The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

The Midwest economy expanded at a robust clip in 1993, with employment, consumer spending, industrial output, and housing activity showing substantial gains for the year as a whole.1 Flooding, supply interruptions in the auto industry, and some slippage in consumer and producer confidence slowed the upswing around midyear, but business activity strengthened markedly as 1993 came to a close. Harsh winter weather put a chill on growth in the region in recent months, but the underlying economic momentum remained quite positive.

This Fed Letter reviews the path of the Midwest economy during 1993 and into early 1994, documenting how that performance fits into a pattern suggesting a long-term revival in the “Rust Belt.” Over the near term, under current consensus expectations for the national economy, the Midwest economy should continue to grow at least as fast as the national economy.

Midwest labor markets among the strongest in the nation

In 1993, Midwest labor markets firmed up considerably. Hiring did slow in mid-1993, in part because of heightened uncertainty about health care reform, weather conditions, and special factors affecting the auto industry.2 A renewed burst of business activity bolstered the labor market recovery late in the year, however, with particularly strong demand for production workers. More recently, the composite picture painted by government data, private surveys, help-wanted advertising, and discussions with personnel firms and large employers indicated further labor market gains in early 1994.

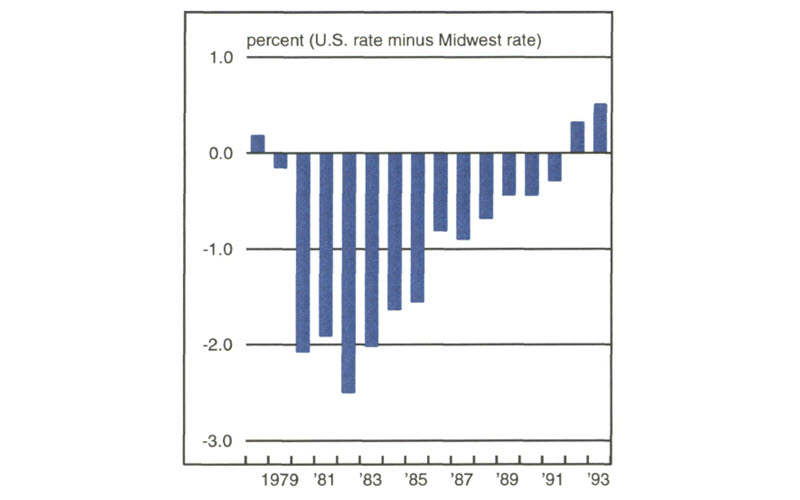

The 1993 gains fit into a developing trend that dispels the region’s Rust Belt image. The aggregate unemployment rate in the Midwest fell further than the national average in 1993 and remained below the national average for the second consecutive year.3 Prior to 1992, the last time the Midwest’s unemployment rate was below the national average was in 1978. Figure 1 shows the difference between the national and Midwest unemployment rates since 1978; the harsh impact of the recessions of the early 1980s is clearly evident. From 1979 to 1982, Midwest payroll employment fell twice as fast as the national average, and the unemployment rate rose to a level fully 2½ percentage points above the national rate. Since 1982, however, the gap between the Midwest and the nation has consistently narrowed in the Midwest’s favor. By the end of 1993, in each Midwest state, the unemployment rate had fallen below or close to its lowest level since 1977.

1. Relative unemployment rate

The gap between the Midwest unemployment rate and the national average even narrowed during 1990 and 1991, a remarkable development considering the traditional recessionary sensitivity of Midwest labor markets. Manufacturing accounts for a greater share of employment in the Midwest than in the nation as a whole, and manufacturing employment tends to suffer greater losses during a recession than overall employment. Adding to the pressure, employment in cyclically sensitive durable goods sectors constitutes a greater portion of manufacturing employment in this area than in the nation.

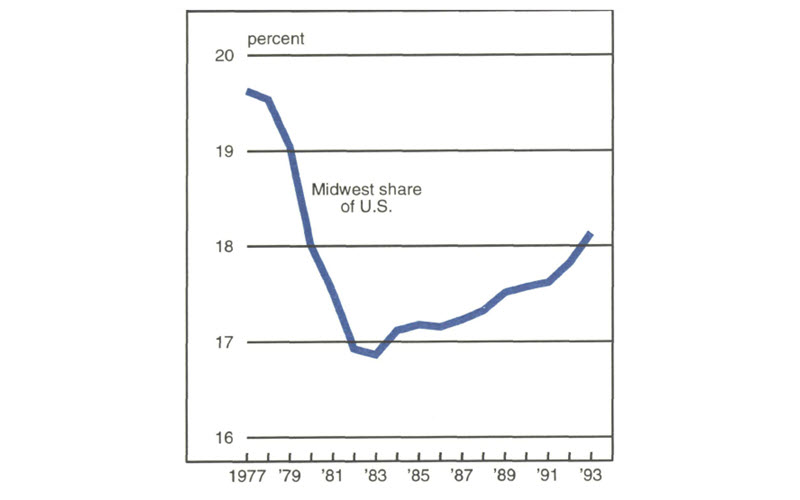

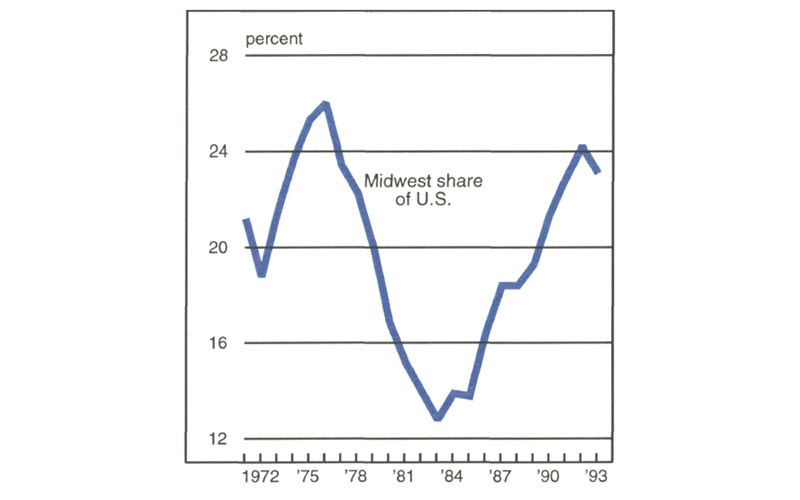

Midwest manufacturing employment fell precipitously in the twin recessions of the early 1980s, over twice as fast as the national average. Since that devastating period, however, manufacturing employment in the Midwest has accounted for an increasing share of manufacturing employment, and the region’s share continued to rise during the recessionary years of 1990 and 1991 (see figure 2).

2. Manufacturing employment

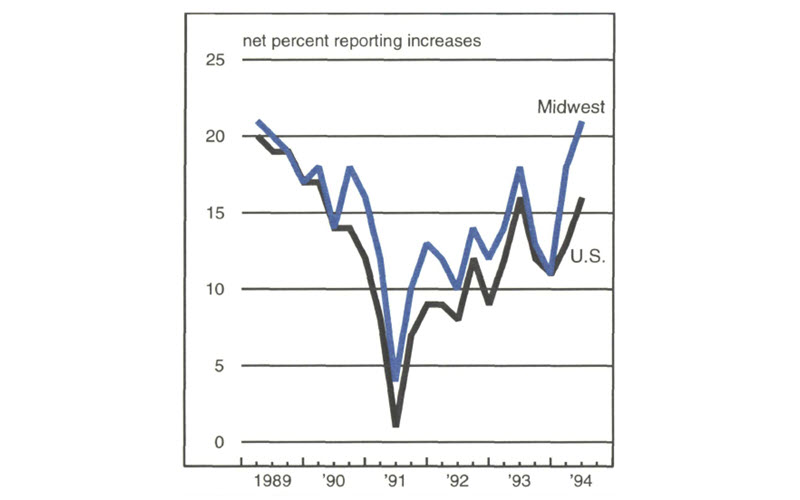

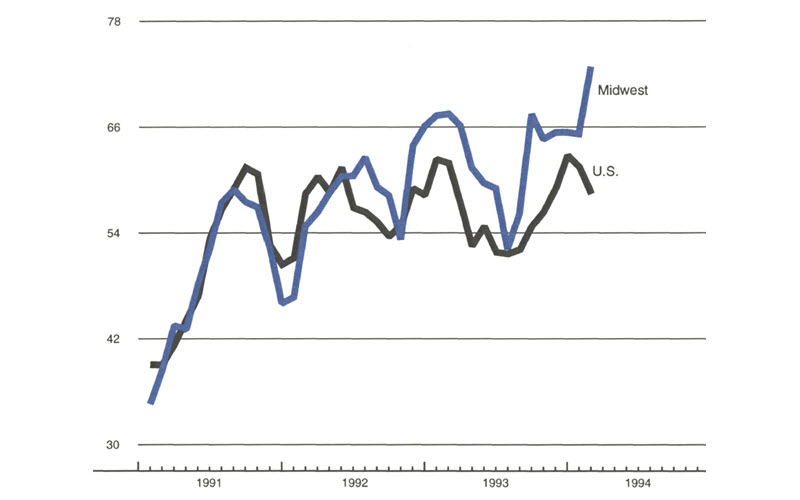

Private surveys have proven valuable alternative tools for assessing labor markets in recent years. One such effort is a quarterly survey of employer hiring plans by a large temporary help company. In 1992, this survey’s results echoed the household survey pattern more closely than it did the payroll survey data, and accurately foreshadowed the ultimate revision in the payroll data. For 1993 as a whole, this survey showed stronger hiring plans in the Midwest census region than in the nation for the fifth consecutive year. Hiring plans improved further in early 1994 (see figure 3).

3. Employer hiring plans

Nationally, the index for hiring plans among durable goods manufacturers topped the list of ten industrial categories in the most recent survey. Hiring plans in the Midwest showed considerable relative strength in early 1994, and not simply because durable goods manufacturers account for a greater share of total employers in this region. The index for Midwest durable goods manufacturers was substantially higher than its national counterpart in early 1994.

Midwest manufacturing on the move

Given the central importance of manufacturing in the Midwest, observers are fortunate to have a variety of reliable, relatively timely indicators of production trends in the region. Purchasing managers’ surveys conducted in Chicago, Detroit, Milwaukee, western Michigan, Indianapolis, and Iowa provide monthly information on trends for manufacturing as a whole. The Chicago Fed’s Midwest Manufacturing Index (MMI) estimates monthly regional output for manufacturing overall as well as for specific industrial sectors. In addition, a good deal of privately produced, publicly available information is available for important Midwest industries such as autos, heavy-duty trucks, steel, farm machinery, construction equipment, machine tools, and appliances.

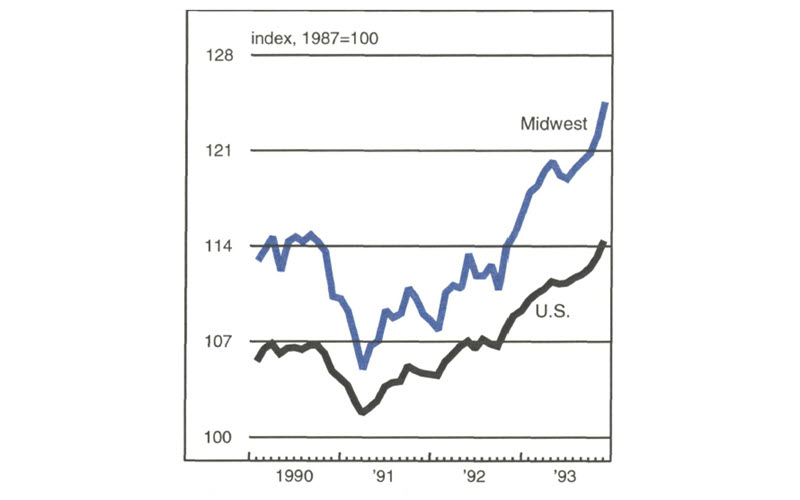

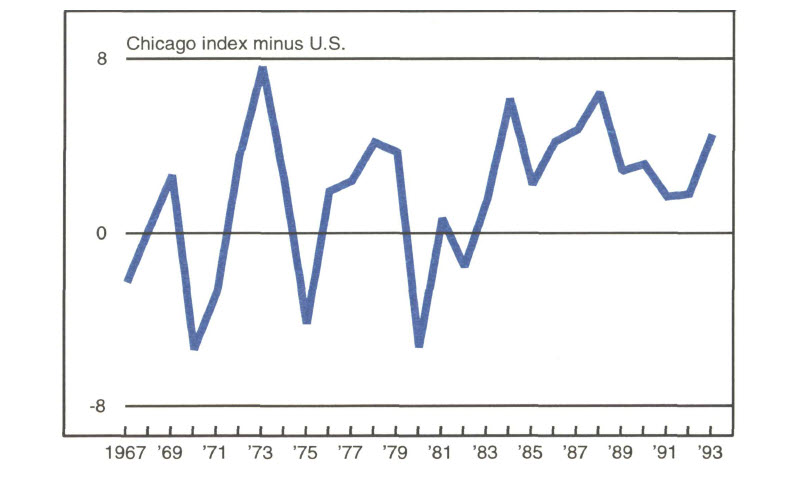

Purchasing managers’ surveys suggest that industrial output grew faster in the Midwest in 1993 than in 1992, and faster than the national average. The pattern in the MMI echoed the purchasing managers’ survey results (see figure 4), showing a midyear slowdown followed by faster growth at the end of 1993. The new-found relative strength in Midwest output during a recession can be seen in a longer-term perspective in figure 5. This chart shows the difference between the overall index for the Chicago purchasing managers’ survey and the national average. In each of the three recessions around 1970, 1973-75, and 1980-82, the Chicago index fell off sharply faster than the national average. Yet from 1983 to 1993, the Chicago index remained consistently above the national average, even in 1990 and 1991.

4. Manufacturing output

5. Purchasing managers’ surveys

The auto industry accounts for a substantial portion of the ebb and flow in the Midwest economy, because of its sizable share of regional output and the cyclically sensitive nature of demand. Increased production and distribution in the industry made a material contribution to welfare in the region last year, and auto output entered 1994 on a high note. Nationally, light-vehicle sales reached nearly 14 million units in 1993, up from 12.8 million units in 1992, and many forecasts call for similar gains in 1994. Temporary supply interruptions slowed assemblies in the third quarter of 1993, but production surged as the year came to a close, and for the year, Midwest output grew somewhat faster than the national average.

Auto sales and output should continue to benefit from factors that promoted demand improvement in 1993, including an aging auto fleet, improved affordability, higher relative used car prices, and greater consumer confidence. Indeed, in March the Big Three announced that significant hiring initiatives would be required in order to keep pace with demand. The relative position of Midwest output should be promoted by a continuing shift in market share for domestically produced cars, as well as the independent and ongoing integration of transplant assembly operations with supply networks in the region. All in all, the new year is currently shaping up very well for the auto industry, and with it, a substantial slice of Midwest economic activity.

The heavy-duty truck market is another important industry to consider when monitoring Midwest manufacturing activity, because of the location of its largest producers, the link to freight hauling, and the concentration of the supplier network in the Midwest. In 1993, the industry experienced what one supplier described as a “production and demand explosion.” North American assemblies rose 35%, and retail sales climbed 37%. Current build plans call for significant growth in assemblies in the first half of 1994. Further gains are unlikely to match those of 1993, however, if only because producers are closing in on capacity limits.

The spillover benefits of an increasingly competitive Midwest manufacturing sector can be seen in the recovery of the Midwest housing market. Housing starts rose somewhat faster in the nation as a whole than in the Midwest census region4 during 1993, partly because of new strengthening in other regions that were relatively weak in the early stages of the housing recovery. Nonetheless, starts in the Midwest rose considerably during 1993, and the longer-term trend toward faster starts in the Midwest than in the nation as a whole seemed to remain intact (see figure 6).

6. Housing starts

Looking ahead

Consensus expectations for national economic growth in 1994 have been on the rise in recent months, with continued relative strength forecast for sectors where Midwest productive capacity is concentrated and increasingly competitive. Midwest economic prospects seem the brightest in over a decade.

How long can the good times last? It should be noted that lower oil prices, the declining exchange rate of the dollar, and declining long-term interest rates enhanced the relative performance of the Midwest economy in recent years. A substantial share of the region’s industrial output consumes oil and its derivatives, and the relative price of regional output is more importantly determined by transportation costs (and oil prices) than the national average. The declining dollar helped boost exports in recent years, and export output provides a higher share of income in the region than in the nation as a whole. Declining long-term interest rates helped boost demand for durable goods in recent years and, in turn, lifted the relative position of the Midwest economy. Predicting the future path of these three factors is a tall order, and in any case, they lie beyond the immediate control of most Midwesterners.

At the same time, improved productivity in the region certainly accounts for much of the brightness in the overall outlook. The Midwest’s manufacturing base suffered greatly during the recessions of the early 1980s. Many of the surviving firms responded by undertaking a variety of productivity initiatives, including more efficient production and inventory management, more closely focused capital spending, organizational restructuring, and the development of more efficient transportation and distribution systems. If private and public policymakers continue to work to identify and improve upon those efforts that promoted the relative position of the Midwest economy in recent years, they can maximize the long-run potential of the regional economy and enhance its performance in good times and bad.

Tracking Midwest manufacturing activity

Manufacturing output index (1987=100)

| January | Month ago | Year ago | |

|---|---|---|---|

| MMI | 129.1 | 127.5 | 117.4 |

| IP | 115.4 | 115.2 | 109.9 |

Motor vehicle production (millions, saar)

| January | Month ago | Year ago | |

|---|---|---|---|

| Cars | 7.0 | 6.8 | 6.3 |

| Light trucks | 5.4 | 5.8 | 4.8 |

Purchasing Managers’ Surveys: production index

| February | Month ago | Year ago | |

|---|---|---|---|

| MW | 72.9 | 65.3 | 67.6 |

| U.S. | 58.5 | 61.5 | 62.4 |

Purchasing Managers' Surveys (production index)

Midwest manufacturing activity expanded at a robust pace in recent months, with the auto industry playing a key role. After rising significantly in the fourth quarter, the composite production index for purchasing managers’ surveys in Chicago, Detroit, and Milwaukee changed little in January, despite the unusually severe weather. The index suggested that output growth then rose substantially in February, led by responses in the Detroit survey. The Midwest composite index has now been above the national average for 16 consecutive months. Domestic light-vehicle production galloped ahead in early 1994, and total assemblies ran at their highest level since the late 1970s.

Notes

1 Unless otherwise specified, Midwest refers to Illinois, Indiana, Iowa, Wisconsin, and Michigan.

2 See “Midwest update,” Midwest Economic Report, third quarter 1993; ‘The Great Flood of 1993,” Midwest Economic Report, fourth quarter 1993; and “Assessing the Midwest flood,” Chicago Fed Letter, No. 76, December 1993, all by Federal Reserve Bank of Chicago.

3 Unemployment rates are derived from data prior to a 1994 change in household survey methodology.

4 Besides the states listed in note 1, the Midwest census region also includes Ohio, Minnesota, Missouri, Kansas, Nebraska, South Dakota, and North Dakota.