The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Confidence is the bulwark of capitalism, as it is of democracy.

—William O. Douglas

A sense of caution framed consumer and business decisions during 1991, culminating in a year-end slump in confidence that helped to smother the recovery. In a cloudy forecasting environment, 38 economists and business analysts participated in the Federal Reserve Bank of Chicago’s fifth annual Economic Outlook Symposium on December 11, 1991. This Chicago Fed Letter summarizes the discussions that took place at that meeting and focuses on conditions in durable goods manufacturing industries important to the Midwest economy. Manufacturing activity helped lead the recovery that began early in 1991 but was also instrumental in the economy’s stalling toward the end of the year. Still, all the forecasts prepared for the symposium expected the economy to avoid declining from 1991 to 1992, with housing starts, car sales, and investment spending each expected to record gains. If so, manufacturing activity linked to spending in these sectors should post improved results in the new year.

1991: what happened to the recovery?

The consensus forecast produced a year ago was prepared in an uncertain atmosphere, with escalating oil prices and consumer confidence shaken by the war in the Persian Gulf. In light of the heightened level of uncertainty, that forecast performed relatively well in describing the economy’s performance in 1991. The economy began to turn upward toward the end of the first half of the year, albeit somewhat slower and later than the consensus forecast had anticipated. But the recovery’s momentum began to unravel in the fourth quarter—a period when last year’s forecast predicted continued improvement in growth. It is now evident that real GNP (in 1982 dollars) declined slightly in 1991, in contrast to last year’s forecast of an increase of 0.4%. Why did the recovery stall?

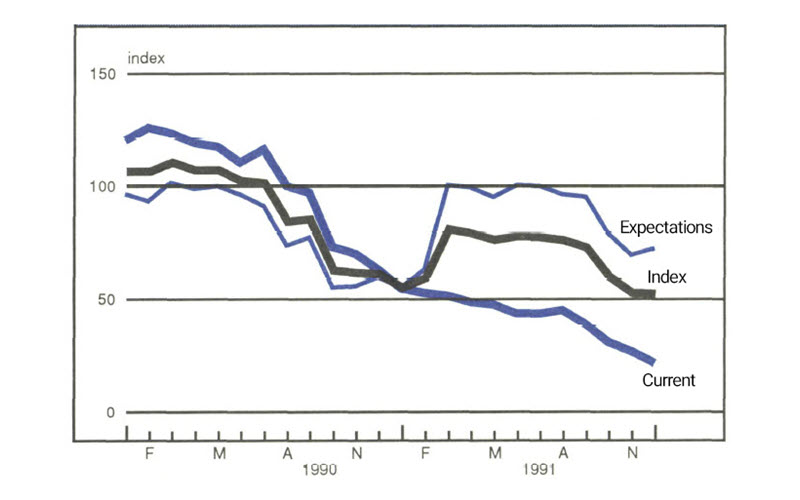

Trends in consumer and business confidence lie near the heart of the problem. A business conditions research firm called the Conference Board conducts a monthly household survey and publishes a diffusion index that measures consumer confidence. The overall index has two major components: appraisals of current conditions, and expectations for conditions six months into the future. When the war in the Persian Gulf ended, the overall index rose dramatically. Interestingly, the improvement was concentrated in expectations, while appraisals of current conditions continued to sink (see figure 1).

1. Consumer confidence

Beginning in the second quarter of 1991, the complex network of manufacturers, wholesalers, retailers, and other businesses supporting the production and distribution of consumer durable goods joined consumers in anticipating a turnaround. Gains in production and distribution activity helped stem the slide in employment and boosted personal income in several durable goods sectors that had suffered during the downturn. Unfortunately, as the year progressed, a sense of caution remained pervasive and prompted the postponement of many consumption and investment decisions. Before committing their present and future resources, consumers and investors waited for solid evidence of a strong recovery. In turn, when consumers and investors delayed their spending, a strong recovery did not occur. Job creation over the second and third quarters was anemic by historical recovery standards, reflecting in part the lack of a commitment to the future on the part of many businesses. In turn, consumers’ appraisals of the recovery remained reserved, as employed people focused on friends and family members who had lost their jobs. Concern with structural problems in the economy, such as the effects of federal, state, and local government fiscal stress, also impacted confidence and spending.

By late 1991, the failure of consumption spending to meet producers’ expectations put a damper on manufacturing activity. Inventory building by durable goods retailers in the third quarter was followed by softening in the production of durable consumer goods in the fourth, which could indicate that much of the inventory building was involuntary. Weakening was particularly evident in the production of autos. Car assembly schedules were pared considerably during the final quarter of the year. In early August, planned assemblies for the second half of 1991 were just 0.5% below the same period in 1990, but actual production in the second half was nearly 7% below year-earlier levels.

The slow improvement in the overall labor market came to a halt late in the year. In November, most of the recovery’s employment gains were erased by a 241,000 decline in payrolls. As the economy failed to improve to meet expectations formed earlier in 1991, confidence slumped again in the fourth quarter, with new deterioration in expectations joining the continuing decline in appraisals of current conditions.

The consensus outlook for 1992

In the face of a weakening recovery, the median forecast produced at the December 1991 symposium still called for modest but improving real GNP growth throughout 1992 (see figure 2). Some economic reports issued in the weeks after the forecasts were prepared were unexpectedly weak, however. This led several economists to attach notes of caution to their forecasts during their presentations. The forecasts were prepared just before the comprehensive revision to national income accounting, adding some additional uncertainty to the forecasting atmosphere. Based on GNP in 1982 dollars, the growth estimates should not be viewed as precise forecasts, but as rough indicators of future patterns.1

2. Symposium’s median forecasts

| 1991 | 1992 | |

|---|---|---|

| (Year-to-year % change) | ||

| Real GNP (1982 dollars) | –0.5 | 2.1 |

| Personal consumption expenditures | 0.3 | 2.2 |

| Business fixed investment | –2.8 | 3.0 |

| Residential investment | –11.6 | 8.6 |

| Government spending | –0.5 | –1.6 |

The estimates for real GNP growth in 1992 fell in a range of slow but positive growth rates (from 1.3% to 3.3%), with personal consumption expenditures, residential investment, and inventory accumulation each expected to provide positive contributions to growth throughout the year. Consumer spending growth was expected to be modest but consistent. Forecasts of business fixed investment and residential investment were more widely distributed than those for consumer spending, but nearly all of the forecasts called for positive growth in 1992. The median growth forecasted for these two forms of investment spending was the highest of the major GNP components, and the median forecast for business fixed investment called for growth to increase as the year progressed.

What industries might benefit in 1992?

Despite the continuing slump in consumer and business confidence, several sectors that are sensitive to changes in sentiment were forecast to provide sources of strength this year, including autos, housing, and business fixed investment. Importantly, spending in these areas is also sensitive to changes in interest rates. Not one forecaster expected higher long-term interest rates in 1992.

In spite of all the bad news coming from the auto industry, new car sales were still expected to rise in 1992, providing perhaps the most important contribution to the predicted recovery. One motor vehicle industry analyst noted that the consumer has been exposed to a series of bad news stories: little change in employment in the last six months, numerous announcements of layoffs by Fortune 500 companies, rising taxes at state and local levels, and little improvement in real disposable income per household.

“The consumer’s ability to spend looks weak,” this speaker stated, “while his willingness to spend looks terrible.” Automotive sales have also faced structural obstacles, particularly as the industry unwinds the effects of the extension of car loan maturities in the mid-to-late 1980s. In addition, domestic automakers’ quality improvements helped lead to longer car holding periods, contributing to near-term sales weakness. Still, this analyst expected an upturn by the second half of 1992, citing the positive effects of lower interest rates on national income. The symposium’s median forecast called for car sales to rise from an estimated 8.4 million units in 1991 to 9.1 million units in 1992, but this pace is still lower than the 9.5 million units sold in 1990.

Production at machining shops is closely linked to demand for autos and other consumer durable goods. Activity in this metal processing industry generally continued to soften over the latter half of 1991, according to an industry survey presented at the symposium, although production levels still remain above those in the early 1980s. A national association of machining firms has forecast a significant improvement in sales to the motor vehicle industry next year, while gains in housing starts were expected to translate into higher orders from manufacturers of household appliances. Housing starts were expected to improve by every forecaster at the symposium, with growth estimates ranging from 9% to 30%. If these expectations are realized, Midwest machining shops linked to appliance and furniture production could join auto suppliers in recovering after a difficult year.

The machine tool was described by a manufacturer’s association representative as “the mother tool, the only machine that can replicate itself.” Sales of this product have long been viewed as a key indicator of trends in investment spending. Orders received by domestic builders of machine tools held up relatively well through the end of 1990. However, as 1991 progressed, low production levels at machining shops and underutilized capacity at more integrated manufacturing firms triggered cutbacks in orders to manufacturers of “the mother tool.” Through October 1991, shipments were 20% below the same period in 1990. It should be noted, however, that several industry participants performed relatively well during the year, with one noting that machine tool purchases have become linked more closely to productivity improvement than to capacity considerations, a development that has helped to mute cyclical swings in spending. A consensus forecast of industry analysts presented at the December meeting called for net new orders received by domestic manufacturers to increase nearly 20% in 1992. Export business provided a bright spot for U.S. machine tool manufacturers during 1991, and the industry may benefit this year from the late December 1991 extension of import quotas. Expansion of durable goods production capacity in Mexico was cited as one key source of future strength, as that country does not have a significant machine tool industry.

Domestic production of most types of capital equipment softened in the final quarter of 1991, but significant improvement in investment spending is still planned for 1992, according to the most recent quarterly survey of investment intentions by the Commerce Department (conducted early in the fourth quarter of 1991). In the survey, real spending for 1991 was projected to decline 1.1%, after an increase of 3.3% in 1990. The anticipated decline for 1991 is small compared with the sharp 4.1% drop registered in 1986, however, and plans for 1992 called for a gain of nearly 6%. Above-average growth in investment was planned by producers of motor vehicles and electrical machinery, although two other important industries in the Midwest that face overcapacity—primary metals and paper—anticipated relatively sharp declines in investment spending.

Low levels of capacity utilization have constrained capital goods investment in another industry important to Midwest manufacturing activity. A producer of medium- and heavy-duty trucks noted that many motor carriers continue to operate with fewer trucks than they own or are able to lease, holding down orders for new trucks and truck engines. Motor carrier freight levels rose with the anticipatory surge in industrial activity that took place in the middle of 1991, but not sufficiently to warrant additions to fleet capacity. Sales of both medium- and heavy-duty trucks fell roughly 20% (in units) in 1991 and remained well below replacement volume. Government purchases account for as much as one-quarter of medium-duty vehicle sales, and state and local fiscal conditions have adversely affected sales of school buses. In the third quarter of 1991, shipments of new school buses fell to their lowest level in three decades. Orders of medium-duty trucks have shown signs of leveling out recently. One manufacturer anticipated that sales would increase roughly 4% (in units) in 1992, with most of the growth coming in the latter half of the year. Heavy-duty truck sales were expected to improve at a slightly faster pace than sales of medium-duty vehicles.

The demand for construction equipment was influenced by developments in the commercial real estate market during 1991, and the outlook for 1992 appears little changed for equipment manufacturers. Retail sales of construction equipment languished last year, leading to sharp cutbacks in production among Midwest manufacturers. In several cases, the soft market prompted equipment manufacturers to reduce production capacity permanently. In addition to the oversupply of buildings, a speaker noted that the outlook for nonresidential construction activity has also been weakened by the fiscal status of state and local governments. This forecaster expected housing starts to continue to recover slowly this year, which could help to support the demand for some types of construction equipment. The recent federal legislation providing new taxpayer funding for transportation construction is also expected to provide some support for the industry.

On the agricultural equipment side of the off-highway vehicle sector, sales generally held up better than construction equipment through most of 1991, although unit sales of combines softened considerably toward the end of the year. Farm income growth remained sluggish during 1991, as the gradual reduction in subsidies combined with softening prices to curb farm revenues. In 1992, one forecaster expected higher acreage plantings and stable land values to lend some support to equipment demand, but retail sales of tractors and combines were still anticipated to show small declines from 1991 levels.

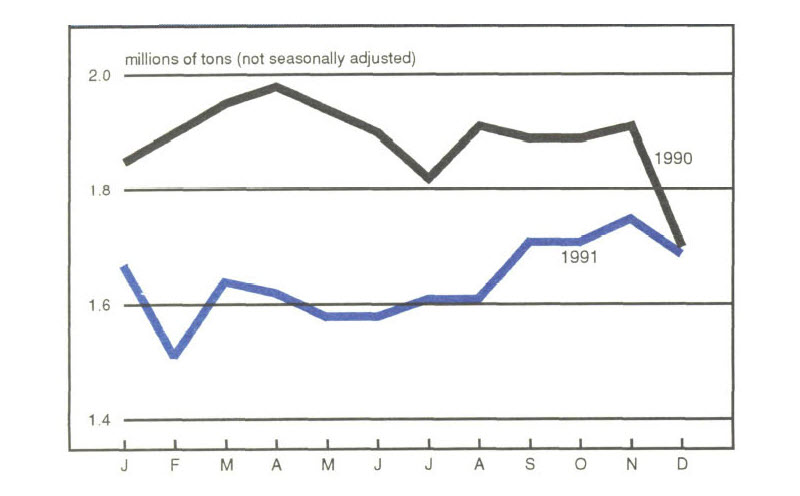

Durable goods spending inevitably translates into demand for steel and other basic materials. A steel industry forecaster expected domestic steel shipments of 78.5 million tons in 1991, and 82 million tons in 1992. The year-over-year gain does not suggest strong improvement, however, as the 1992 pace is flat compared to the second half of 1991. This forecaster noted that trends in steel are a good indicator to watch when gauging the strength of investment, in part because basic materials procurement leads total investment spending. This producer noted a steady increase in orders and shipments as 1991 progressed after a particularly difficult first quarter, and domestic steel production showed gradual improvement (see figure 3). The upturn came first in demand for light products designed for autos and appliances. Orders for heavy products such as electrical machinery, which are more closely tied to investment spending, turned upward later in the year. Demand for steel used in heavy products was expected to stand a better chance of improvement in 1992 than demand for light products, as the outlook for consumer spending remained restrained, and the prospect for investment spending by corporate customers was enhanced by financing activity late in 1991. Industries expected to contribute to relative strength in sales of products earmarked for business investment included food processing and chemicals. Still, this analyst presented his forecast with a high degree of caution.

3. Domestic steel production

Lower interest rates and the outlook for recovery

If the future unfolds as the forecasts expect, industrial activity linked to housing, the auto industry, and durable goods spending could again help lead the national and Midwest economies onto a path of moderate, sustainable growth. Predicting the future of an economy sensitive to shifts in confidence is a difficult task, however. Indeed, the weakening in the recovery in the fourth quarter of 1991 was unexpected by most present at the symposium and could also indicate that structural obstacles to growth are stronger than previously thought. Developments since the December symposium suggest that the forecasted levels of growth could be over-optimistic, but the pattern of growth (with most of the gains concentrated in the latter half of 1992) currently appears to be the most likely outcome.

Since the December 1991 meeting, interest rates have continued to decline. For instance, the discount rate dropped to 3.5% on December 20, reaching its lowest level in 27 years. It is also noteworthy that no forecaster at the December meeting predicted that long-term interest rates would be higher in 1992 than in 1991. Lower interest rates should have at least two stimulative effects: They reduce the cost of goods purchased on credit, and they can relieve consumer and business debt burdens through refinancing activity. Lower rates should also provide an important indirect benefit: By reducing the cost of acquiring and holding assets that require financing over an uncertain future, lower rates can help support economic activity in the presence of weakened confidence and prompt the initial risk-taking required to help rebuild more generalized confidence in future economic growth.

Note

1 Among the revisions, Gross Domestic Product replaced GNP, and the base year for prices was updated to 1987. For a brief overview, see Robert P. Parker, “A preview of the comprehensive revision of the National Income and Product Accounts,” Survey of Current Business, October 1991, pp. 20-28.