Innovation in Electric Power?

Electric power is often considered the most transformative technology of the past 100 years. Its near universal adoption in our homes and workplaces (e.g., to power appliances, communications, and computers) is indeed remarkable. As a result, the electric industry today boasts $600 billion in assets in the U.S., as well as yearly sales of $260 billion (double that of the telecom industry). However, many believe that the business model by which the U.S. and Midwest produces and delivers electric power is outmoded and subpar. Movement toward a more competitive framework can be expected to produce innovations that would achieve significant cost reductions, greater reliability, and a cleaner environment.

The executive director of the Northeast-Midwest Institute, Dick Munson, has recently written a book entitled From Edison to Enron, which recounts the history of electricity and suggests an innovation-based vision for the future of the power industry.

In it, Munson describes major shifts in the electric power industry since its inception. At the dawn of the twentieth century, Chicago mogul Samuel Insull combined many small neighboring electric generation facilities, which achieved economies of scale and balanced loads throughout the day. In doing so, Insull was able to lower prices and increase reliability, thereby expanding the market and use of the product. At the time of his company’s peak in the 1920s, it served 4 million customers in 32 states.

Insull’s innovations transcended the physical production process. Tired of dealing with (and compensating) many local governments for the rights to serve fragmented local markets, Insull successfully pushed for state level regulation of electric power. And so, the state-regulated monopoly model eventually became the national norm. This bargain provided reliable power at regulated prices to consumers in return for state-sanctioned rates of return on investment for utility owners.

Though this model remained intact for most of the twentieth century, Insull’s business empire eventually collapsed amidst charges of corrupt business practices. Munson draws a thoughtful parallel between Samuel Insull’s business and Kenneth Lay’s Enron Corporation. Laying aside the later collapse of Enron, its futuristic business model for electric power production and delivery, trading across the broad geography of the United States, continues to shape the industry today. It is a model of competitive power production and, in some instances, competitive delivery, in which individual power producers have the incentive to innovate because they have a broad market in which to sell their product.

What are the possible gains (i.e., possible innovations) in following this new business model? According to Munson, the costs to businesses of power interruptions are on the order of $120 billion per year under the existing state-regulated monopoly model. Yet, under this older model, almost no research and development (R&D) takes place by the industry. At a recent book chat at the Chicago Fed, Munson said, “Last year, R&D expenditures by the dog food industry exceeded those of public utilities.”

Munson believes that we are on the verge of a vast array of innovations, if only they are not blocked by existing legislation and the old business model. In particular, progressive techniques for co-generation and other recycling of energy and waste energy are capable of producing remarkable efficiency gains. For instance, Scandanavian countries such as Finland are leading the way in co-generation, achieving upwards of 80% energy efficiency in electric power–heat production. And from an environmental perspective, efficiency gains from such techniques are every bit as “clean” as those touted from alternative fuels.

The Great Lakes region could become a leader in reforming its power industry if it chose to do so. However, if the region is to acheve a workable model of competition, a large and well-managed infrastructure must be put into place which would allow buyers and sellers to readily trade electric power.

In the meantime, the monumental price-spike disaster in California five years ago, following its experiment to decouple power production from the distribution of electric power, continues to give policymakers great pause. For instance, Illinois passed the Restructuring Act of 1997 that began to decouple power generation businesses from the power delivery and service businesses. In northern Illinois, very large customers (e.g., big corporations) began to negotiate their own purchases of electric power, while their local utility company typically maintained the responsibility for delivering it. For smaller customers, particularly residential customers, decoupling was deferred until 2007, and rates were frozen (actually lowered 20 percent) until that time. In the meantime, independent power producers were encouraged to get on to the delivery network. After 2006, the utility company, Commonwealth Edison (CE), will act as a purchasing agent for residential customers, buying power from independent producers through an auction process and passing along both distribution charges and power costs to consumers.

After the rate freeze expires, CE will require a rate increase to pay for its infrastructure investments in the distribution system since 1997. In 2005, some critics feared that the particular process by which CE would bid for power would raise customer rates unduly. And so, the prospect of a price spike for residential customers when the price freeze expires contributed to an outcry over CE’s plans to move to the auction process in 2007. Nonetheless, plans for this next phase of deregulation were approved by the state’s regulatory authority.

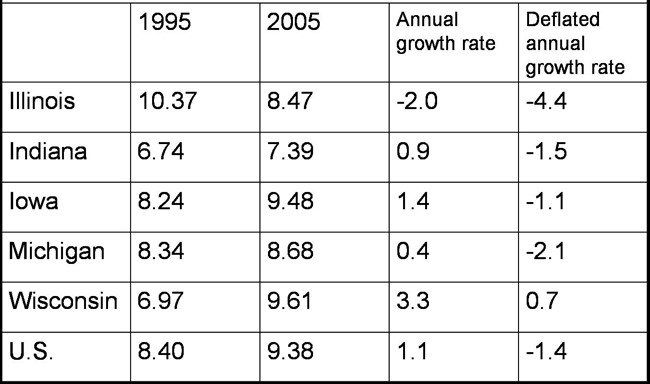

Much like residential and small customers in most of the nation, those in Illinois have enjoyed a long period of stable or declining prices. From 1995 to 2005, the real or inflation adjusted price of electric power has declined by an annual average of 4.4 percent. Of course, electric bills have climbed along with the increasing consumption of electricity in powering home electronics and electrical appliances.

The chart below displays average electric revenues (so-called average prices) for providing electric power to residential customers in the Seventh District states. Price rises since have been tame or have declined in real terms.

1. Residential electricity prices in the 7-G (average revenue per kilowatt / hour)

However, residential electric prices will soon be rising, on average, in the Midwest and nationwide. That is because fuel costs, including those for natural gas, coal, and petroleum, have been rising sharply for power generators, much as they have been rising in other end-use sectors (link). Because of lags in the passing through of fuel costs in the quasi-regulated environment, small customers in the residential sector have not yet felt the impact of fuel price rises (which typically make up two-thirds or so of delivered electricity costs for residential consumers). But the pass-through of rising fuel costs is now “in the pipeline.”

The rising prices for electric power are likely to confuse and frustrate many customers who will associate price hikes with the shifting regulatory structure of the industry, especially those who remember the mistaken path to deregulation taken by California. It will be a shame if their confusion and frustration over rising prices stalls the necessary innovations in power production that Dick Munson envisions for the Midwest in the years ahead.