The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Some of the biggest news in the U.S. financial press over the past few years has been the wave of “megamergers” among the nation’s largest commercial banks. Bank of America merged with NationsBank to become the first truly nationwide bank in the U.S. Bank One merged with First Chicago, which had only recently merged with NBD. CitiCorp merged with Travelers, combining the second largest U.S. bank with one of the world’s major insurance firms. Wells Fargo merged with Norwest, Chemical Bank combined with Chase Manhattan; the list goes on and on.

Megamergers (mergers between two banks each with more than $1 billion in assets) have grabbed the headlines, but they account for only a small portion of the merger and acquisition (M&A) activity in the banking industry in recent years. M&As have reduced the number of commercial banks in the U.S. by between 4% and 6% in every year since the mid-1980s, and most of the banks that have disappeared were small. For example, in 75% of the over 6,000 mergers of unrelated commercial banks between 1980 and 1994, the target bank held less than $100 million in assets.

Although this historic merger wave is not over, it has recently shown signs of maturing. At least one large and very acquisitive U.S. bank has announced that mergers have become an outdated growth strategy.1 In this Chicago Fed Letter, I review the reasons for bank mergers, how they have changed the structure of the banking industry, and the effect of mergers on competition in retail banking and small business banking. In a subsequent Fed Letter, I will analyze the prospects for small banks in a post-merger wave banking industry.

Local market structure

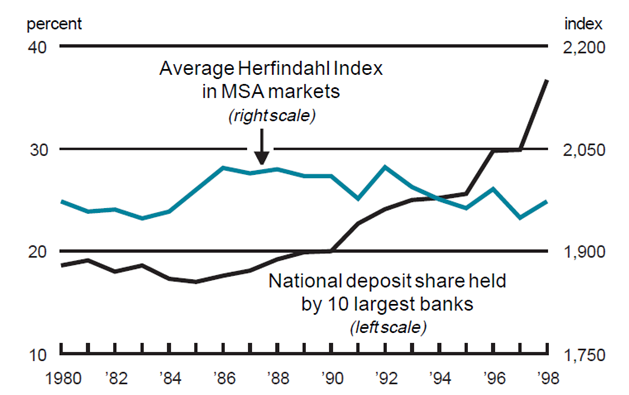

Whenever two large businesses combine, the initial public policy concern is whether or not the merger will reduce competition. If market share is an indicator of market power, then on the surface the recent bank megamergers appear to have worsened an already troubling banking industry trend. As seen in figure 1, between 1980 and 1998 the share of domestic deposits held by the nation’s ten largest commercial banks nearly doubled, from about 19% to 37%.

1. National and local market structure

Source: Board of Governors of the Federal Reserve System.

But the national market shares of the largest banks remain low compared to those of top firms in many other U.S. industries (e.g., airlines, automobiles, and brewing). And at least for the time being, the relevant market for many of the retail and small business products offered by banks is local, not national. Figure 1 also shows the average level of the Hirschman-Herfindahl Index (HHI) between 1980 and 1998 for commercial banks in metropolitan statistical areas (MSAs). The HHI is a standard indicator of market structure used by antitrust authorities. This index equals 10,000 for a monopoly market and takes on lower values as more banks enter the market. Contrary to the increasing trend in nationwide market shares, the HHI shows no pattern of decreased competition in MSAs, where most of the merger activity has occurred. Judging from this measure, the number and size of banking competitors in local markets has not been materially affected by the bank merger wave.

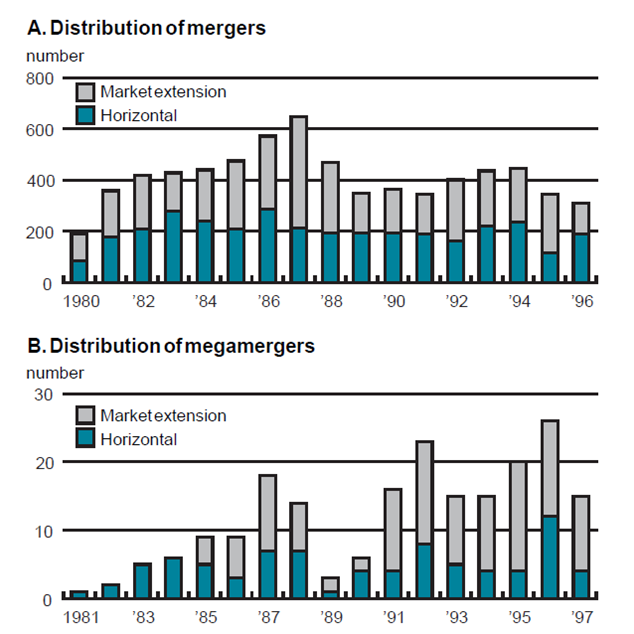

There are a number of explanations for the discrepancy between nationwide and local banking market structure. First, as shown in figure 2, over the past two decades about half of all bank mergers, and about two-thirds of all megamergers, were market extension mergers that combined banks that operated in different geographic markets. Thus, for every horizontal megamerger like Chase Manhattan–Chemical Bank that combined banks operating primarily in the same market, there were two megamergers like Wells Fargo–Norwest that extended the geographic reach of one bank by pairing it with a bank from a different state or region. Large market extension mergers increase the nationwide concentration of deposits, but at the local level they merely change the ownership of the acquired bank without reducing the number of banks competing in either of the two local markets.

2. Distribution of mergers and megamergers

Second, in many cases bank regulators will not approve a horizontal merger unless the merging banks agree to sell some of their branches or deposit accounts. For example, regulators approved the merger that created the new Bank One only after numerous branches in MSA markets in Indiana were sold off to smaller banks. Divestitures of branches reduce the impact of horizontal mergers on market competition by dampening or eliminating any increase in local HHI.

Third, since 1980 federal and state banking authorities have chartered over 3,000 new commercial banks. Although these de novo banks start out relatively small and can be financially fragile, over time they can become an important competitive alternative in local markets. Recent research finds that new banks tend to focus on small business lending, and that they are attracted to local markets that have recently experienced mergers.2

Retail prices & customer convenience

Surveys conducted by Federal Reserve staff suggest that retail banking fees have been relatively stable over the past three years.3 However, when fees did change they were more likely to increase than decrease. The most frequent increases were fees for ATM transactions and special fees for items such as returned checks, insufficient funds, or account overdrafts. Furthermore, the surveys find that large multistate banks charge higher fees for retail banking services than small single-state banks.

Does the fact that larger banks charge higher fees constitute prima facie evidence that bank mergers have reduced competition? As with the national market share statistics, what on the surface appears to be evidence of growing market power becomes less clear upon further consideration. If the merger wave increased market power, why wouldn’t fees have increased across the board, for all products and at all banks? Given the large number of small banks to which customers could switch and avoid these fee increases, there should be a plausible explanation for these localized fee increases other than market power.

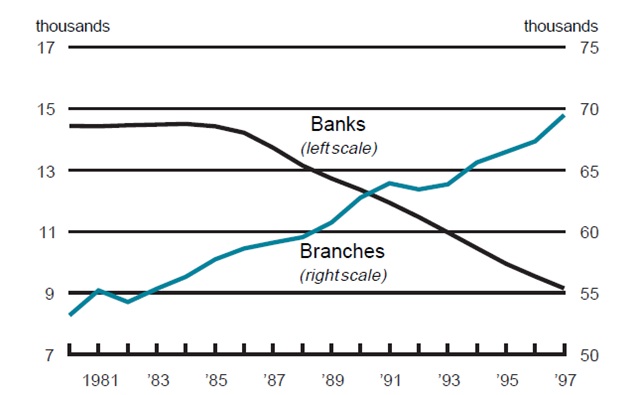

Higher fees may reflect the willingness of some customers to pay more for higher quality service and greater convenience. Figure 3 shows that the number of banks in the U.S. has decreased by about 40% since the mid-1980s, but at the same time the number of banking locations has increased by over 25%. This increase in branch locations, considered together with the explosion in ATM locations (from fewer than 10,000 in 1980 to over 200,000 today), suggests that retail banking convenience increased significantly during the bank merger wave. If different depositors prefer different service characteristics, then the difference in fees between big banks and small banks could be a sign of a clientele effect and not a sign of reduced competition. Depositors who value convenience might be opting for large, high-fee banks that offer far-flung ATM and branch networks, while depositors who do not value convenience highly may be opting for local banks that charge lower fees. By adopting a fee structure that covers the costs of producing its own mix of financial services, a bank can profitably serve its target clientele, and shed clients better served by banks that offer different mixes of services and charge different combinations of fees.

3. Banks and bank branches in the U.S.

Credit availability for small business

The typical small business is not well-known or large enough to issue securities in the capital markets or credit markets. Local commercial banks have traditionally been well-situated to gather the financial, business, and personal information necessary to make informed credit decisions about these firms.

Small businesses worry that their credit supply will be interrupted when the small, local bank they have been borrowing from is acquired by a large, out-of-state bank. The loan officer that services a small business account might lose her job during post-merger cost-cutting, or the bank’s small business lending culture might change after it is acquired. Similarly, local communities worry that large out-of-state banks will siphon off local deposits and invest them elsewhere. In large banking companies, branch managers may have little stake in the local community, because their career paths lead to higher-paying jobs at branches in larger towns.

Recent research indicates that, on balance, the bank merger wave has not reduced the amount of credit available to small businesses. Not surprisingly, this research finds that mergers among small banks do not reduce lending to small businesses. The more interesting finding is that acquisitions of small banks by large banks can reduce small business loans (especially if the acquiring bank did not make many small business loans prior to the merger), but that these merger-induced reductions in small business loans tend to be offset by increased lending by other banks operating in the local market.4

Why are banks merging?

The most frequently cited motivation for bank mergers is that they improve performance by cutting costs and/or capturing economies of large scale. Recent models of bank production functions show that even very large banks can benefit from scale economies.5 However, merging the operations and corporate cultures of two large banks can be difficult and, if not done skillfully, can actually stifle performance by alienating depositors and causing them to change banks. Studies generally find that only a little over half of all bank mergers reduce costs. But these same studies find that banks experienced at making acquisitions are more successful at cutting costs than infrequent purchasers; that market extension mergers tend to reduce the volatility of bank earnings; and that bank revenues tend to increase after a merger because the loans and other assets of the acquired banks get invested more effectively.6

Self-interested behavior by bank managers also helps explain why banks merge. The labor market tends to set the salaries of corporate managers in proportion to the size of the firm they manage. This provides bank managers with a clear incentive to make the bank larger, which can be accomplished most quickly by making acquisitions.7

A quest for market power is a third potential explanation for bank mergers. Indeed, studies have shown that banks in highly concentrated markets are able to charge higher loan rates and offer lower deposit rates.8 But as we saw in figure 1, local market concentration did not increase during the bank merger wave, which suggests that the merger wave has not increased market power for banks.

Conclusion

Over the past two decades, an accelerating wave of mergers has drastically altered the landscape of U.S. commercial banking. Despite fears that this rapid industry consolidation would result in market power, reduced access to credit for small business, and higher prices for retail financial services, very little of this has come to pass. Concentration in local banking markets has not increased. Small business lending has not diminished. And while fees for some retail banking services have increased, these increases have been limited to certain services offered by large banks and seem better explained by interbank differences in service quality and consumer preferences than by market power.

But this may be an optimistic diagnosis, because it is based in large part on the assumption that banks compete with each other for retail and small business accounts in local geographic markets (e.g., within an MSA). Information technology is rapidly changing the way that banks deliver their products to customers, and as this happens an increased number of retail banking products will be sold on a national market. This may have serious competitive implications because, as we saw in figure 1, the concentration of large banks in the national market is increasing. I will address this issue in a subsequent Chicago Fed Letter.

Tracking Midwest manufacturing activity

Manufacturing output indexes (1992=100)

| June | Month ago | Year ago | |

|---|---|---|---|

| CFMMI | 131.9 | 130.4 | 127.2 |

| IP | 138.6 | 138.4 | 133.7 |

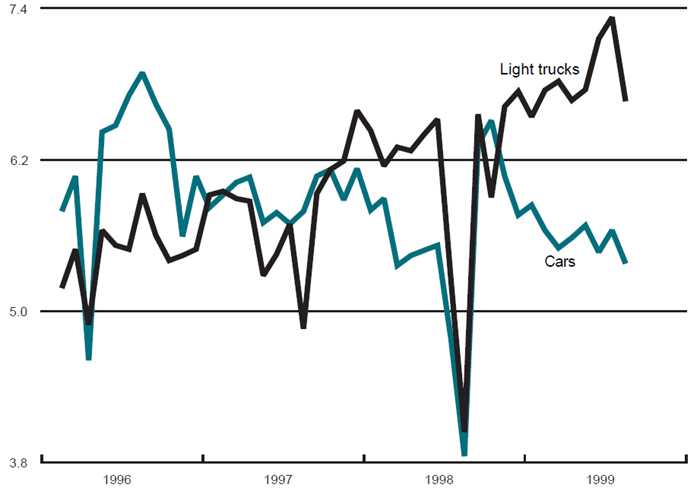

Motor vehicle production (millions, seasonally adj. annual rate)

| July | Month ago | Year ago | |

|---|---|---|---|

| Cars | 5.4 | 5.6 | 3.9 |

| Light trucks | 6.7 | 7.3 | 4.0 |

Purchasing managers' surveys: net % reporting production growth

| July | Month ago | Year ago | |

|---|---|---|---|

| MW | 62.2 | 65.0 | 51.1 |

| U.S. | 58.2 | 63.0 | 49.2 |

Motor vehicle production (millions, seasonally adj. annual rate)

Light truck production decreased from 7.3 million units in June to 6.7 million units in July, and car production also decreased from 5.6 million units in June to 5.4 million units for July. The Chicago Fed Midwest Manufacturing Index (CFMMI) rose by a very strong 1.2% from May to June, to a new record seasonally adjusted level of 131.9; revised data show the index fell 0.3% in May. The Federal Reserve Board’s industrial production index for manufacturing (IP) increased 0.1% in June, after rising 0.3% in May.

The Midwest purchasing managers’ composite index for production decreased to 62.2% in July from 65% in June. The purchasing managers’ indexes increased for Chicago but decreased for both Detroit and Milwaukee. The national purchasing managers’ survey for production also decreased from 63% in June to 58.2% in July.

Notes

1 In May 1999, Bank One Chairman John McCoy stated that his bank may have made its last bank acquisition, because it can now grow through electronic distribution channels. See John McCoy, 1999, “The changing landscape of the banking industry,” Proceedings of the 35th Annual Conference on Bank Structure and Competition, Federal Reserve Bank of Chicago, forthcoming.

2 For additional discussion, see Robert DeYoung, 1999, “The birth, growth, and life or death of newly chartered banks,” Federal Reserve Bank of Chicago, Economic Perspectives, Volume 23, Third Quarter, pp. 18–35.

3 Board of Governors of the Federal Reserve System, 1997, 1998, and 1999, Annual Report to Congress on Retail Fees and Services of Depositories, June.

4 See Allen N. Berger, Anthony Saunders, Joseph M. Scalise, and Gregory F. Udell, 1998, “The effects of bank mergers and acquisitions on small business lending,” Journal of Financial Economics, Vol. 50, pp. 187–229.

5 See Allen N. Berger and Loretta J. Mester, 1997, “Inside the black box: What explains differences in the efficiency of financial institutions?” Journal of Banking and Finance, Vol. 21, pp. 895–947.

6 See Robert DeYoung, 1997, “Bank mergers, X-efficiency, and the market for corporate control,” Managerial Finance, Vol. 23, pp. 32–47; Joseph P. Hughes, William Lang, Loretta J. Mester, and Choon-Geol Moon, 1999, “The dollars and sense of bank consolidation,” Journal of Banking and Finance, Vol. 23; and Jalal D. Akhavein, Allen N. Berger, and David B. Humphrey, 1997, “The effects of megamergers on efficiency and prices: Evidence from a bank profit function,” Review of Industrial Organization, Vol. 12, pp. 95–139.

7 See Richard T. Bliss and Richard J. Rosen, 1999, “CEO compensation and bank mergers,” Proceedings of the 35th Annual Conference on Bank Structure and Competition, Federal Reserve Bank of Chicago, forthcoming.

8 See Allen N. Berger and Timothy Hannan, 1989, “The price–concentration relationship in banking,” Review of Economics and Statistics, Vol. 71, pp. 291–299; and Allen N. Berger and Timothy Hannan, 1997, “Using efficiency measures to distinguish among alternative explanations of the structure-performance relationship in banking,” Managerial Finance, Vol. 23, pp. 6–31.