The Clean Air Act Amendments of 1990 set forth strict air quality standards for the nation.1 In addition, they lay out a schedule for meeting these standards and specify costly penalties for any nonattainment areas that fail to meet their designated deadlines.

The 1990 Amendments are thus explicit and uncompromising in one regard. Yet at the same time, they introduce a degree of flexibility for meeting air standards. Rather than relying exclusively on traditional command-and-control approaches as in the past, the regulations give firms and states considerable latitude to determine how they will meet federal air standards. By exercising creativity and exploring options such as market-based incentive programs, individual firms, states, and regions may be able to develop cost-effective strategies that will mitigate the costs of environmental compliance. Such creativity in turn will promote firm innovation that can enhance regional fortunes.

This Chicago Fed Letter describes the flexibility aspect of the new regulations and explores how it may alter a region’s compliance costs.

The three eras of air emissions regulation

Air emissions regulation has gone through three distinct eras. In the first, defined here as prior to 1977, a command-and-control approach reigned. Environmental regulations specified not only which levels of air pollution were allowable but also which methods and technologies should be used to reach compliance. During this period, regulations tended to place most of the responsibility for reducing pollution on large firms and emissions sources. As a result, direct regulatory costs were concentrated on a handful of mostly large facilities in a few industries such as petroleum and chemicals that could be characterized as large emitters. (As figure 1 shows, because of the nature of their production, these industries continue to bear most of the costs of pollution abatement.)

1. 1991 pollution abatement costs

| Top 5 industries | Percent of total abatement costs in manufacturing |

|---|---|

| Chemicals | 23 |

| Petroleum/coal | 16 |

| Primary metals | 12 |

| Paper | 9 |

| Food | 7 |

| Top 5 combined* | 68 |

Source: U.S. Department of Commerce, Current Industrial Reports, Pollution Abatement Costs and Expenditures, 1991.

In those years, the cost of complying with environmental air regulations varied across regions, depending on the geographic distribution of polluting industries and the severity with which individual states enforced federal standards. The resulting regional disparities in compliance costs led industrial states to fear that firms would try to avoid strict emission standards by relocating to states with lower standards or to states with “clean” environments that could more easily tolerate increased pollution. To counter this possibility, a second era of environmental regulation was born with the adoption of the prevention of significant deterioration (PSD) regulations in the Clean Air Act Amendments of 1977.2 These regulations prevented states with “clean” environments from accepting a deterioration of their environment as the price of attracting industries that would have had to comply with stricter emission standards elsewhere. Under PSD, new facilities that were built in states with superior air quality nevertheless had to meet stringent air quality standards. During this era, command-and-control strategies were still used to compel compliance with emissions standards, but PSD was intended to narrow the range of compliance costs across regions.

While the adoption of PSD would seem to have been a significant victory for industrial states, empirical studies of the pre-PSD era find that regionally differentiated compliance costs had only a small effect on location decisions.3 However, this finding may merely reflect the generally lax enforcement of environmental rules during that period. Several deadlines passed without the nation’s achieving the goals set by previous air emissions legislation. In addition, these studies did not specifically concentrate on the high-pollution industries in which one would expect regional cost variations to have sizable effects on location decisions.

This brings us to the third era of air emissions regulation, ushered in by the Clean Air Act Amendments of 1990. Moving away from a one-size-fits-all approach, these amendments classify nonattainment areas into five different categories, each of which has a different length of time to reach target air quality standards (see figure 2). “Severe” and “extreme” nonattainment areas will probably find it very costly to comply, yet stiff penalties are in store if they fail to do so. At the same time, however, the amendments permit states to devise their own innovative plans for compliance, including market-based incentives such as the trading of sulfur dioxide (SO2) emissions credits.

2. Ozone nonattainment categories

| Compliance deadline (from 11/15/90) |

|

|---|---|

| Marginal | 3 years |

| Moderate | 6 years |

| Serious | 9 years |

| Severea | 15 or 17 years |

| Extreme | 20 years |

The option for flexible compliance does not mean the elimination of all command-and-control regulation. Partly, this is because market-based systems will not be feasible for all emissions. Such systems require regular, precise monitoring of emissions in order to verify compliance and to establish an inventory of credits that can be traded. This kind of exact monitoring is not currently possible for volatile organic compounds (VOCs), a major category of ozone precursors.

Besides introducing the option of flexible compliance, the 1990 Amendments also increase the numbers and types of sources to be controlled. No longer will bringing large emitters into compliance be enough to meet environmental standards. In the Chicago area, for instance, it has been estimated that almost half of all VOCs are emitted by mobile sources.4 For this reason, mobile sources will also be subject to emission controls. So too will small firms. At present, it remains unclear how adding these firms to the list of controlled sources will affect the distribution of compliance costs among firms of differing size.

Given the combination of strict enforcement and inclusion of previously unregulated sources, the costs of complying with the 1990 Amendments will probably be high, particularly for severe nonattainment areas. However, the amendments also require each state to develop its own state implementation plan for meeting federal standards. By exercising creativity, states may devise plans that allow firms to meet air quality standards in flexible ways and thus reduce the cost of compliance. Options include switching to less environmentally harmful production inputs, installing emission control devices, buying “emission credits” from other firms, or any combination of the above.

Illinois is now developing an example of an NOx emission credits plan, which it will institute within the next year. Companies will be assigned maximum allotments of NOx emissions, and firms that reduce their emissions below their allotted levels will be allowed to sell the excess “credits” to others that find it harder or more costly to meet their own requirements. The price of the credits will be set by the market.

Such a program could well provide Illinois firms with a more cost-effective way to meet NOx standards than traditional uniform controls. A side benefit is that the program offers firms incentives to install continuous emissions monitors. These monitors will not only assess compliance, they will also yield more information about NOx emissions than has been attained under command-and-control methods, which often rely on periodic monitoring of compliance. NOx emissions are particularly amenable to measurement and recordkeeping at a reasonable cost, since a significant fraction is produced by large stationary sources.5

In some cases an entire region is working together to coordinate and improve its regional environmental policy. Eleven East Coast states and the District of Columbia, for instance, have established an Ozone Transport Commission (OTC), which produced a memorandum of agreement establishing guidelines for a possible interstate market for NOx emissions-offset trading. The establishment of such a program is still some time off. Yet the OTC has convinced member states to try to set up their intrastate trading systems in a compatible fashion so that they can be integrated into an interstate program in the future. Ultimately, such an arrangement would greatly increase the compliance options available to companies in the region.

How will the new regulatory framework affect regional economies?

From the point of view of regional growth and competitiveness, the key question regarding the flexibility aspect of the 1990 Amendments is how it will affect the incidence of compliance costs across regions. There are two ways of exploring this question. One is by looking at the impact of flexibility on individual firm behavior; the other is by examining the broader implications for an entire region.

A company is assumed to maximize profit, i.e., minimize costs. Under command-and-control regulations, a firm usually had to purchase a designated technology in order to comply. As such, the cost of compliance was added on to existing production costs, and the cost of the purchased technology was essentially the same for all like firms with similar-sized production facilities within a given industry. Flexibility in meeting standards will change both of these facts. Rather than being treated as an add-on to production costs, environmental constraints can now be built into a firm’s production decision.

Moreover, by adopting unique, least-cost methods for meeting environmental requirements, individual firms may actually be able to lower their compliance costs relative to their competitors. Since firms can treat pollution control as another input in their production function, they may be able to devise firm-specific advantages just as they do in regard to labor, capital, and materials decisions. The success of individual firms in capturing these compliance cost savings will depend on their ability to include environmental regulatory costs as part of their input substitution scheme. Because this ability may vary across firms, the variance in compliance costs across similar firms may increase as a result of the new flexibility.

Obviously, the flexibility available to firms will depend largely on the particular state’s compliance programs. By the same token, flexible programs are likely to have a wider impact than merely lowering the compliance costs of individual firms. For example, Harrison and Nichols estimate that California’s highly innovative Regional Clean Air Incentives Market program (RECLAIM), which establishes flexibility and market incentives to meet a variety of air emissions targets, might reduce the state’s aggregate compliance costs by up to 40%.6 Creative compliance programs that can generate similar savings could certainly help businesses located in the states or regions offering them.

How important the concentration of benefits from trading will be to a region’s economic development will also depend on whether regionally significant industries are recipients of these benefits, and whether the cost savings to individual firms are significant. If the savings are concentrated in industries that produce a large share of the region’s output, the total benefit to the region could be significant. However, if compliance costs are insignificant relative to labor, capital, and other costs, even a substantial savings in compliance costs may not yield any regional advantage.

Robinson argues that the real regional economic benefits of flexibility may be generated in the area of nonprice competition.7 Many economists find that market advantage tends to flow to firms that innovate and can move rapidly into new markets.8 Thus regulatory flexibility may provide the most significant advantage to firms (and to regional economies) not because it yields immediate cost savings, but because it encourages technical change and the productive flexibility that help firms innovate and exploit market niches. For example, in the case of emission reduction credits, polluters have incentives to accelerate compliance in order to generate credits that they can then sell on the market. This allows firms to use their in-house expertise to innovate rather than being forced to use a standard technology to reach a mandated air quality threshold. Obviously, regions that can nurture creativity in this way will benefit from the increased innovation occurring in their local firms.

Conclusion

The 1990 Clean Air Act Amendments are likely to raise compliance costs for nonattainment areas because they impose a strict schedule for meeting air standards and increase the number of firms subject to the new rules. However, the amendments provide for flexible implementation through means such as market-based approaches. It is this aspect that can mitigate the costs of complying for individual firms, states, and regions as well as stimulate innovative activity. In some cases, this flexibility may reduce the variance in compliance costs between attainment and nonattainment areas. It may even enable regions (particularly nonattainment areas) to gain an advantage over areas that do not allow flexibility. The critical questions will be to what extent individual states take the lead in devising innovative, market-based incentive plans, and how firms choose to achieve compliance with environmental standards. The results of these efforts are likely to affect the ability of regions to attract and retain businesses.

Tracking Midwest manufacturing activity

Manufacturing output index (1987=100)

| March | Month ago | Year ago | |

|---|---|---|---|

| MMI | 118.4 | 118.0 | 110.4 |

| IP | 113.4 | 113.3 | 108.5 |

Motor vehicle production (millions, saar)

| March | Month ago | Year ago | |

|---|---|---|---|

| Autos | 6.2 | 6.3 | 5.2 |

| Light trucks | 4.8 | 4.3 | 3.8 |

Purchasing Managers’ Surveys: production index

| April | Month ago | Year ago | |

|---|---|---|---|

| MW | 61.5 | 66.3 | 58.6 |

| U.S. | 51.8 | 57.4 | 56.9 |

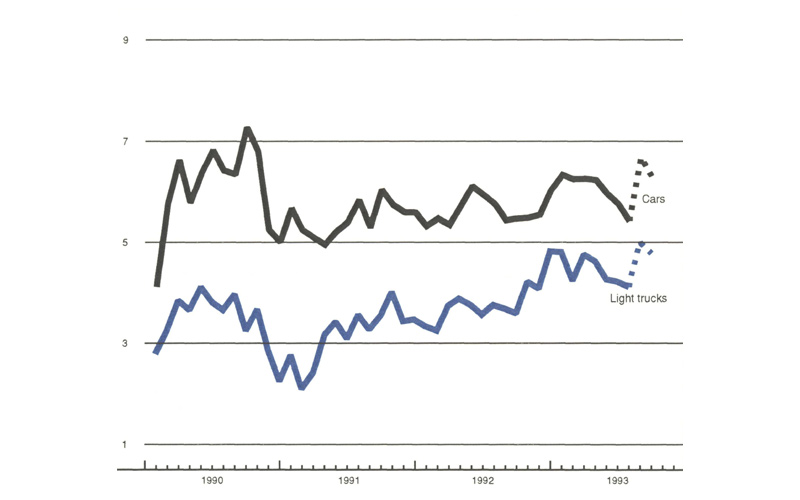

Motor vehicle production, millions (saar)

Sources: The Midwest Manufacturing Index (MMI) is a composite index of 15 industries based on monthly hours worked and kilowatt hours. IP represents the FRBB industrial production index for the U.S. manufacturing sector. Autos and light trucks are measured in annualized physical units, using seasonal adjustments developed by the Federal Reserve Board. The PMA survey for the U.S. is the production components of the NPMA survey and for the Midwest is a weighted average of the production components of the Chicago, Detroit, and Milwaukee PMA survey, with assistance from Bishop Associates and Comerica.

After slipping in the second quarter, domestic light vehicle production dropped further in July. Car and light truck output each declined on a seasonally adjusted basis. Despite the significant reduction in July, assemblies were still higher than the average level for 1992.

Sales have held up relatively well in recent months, and industry inventories are in good shape, particularly as fleet sales (some of which can represent a subtle form of inventory building) have been deemphasized in 1993. Flat to modestly improving sales should support production schedules calling for a significant increase in assemblies in August and September.

Notes

1 For a discussion of the Clean Air Act Amendments of 1990, see Don Hanson and William Testa, “Urban ozone regulations,” Chicago Fed Letter, Number 71, July 1993..

2 Peter B. Pashigan, “Environmental regulation: whose self-interests are being protected?” Economic Inquiry, Vol. 23, No. 4, October 1985, pp. 551-584..

3 Other location-specific costs such as the prices of land and labor were far more significant than environmental costs. Moreover, in the case of high-polluting firms, locational choices might have shifted production overseas rather than to lower-cost regions in the U.S. See Timothy J. Bartik, “The effects of environmental regulation on business location in the United States,” Growth and Change, Vol. 19, No. 3, Summer 1988, pp. 22-44; Virginia D. McConnell and Robert M. Schwab, “The impact of environmental regulation on industry location decisions: the motor vehicle industry,” Land Economics, Vol. 66, No. 1, February 1990, pp. 67-81; and Kevin T. Duffy-Deno, “Pollution abatement expenditures and regional manufacturing activity,” Journal of Regional Science, Vol. 32, No. 4, November 1992, pp. 419-436.

4 George Tolley, Jeffrey Wentz, and Steven Hilton, “The urban ozone abatement problem,” Proceedings of the Conference on Cost-Effective Control of Urban Smog, Federal Reserve Bank of Chicago, forthcoming, 1993.

5 John Calcagni, “Title l of the CAAA and implications for market-based strategies,” ibid.

6 David Harrison, Jr., and Albert Nichols, “An economic analysis of the RECLAIM trading program for the south coast air basin,” Cambridge, MA: National Economic Research Associates, Inc., March 1992.

7 Kelly Robinson, “The regional economic impacts of marketable permit programs: the case of Los Angeles,” Proceedings of the Conference on Cost-Effective Control of Urban Smog, op. cit.

8 For more on economic development strategies, see Michael E. Porter, The Comparative Advantage of Nations, New York: The Free Press, 1990; and Robert B. Reich, The Work of Nations, New York: Knopf, 1991.