The following publication has been lightly reedited for spelling, grammar, and style to provide better searchability and an improved reading experience. No substantive changes impacting the data, analysis, or conclusions have been made. A PDF of the originally published version is available here.

Why are U.S. natural gas prices currently at the high end? What are the implications of recent regulatory changes and changes in market fundamentals? This article explains the boom-and-bust nature of natural gas prices and some ways to reduce this volatility going forward.

Current natural gas prices in the U.S. are high—more than double their historical trend over the last five years—and futures prices indicate that natural gas supplies are likely to continue to be tight for at least the near term. High and volatile fuel prices are the consequence of both changing market fundamentals and regulatory decisions. Accordingly, the interplay of these effects could have substantial consequences, both nationwide and in the Midwest.1 This Chicago Fed Letter describes conditions that have put pressure on gas prices and suggests some potential strategies that might mitigate gas price volatility in the future.

Domestic market

Natural gas markets have been deregulated for the most part since the late 1970s, when the Federal Energy Regulatory Commission first allowed competitors to enter the natural gas pipeline industry. This deregulation movement broke the vertically integrated structure of the natural gas industry, which had arisen from federal interstate regulation dating back to early in the twentieth century. Deregulation opened up previously unrealized value creation opportunities that benefited most consumers and some producers. As a result, by the 1990s natural gas was widely available at very low prices, so low, in fact, that some producers went out of business or confined their extraction to existing deposits. Low prices reduce exploration, and high prices encourage it, resulting in a boom-and-bust cycle, which has historically been a feature of the industry.

Another development that has followed deregulation in the natural gas industry has been the creation of liquid, sophisticated financial markets for natural gas. The development of a wide range of financial instruments has enabled risk spreading in natural gas markets. The resulting ability to hedge risk across time and across different market conditions has substantially decreased the volatility in natural gas prices associated with the boom-and-bust cycle that characterizes extractive industries like natural gas.

So, why the recent spike in natural gas prices? The price increase has been fairly sudden but not unpredictable. In fact, natural gas prices have been edging up since the late 1990s. Still, while the current and expected price increases are the consequence of the interaction of demand, supply, and other forces that shape the market, supply issues seem to be a particularly important factor.

Many analysts and energy industry experts have, correctly, pointed to regulatory restrictions as the prime cause of the rigidity of natural gas supply. In particular they argue that limitations on drilling on federal lands, in consideration of the environmental amenities attached to those lands, have greatly limited exploration options. Approximately 40% of known natural gas reserves in the U.S. are off limits to exploration and production.

Another potentially abundant source of supply is imported liquefied natural gas (LNG) from such places as the Middle East, Russia, China, West Africa, and the countries around the Caspian Sea. However, the industry still has some work to do to convince the U.S. public that long-distance transportation of LNG is safe. And, even if the industry succeeds in this effort, it then has to build the necessary infrastructure to facilitate LNG imports onshore. LNG off-loading and storage at port requires specific technology in the terminals. Few such terminals exist in North America, and they take a long time to build. Construction of new LNG terminals can take up to a decade, taking into account siting and environmental regulatory processes. Accordingly, LNG terminal construction and imported supply is a long-term, though important, response to the current market imbalance.

Constrained supply is not the only cause of high natural gas prices. Environmental regulation of U.S. air pollutants was predicated on the assumption of abundant natural gas as a substitute fuel. Specifically, natural gas is a clean (and formerly cheap) fuel for electricity generation, particularly relative to bituminous coal. Improvements to existing power plants that have occurred in the past 30 years have overwhelmingly used natural gas to comply with the new source review regulations introduced in the early 1970s. And air quality regulations have led to a situation in which the only economical way to build new power plants is to fuel the facilities with natural gas. For example, 93% of new electricity generation capacity that will come online in the next two years will use natural gas to fuel generation.

This emphasis on natural gas as the way to achieve air quality improvements without dramatically increasing power generation costs has had the unforeseen consequence of reducing the resiliency of natural gas markets. Regulatory mandates have reduced our ability to apply the lessons of portfolio diversification to our energy choices. This is a very high price to attach to the environmental amenities of improved air quality, air quality that could conceivably have been achieved through other means if environmental regulations had not specified natural gas as the fuel input.

The potential implementation of the Kyoto Treaty exacerbates this costly balkanization of fuel portfolios. Even if the U.S. does not ratify the treaty, Canada’s implementation of it would have a significant impact on the U.S. market as well. Canadian electricity generators would have to substitute into natural gas as they reduce their use of coal to meet the carbon dioxide reduction targets. If Canadian demand for natural gas increases to fuel its own power needs, then barring a substantial and unlikely increase in Canadian drilling and recovery, there will be much less Canadian natural gas available for export to the U.S. Most of our imported natural gas comes from Canada, both nationally and in the Midwest, so the dislocation to the U.S. natural gas market would be acute.2

Natural gas and the Midwest

At a June 26, 2003, conference sponsored by the U.S. Department of Energy, Secretary of Energy Spencer Abraham warned that tight natural gas supplies would translate into a 20% jump in home heating bills in the Midwest for the coming winter.3 This would mean that the average heating bill for the November through March “official heating season” would rise to $915. Even more worrisome is that such an estimate is based on normal weather conditions. A colder than normal winter would drive demand and prices even higher.

Since the secretary’s announcement, natural gas conditions have improved. The combination of increased drilling activity, mild summer weather, and some demand decreases and fuel switching by large industrial users have improved the supply balance, allowing for significant injections of natural gas into underground storage. By mid-July, estimates of working gas in storage stood at about 13% below the previous year.4 However, a return of warm weather could reverse this trend toward replenishing stocks if gas is needed for electricity generation. Similarly, gas prices as reflected by the futures contract on the New York Mercantile Exchange have fallen 25% since early June highs to around $5 per million Btus (British thermal units).

However, the secretary’s analysis points to one of the fundamental differences between the use of natural gas as a fuel in the Midwest versus the rest of the nation. While much of the gas supply problem during the summer has been blamed on the increasing use of natural gas to fuel electricity generation, in the Midwest, natural gas is disproportionately used for residential service and particularly home heating. As figure 1 demonstrates, per capita residential use of natural gas for the Seventh District is nearly twice the U.S. average. Thus, high gas prices will become particularly noticeable to Midwest consumers with the onset of winter. Also notable is the heavy usage of natural gas for industrial purposes in Indiana and Iowa. Many analysts have suggested that natural gas used for industrial purposes will be among the first to feel the effects of higher prices. Industrial customers are often more exposed to wholesale prices, and price spikes often lead to plants reducing activity or shutting down altogether. Industries such as aluminum, petrochemicals, plastics, and fertilizers are particularly vulnerable and, with the exception of aluminum, these industries do have a significant presence in the Midwest. As increasing natural gas prices raise production costs, some of these costs are likely to be reflected in the prices of fertilizers, chemicals, plastics, metals, and the products that use them as inputs, such as agricultural products.

1. Natural gas consumption per capita, 2001

| Residential | Commercial | Industrial | Vehicle | Electricity | Total | |

|---|---|---|---|---|---|---|

| (--------------------cubic feet in thousands--------------------) | ||||||

| Illinois | 34.39 | 15.23 | 22.33 | 0.02 | 3.58 | 76.44 |

| Indiana | 24.33 | 12.91 | 41.24 | 0.05 | 2.89 | 81.3 |

| Iowa | 24.29 | 15.69 | 31.63 | 0.01 | 1.97 | 73.59 |

| Michigan | 34.58 | 17.49 | 22.52 | 0.02 | 13.59 | 88.40 |

| Wisconsin | 23.36 | 14.25 | 24.73 | 0.03 | 4.17 | 66.54 |

| Midwest | 30.34 | 15.35 | 26.60 | 0.03 | 6.13 | 78.81 |

| U.S. | 16.97 | 10.79 | 26.16 | 0.05 | 19.73 | 80.79 |

The one limited positive for the Midwest is the relative underutilization of gas for power generation. As figure 1 shows, gas use for electricity per capita in the region is less than one-third the U.S. average. The region’s historical use of coal and nuclear fuel for power generation has tended to limit the use of natural gas for electricity. Given this historical investment in other generation assets, spikes in natural gas prices during the summer months will have less of an impact on consumer electricity prices in the region. But the seasonal effect of winter weather on natural gas prices in the Midwest remains important because Midwest consumers rely heavily on natural gas for heating.

Gas prices in the Midwest

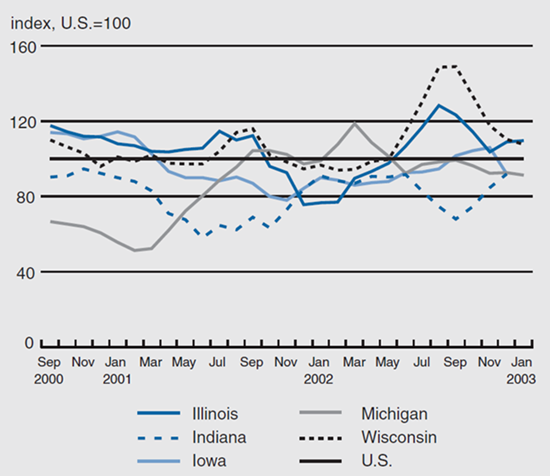

Gas prices (as measured by price paid in dollar per thousand cubic feet at the city gate) have exhibited considerable volatility both nationally and locally. However, with a few notable exceptions, Midwest gas prices tended to be lower than the U.S. average during the period September 2000 to October 2002 (see figure 2.) The region has benefited from its relatively lower reliance on natural gas in the summer months, and in 2001–02 a relatively mild winter lowered demand.

2. City gate gas prices, 3-month moving average

Storage and transmission

Storage capacity is an issue in some of the Midwest states. For example, Wisconsin has virtually no storage capacity, and storage capacity in Indiana amounts to only 43 days of average usage. Storage capacity is greater in Illinois (165 days of average usage), Iowa (242 days), and Michigan (264 days—however, by February 2003 Michigan’s storage level had fallen to 51% of capacity). Michigan needs a significant level of storage capacity because interstate pipeline capacity is limited, with the existing pipelines running at 95% of capacity. Without significant storage, out-of-state gas may be unavailable because of pipeline limitations. Available pipeline capacity is better in Illinois (75%), Iowa (55%), and Wisconsin (60%). Storage is a significant concern in Indiana, where pipeline capacity runs at 91% and current storage capacity is slim.5 The last major pipeline expansion in the region was the addition of the Alliance pipeline between British Columbia, Canada, and Joliet, IL, in 2000. Since then, most additional pipeline capacity has focused on moving natural gas from the Chicago hub to markets in southern Wisconsin and northeastern Illinois.

Recommendations

Further deregulation that would make energy markets more robust and resilient would help stabilize natural gas prices and provide some certainty to Midwest businesses and homes that consume natural gas. One frequently cited recommendation this summer has been to remove existing obstacles to fuel substitution and to the importation of LNG. In fact, retooling existing petroleum terminals to take some small LNG imports would be a low-cost first step toward creating integrated global natural gas markets. Imported LNG is more realistically seen as a long-run move, furthering the resiliency and global integration of natural gas markets.

Regulatory obstacles that constrain supply, including limitations on LNG terminal construction, exploration and drilling on federal lands, and offshore exploration and drilling, should be evaluated and subjected to a thorough cost–benefit analysis. This test would ensure that the combined environmental benefits of the regulations and the fuel supply benefits would outweigh the costs, including the opportunity costs of the foregone environmental and fuel supply benefits.

On the natural gas demand side, our approach to air quality regulation relies too heavily on natural gas. Too much air quality regulation mandates inputs, such as the use of natural gas or a particular coal emission scrubbing technology. An air quality regulatory framework that stipulates air quality objectives and enforcement technologies that regulators will employ would provide better incentives to apply technological change in decreasing both emissions and fuel use. Setting outcome-based air quality performance standards and introducing a transparent means of evaluating and enforcing performance would provide polluters with the flexibility to improve and innovate to find better ways of meeting the performance standard. This innovation would reduce costs and produce new technologies. New knowledge could enhance our ability to achieve higher air quality and make available different fuels at prices we are willing to pay.

Another constructive action governments could take to make energy markets more resilient would be to change state-level electricity regulations to allow retail competition and demand-side bidding in retail markets. An active demand in retail electricity markets would not only discipline the ability of suppliers to raise prices, it would also equip consumers with their most effective energy conservation tool. Demand response, particularly in large industrial and commercial customers, can send signals to power producers of how much investment in generation they should undertake. Conservation and shifting of demand away from costly peak hours can actually decrease the amount of required investment in generation capacity, as well as reducing overall fuel use.

Price increases, such as those seen recently in natural gas, transmit valuable information to consumers. That information enables them to decide when it is worth it to them to conserve. Price increases serve as the most effective inducement to conservation, because they signal to consumers large and small that the relative value of natural gas has increased. They also tell suppliers when it is worth bringing more to market and when to invest in more capacity, and through this interaction across time and place, fuel portfolios become more certain and prices become more stable. Most importantly, timely price information can help fashion appropriate (cost–benefit) public policies with respect to the environment, infrastructure, and regulation.

Notes

1 The Midwest is defined here as the states of the Seventh Federal Reserve District—Illinois, Indiana, Iowa, Michigan, and Wisconsin.

2 In 2001, 99.5% of all imported natural gas to the U.S. by pipeline originated in Canada. This represented 109.2 billion cubic meters or roughly 18% of U.S. consumption (BP Statistical Review of World Energy, June 2002).

3 Melita Marie Garza, 2003, “Energy chief warns of 20% jump in Midwest heating bills,” The Chicago Tribune, June 27.

4 Energy Information Administration, 2003, Weekly Natural Gas Storage Report, July 18.

5 Underground gas storage capacity and pipeline capacity, December 2001.