Like It or Not, 90 Percent of a 'Successful Fed Communications' Strategy Comes from Simply Pursuing a Goal-oriented Monetary Policy Strategy

Thank you for inviting me to speak today about monetary policy strategy and communications. Before I begin my comments, let me note that the views I express here are my own and do not necessarily reflect the views of the Federal Reserve Bank of Chicago or of my colleagues on the Federal Open Market Committee (FOMC) or within the Federal Reserve System.

Communications are critical for effective monetary policy strategy – they are inextricably linked. There are different approaches to, and much debate regarding, best practices. One approach is to have a full-throated discussion at the FOMC meetings, release a statement summarizing our view and then have the Chair hold a quarterly press conference to announce and explain the policy action to the public. This approach also includes describing how the action is intended to achieve the Committee’s policy goals. These post-meeting communications are followed by the release of the minutes, which give a fuller description of the comments made at the meeting. An alternative approach is to adopt a simple policy rule, like Taylor’s 1993 policy rule. The Committee would follow the policy rule prescription and report on any particular details regarding how the rule was implemented at each meeting. Again, a press conference could be used as a communications enhancement.

Although all central banks face these strategy and communications issues, and they implement them somewhat differently, my view is that 90 percent of the communications challenge is met by expressing policy intentions clearly so that the public can understand the Federal Reserve’s goals and how the Fed is committed to achieving these goals in a timely fashion.A clear expression of policy intentions requires stating the Fed’s policy goals clearly and explicitly. These messages need to be repeated – over and over again. It is also necessary to clearly demonstrate our commitment to achieving these goals in a timely fashion with policy actions.

An equivalent and more operational statement of this principle is that the Fed should follow a goal-oriented monetary policy strategy and should provide full accountability.

Notice the links between these two statements: “Express policy intentions clearly so that the public can understand the Federal Reserve’s goals” is captured by “follow a goal-oriented monetary policy strategy.” “The Fed’s commitment to achieving these goals in a timely fashion” is captured by “provide full accountability.” The final 10 percent of communications represents details that are crucially important for individuals and market participants, but the first 90 percent is the key to the public’s understanding of our policies.

Throughout the Great Recession, financial crisis and weak recovery, the Bernanke FOMC followed this goal-oriented approach. The September 2012 open-ended quantitative-easing (QE) program indicated the FOMC’s clear intention to facilitate maximum employment in a more timely fashion. The numerical forward-guidance thresholds we introduced in December 2012 reinforced this communication. The September 2013 decision to delay tapering the QE3 purchase rate was another clear indication of our intentions, as it further reinforced the data-dependence of this nontraditional monetary policy action.

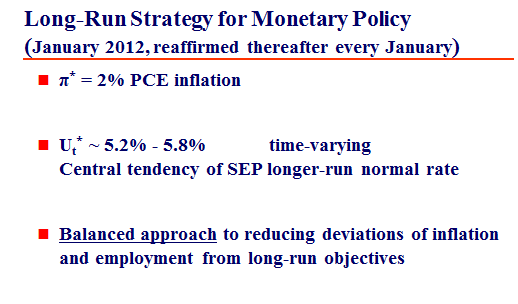

The January 2012 statement of long-run monetary policy strategy clearly expresses the FOMC’s policy intentions: It states that the FOMC’s explicit inflation objective is 2 percent for the price index for personal consumption expenditures (PCE) in the long run and that maximum employment is associated with a sustainable unemployment rate that properly reflects structural developments that may alter this rate over time. Our long-run strategy also points to the Committee’s Summary of Economic Projections (SEP) to provide a range of values for the sustainable unemployment rate. Currently, the central tendency for this range is between 5¼ percent and 5¾ percent. Finally, our strategy states that the Committee will use a balanced approach to reduce deviations from our long-run objectives.

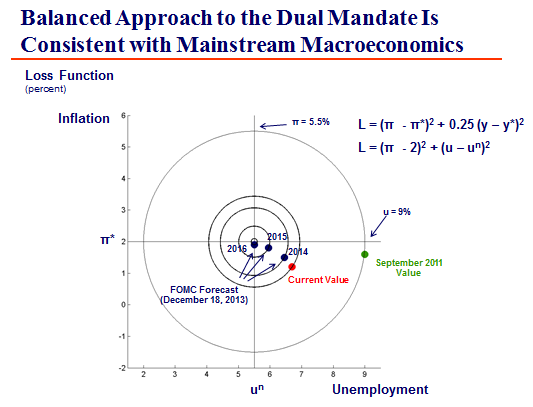

This balanced approach implies strongly that our policy loss function can provide what I refer to as “bull’s-eye” accountability. This entire chart is like a simple “corporate scorecard” for our two-dimensional policy objectives in unemployment and inflation outcomes. The circles provide collections of unemployment and inflation rates that are equally uncomfortable for FOMC participants. The chart clearly depicts the unemployment dilemma that the Committee still faced as of September 2011. For example, it tells us how a 9 percent unemployment rate can be depicted in “inflation-loss equivalent units” by showing what inflation rate gives an equivalent loss when unemployment is at its sustainable rate. The answer is 5½ percent inflation! All post-Volcker central bankers would respond to 5½ percent inflation as if their “hair was on fire.” Such a situation would call for strong and decisive monetary action. The bull’s-eye scorecard provides accountability. And indeed, in response to this loss, the FOMC acted. The FOMC had already employed QE2 in the fall of 2010. In August 2011, the FOMC employed a form of forward guidance and followed that up in September 2011 with the Maturity Extension Program, or “Operation Twist.”

The most recent December 2013 Summary of Economic Projections shows that the Committee forecasts that unemployment and inflation will reach the bull’s-eye mark by the fourth quarter of 2016. This is a relatively slow attainment of our long-run goals. It also should be pointed out that these are still just projections of improvement, yet to be achieved. Nevertheless, the enhancements to our communications in recent years go a long way toward meeting our communications objectives by using this scorecard to depict progress toward our dual mandate goals.

Our actions are strongly reinforced when the public knows that the FOMC is committed to achieving the bull’s-eye within a reasonable period of time with appropriate monetary policy actions. This is particularly true for unconventional policy actions. For example, consider Chairman Bernanke’s April 2012 press conference. At this event, numerous questions from journalists expressed skepticism that the FOMC’s Summary of Economic Projections indicated a clear commitment to closing the unemployment gap in a timely fashion. Following the adoption of our January 2012 strategy document, this public questioning was trying to assess whether these forecasts reflected a difference of opinion between the FOMC and the public on what is a “balanced approach to reducing imbalances,” or whether the forecast reflected the difficult and time-consuming process of consensus policy decision-making. In either case, the open public discussion of the issue enhanced the Fed’s accountability regarding the bull’s-eye scorecard. The entire discussion was taking place in public and contemporaneously with the policy decision. This is goal-oriented monetary policy with accountability. It is the combination of our January 2012 strategy statement, the quarterly SEP, the Chair’s press conference and repetition.

So, my claim is that to be any good, monetary policy communications regarding policy actions must be consistent with the Fed expressing policy intentions clearly, so that the public can understand the Fed’s goals and its commitment to achieving these goals in a timely fashion. This should be a principle for all effective monetary policy strategies and communications: to state monetary policy intentions clearly.

I will now be critical of incomplete attempts to solve this strategy and communications challenge by invoking and following an overly simple policy rule. John Taylor has repeatedly argued that the Fed has failed because it has not followed the 1993 Taylor rule. In March 2011, during his Senate testimony, Chairman Bernanke was asked why the Fed had not followed the Taylor rule.1 Chairman Bernanke replied that Fed policy has been remarkably consistent with the 1999 version of the Taylor rule. He also pointed out several issues associated with the fact that there is a zero lower bound on the fed funds rate.

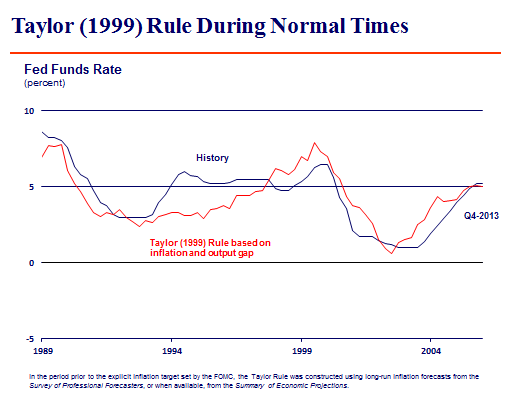

For me, there is a problem with simplistic approaches. Simple Taylor rules fail the strategic principle to express policy intentions clearly. At the zero lower bound, simple rules simply cannot be implemented. Accordingly, they cannot express policy intentions and do not allow the public to clearly understand the Fed goals and the Fed’s commitment to achieving these goals in a timely fashion. During quieter, normal times when short-term interest rates are 2 percent or more, many approaches may work. But how structurally sound are these simple rules? If a policy rule is sturdy, the test of its structural foundation comes when a hurricane or an earthquake hits.

The 1999 Taylor rule captures Fed policy reasonably well during normal times. I’d note, though, that the Taylor errors in the 1990s are big – actually, bigger than the loudest complaint that John Taylor lodges against the Fed for the 2003–06 violations of the rule.

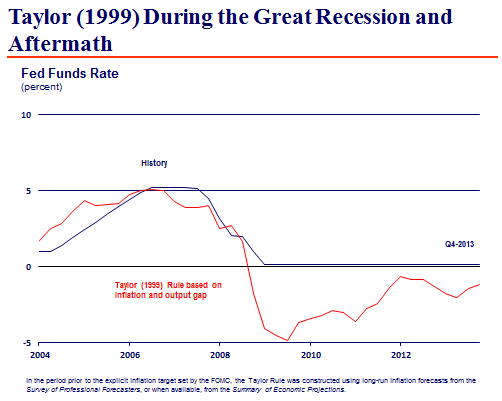

Of course, the rule completely breaks down during the Great Recession and its aftermath. It says to set the federal funds rate at minus 5 percent in 2009. We can’t do that. Moreover, there is no emergency handbook that comes with the rule that says what to do in this event. The effective policy rule is really the maximum of zero and the prescription from real rates and output and inflation gaps. We are thus left with inaction, and inaction looks like policy abdication and a failure to make timely progress in reducing policy imbalances. In these cases, this “policy rule” fails to provide clear policy intentions to achieve goals in a timely fashion and it fails to produce accountability at the zero lower bound. This rule cannot be the be all and end all — for a policy rule that some suggest should govern the implementation of monetary policy in the U.S., this is an absolute failure.

Furthermore, once the rule has failed, and done so for so long, how can we be confident that its prescriptions will still be a good policy to follow once the rule says that the fed funds rate should rise above zero again? More generally, it is difficult to figure out how to jury-rig work-arounds for these simple rules, because they often have a loose and ad hoc relationship between economic theory and the right-hand-side variables and parameters. It is particularly disconcerting that simple Taylor-type rules are typically offered without an explicit theoretical underpinning for the rule. Consider Taylor 1993. This specification follows a “rule of 2s:” 2 percent inflation objective relative to pre-1992 experience, 2 percent equilibrium real interest rate and parameter weights of ½.

The resulting constant intercept term in the rule is particularly vexing. It is well known that policy actions that fail to account for the time-varying nature of the natural rate of unemployment can lead to seriously inappropriate monetary outcomes — like double-digit inflation in the 1970s. Just as relevantly, it is well known that the equilibrium real interest rate is not a constant. However, the Taylor rule sets this intercept at 2 percent — a constant. How is this less egregious than simply assuming that the natural rate of unemployment is always 4 percent? Consider Larry Summers’ recent hypothesis that the U.S. may be facing a secular stagnation, which would contemplate a lower and perhaps negative equilibrium real rate. Maybe that is a small risk, but it has an extraordinarily high policy loss associated with the wrong robotic prescriptions for policy. According to Mehra and Prescott (1985), the historical average short-term real interest rate is less than 1 percent, with large variations over the long period they study.2

As I mentioned earlier, the Bernanke FOMC has worked hard to make the Fed’s policy intentions clear and provide accountability for our nontraditional policy actions to support more timely achievement of our goals. With the January 2012 long-run policy strategy, policy intentions are explicit: Get to bull’s-eye with labor market near 5½ percent unemployment rate and PCE inflation at 2 percent. When the federal funds rate is stuck at zero and goal-oriented monetary policy says do more — Do more! The quantitative-easing programs and enhanced forward guidance on short-term interest rates reflect a commitment to a clear policy principle. The Bernanke FOMC’s attention to policy misses has been vigilant throughout. And so the misses have led us to numerous policy interventions: QE1 in March 2009; QE2 in fall 2010; the forward guidance in August 2011; Operation Twist in fall 2011; the open-ended QE3 in fall 2012; and the threshold forward guidance in December 2012. What is the accountability test? Although much has been done — looking at the bull’s-eye scorecard — if anything, the FOMC has been less aggressive than the policy loss function might admit.

Despite the enhancements in recent years, there are remaining communications challenges regarding Fed policy intentions. The Fed has demonstrated that it will act aggressively to reduce resource slack when it is well away from its objective. It is less clear the public understands that we should be willing to overshoot our objectives in order to more speedily re-attain our goals. A slow glide toward our goals from large imbalances risks being stymied along the way and is more likely to fail if adverse shocks hit beforehand. The surest and quickest way to get to the objective is to be willing to overshoot in a manageable fashion. With regard to our inflation objective, we need to repeatedly state clearly that our 2 percent objective is not a ceiling for inflation. Our “balanced approach” to reducing imbalances clearly indicates our symmetric attitudes toward our 2 percent inflation objective.

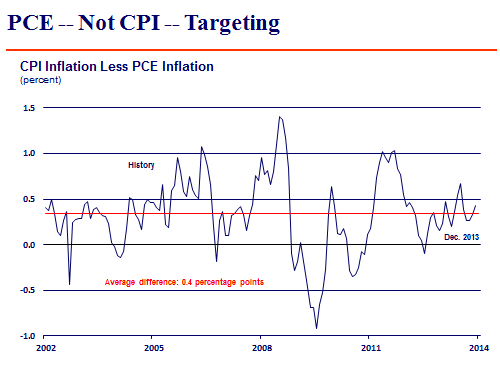

Let me point out another misperception regarding our inflation objective. It must be noted repeatedly that our 2 percent inflation objective is for the PCE price index. The more popular Consumer Price Index (CPI) tends to run about a quarter to a half point higher on average than the PCE index. Accordingly, this implies that price stability in terms of CPI inflation is higher, closer to 2½ percent. This is particularly important to note since a number of useful measures such as the Treasury Inflation Protected Securities (TIPS) inflation compensation that we and market participants so often refer to is in terms of the higher CPI numbers. Moreover, consumer inflation expectations likely are closer to CPI expectations, since the CPI is restricted to out-of-pocket expenditures and gets used for Social Security adjustments and the like. The PCE price index is the preferred inflation measure on theoretical grounds, and so it is the appropriate index to use for our inflation target; but as policymakers, we should call attention to these inflation measurement discrepancies in order to best communicate our policy intentions and make sure the public correctly interprets our policy goals.

There is a very real risk of confusion on this score. Last Friday, Jon Hilsenrath of the Wall Street Journal, who follows Fed communications very closely, mentioned that CPI inflation, at 1.6 percent, was rising a bit and it was getting closer to the Fed’s 2 percent objective.3 That is misleading. Our 2 percent objective is with respect to the PCE index. For the CPI, 2½ percent is a more accurate calibration of our price stability goal.

To conclude, clear communication is key to effective monetary policy strategy. I believe the Fed can meet 90 percent of its communications challenge by seeking to: “Express policy intentions clearly so that the public can understand the Federal Reserve’s goals and the Fed’s commitment to achieving these goals in a timely fashion.”

Notes

1 Ben S. Bernanke, 2011, “Semiannual monetary policy report to the Congress before the Committee on Banking, Housing and Urban Affairs,” U.S. Senate, Washington, DC, transcript, March 1.

2 R. Mehra and E. C. Prescott, 1985, “The equity premium: A puzzle,” Journal of Monetary Economics, Vol. 15, March, pp. 145-161. It is worth noting that updating the Mehra and Prescott results to include the more recent period yields similar results – low average real short-term interest rates with large swings across decades.

3 Jon Hilsenrath, 2014, “Grand Central: Maybe inflation isn’t as low as Fed thinks,” Wall Street Journal, Real Time Economics, blog, February 21.