We use a model based on the historical relationships between unemployment, inflation, and recessions, along with the Summary of Economic Projections (SEP) from the Federal Open Market Committee (FOMC),1 to examine the medium-term implications of current and projected unemployment rates for the U.S. economy. Our model predicts a low probability of a recession in the next two to three years based on SEP forecasts for additional labor market tightening over this horizon.

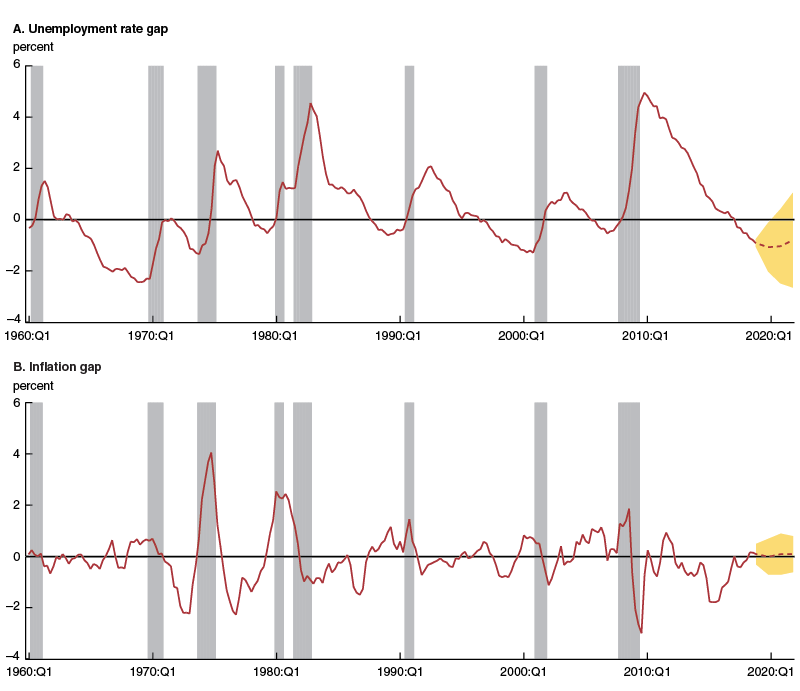

The difference between the unemployment rate and its “natural” rate—referred to as the unemployment rate gap—is commonly used to measure the amount of slack in the labor market. The natural rate captures the full employment potential of an economy. Like the unemployment rate, it may vary over time because of a variety of factors (such as changes in demographics, educational attainment, and unemployment insurance). The unemployment rate gap represents a point-in-time measure of labor market utilization. A positive gap implies an underutilized labor market, where unemployment is above the level consistent with full employment. Conversely, a negative gap implies a tighter labor market, where firms must compete for less readily available resources, leading to faster increases in wages and prices.2

At 3.8% in the third quarter of 2018, the U.S. unemployment rate was somewhat below its natural rate of 4.6% as estimated by the Congressional Budget Office (CBO),3 suggesting a moderate degree of tightness in labor markets. For perspective, the time series of the gap since 1960, along with U.S. recessions as identified by the National Bureau of Economic Research (NBER), is shown in panel A of figure 1. Historically, the gap has reached its lowest point in the business cycle (i.e., its cyclical trough) an average of three quarters before the beginning of a recession, with a range from zero to six quarters based on the eight recessions since 1960. The reversion to the mean that occurs just in advance of recessions evident in panel A is sometimes used to suggest that tight labor markets predict recessions.4 Underlying this hypothesis is the idea that these periods characterized by tight labor markets correspond with times when inflation is rising, prompting tighter monetary policy that results in slower growth and higher unemployment.

1. Unemployment rate and inflation gaps

Sources: Authors’ calculations based on data from Haver Analytics; and the Federal Open Market Committee, 2018, Summary of Economic Projections, Washington, DC, September 26.

In this Chicago Fed Letter, we develop a model for U.S. recessions that captures this notion, based on the historical relationships between the unemployment rate, inflation, and recessions. We then use this model and the Federal Open Market Committee’s Summary of Economic Projections to examine the medium-term implications of the unemployment rate gap for the U.S. economy.

The unemployment rate gap, inflation, and recessions

To quantify the joint dynamics of unemployment, inflation, and recessions, we use an endogenous switching regression model. Specifically, we estimate the probability of a recession in a given quarter based on 1) the current change and prior level of the unemployment rate gap according to a probit specification and 2) the differences during economic expansions and recessions in the level and slope of the Phillips curve—i.e., the correlation between the unemployment rate gap and detrended inflation according to the Price Index for Personal Consumption Expenditures (PCE).5 The time series of the latter, referred to as the inflation gap, can be seen in panel B of figure 1. Finally, we allow for correlation in the unobserved drivers of our probit specification and the Phillips curve, but restrict the form it can take to facilitate the estimation of the model. Further details can be found in the accompanying technical appendix.6

The probit side of our model suggests two things about recessions and the unemployment rate gap. First, the larger the quarter-to-quarter increase in the gap, the higher the likelihood that the economy is in recession. Second, the more negative the initial reading of the gap, the more likely a recession might ensue in the subsequent quarter. In other words, the model assigns a very high probability to a recession developing whenever it sees large increases in the gap from very low levels. In this sense, it should allow us to quantify the importance of the mean-reverting property of the unemployment rate gap, which has often been cited as leading evidence of a recession.

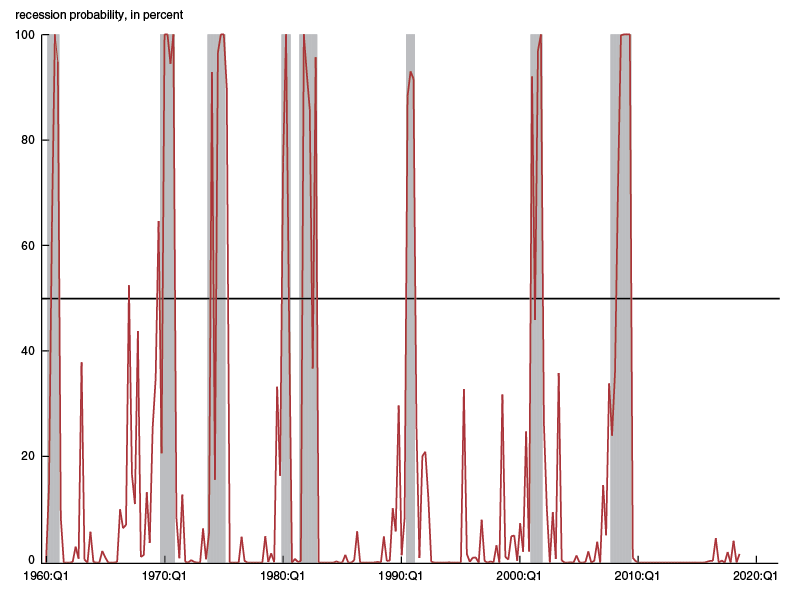

To address the accuracy of the model in this regard, we produce the model’s fitted probability for historical U.S. recessions, shown in figure 2. The close visual correspondence between the level of this probability and the dark gray regions indicating NBER recessions is verified by the fact that the fitted probability is 97% accurate in separating expansions from recessions using the nonparametric classification method of receiver operating characteristic (ROC) analysis.7 This level of accuracy puts it on par with well-known coincident indicators of recessions for the U.S. such as the Chicago Fed National Activity Index (CFNAI).8 Like any model, however, its predictions are not perfect. For example, it produces two false positive recession signals (i.e., recession probabilities greater than 50% during an expansion), as well as several false negative signals (i.e., recession probabilities less than 50% during a recession), as shown in figure 2.

2. Model’s fitted probability for historical U.S. recessions

Source: Authors’ calculations based on data from Haver Analytics.

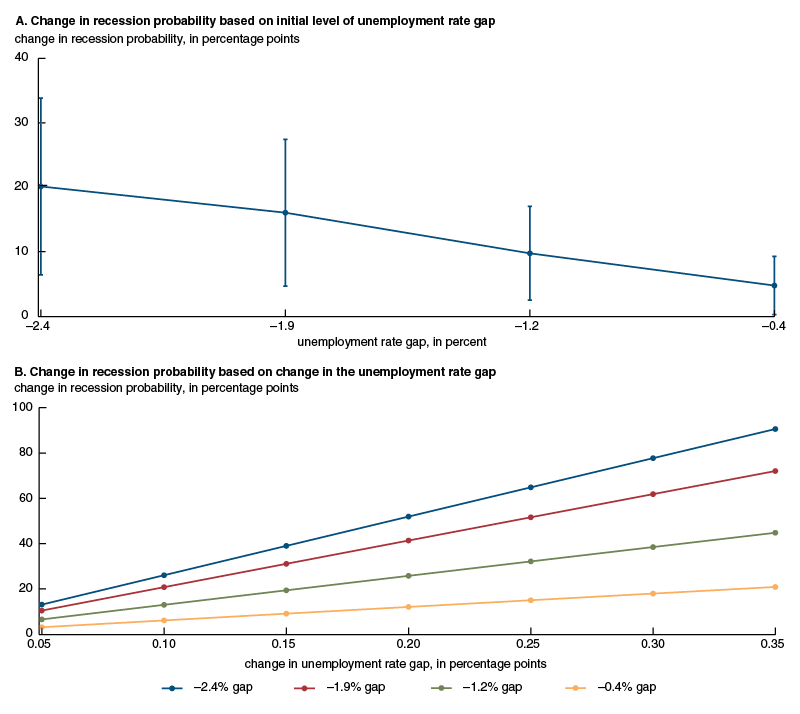

To understand the extent to which the model predicts an increasing likelihood of recession in a tightening labor market, we next examine the marginal effect of varying the level of the unemployment rate gap on the probability of a recession, shown in panel A of figure 3.9 At one extreme, a level of the gap equal to –2.4%, roughly equal to the lowest observed gap in our sample before a recession, leads to an increase in the likelihood of a recession of 20 percentage points. At the other extreme, a level of the gap equal to –0.4%, roughly equal to the highest observed gap in our sample before a recession, is associated with an increase in the likelihood of a recession of about 5 percentage points.

3. Marginal effects of the level and change in the unemployment rate gap on the probability of a recession

Source: Authors’ calculations based on data from Haver Analytics.

The current change in the unemployment rate gap plays an important role in predicting the transition from a period of economic expansion to recession for a given initial level of the gap, as shown in panel B of figure 3. For instance, with a gap of –0.4%, we estimate that an increase of 0.35 percentage points would raise the likelihood of a recession by about 20 percentage points.10 If the level of the gap is instead roughly triple in size at –1.2%, a 0.35 percentage point increase in this case would raise the likelihood of a recession by a little more than 40 percentage points.

The probit model’s identification of this transition is also aided by the differences in the levels and slopes of the Phillips curves that we estimate separately for expansions and recessions. On average, periods of expansion are associated with below-trend readings of PCE inflation, or, equivalently, negative readings of the inflation gap. In contrast, readings of the inflation gap are positive, on average, during recessions. For both expansions and recessions, we estimate small negative slopes in the Phillips curves, suggesting that a tightening labor market leads to modest upward pressure on inflation (and a loosening labor market leads to modest downward pressure on inflation). However, the slope of the Phillips curve that we estimate for recessions is roughly four times the slope that we estimate for expansions.11

Taking all of these factors into account, our model currently indicates a negligible likelihood that the economy is in recession, as seen in figure 2. The reason for this is twofold: 1) PCE inflation, at 2.2% in year-over-year terms in the third quarter of 2018, is only slightly above the Federal Reserve’s 2% inflation target that we equate with trend inflation, and 2) recent movements in the inflation and unemployment rate gaps are highly consistent with the very flat Phillips curve that we estimate for periods of economic expansions.

Monetary policy and the Summary of Economic Projections

Absent in the discussion so far is the critical role played by monetary policy in shaping both unemployment rate and inflation gaps and their impact on the likelihood of a recession. To address the role of monetary policy, we extend the predictions of our model beyond the end of its sample period in the third quarter of 2018 by conditioning it on the FOMC’s September 2018 Summary of Economic Projections.12

We use the median projections of the unemployment rate and PCE inflation through the end of 2021 and over the longer run (the latter for the natural rate and inflation trend13) to obtain predictions for both gaps.14 The expected paths for the gaps can be seen in the dashed red lines in both panels of figure 1. To account for uncertainty in the unemployment rate and PCE inflation projections, we use the historical forecast errors from the SEP to construct the 70% confidence intervals in the figure.

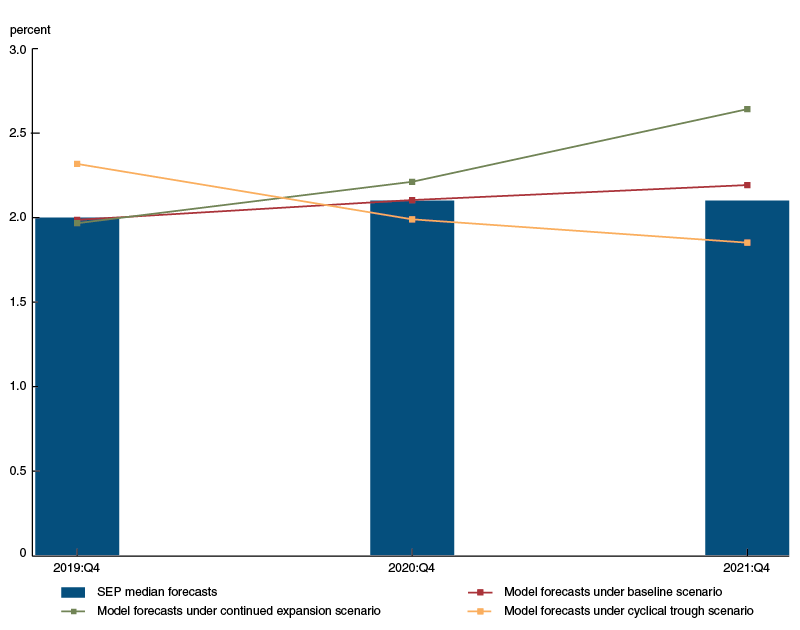

The SEP presents each FOMC participant’s views on appropriate monetary policy. Based on these views, each participant submits projections for the unemployment rate and inflation for the next three years (and over the longer term). Thus, we can evaluate whether or not the SEP median forecasts for unemployment and inflation are in agreement with historical data and our estimated model. We do this by comparing the level of inflation our model would expect given the SEP median forecasts for the unemployment rate gap against the actual SEP median forecasts for inflation.15

This comparison can be seen in figure 4. Current SEP median forecasts for PCE inflation are indeed largely consistent with our model (i.e., the “baseline scenario” shown in figure 4). To generate more inflation based on the tightness of the labor market, our model would require a much lower level for the unemployment rate gap than the SEP median forecasts or a much higher probability of a recession (recall that the estimated slope of the Phillips curve is steeper in this case). Under the baseline scenario, our model predicts a gradually increasing recession probability (not shown) over the forecast horizon (peaking at about 15% in early 2021).

4. Projections for PCE inflation

Sources: Authors’ calculations based on data from Haver Analytics; and the Federal Open Market Committee, 2018, Summary of Economic Projections, Washington, DC, September 26.

To illustrate the sensitivity of this result, we also include two alternative predictions based on the SEP forecasts in figure 4. In the first one, we use the lower end of the 70% confidence interval shown for the unemployment rate gap in panel A of figure 1, which we refer to as the “continued expansion scenario” in figure 4. Doing so has only small effects on the model’s prediction for inflation in 2019, consistent with the small negative effect of the level of the unemployment rate gap on the probability of a recession and the small estimated slope of the Phillips curve during expansions. However, the lower level of the unemployment rate gap starts to have an impact on our inflation forecast by 2020, as a higher probability of a recession (peaking at just over 20% by the end of 2021) leads to a steeper slope of the Phillips curve, raising our inflation forecast 0.1 percentage points above that of our baseline scenario in 2020 and 0.4 percentage points in 2021.

In the second scenario, which we refer to as the “cyclical trough scenario” in figure 4, we instead use the upper end of the 70% confidence interval for the unemployment rate gap from figure 1, panel A. Here, a shrinking unemployment rate gap leads to a higher probability of a recession (peaking at roughly 35% in early 2019 and steadily declining to just under 10% by the end of 2021), which causes our PCE inflation projection for 2019 to be 0.3 percentage points higher than that of our baseline scenario. Under the cyclical trough scenario, PCE inflation then reverses in 2020 and 2021 once the unemployment rate gap turns positive, resulting in predictions for inflation that are below those of our baseline scenario by 0.1 and 0.4 percentage points, respectively.

Conclusion

While tight labor markets have preceded recessions in the past, on their own they do not necessarily signal the end of an expansion, as reflected in our model and the SEP forecasts. The current level of the unemployment rate gap suggests a very low probability of a recession based on the historical relationships between the gap, PCE inflation, and recessions captured in our model. Furthermore, when conditioned on the SEP forecasts for the unemployment rate gap over the next three years, our model suggests very little risk of a more rapid increase in inflation arising from a tightening labor market than what is already suggested by the SEP median forecasts for inflation. While this result is somewhat sensitive to model assumptions, plausible alternative scenarios incorporating the SEP’s historical forecast errors continue to point to a significant likelihood of a “soft landing” for the labor market and inflation over the next two to three years.

1 The FOMC is the monetary policymaking arm of the Federal Reserve System.

2 This is often referred to as the “natural rate hypothesis” and attributed to Milton Friedman and Edmund Phelps.

3 More information on the CBO’s measure of the natural rate of unemployment is available online.

4 For example, Boston Fed economists find that since 1949 a 0.5 percentage point increase in the unemployment rate has always coincided with the start of a recession and that this tends to occur when the unemployment rate gap is negative; their recent research is available online.

5 The original Phillips curve relationship described the statistical correlation between the unemployment rate and wage growth. Our use of the correlation between the unemployment rate gap and detrended inflation instead is meant to proxy for modern refinements of the Phillips curve capturing supply-side constraints on labor market dynamics, nominal price and wage rigidities, inflation expectations, and inflation-targeting monetary policy. We obtain the PCE inflation trend with the Hodrick–Prescott filter. However, once the long-term trend settles at 2% in 2002:Q4, we hold it fixed at this level.

6 The technical appendix is available online.

7 For further details on this method, see Travis J. Berge and Òscar Jordà, 2011, “Evaluating the classification of economic activity into recessions and expansions,” American Economic Journal: Macroeconomics, Vol. 3, No. 2, April, pp. 246–277. Crossref

8 More information on the CFNAI is available online.

9 More accurately, we examine at what trough level of the gap we are likely to see a substantial increase in the probability of a recession, as we assume that the current change in the unemployment rate gap is 0 percentage points and the lagged change is –1 percentage point.

10 For perspective, a quarterly increase of 0.38 percentage points represents the 90th percentile of the distribution of quarterly changes in the gap since 1960.

11 See the technical appendix (mentioned in note 6) for the estimated coefficients of our model.

12 More information from the September 26, 2018, Summary of Economic Projections used in this article is available online.

13 We associate the SEP median longer-run projection for unemployment with the natural rate. Also, we associate the SEP median longer-run projection of 2% for total PCE inflation with the inflation trend; see the technical appendix (mentioned in note 6).

14 The SEP only provides fourth quarter values. To arrive at intermediate values in each year, we assume a smooth linear transition between the fourth quarter values of consecutive years. For the natural rate, we also use a smooth linear transition from the CBO estimate of 4.6% in 2018:Q3 to the SEP longer-run estimate of 4.5%.

15 To be able to make this comparison, we also have to assume a path for the recession indicator variable and the inflation gap in order to estimate the probability of a recession over the SEP forecast horizon with our model. For the former, we assume a baseline no-recession scenario consistent with the SEP median forecasts for real gross domestic product growth; and for the latter, we use the SEP median forecasts for inflation. However, we hold fixed all of the Phillips curve and probit coefficients of the model at their previously estimated values, such that the SEP forecasts are only allowed to alter the estimated covariance matrix of the model’s shocks. This process ensures that our model’s predictions for the inflation gap reflect only the additional information on the likelihood of a recession over the next three years provided by the SEP.