The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

When the final bill is in for the 1980s, the difference between assets and liabilities at insolvent banks and thrifts may well turn out to have been as great a $200 billion—over $2,000 per household. The magnitude of the losses has propelled the debate over deposit insurance reform to the top of the political and regulatory agenda.

Economists have argued about deposit insurance reform for many years. For most of that time, their arguments—both pro and con—were based more on theory than on empirical evidence. But events in the financial services industry, especially in savings and loans (S&Ls), have now provided the needed empirical underpinning. Recent research has further amplified our knowledge of the effects of deposit insurance and the importance of market forces in the regulation of banking.

Based on the accumulated evidence, this Chicago Fed Letter asserts several propositions that should form the basis of future debates on deposit insurance.

1. Deposit insurance is different

What has become abundantly clear is that deposit insurance is very different from other forms of insurance. With other forms—life, auto, etc.—the insurer has only limited control of risk once the decision to insure and the terms of the contract are set.

With deposit insurance, the insurer can control risk. Indeed, losses are only incurred when the insurer has failed to act promptly with the regulatory tools it has at its disposal—particularly its power to close an institution before, or as soon as, it becomes insolvent. Thus, the costs of deposit insurance can be made arbitrarily small by forcing recapitalization, liquidation, or merger before losses begin accruing to the insurer.1

2. Moral hazard is real

The failure—for whatever reasons—of the regulatory bodies to use their preventive tools to avert deposit insurance losses represents, in effect, a subsidy to insolvent and poorly capitalized financial institutions. The availability of this subsidized deposit insurance gives beneficiaries an incentive to increase their expected profits by taking additional risks. This is known as moral hazard. The evidence that moral hazard is an important part of the deposit insurance problem takes several forms.

For example, Charles Calomiris found that during the 1920s failure rates for banks participating in state-run deposit insurance schemes were more volatile than failure rates for uninsured national banks. This suggests that insured banks were taking greater risks than uninsured banks.

Other evidence comes from the thrift industry during the 1980s. Capital-deficient and insolvent thrifts were the ones most heavily involved in nontraditional activities at that time. What is less well- known is that most of these thrifts were already insolvent when they began their expansion into nontraditional activities following the passage of the Garn-St Germain Act in 1982. Indeed, those institutions that are the most insolvent today were also the most insolvent in 1982. This fact suggests, and several studies confirm, that these institutions were engaged in end-of-game play—going, as it were, for broke. This kind of behavior was made much easier by deposit insurance and the failure of the regulatory agencies to enforce meaningful capital guidelines.

Several recent studies suggest that poorly capitalized institutions have actively sought to take additional risk. George Benston and Michael Koehn found that increased emphasis on riskier nontraditional activities by these thrifts resulted in greater stock price volatility. In contrast, shifts toward nontraditional activities by healthy thrifts reduced stock price volatility. This suggests that distressed thrifts were acting to maximize the value of deposit insurance. Elijah Brewer tested the hypothesis that shareholders of distressed thrifts rewarded additional risk-taking by management. He found that the announcement of shifts in asset composition toward nontraditional activities resulted in a one-time increase in the market value of equity for distressed institutions but had no effect on healthy institutions. This suggests that the shareholders encourage moral hazard by rewarding actions that raise the value of the insurance subsidy.

The evidence of moral hazard in banking is weaker than it is in S&Ls, perhaps because only a small portion of the industry has been insolvent at any one time. However, there is evidence that the same factors are at work. Gregory Gajewski used a failure prediction model to identify 600 small banks that were “persistently vulnerable” to failure. A third of these 600 banks displayed the same rapid growth of assets that has been associated with end-of-game play in the thrift industry.

3. Forbearance is costly

Allowing an insolvent financial institution to remain open is known as forbearance. Deposit insurance creates a climate that fosters forbearance. Those who stand to lose from closures—stockholders—can apply great political pressure to regulators. Regulators themselves may be reluctant to admit that banks under their supervision need to be closed. During the 1920s, for example, Nebraska regulators permitted some insolvent banks to operate for 10 years before they were closed.

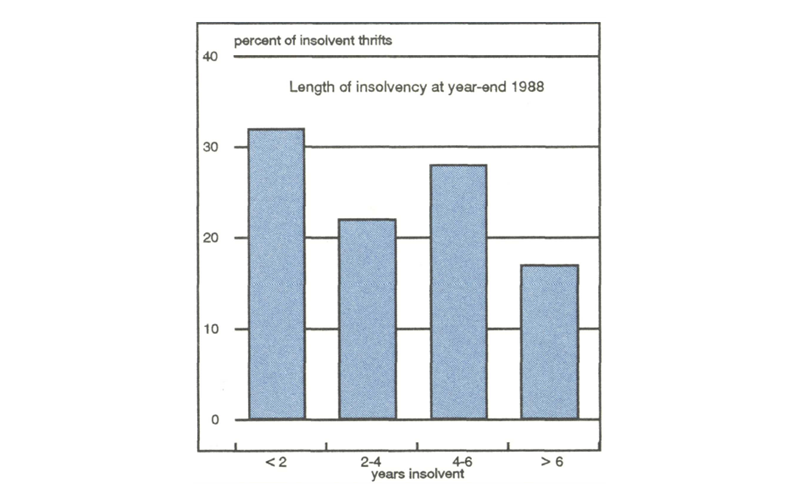

Forbearance was endemic in the thrift industry during the 1980s. James Barth, former research director for the Federal Home Loan Bank Board, reports that 45% of the thrifts that were insolvent in 1988 had been insolvent for four or more years. (See figure 1.)

Figure 1. Fruits of forbearance

During the 1980s, forbearance has also occurred in commercial banking. Bank regulators did not force commercial banks to reflect fully their losses on loans to less developed countries (LDCs). Also, during the 1980s, Congress gave preferential treatment to small agricultural banks facing capital problems.

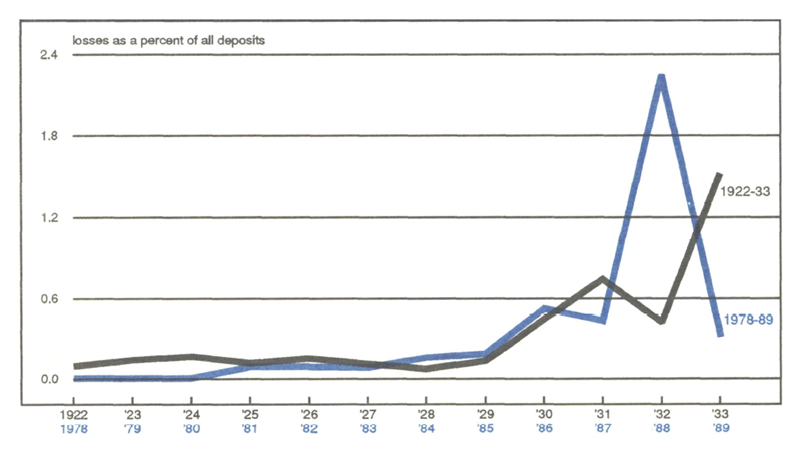

The final piece of evidence is that the banking system is incurring more losses today, when it is shielded from the market by deposit insurance and forbearance, than it did prior to the creation of federal deposit insurance. Losses per dollar of deposits are higher today than in the 1930s. This is particularly striking because GNP fell 30% in the early 1930s while it rose during the 1980s by 28%. (See figure 2.)

Figure 2. Depositor and insurance fund losses

One could argue that the 1920s provide a more relevant comparison. And here the contrast is even more striking. Loss rates during the 1920s were about 0.1% of all deposits while in the last half of the 1980s they were about 0.7% of all deposits.

4. Market forces are valuable

Market participants do not necessarily have better information. However, they have different incentives to make use of the information they do have. Depositors at uninsured banks have an incentive to run as soon as they have doubts about the condition of the bank. In this environment, forbearance is more difficult to achieve. With deposit insurance in force, however, the closure decision becomes entirely a regulatory event.

The elimination of uninsured creditors also has political implications. When uninsured creditors are present, effective forbearance merely redistributes money from these creditors to shareholders. For every shareholder who benefits from forbearance, there will be an uninsured creditor who loses. Thus, forbearance generates few benefits for politicians or regulators. With the elimination of creditor discipline, the only market influence left is from shareholders. The goal of the shareholders of an insolvent bank is simple—to keep the bank open as long as possible. To do so, shareholders will lobby anyone and everyone in sight. The result is greater forbearance and a more costly deposit insurance system. Deposit insurance reforms that restore creditor discipline will be doubly effective because they will also restore political discipline.

5. Banks—and regulators—need sensible, explicit directives

One of the reasons the current system has broken down is that regulators have, rightly or wrongly, been so concerned about deposit runs that they have been unwilling to permit uninsured depositors to suffer losses. But lowering insurance limits will not be sufficient to restore creditor discipline. Congress must either explicitly tell regulators that it wants these losses imposed, or Congress and regulators must find a way to restore creditor discipline without relying on deposit runs.

Indeed, the experience of the 1980s has shown that at least some creditors of large institutions can be penalized without creating spillover to the rest of the system. The best support for this proposition comes from our experience in Texas. Creditors at several large Texas holding companies suffered significant losses during the 1980s. The systemic effects of this have been minimal. Clearly, if the notion that some banks are too-big-to-fail has any implications, they are about who in the private sector should bear losses, not whether or not the losses should be borne by the private sector. This suggests that proposals to place the primary burden of creditor discipline on subordinated creditors,2 on private insurers, or on mutual guarantee systems may be more compatible with regulators’ incentives, and hence more useful, than a proposal to simply adhere to de jure insurance limits.

How can the regulatory system promote rapid closure? The SEC’s regulation of broker dealers provides an example. Minimum capital requirements, market-value accounting, uninsured debt, “haircuts,” and a closure rule that shuts firms down while they still have positive capital work together to control losses arising from asset portfolios that are much more volatile than those held by banks. Similar systems are employed by futures clearinghouses to regulate clearing members. It is interesting to note that, despite the risky nature of the business they conduct, no clearing member of the Chicago Board of Trade or the Chicago Mercantile Exchange has ever failed. Bank regulators would do well to study these sorts of systems more closely than they have.

6. Reform should precede new powers

When high-risk activities can be funded with artificially cheap insured deposits, expanding banks’ powers only serves to broaden the opportunities for bank risk-taking. However, with proper restrictions in place, expanded powers can be beneficial. In another study, Brewer examines the impact of expanded powers on bank holding companies. The findings are instructive. In contrast to the thrift experience, Brewer finds that nontraditional activities were risk-reducing for all holding companies and were most beneficial for holding companies that initially had the greatest risk of failure.

Why the difference between the two industries? As noted earlier, BHC creditors have sustained substantial losses. Because creditors will be at risk, BHCs’ subsidiaries will not be able to fund themselves unless they make prudent investments. In this case, firewalls perform the vital function of keeping nontraditional activities from being funded with insured deposits. The lesson is clear: With creditor discipline, expanded powers are beneficial. Without creditor discipline they are a disaster.

Conclusion

The heavy losses suffered by insolvent banks and thrifts during the 1980s make clear the important role that the closure decision plays in controlling the cost of deposit insurance. Had creditors or regulators closed down these institutions as soon as their condition had become imperiled, the losses to the deposit insurance funds would have been much smaller. However, the government’s de jure and de facto guarantees eliminated depositor incentives to withdraw funds from capital deficient and insolvent institutions.

This loss of creditor discipline had two consequences. First, the government regulators were forced to bear the entire responsibility for restructuring insolvent institutions. Second, there ceased to be a political constituency interested in seeking the rapid closure of insolvent institutions. This led to delays in closing insolvent institutions and in turn created a serious moral hazard problem.

These developments underline the crucial role that creditor discipline plays in controlling risk-taking. They also suggest that deposit insurance reforms that fail to create a private sector constituency for prompt closure begin their operations with a possibly fatal flaw. If legislators and regulators wish to avoid failure of future deposit insurance systems, it is important that creditor discipline be reintroduced and that regulators have an incentive to permit that discipline to work.

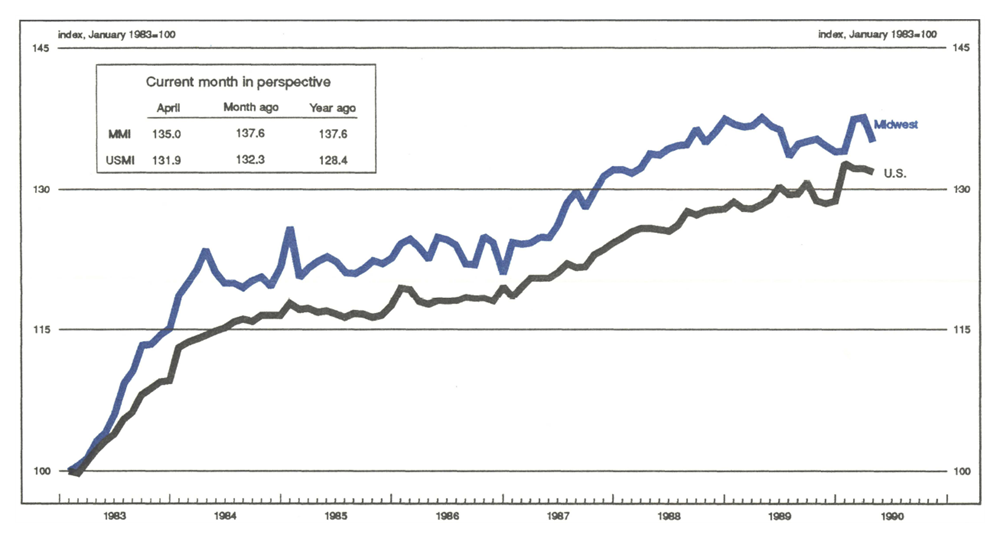

MMI—Midwest Manufacturing Index

After rebounding in February and March from January’s depressed auto production levels, manufacturing activity in the Midwest dropped sharply (down 1.8%) in April. Most industries experienced the decline, led by transportation equipment and primary metals. Only industries in the chemical sector continued to expand in April. Nationally, manufacturing activity declined 0.3%.

The pattern in manufacturing activity is being heavily influenced by auto production. Auto production dropped to a 4 million- unit annual rate in January, from over a 7 million rate at the end of 1989. After rebounding to a 7 million-unit rate in March, production dropped again to a 6 million rate.

Notes

1 Benston, George J., Robert A. Eisenbeis, Paul M. Horvitz, Edward J. Kane, and George G. Kaufman, Perspectives on Safe and Sound Banking: Past, Present, and Future, Cambridge, Mass.: MIT Press, 1986.

2 See, for instance, Silas Keehn, Banking on the Balance: Powers and the Safety net, Federal Reserve Bank of Chicago, 1989.