take into account the average miles per gallon your car gives, the proportion of city vs. highway driving, and many other factors that may affect your car's mileage. You are more likely to unwittingly run out of gas by using the logbook method of accounting than by consulting your online, real-time gas gauge.

Banks and savings and loans (S&Ls) must account to regulators for their assets. To do this, there are a number of basic accounting yardsticks, just as there are various ways to measure gas and gas consumption in cars. And, while the analogy with automobile gas tanks should not be pushed very far, there are some suggestive similarities. This Chicago Fed Letter argues that a realistic market-value accounting of S&L assets over the last decade or two could have lessened the financial price of the present S&L bailout by providing policymakers with better information on the magnitude of the problem. Indeed, the introduction of market-value accounting now may help prevent future financial losses.

How it is done today

S&Ls and other depository institutions keep their books and render their financial reports on the basis of generally accepted accounting principles (GAAP) or regulatory accounting principles (RAP), when these are prescribed by regulators. Still another accounting method, called tangible accounting principles (TAP), is sometimes used. These procedures generally call for the continued carrying of assets and liabilities on balance sheets at book value (including any amortization or accretion), ignoring many subsequent economic events that might affect their market values.

Such events include changes in interest rates, in the value of loan collateral, or in the riskiness of unsecured loans. Gains and losses in these assets are registered generally only when they are sold.

Why it is done that way

The traditional appeal of conventional accounting practice arises from its use to track cash flows and transactions. But accounting numbers are also used to determine the solvency of firms. As a result, many bank and S&L managers genuinely believe that the conventional practice of reporting assets and liabilities at book value is more appropriate than market-value accounting. Market-value accounting seems to them to be synonymous with "liquidation value"; therefore, it should not apply to a going concern.

What is the S&L industry worth?

Three book-value measures and one market-value measure of S&L capital from 1980 to 1988 are shown in figure 1. The differences among the book-value measures and the market-value measure (MVAP) are startling.1 The book-value measures of net worth were all positive throughout the 1980s, while the market-value measure of net worth was negative, reaching a low of about −$100 billion in 1982. The losses associated with the 1979-81 interest-rate runup were never fully reflected in the book-value measures of net worth, but they were reflected in market-value net worth. The decline in interest rates since the end of 1982 has resulted in an improvement in market-value net worth, but it still remained negative at the end of 1988. Since December 1982, book-value net worth has significantly improved due to permissive accounting practices allowed by Congress and the S&L regulators.

1. Four measures of S&L worth

During the early 1980s, the health of the S&L industry appears best when net worth is measured according to RAP. RAP allows S&Ls to count, as part of capital, net worth certificates issued by the Federal Home Loan Bank Board (FHLBB) to increase recorded, though not economic, net worth, appraised equity capital, and qualifying subordinated debentures, and to defer losses on the sale of assets that bear below-market interest rates. At year-end 1982, RAP net worth of the industry was $25.3 billion compared with $27.8 billion at the end of 1981. Capital computed according to GAAP, however, declined from $27.1 billion in December 1981 to $20.2 billion in December 1982. When capital is calculated by TAP standards, goodwill and other intangible assets are excluded to arrive at the tangible capital. By this net worth measure, capital declined from $25.5 billion in December 1981 to $3.7 billion at the end of 1982.

The intangible-equity categories were primarily responsible for the rise in RAP to $64.5 billion by the end of 1988. By December 1988, GAAP net worth had also risen to $53.6 billion. However, generally accepted accounting principles continue to allow S&Ls to count as part of capital the amount of goodwill and other intangible assets resulting from mergers. When net worth is calculated by TAP standards, capital rose to $32 billion by the end of 1988, but was still below its level at the beginning to this decade.

While TAP provides a more accurate measure of S&L capital than RAP and GAAP, it tends to a similar overstatement of equity because mortgages and other fixed-interest long-term obligations are still carried at book rather than at lower market values.

Capital measured in MVAP terms, adjusted for goodwill, paints a different picture. S&Ls' fixed-rate mortgage portfolios have been marked down as necessary to reflect the investment's current value. Restating TAP net worth to reflect the decline in the value of fixed-rate mortgages provides an estimate of the market value of capital. Measured by MVAP, the industry was insolvent throughout the 1980s, reaching a deficit of $100 billion at the end of 1982. Since December 1982, MVAP capital has significantly improved due to lower interest rates but still remained negative at the end of 1988.

Other approaches to measuring net worth show the industry to have been solvent throughout the period. Figure 1 shows that book-value measures have been extremely misleading yardsticks of the overall financial health of the S&L industry. Because book-value accounting measures fail to account for the real changes in the financial condition of a S&L, they may lead to different enforcement and closure decisions than will MVAP. The negative MVAP numbers provide a better picture of the current financial condition and explain the rise in S&L riskiness and failure throughout the 1980s.

Why MVAP is better

Because many assets and liabilities have been purchased under different credit market conditions, their book values are of little help in evaluating the current financial condition of S&Ls. For example, if an S&L originally paid $1 million for each of two securities, both due in 1992, one bearing an 8.25% coupon (bought in 1985) and the other bearing an 11.5% coupon (bought in 1982), both securities would be reported as $1 million in assets on this year's balance sheet. However, it is highly unlikely that both of these securities would sell for $1 million at the same time. Because the acquisition prices of these assets were dictated by prevailing economic conditions and interest rates, conventional book-value financial statements measure each S&L's financial condition by a yardstick, unique to that S&L, that blends past credit market conditions. These yardsticks are not only irrelevant for the current structure of interest rates, but they do not allow us to compare the balance sheets of different S&Ls.

Market-value accounting, on the other hand, reports the current market value of assets and liabilities so that prevailing market conditions become a common standard of measurement. Market-value accounting principles will mark asset portfolios up or down as necessary to reflect the investment's present value.

Let's suppose that an S&L made a 30-year, fixed-rate $150,000 mortgage loan at the prevailing mortgage interest rate of 8.35% at the beginning of 1970. The unpaid book value would be reported on the S&L balance sheet at the end of each year. (This number is not the same as current market values.) Figure 2 shows the unpaid book and market values at the end of each year over the 1980-88 period. At the end of 1980, the mortgage loan had an unpaid book value of $129,832 and a market value of $94,424 at the prevailing higher interest rate of 13.28%. The difference between the book and market values of $35,408(=$129,832−$94,424) provides an estimate of the overstatement of S&L assets caused by using historical cost accounting rather than market valuation. This overstatement had fallen to $4,524 at the end of 1988, reflecting the decline in interest rates.

2. A loan’s worth to an S&L

Although critics of market-value accounting claim that, because interest rates are volatile, market-value accounting financial statements will be everchanging, proponents of market-value accounting welcome these revisions because they provide timely descriptions of each S&L's financial health. Critics also suggest that market-value accounting encourages analysts to become myopic, to pay too much attention to temporary and fleeting credit market yields, but proponents reply that marking assets and liabilities to market encourages longer-run earnings analysis.

Why do regulators need market-value information?

The deficiencies of current accounting procedures are no minor matter. The cost of the S&L bailout has been and continues to be affected by the decision rules on when to require an institution to be recapitalized or liquidated. The federal deposit insurer must have both the regulatory authority and the information to be able to intervene in the operations of an S&L that is headed for insolvency. Ideally, the deposit insurer would be able to force recapitalization sufficiently in advance of insolvency so that there would be no financial cost to the deposit insurance fund. With early intervention, the improper practices of the S&L would be corrected and its financial fortunes turned around, or it would be placed in more competent hands.

Almost no one disputes that the federal deposit insurer needs adequate examination and supervisory powers to achieve this task. But there is much less recognition that up-to-date, market-value information on S&Ls' assets and liabilities is equally important for this regulatory function. To know which S&Ls truly are in trouble, where the problems are worst, and where the greatest cost exposure to the deposit insurer lies, the deposit insurer needs to know the current market value of its insureds' assets and liabilities. This must include the effects of current interest rates and economic conditions on asset and liability values, as well as their effects on off-balance-sheet items such as interest-rate swaps, loan guarantees, and letters of credit. Market-value accounting information will enable the calculation of true capital and the identification of economically insolvent S&Ls.

Often, federally insured depository institutions are not declared legally insolvent at the time that they become economically insolvent. Rather, a depository institution is declared insolvent by the appropriate regulatory agency, generally the chartering agency, when the value of its assets by whatever accounting standard applied by the agency, usually GAAP or RAP, declines below the value of its liabilities. The FHLBB historically used RAP-insolvency as a basis for certification of insolvency.

Because legal insolvency differs from economic insolvency, a market-value accounting system would not take the failure decision out of government hands. As long as the deposit insurance agency remains free to offer capital assistance to failing firms, market-value accounting would merely curtail rather than eliminate regulatory discretion as to whether and when to close an economically insolvent institution. However, by forcing more timely and more explicit forms of intervention, market-value accounting would reduce an insolvent institution's opportunities for pursuing go-for-broke strategies. Stale, cost-based, historical, book-value accounting information is simply inadequate and irrelevant for this purpose.

S&Ls whose portfolio book values mask market-value insolvency promote the sunny, though dangerously false, view that unrealized losses are less harmful to society than realized ones. However, the main difference between the two types of losses lies in the incentives they generate. In realizing a loss, the institution publicly acknowledges its effect and takes out of its portfolio the continuing risks associated with the investment that generated the loss. When past net losses remain unrealized, the effect remains hidden and the investments that generated the losses stay in the portfolio to grow or decline in the future. Because unanticipated gains tend to accrue in greater proportion to stockholders while unanticipated losses tend to accrue disproportionately to the federal deposit insurance agency, it is inappropriate for regulators to employ an accounting scheme that neglects the impact that unrealized losses have on the institution's capital position and risk-taking incentives. The use of market-value accounting should improve the regulators' ability to enforce meaningful capital requirements.

Conclusions

The commonly used accounting principles fail to account for the real changes in the performance of S&Ls and, as a result, keep us in the dark on the true financial health of the S&L industry. Market-value accounting provides a more accurate measure, especially when unexpected changes occur. Market-value accounting is not popular among many bank and S&L managers, especially those for whom it would mean unfavorable accounting results in the short run. But the viability of the deposit insurance fund requires a longer-run focus, by regulators and Congress, on the type of accounting information needed. MVAP cannot prevent bad decision-making or fraudulent practices, but it can make it easier for regulators, investors, and bank and S&L managers to make sound decisions.

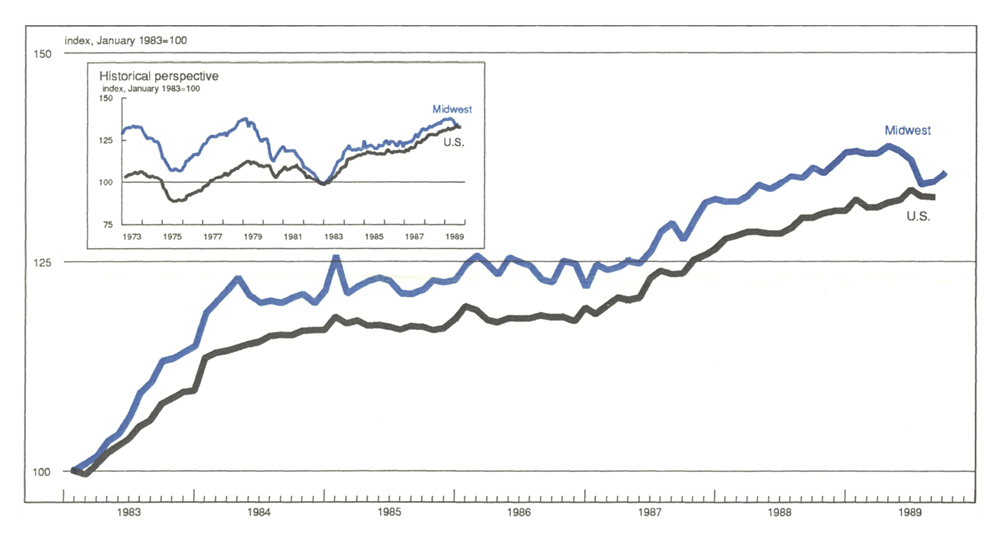

MMI—Midwest Manufacturing Index: Current expansion

Manufacturing activity in the Midwest edged upward in September for the second month in a row, after three straight months of softening. The gains in September were widespread among both durable and nondurable industries. An encouraging sign was that both labor and capital usage were up.

Nationally, manufacturing activity, measured by a methodology similar to the MMI, declined in both July and August. Given employment declines in the manufacturing sector for September, announced by the Labor Department, the USMI is expected to show further decline in September. If so, the softness indicated by the MMI will have anticipated the national weakness by three months, which is consistent with past behavior.

Note

1 For a more detailed study of accounting and the S&L crisis, see Brewer, "Fullblown crisis, half-measure cure," Economic Perspectives, Federal Reserve Bank of Chicago, November/December 1989.