The Covid-19 pandemic had an immediate and substantial impact on the commercial real estate (CRE) market—emptying workplaces, shopping centers, and hotels, thus affecting the cash flows of businesses occupying commercial space and in turn the ability of commercial space owners to meet their debt obligations.

Delinquent CRE loans began to surface soon after the pandemic started and remain elevated in 2021. Broad loan delinquencies would represent a potential threat to bank capitalization and solvency, particularly for smaller banks that tend to have higher concentrations in CRE lending. Collateral and loan performance have varied significantly by property type during the pandemic. However, regulators do not collect information on CRE exposures by property type at smaller banks, which limits our insight into the systemic implications of CRE exposures at these firms.

In this Chicago Fed Letter, we explore the shock to the CRE market brought about by Covid-19 and describe how it has affected bank portfolio-held CRE loans to date. Our insights are derived from large banks’ data since small banks, which turn out to be the most exposed to CRE loans, have less granular reporting requirements. We also discuss the headwinds facing the sector, considerations for banks and regulators going forward, and potential regulatory blind spots due to reporting data granularity.

The Covid-19 pandemic caused an immediate reduction in on-site business activity, reducing the cash flows of companies occupying commercial properties. As businesses shut down or downsized, vacant CRE space increased. The shock varied heavily across sectors as certain property types (e.g., hotel, retail, and office) experienced more dramatic stress than others (e.g., multifamily and industrial). Similar variation in market fundamentals was observed across geographies, with large, urban locales faring worse than smaller metros and suburban areas.

The shock to the CRE market affected the ability of property owners to satisfy their debt obligations. Delinquent CRE loans began to surface soon after the Covid-19 pandemic started and remained at elevated levels as of 2021:Q1. The pandemic has also led to declines in collateral valuations, which can affect the dollar amount banks recover when foreclosing a delinquent loan.

The outlook for the CRE market is uncertain, though recovery is likely to differ significantly across property types and geographic locations. Prolonged stress in the CRE market presents a direct risk to the banking sector as more CRE loans are issued and held on bank balance sheets than any other lender type. Within banks, however, smaller (community and regional) institutions tend to have much higher CRE loan concentrations relative to capital than their larger peers. Accordingly, any loan losses resulting from the pandemic will not fall uniformly across the banking sector. From a regulatory perspective, monitoring this issue is compounded by data limitations for community and regional banks; these entities are considered to pose less systemic risk and are not subject to the same detailed regulatory reporting requirements as their larger peers.

Introduction to CRE lending

Commercial real estate loans are generally used to finance the acquisition or construction of commercial space (e.g., apartment buildings, strip malls, warehouses, and offices). Many of these loans are issued by banks, although other financial institutions like government-sponsored enterprises (GSEs) and insurers also issue commercial mortgages. Unlike a residential mortgage, a commercial borrower’s ability to repay the loan is generally tied to the cash flows generated by the property itself, i.e., rents from leasing physical space to tenants. When tenants experience financial stress, their ability to pay rent, renew their lease, and/or demand new space is affected, and in turn the likelihood that the property owner (borrower) can make good on their mortgage payments decreases. If trouble persists, the borrower might eventually miss on its payments.

When there is risk that the borrower misses a payment, the lender must set funds aside (called reserves) for the possibility that the borrower does not pay back the outstanding amount in full. The higher the probability that the borrower does not pay, the higher the reserves the bank must set aside. Capital requirements are set so that in most cases banks have enough funds to cover their losses from unpaid loans. However, if the number of delinquent borrowers is unexpectedly large, expected losses might surpass available funds, and banks might need to raise additional capital to stay solvent.

Effect of the Covid-19 pandemic on CRE market fundamentals

The onset of the Covid-19 pandemic in the United States was accompanied by sweeping restrictions on the movement and gathering of people in shared spaces. Commercial real estate was instantly and profoundly impacted, with some property types experiencing much more stress than others.

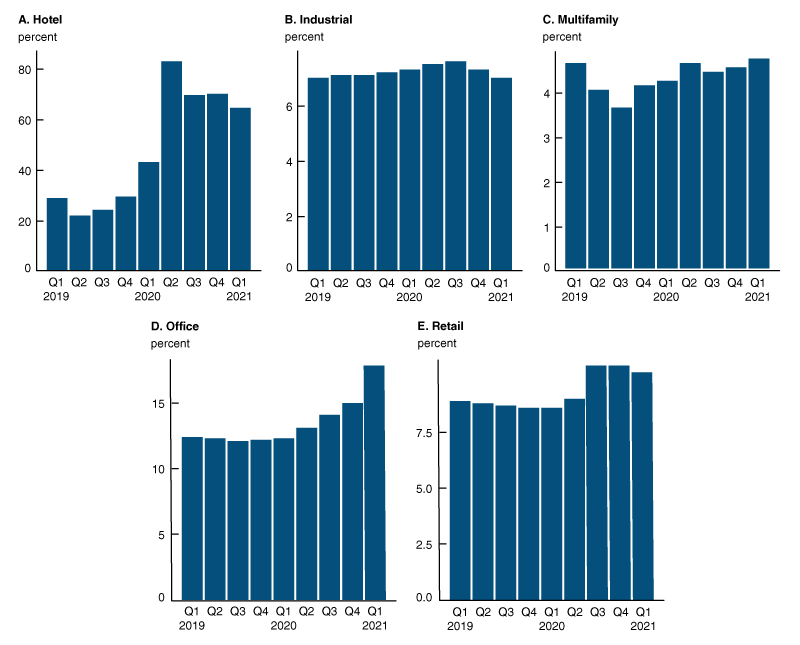

Travelers largely stopped visiting hotels immediately after the pandemic commenced. Hotel vacancy rates, as reported by CBRE Econometric Advisors, peaked at historically unprecedented levels in the spring and summer of 2020, and recovered only slightly by year-end. The national aggregate hotel vacancy rate was 64.4% in 2021:Q1, a dramatic increase from 28.6% in the same quarter of 2019, before the pandemic began (figure 1).

Office buildings began to see the effect of companies reducing their physical footprint in favor of remote/flexible work arrangements, reflected in an increase of 360 basis points (bps) in vacant office space from pre-pandemic levels to 16.0%. The first quarter of 2021 marked the fourth consecutive quarter in which vacant office space increased by 80 bps or more. Because office space is typically leased for three- to five-year terms, it is possible that this trend will continue throughout 2021 and into 2022 as existing leases expire and tenants are forced to make decisions about space requirements under new work arrangements.

Retail properties faced headwinds from the decline of brick-and-mortar shopping, with vacancy rates peaking at 9.4% in 2020:Q4 and recovering to 9.1% as of 2021:Q1, 50 bps higher than one year prior. Multifamily vacancies also rose from pre-pandemic levels throughout 2020 and as of 2021:Q1 were 50 bps higher than one year prior (but within 10 bps of the same quarter in 2019).

1. National-level vacancy rate by property type

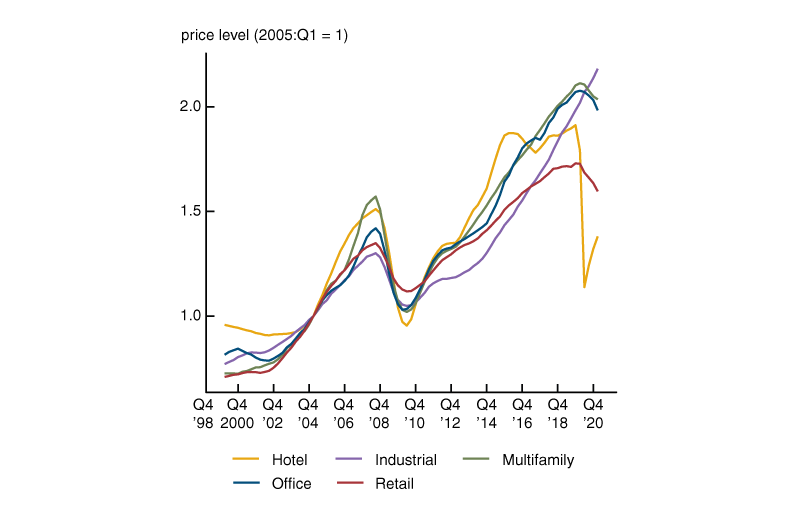

Deterioration in market fundamentals for CRE properties was reflected in declining value indexes for the property types most affected (see figure 2). Hotel valuations (as reported by CBRE) fell by more than 50% in 2020:Q2 but had recovered slightly by 2021:Q1. Retail, office, and multifamily (apartment) value indexes were all trending downward at the end of 2021:Q1. Industrial properties have been the major exception during the Covid-19 pandemic, as demand for warehousing and other industrial space has continued to climb in response to broader consumer trends.

Performance of CRE properties in 2020 was bifurcated not only by property type, but also by geography. Large, gateway cities and central business districts fared worse than smaller markets and suburban areas. San Francisco, for example, saw retail vacancies rise by 210 bps and multifamily vacancies by 310 bps on a year-over-year basis in 2021:Q1. New York hotel vacancies remained elevated above 75% in 2021:Q1, while office vacancies were up 420 bps, multifamily 170 bps, and retail 160 bps from a year prior.

The performance of the CRE market has direct implications on the loans used to finance these projects, and therefore on the issuers of these loans. Next, we describe bank exposure to this market and the effects we have observed on bank CRE loan portfolios to date.

2. National-level property value index by property type

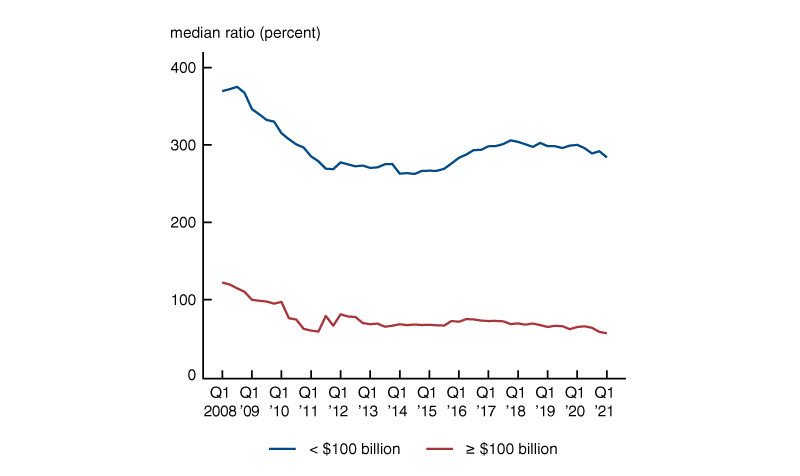

3. Median CRE concentration by firm size in total assets

CRE loan exposure in the banking sector

Banks hold the largest share of the CRE debt market, with roughly 38% of outstanding debt held on bank balance sheets as of 2020:Q4. Other sources of funding active in the CRE market include GSEs (e.g., Freddie Mac) with 22% of total outstanding CRE debt, life insurance companies with 15%, nonagency commercial mortgage-backed securities (CMBS) with 14%, and real estate investment trusts (REITs) with 2%; the remaining 9% is held by other institutions.

Community and regional banks tend to have higher concentrations of CRE loans relative to capital than larger firms. This disparity is shown in figure 3 as a comparison of the median CRE concentration of banks with less than $100 billion in total assets against the median concentration of banks with $100 billion or more in total assets. We define CRE loan concentration for a given bank as the ratio of CRE loan balances to tier 1 capital plus allowance for loan and lease losses (ALLL), as reported on the FR Y-9C.1 As of 2021:Q1, the median CRE concentration of smaller banks (289%) was over five times that of the largest banks (56%); this gap in CRE concentration has been present at a similar magnitude since at least 2008.

While the largest banks have much lower CRE exposure (relative to tier 1 capital) than smaller firms, regulatory data for these banks are available at a much more granular level through the FR Y-14Q collection,2 which covers firms with $100 billion or more in total consolidated assets. We use large bank data from the FR Y-14Q to illustrate differences in loan exposure and performance across major property types. This level of information (property type) is unavailable from reporting data for smaller firms, but crucial to evaluating and understanding the impact of the Covid-19 pandemic.

As of 2021:Q1, FR Y-14Q participating firms reported $748 billion of committed CRE loan balances in aggregate. Multifamily loans accounted for the largest share of CRE balances by property type at 37%, followed by office loans at 22% (figure 4).

4. FR Y-14Q committed exposure by property type

| Property type | Committed exposure (billions of dollars) | Share of total (percent) |

|---|---|---|

| Hotel | 50.12 | 6.70 |

| Industrial | 62.14 | 8.31 |

| Multifamily | 276.89 | 37.02 |

| Office | 166.30 | 22.23 |

| Other | 110.12 | 14.72 |

| Retail | 82.43 | 11.02 |

CRE loan performance during the Covid-19 pandemic

Signs of distress in CRE loan performance emerged early in the pandemic and have continued into the second half of 2020 and early 2021, particularly in the hotel and retail sectors.

In the CMBS market, hotel and retail loans moved into special servicing3 rapidly and in large numbers early in the pandemic. Roughly 30% of CMBS hotel balances and 20% of retail balances were either in special servicing or more than 30 days past due by June of 2020.4 Special servicing stabilized at those elevated levels throughout the remainder of 2020 and had decreased slightly to 25% of hotel balances and 16% of retail balances by March of 2021.

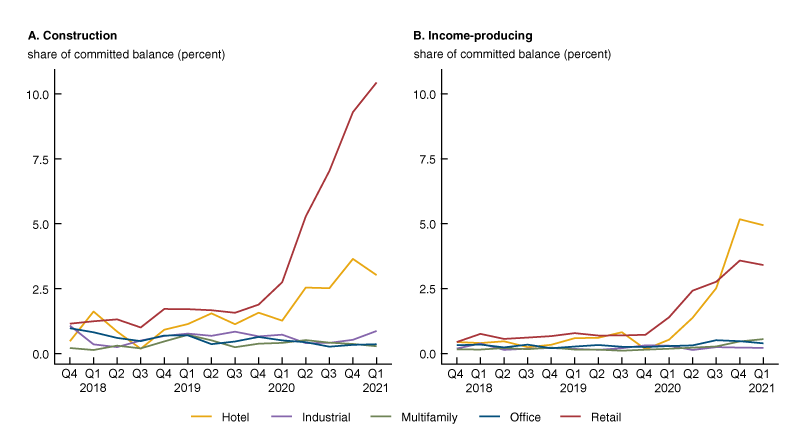

FR Y-14Q data also show bank loans in the retail and hotel sectors as the most affected by the pandemic to date (figure 5). Specifically, the share of retail construction balances either 30 days past due or on nonaccrual status grew from about 2% pre-pandemic to over 10% as of 2021:Q1. Approximately 5% of income-producing hotel and 3.5% of income-producing retail balances fell under the same categorization in 2021:Q1, though these numbers had declined slightly from the prior quarter.

Loans backed by office buildings have not seen the same effects on loan performance to date, despite the mounting vacant space in the sector we described earlier. Office loans, however, likely warrant continued attention going forward as longer-term leases expire and the market adjusts to the changing space requirements of office tenants.

5. FR Y-14Q loans more than 30 days past due or marked as nonaccrual

Given the relatively high concentration of CRE lending at small banks, and assuming loan performance at small banks during the pandemic follows a similar pattern to that of larger firms, it is possible that small banks have been particularly affected by the pandemic. Small banks with market footprints in the most at-risk locations and property types might have experienced material impacts to their portfolios and will likely be the most vulnerable going forward if stress to the CRE market persists.

Outlook

The outlook for the CRE market is uncertain, though recovery is likely to differ significantly across property types. Retail properties, for instance, will likely continue to face headwinds as consumers had already been shifting away from brick-and-mortar stores to online retail before the pandemic, and this pattern was accelerated by the pandemic. The extent to which the pandemic has a transitory impact on consumer behavior or a more long-lasting impact on the demand for retail commercial space is an open question for the industry.

Demand for hotels has started to return as vaccines have rolled out and movement restrictions have been lifted. Industry forecasts, however, suggest hotel demand is unlikely to reach pre-pandemic levels in the near term, due in part to lagging corporate travel and the potential that businesses adapt their practices and travel policies going forward. Considerable long-term uncertainty exists in the office sector as companies rethink their needs for space, with many implementing flexible and remote working arrangements; several large firms have already reduced their physical footprint. As noted above, office vacancy rates were rising and valuations falling at a sustained pace in early 2021.

Deterioration in fundamentals for multifamily properties has been comparatively limited throughout the pandemic, though some major markets and urban cores experienced outsized impacts and are still in the process of recovery. Fundamentals in the industrial sector remain strong in light of demand for warehousing space and consumer durable goods.

Given the projected variation in recovery across property types, it is likely that the heterogeneity observed in loan delinquencies to date will continue and that any losses resulting from delinquent loans and/or the sale of distressed assets will have different timing and severity depending on the sector.

The full scope of CRE loan loss going forward is still unknown, particularly for banks with a strong focus on the most-affected CRE sectors. While we expect less-exposed banks to be heading into calmer waters soon, the most heavily CRE-concentrated banks might be at heightened risk for some time. Notably, smaller (community and regional) banks tend to be much more exposed to CRE lending than larger banks, but the lower granularity of their reporting makes it difficult to evaluate their exposure to the most at-risk sectors. Insights from the more granular regulatory data available for the largest firms show that these at-risk sectors experienced distress following the onset of the pandemic and are at continued risk going forward.

Conclusion

The Covid-19 pandemic and associated behavioral changes immediately and substantially affected the CRE market and have already resulted in loan distress at banks with CRE loan portfolios. The speed and shape of the recovery for the CRE market is uncertain (especially for hotel, retail, and office properties); prolonged stress has the potential to cause continued loan delinquencies across the industry, while declining collateral values limit the amount banks can recover from delinquent loans.

The unique effects of the pandemic on the CRE market have highlighted a stark contrast in the concentrations of CRE loans at small banks relative to their larger peers. Regulatory reporting data required for the largest firms include more granular information than for firms under $100 billion, such as property type, which has been a distinguishing feature of loan performance in the pandemic. While the costs of additional reporting requirements for smaller firms must be considered, our observations highlight the likely benefits of improved transparency and capability to assess such firms’ potential risk should they come under simultaneous financial stress from a common risk factor in a material asset class.

Notes

1 FR Y-9C is a quarterly reporting schedule filed by domestic bank holding companies, savings and loan holding companies, U.S. intermediate holding companies, and securities holding companies with $3 billion or more in total consolidated assets. The information includes basic financial data on a consolidated basis (balance sheet, income statement, and detailed supporting schedules).

2 FR Y-14Q Schedule H.2 (commercial real estate) is a credit facility-level quarterly reporting schedule, including all balance-sheet loans at participating firms secured by commercial real estate with a committed balance greater than or equal to $1 million. Loans reported on the schedule include loans secured by multifamily properties or by other nonfarm, nonresidential properties (e.g., office buildings, hotels, etc.), as well as construction loans secured by real estate.

3 CMBS loans are occasionally transferred directly from the master servicer to a special servicer, specializing in workouts and modifications, if the loan is perceived as distressed and in need of more targeted attention. This can occur even if payments are still current on the loan but is generally an indicator that the loan is troubled.

4 More details are available online.